HDFC Group is coming out with its first IPO in 22 years with HDFC Life. Issue opens on Nov 7th and here are my notes.

Why Insurance is a Good Business?

National Pension System (NPS)

The Govt wants to popularize the pension scheme and move India towards a pension society. A CRISIL Research study on the need to build pension net indicates that the number of people aged over 60 in India will triple from 112 million in 2014 to 300 million by 2050. A very few people (8% as per report) only receive a formal pension and thus there is a huge gap to be met.

There are many sub schemes in this NPS like: Central Government Plans, State Government Plans, NPS Lite (Swavalamban) Plans, Atal Pension Yojna, TIER I and TIER II plans. NPS is mandatory for Central/State Govt staff, PSUs, etc. Over the years, the Govt has made the NPS attractive by offering additional Rs 50,000 tax breaks, 40% tax free withdrawal, high equity allocation, tax breaks for employers, etc. I’m a NPS subscriber for around five years and the present NPS is much better than what it was in the past. It might get better in the future and much attractive.

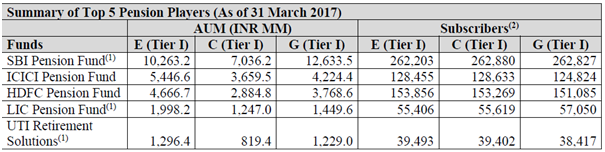

In 2012, they established their wholly-owned subsidiary, HDFC Pension, to operate our pension fund business under the NPS. HDFC Pension is the second largest private pension fund management company in India in terms of AUM and subscribers in Fiscal 2017 after ICICI Prudential Pension Fund.

NPS AUM is increasing every year much like mutual funds inflows and likely to grow further. HDFC Pension’s AUM as on March 31, 2017 stood at Rs 1,163.0 with a growth of 209%. ICICI Prudential Pension Fund’s AUM increased by 106% at Rs 1,441 Cr.

The CEO of HDFC Life has commented on this that:” While the private sector fund managers do not have access to the government funds as yet and it is a restriction, this subsidiary has performed well. HDFC Pension gets almost 50 percent of the corporate NPS subscribers and has been increasing our market share. The company is at the second position on the private side and if the flows continue as they are, it should be number one on the private side by the end of this year. This is despite us being a late entrant by four years and had a case going in Supreme Court which we won. It is still early days and there is huge opportunity. It also feeds well into the annuity business of the insurance company and are building it up slowly.”

HDFC Pension Fund is among the best performing fund and recently even I’ve changed my fund manager to HDFC Pension recently. You may check the fund manager’s performance here.

NPS subsidiaries are loss making and fee income is low now but the opportunities is high and the fee structure and management expense ratio has gone up over the years.

Annuity Business – Pension Products

Annuity is an insurance product where the insurer receives a lumpsum amount which is paid to the policy holder till he is alive. There are many variants available and based on the variant, the payout would differ. Annuity rates in India offered by insurance companies are very low. LIC offers the best rates and it is 8.39% for a 60 year person. If the policy holder dies, then there would be no payout. Thus the longevity risk is passed on to the insurer. It is a great product for both the insurer and the insured and I think

by far the biggest float generating product.

Why is this product important? Well, the Rs 206,331 Cr AUM of NPS (as on 31st Sep 30, 2017) will find its way to annuity. NPS has a minimum 40% allocation requirement to annuity which is compulsory and 80% allocation for premature withdrawal. Since only 40% of NPS corpus would be tax free, subscribers would allocate 60% for annuity products.

NPS was compulsory for people joining the Govt workforce since last 7-8 years only so in the next decade or two later we would have huge annuity take off waiting.

A TIP or a Term Insurance Plan – Protection Plans Opportunities

A term insurance plan is a “protection” product and it is a high margin business. Here the policy holder pay fixed sum every year for the entire policy tenure. People mostly take policy till 60 years (retirement age) whereas we know that the life expectancy is going up. Insurers mostly issue till 70 years or so. The higher the policy tenure, higher the premium.

We all know how the word “SIP” became famous and people think it is a product by itself. Now we are hearing the word- “TIP” or Term Insurance Plan. See this article from VRO.

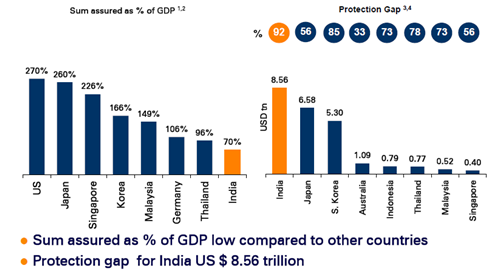

India has the highest protection gap in the region, as growth in savings and life insurance coverage has lagged behind economic and wage growth. Protection gap has increased over 4x in last 15 years with significantly low insurance penetration and density.

HDFC Life is having the highest protection policies as percentage of new business. For FY17, the protection policies share is 21.6% of new business. All the life insurers that I track are focused on improving the mix of protection plans.

Health/Critical Illness cover and Cancer cover are also protection plans. HDFC Life was among the first to introduce a cancer cover and they intend to grow these policies even further.

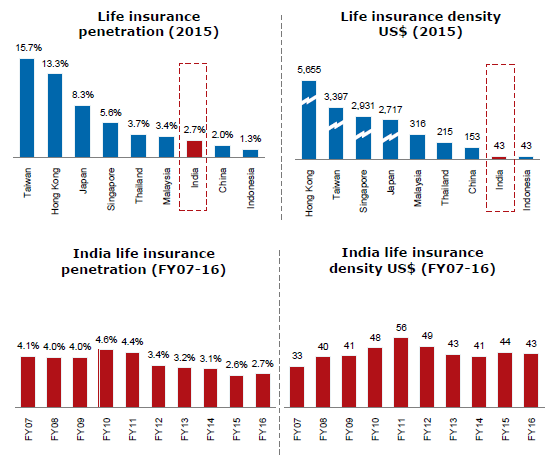

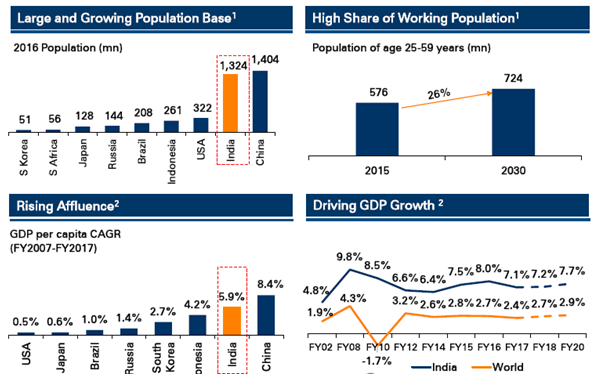

Low Penetration, favorable demographics

There is ample scope for covering more lives under insurance. We are the second most populous country with high working population, rapid urbanization and rising affluence.

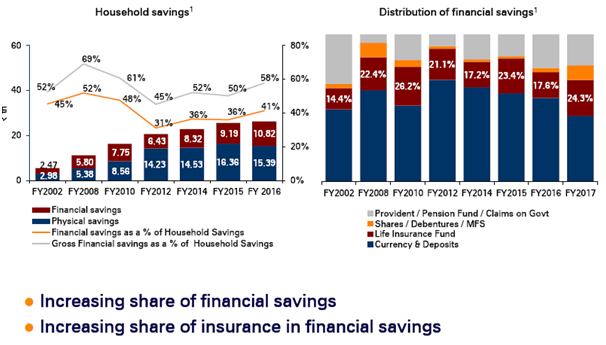

Financialization of assets

The present Govt has favored digitization and financialization of assets. Some portion of savings has found its way to insurance post demonetization. Govt. has introduced in 2015 a group term insurance plan called: Pradhan Mantri Jeevan Jyoti Bima Yojna Plan which offers Rs 2 lakh life cover for Rs 330/year.

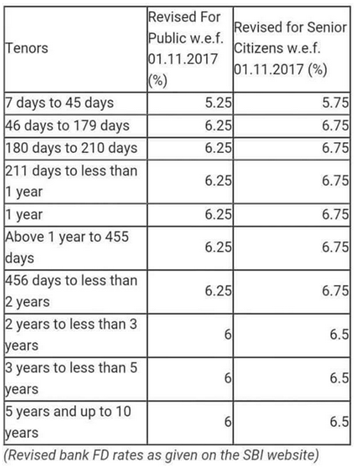

Bank FD rates are going down, most banks now offer 3.5% interest rates on SB account, small savings rates are going down, etc. The biggest beneficiary of this is equities and mutual funds but some amount have come to life insurance too. Latest SBI FD rates:

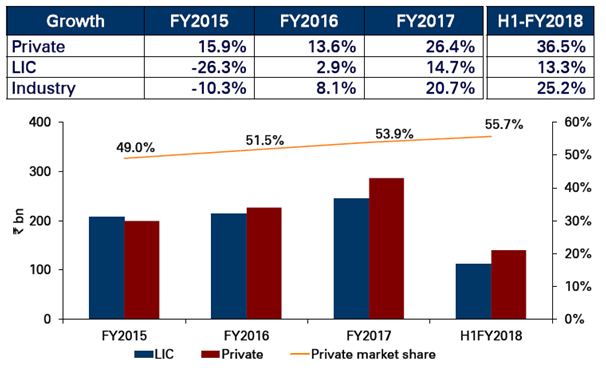

Improving market share of private insurers

Like how the private banks were able to improve market share, be profitable and give better service over the past 15-20 years, the same thing has been playing out in the insurance space. LIC is almost continuously loosing market share to private players.

Capital Intensive Business with good ROE

Insurance business is capital intensive and thus it might not be easy for new players to start one. However once the solvency margin is above the required 150%, it does not take much capital to grow. The return ratios are good. The ROE stands at 25.7% and ROIC stands at 41%. The average ROE for HDFC Life from FY15-17 stands at nearly 30%.

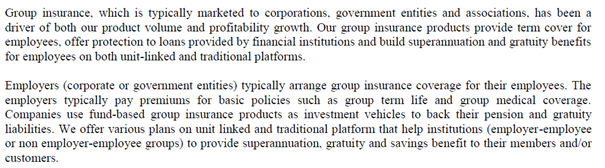

Credit Life Products

Credit Life products are issued to banks/financial institutions to cover full or partial repayment of outstanding loan amounts in the event of death, disability or illness. Beneficiaries of our Credit Protect products can apply the payouts from such products towards full or partial repayment of outstanding loan amounts in the event of death, disability or illness of the relevant individual borrowers. No benefits will be paid in the event of a loan default. Credit Protection plans of late has been pushed by lenders while giving home loans and other credit.

It may be mandatory to obtain insurance forgetting home loans, etc. SBI Life states this:

![]()

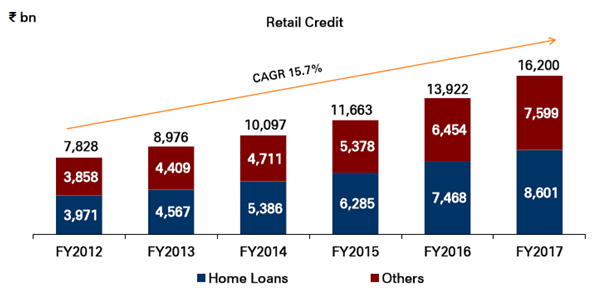

Loans where credit life insurance can be sold has shown an uptick:

Why HDFC Life is a Good Insurance Company

Better Product Mix

Unlike ICICI Pru Life or even SBI Life, the product mix is balanced and not skewed towards ULIPs. ULIPs: 52%, Traditional Par: 35%, Traditional non par:13%. On basis on APEs, protection plans account for 21.8% of total premium.

HDFC Life is able to consistently increase the share of protection products, which are high margin, as observed below:

High Group business Premium

HDFC Life has the highest group business premium. As high as 50% of new business premium. Here is what the management said in their IPO prospectus:

An interesting thing is they have a very strong non-traditional channels to sell their protection plans like JetPrivilege. Taken from Jet Airways/JetPrivilege site:

Innovative (and high margin?) Products

They recently launched a protection plan - HDFC Life Click 2 Protect 3D Plus which refers to a feature of the plan which it provides cover for 3Ds – Death, Disease, and Disability. Hence, it is nothing but the Term Insurance clubbed with accidental and critical illness disability riders. There is also option to cover our life for the whole life!

Term + Health Insurance Combo cover

Click 2 Protect Health covers both life and health. Health insurance is done by Apollo Munich health insurance company. This offers operational convenience to the policy holder in the way that there will be only one medical test, single form, 5% discount, etc.

Strong Bancassurance Partners and Investment Float

Bank sponsored life insurers have an edge over the other players mainly due to the good distribution network. HDFC is a trusted brand name which aids its business further. Moreover HDFC Bank is retail focused bank where they might be able to cross sell products to their customers. Banca is an important channel and HDFC Life is able to increase the banca partners over the years:

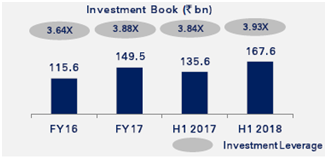

Also there is no need to emphasis on the “float” that an insurance company may generate. Investment yield for FY17 (on shareholders’ funds) is 12.7% without unrealised gains and 8% with unrealised gains for HDFC Life. Saw an interesting slide in ICICI Lombard presentation about the investment leverage (ratio of total investment assets to net worth) :

Risks

Heavy Competition

There are over 23 life insurers where you could cover your lives.

Mis-Selling

Insurance being a push product where there are commissions involved for the policies sold, there is bound to be mis-selling.

Open Banca architecture

Now an institution can sell products of three insurers. If HDFC Bank is selling other insurer’s product then the share of policy sold will come down. However we can argue that ICICI Bank can sell products of HDFC Life too. We need to wait and see how this pans out.

Variation in actuarial assumptions and reality

The assumptions of inflation, interest rate or mortality rate changes drastically from what was assumed then we have an altogether a different picture on the future profitability.

Natural Calamity and Disaster

Maharashtra, Gujarat, Karnataka, Tamil Nadu and Delhi accounted for 63.8% of the total received premium from new business premium for H1FY18. If there is an earthquake, flood or Tsunami affecting the region, then HDFC Life would have to pay out claim. This is mitigated to certain extent by having

re-insurance covers.

Please go through the IPO Prospectus of complete risks involved.

Comparison

I’ve posted my notes on the comparison of SBI Life, ICICI Pru Life and HDFC Life here: Life Insurance Companies - Comparison

My notes:

Life Insurance Cos -v2.docx (14.1 KB). Please note that this is NOT updated for H1FY18.

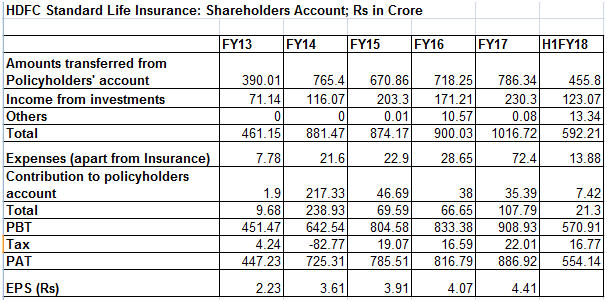

Financials

We can’t analyze insurance companies by normal methods since revenue-expense would not mean profits. Due to the long term contract nature of the insurance policies, the benefits/claim would be paid at a much later date or if the person survives, there won’t be any payout.

Actuaries, appointed by the insurance company, would make provisions and build models based on assumptions like future interest rates, mortality rate, Yield expected on investment and inflation assumptions. ICICI Pru Life are more conservative in their assumptions.

Valuations

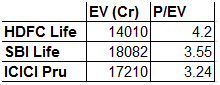

As per the latest CMP, these are how the insurers are trading:

I feel when the EV itself is growing around CAGR 16-18% with good visibility for the next 2-3 years, there is no point in looking at the EV multiples while investing. Moreover when there is assumptions involved and even the EV is calculated in different methods by insurers there is no point at looking at EV and investing. Investors felt ICICI Pru Life was overpriced at IPO however both SBI Life and HDFC Life is priced even higher so the goal post has changed in bull market?

This is a sunrise sector with fantastic opportunity so I would not mind investing in any of these three insurers. However, I feel ICICI Pru Life is one of the very few bargains left in this market to buy.

Disclosure: I’m not a SEBI registered analyst and this is not a recommendation to buy/sell. I’m going to apply for HDFC Life IPO and my family members will also apply. I own ICICI Pru Life and my family members own SBI Life and ICICI Pru Life.