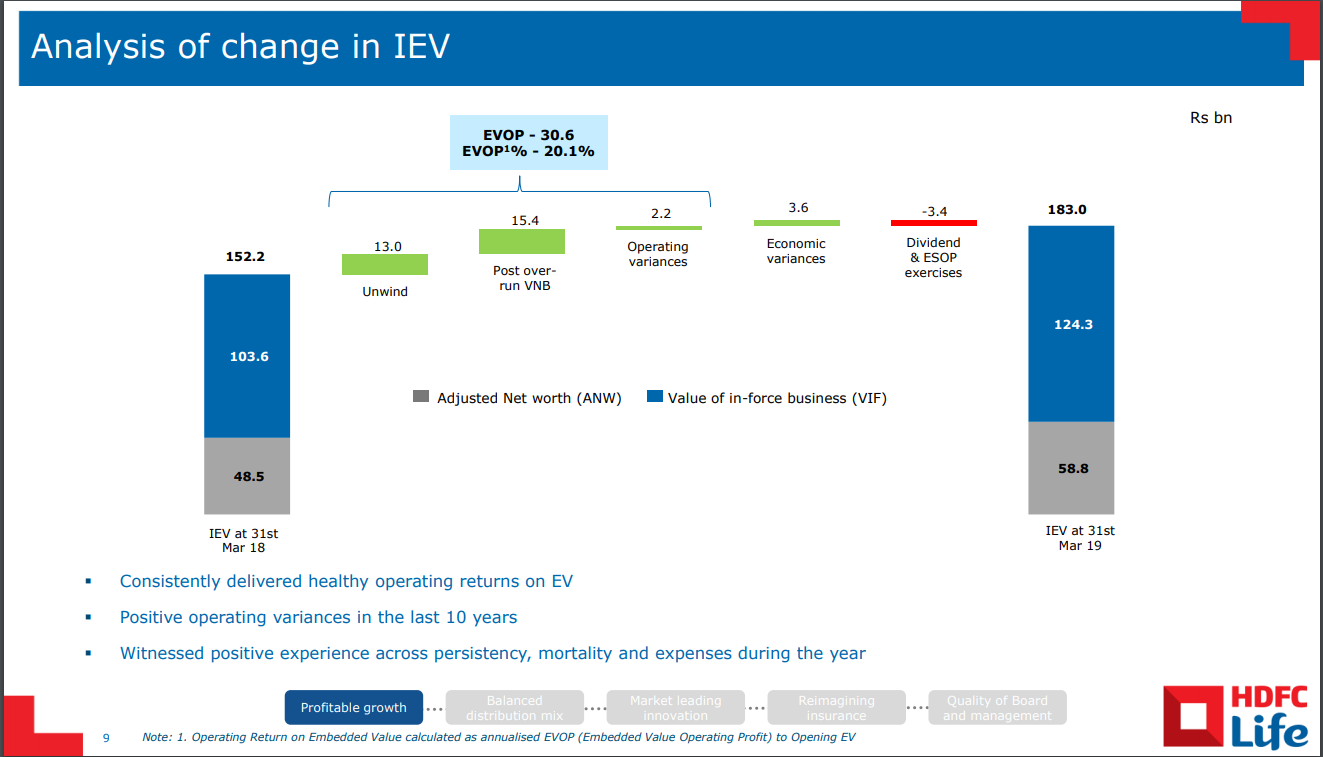

The “E” in P/E ration refers to earning power of the company with the time unit of one year.

In case of life insurance companies, earnings power comes from two sources -

- Back book profits - through unwind & operating variances (positive or negative)

- Value of New Business (VNB)

EVOP = Back Book Profits (Unwind + Operating Variances) + VNB

And hence P/EVOP is similar to familiar P/E ratio for life insurance companies.

Hope this helps.

Thanks , well explained

So current valuation is justified according to this analogy

Disclosure

Invested and positive on opportunities size

Ashit

how much is the valuation now ? say closing price is 480 and EVOP is 30.6…how do we calculate?

what will be the outcome if FDI is further open up in insurance? FM says they are willing to open in insurance intermediates…what does that mean?setting up insurance takes a lot of time…what does this have impact on existing players…any senior boarders views please?@rupeshtatiya

what are insurance intermediates government permitting

how much time it will take

how it going to damage India insurance industry

FDI in intermediaries will not damage the industry. It will increase insurance penetration in long run. It would benefit digitally ready insurance companies. Mostly digital intermediaries would get this FDI benefit. Although penetration would increase, which is exactly what government wants and rightly wants, not sure if insurance companies margins would be impacted as digital intermediaries may give big discounts, the burden of which will be taken by the FDI player and also somewhat by insurance company or by any other means. And if yes, then will the benefit of increased penetration more than compensate any small loss of decreased margins. Any thoughts on that?

Developed countries have large insurance penetration and share 10% of GDP; while in India its still around 3%. India is also on right track if they allow 100% FDI in insurance sector. These talks are going now since last 12 years.If it is allowed it will be very big boost. In some countries Insurance companies are bigger than banks. Number of insurance cos to open in future will be very very high, good for economy as well.

It means that many segments like insurance broking, Third Party admins etc will have 100% FDI. This would lead to more competition to sell insurance and good for insurance cos particularly general insurance where fintech should play a bigger role.

My personal take is that physical selling of insurance by foreign entities is not going to happen. how many 3rd party insurance brokers are there? And why will someone come in and setup distribution in India? Maybe it will help some of the lage fintech companies, so expect Amazon, Flipkart, Paytm etc to start selling insurance now.

Yes that s true, but what’s important for us is to know how will it impact life and general insurers…will they protect their margins and also if margins reduce, will increase in penetration compensate for that. Amazon can sell some brands at year long bug discounts while premium ones discount is limited time and money…if insurance were to become brands being sold at retail platforms then do they have the brand moat of say apple, jockey and 3 Ms where discounts are hard to find and still products sell…and lastly and most importantly with insurance being a unique product, will management have ability to derive benefit of moat in excess of margin reduction and discount selling, if at all it happens…and therefore my bet would remain with the best here…

Insurance is a curious business in my opinion. The product (or service) is pure commodity so it needs to be sold. yet, by its nature people tend to gravitate towards bigger and more trusted brands. I don’t think 3rd party intermediation will change anything. Just thing if a policybazar has made any difference to any insurance company? Moreover, the challenge for a fintech company is that it is also facing the challenge of direct online selling by the insurance companies themselves.

To summarise, I think, and I could be wrong, that all this is practically ignorable. Pure noise. Nothing meaningful will change.

The current and famous intermediatory is policybazaar(infoedge owns this), that will be benefitted out of this. There are other intermediatories such as coverfox, insurancedekho. Flipkart and Amazon are selling insurance for their products, whereas acko is selling their insurance as a product in amazon. So these e-com companies with deep pocket can be coming out with all guns blazing.

Amazon has invested in acko and hence they have vested interest in selling acko insurance.

Also Sir Insurance specially life insurance company will incur loss in case of mis-selling.If the product is not suitable for customer , they may stop paying premium soon. Its a loss for both insurer and Customer. Insurer will bear an upfront cost interms of fees paid to distributor benfit for insurance company start flowing gradually as year goes on. Also there is surrender policy set by IRDA where customer has to pay 3 years of premium (for 10 years or more insurance term) to get back something. So I also think …this type of distribution will have much of an effect.

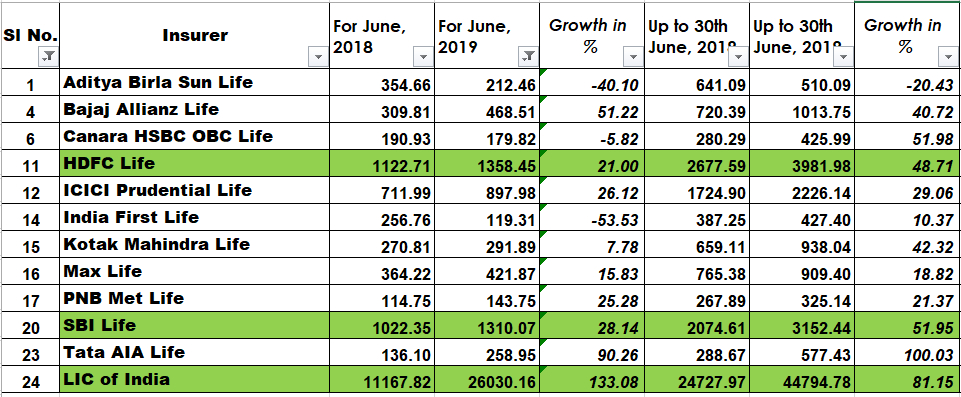

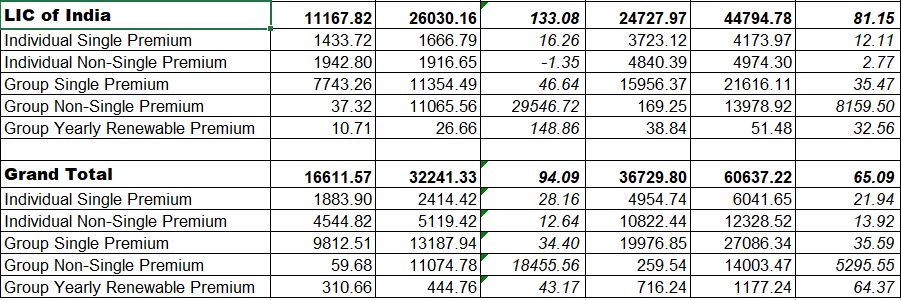

Good June numbers from HDFC LIFE. But look at LIC, are they gearing up for challenge from private sector? Not so sure as main growth seems to have come from Group - Non Single Premium just for the month of June.

This news is regarding General Insurance, not Life Insurance. Better post it in a GI thread.

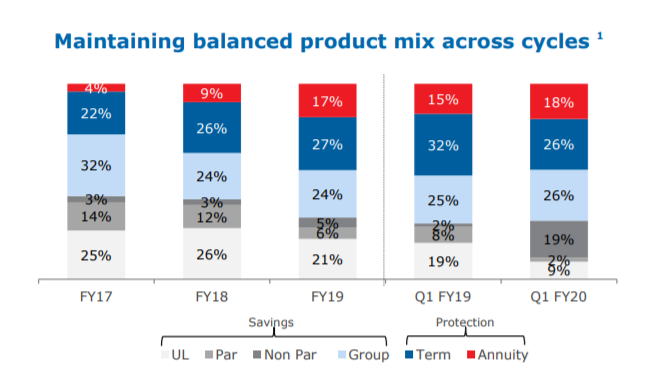

HDFC Life’s Q1 PPT was one of the most interesting PPT where they provided some texture of risk management philosophy & some other things.

This quarter’s product mix shows that Non Par Savings (primarily Sanchay) has gone from 2% in Q1 FY19 to whopping 19%. Non par savings was at 5% in FY19. The UL share was down at 9% in tandem with mayhem in markets but that has resulted in highest ever VNB margins for the company. The VNB grew a whopping 104%.

Now coming to the first risk management slide →

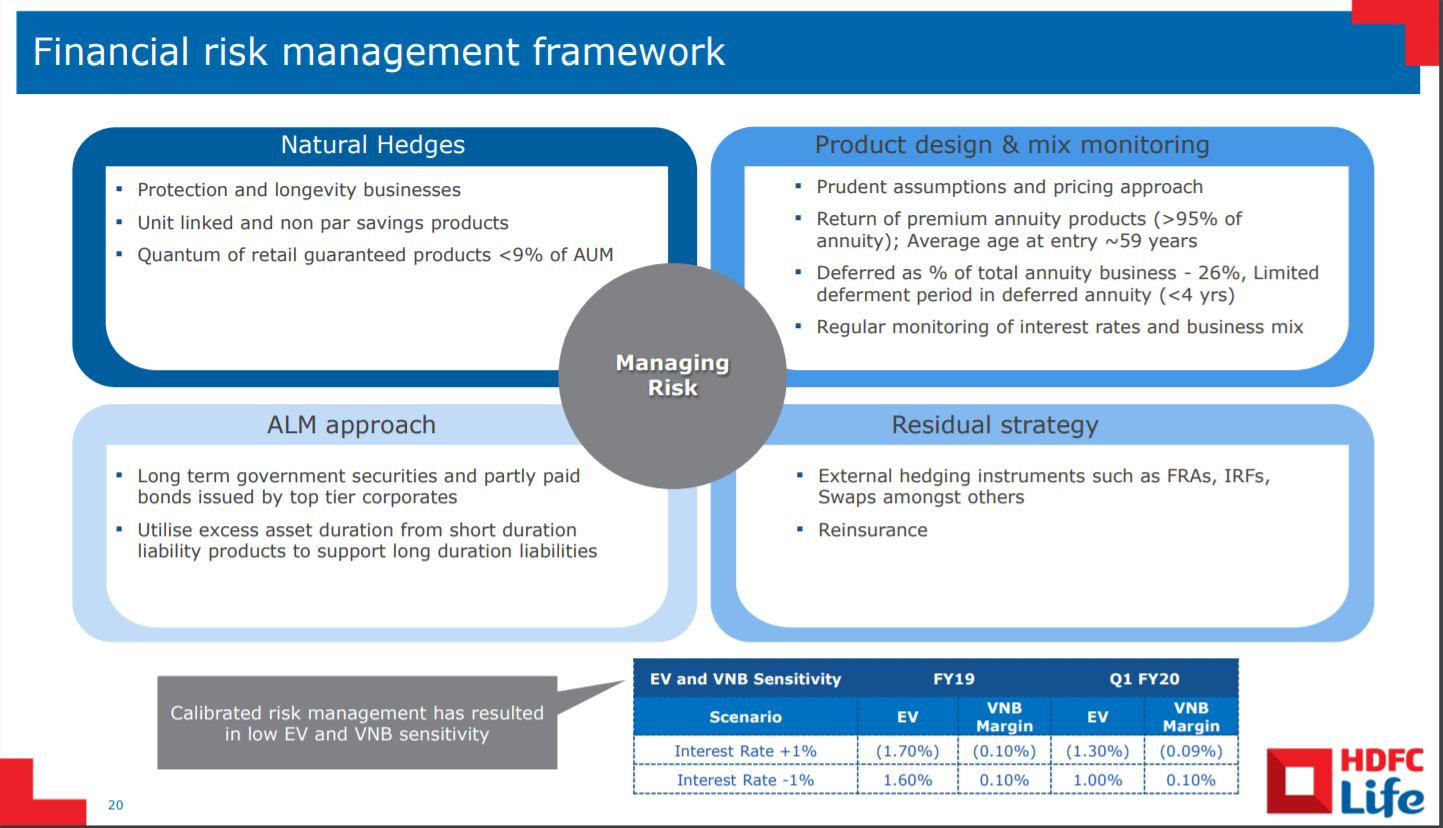

Slide 20

- It is obvious that protection & longevity businesses have natural hedge. If more people live longer, the lesser the payout from the term protection policies.

- Another important concept to know is “return of premium” (ROP) products (also known as return of purchase price - ROPP).

e.g. In case of term insurance of 30 years for 1cr costs 20k per year, then one will get 20k * 30 premium returned on survival if ROP Term Protection policy is bought.

In case of Annuities, if one took annuity of 1Cr for 20 years & the person dies after 10 years, the beneficiary might get remaining 1Cr to him. - I did not understand why having > 95% policies as ROP policies for Annuity is a risk management tool. Average age of 59 for annuity products & life expectancy of 67 years means the risk is manageable.

- Another point is deferment period for deferred annuities is < 4 years. If deferment period was like 10-20 years, then guaranteed return products would become a huge headache as asset returns can go down significantly.

- As shown below later, there are enough long term government bonds available (> 15 years) for innovative insurance companies to create long term products.

- Another concept that was introduced was - “utilizing the excess asset duration from short duration liability products to support long duration liabilities”.

Here company is using credit protect products (which are 3 to 5 years) to support longer duration products like Sanchay Plus. Whatever assets company has bought for these products (and CP is highly profitable product), these can be used e.g. to support like 20th year annuity or 10th year of Sanchay plus. This is the concept in principle. This needs to be tracked, questioned & understood more properly.

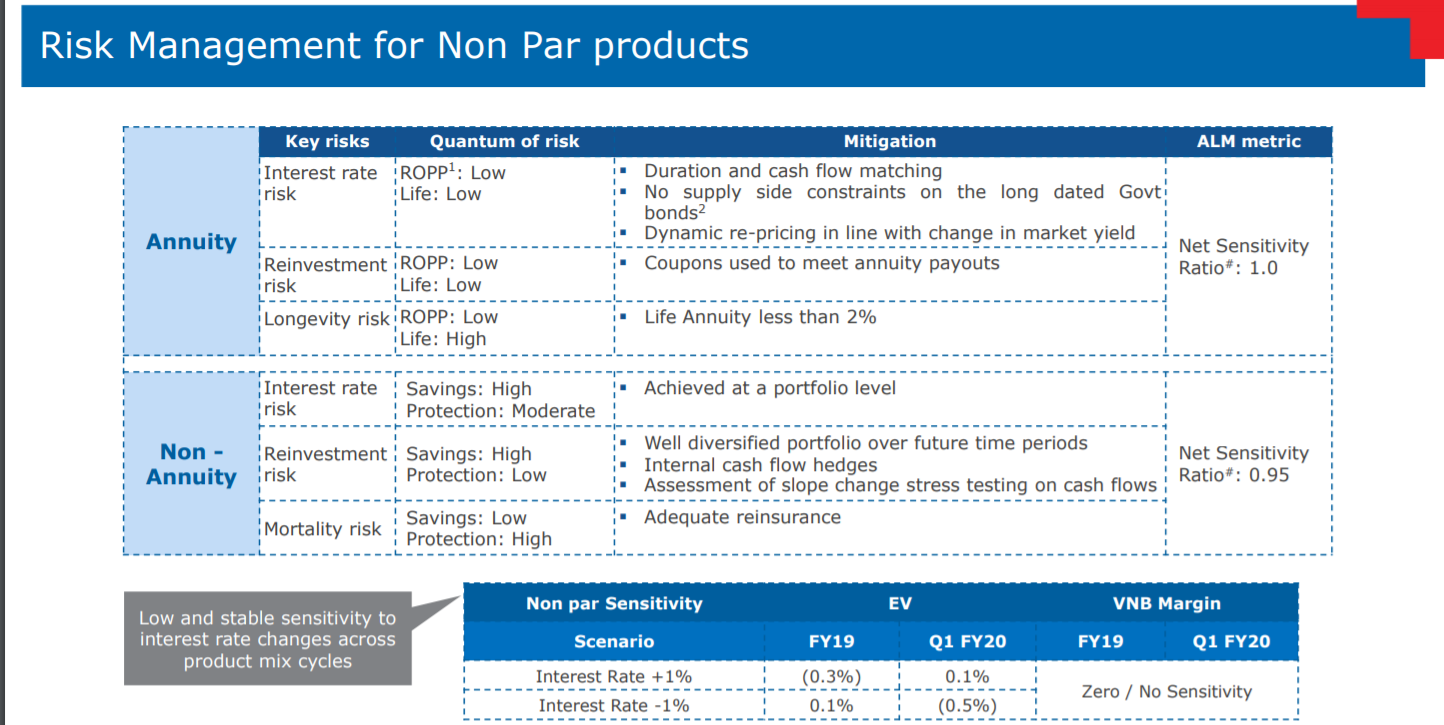

Slide 21

- The easiest aspect to notice here is that longevity risk is high for Life Annuity products. i.e. if someone lives for 100 years & has entered annuity policy at 60th year - the insurance company has to keep paying annuity at guaranteed rate for 40 years, that’s really risky. So good to know that Life annuities are less than 2%.

- Another thing is logically interest rate risk shall be high for annuity products but the company is managing this by two aspects - buying long duration government bonds (> 15 years) and dynamically re-pricing with market yield. The duration & cash flow matching are interesting concepts & It will be covered in small para later.

- The next obvious point is non par protection has high mortality risk i.e. too many people dying in concentrated area or time period. This is covered by re-insurance - pretty standard worldwide.

- The interest rate risk & re-investment risk are high for non par savings products is high (like Sanchay). The key principle here is - these are managed at portfolio level & not at individual product level.

Portfolio Level Risk Management, Cash Flow & Duration Matching

- First aspect is already covered above i.e. using excess asset duration from small duration product to support long term product e.g. CP supporting Sanchay

- Cash flow matching is basically liquidity management where you do not have to sell your assets in distress e.g. highly profitable & short term CP gives a lot of cash flow to pay out annuity payments i.e. it gives you cushion not to distress sell your assets.

- Duration matching is like - having one product behave in one way for x number of years & having another product to behave opposite way for same x number of years.

Questions

- I did not understand how ULIP & non par savings products are direct hedges of each other.

- I do not understand why having > 95% of annuity products as ROP products is a risk management tool.

- I did not understand the management’s claim that - deferred annuity & immediate annuity are kind of matching each other in terms of cash flows.

Other Interesting Comments

- Credit protect business grew at 21% on NBP basis, slowdown due to end lending has slowed.

- HDFC bank has grown at 44% in terms of premium. Last year they lost some share as HDFC bank embraced open architecture, its good to see that they have grown from that base.

- The spreads on Sanchay Plus are wafer thin & not 2-3% as claimed by one of the analyst. Some smaller insurance companies think that it is a lapse driven product as lapse charges are pretty high. MD felt that designing a products to be lapse driven is a corporate governance issue & claimed that company will make money even without lapses.

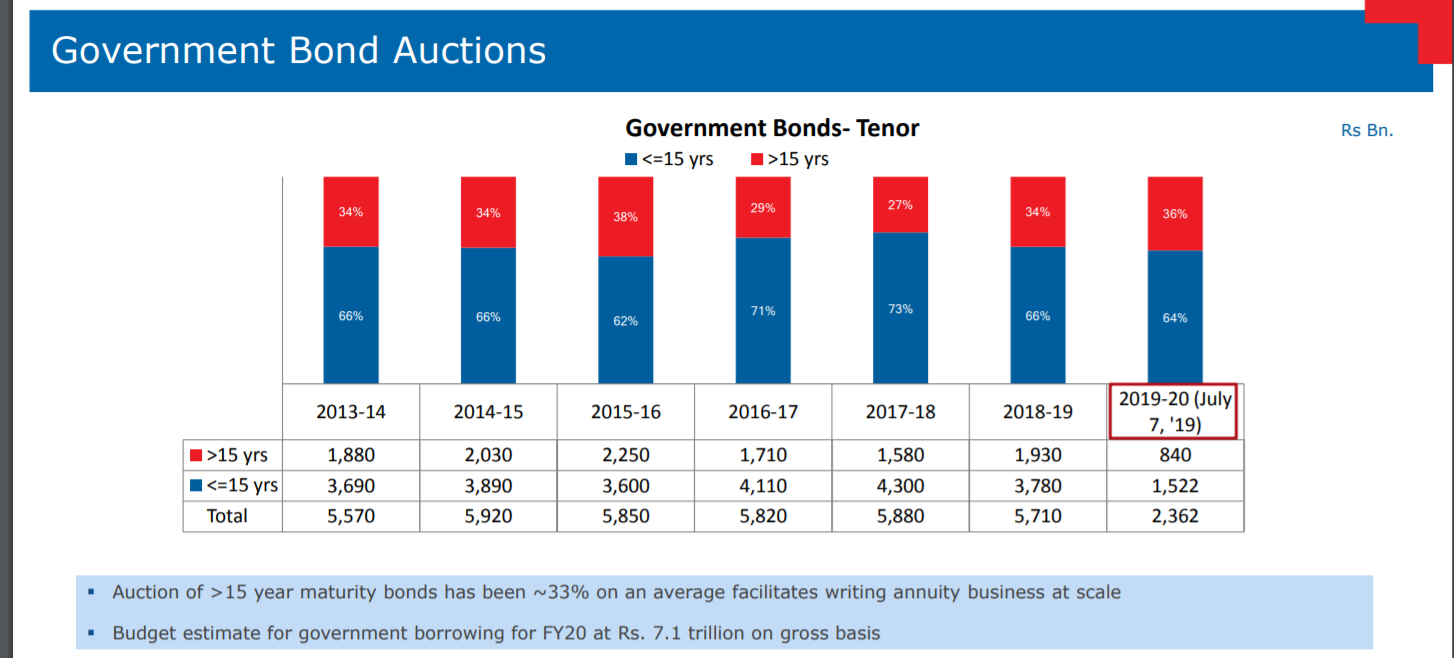

Government Bond Auctions

As mentioned by company that low sensitivity to interest rate risk is secret sauce & they have given some texture of this in Q1 PPT. I feel understanding this is akin to understanding the moat of the company if any.

Disc - Invested.

Standard Life will sell stake in HDFC Life at Rs 477.80-493.40 per share on August 14.

New OFS by HDFC Life at price between 477.80 to 493.40 a share

IPO was at 290 ₹

And few months back March 19 OFS floor price 357 ₹

Little I know on valuation of life insurance company … growing companies should be valued by Appraisal vaue method

AV = EV + structural value

Structural value =VNB *multiple(X)

=(APE * VNBmargin ) * multiple (X)

Normally fair VNB multiple should be based on margin growth and longevity of growth (this most difficult part for me )

Grossly what I see that if I consider above method it’s don’t look expensive as it looks

If someone can guide me for X multiple then I can roughly value Hdfc life business (obviously everyone has figure of EV, APE, VNB margins)

Disclosure Invested in IPO and March OFS

Thanks

Ashit