Might just be one off cause Embedded value is growing steadily. Let’s see.

https://tijorifinance.com/company/hdfc-standard-life-insurance-company-limited#operationalmetrics

Disc: Invested

Might just be one off cause Embedded value is growing steadily. Let’s see.

https://tijorifinance.com/company/hdfc-standard-life-insurance-company-limited#operationalmetrics

Disc: Invested

Nice presentation!

Do you know of any primer I can refer to to understand the business? Seems fairly complicated with lots of industry specific terms and definitions!

The below links should give you a brief starting point and then you can dig down the rabbit hole as much as you want:

The links posted above are great.

Before investing, I personally wrapped my head around the insurance business by looking at it how you would look at other subscription businesses. So what would matter are subscription revenue per month ( New business premiums per month), Avg revenue per subscriber (Avg revenue per policy holder), stickiness of subscriptions (persistency ratio’s), Current value of all future subscriptions(Embedded value). It’s not completely accurate but I personally found it useful.

Hi. I would like to know what do you guys think of the below tax risk? if direct taxes on insurance are increased, based on the sensitivities that these companies give in their filings there could be downside of 10-15%. Though article below is dated I believe the risk is still there?

Article also says that insurance income from policyholders will be taxed unless sum assured is 20x of premium

Yes ,tax rate increase will negatively impact Embeed Value of insurance company.

One more type of tax all insurance company battelling currently is capital gain tax on realization of profit from the float they have.

Summary of concall (source:capital market)

The company has continued to record above industry level growth and maintain leadership position on profitability. The company has recorded growth across all key parameters in FY2019.

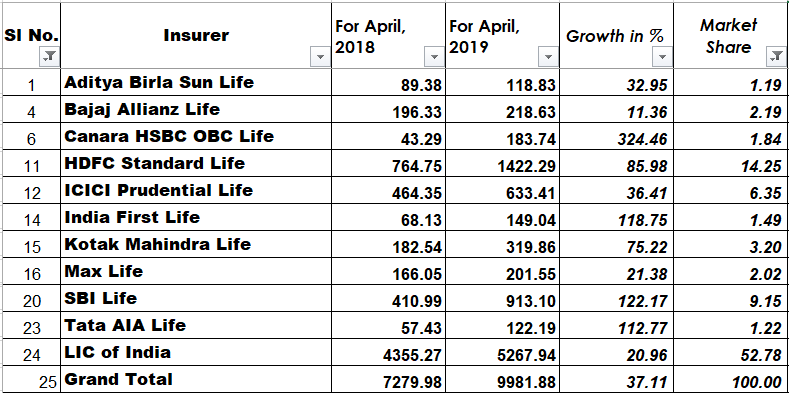

The company has registered strong growth in total premium collection at 15% to Rs 10326 crore in Q4FY2019, while it has increased 24% to Rs 29186 crore in FY2019.

The company remained the market leader in terms of total new business received premium with a market share of 20.7% in the private sector compared to 19.1% in FY2018.

The company has continued to focus on maintaining a balanced product mix, while enhanced emphasis on protection business.

Accordingly term protection APE (Annualized Premium Equivalent) has surged 67% to Rs 1045 crore in FY19 from Rs 624 crore for FY18. Annuity APE has jumped over 140% to Rs 261 crore for FY19. Protection business share moved up to 27% and annuity businesses to 17% of total new business premium in FY2019 from 26% and 9% in FY2018.

The company expects to maintain individual APE growth at 2-2.5 times of GDP at 17-20%.

Annuity business is showing strong performance, while central government employees allowed to choose private pension players from 1 April 2019 would further support pension growth through its subsidiary HDFC Pension.

The company has issued 36 thousand policies in FY2019, more than doubling from FY2018.

ULIPs contributed 55%, Par 18% and Non par 27% of the Individual APE. The company expects the share of ULIP to decline below 40% over a period of time.

The company has continued focus on diversifying distribution mix, which is underpinned by the growth of proprietary channels and dominant presence across all product segments. The company has strong diversified network of 250+ partners through several tie-ups comprising NBFCs, MFIs, SFBs, etc and including 39 new emerging ecosystem partners.

The company has added 28500 agents in FY2019.

The company has reinvented its business model to grow under open architecture adopted by HDFC Bank. The share of HDFC Bank in bancassurance has declined to 82% in FY2019 from closer to 90% in FY2018. However, the non-HDFC Bank bancassurance has jumped 30% in FY2019. The share of overall bancassurance in business mix has declined to 64% from 71% last year. The company expects upward growth from bancassurance channel from here on which should support margins.

The online segment is showing strong growth momentum, which has posted 46% growth for FY2019.

The credit protect business of the company has posted strong growth of 36% in FY2019. The company has diversified partner network in credit protect business with HDFC group contributing 28% of premium, while no other partner contributes more than 10% of premium. Segment wise, housing and LAP contribute 37%, microfinance 29% and others (personal loans, vehicle and tractor finance) rest of the credit protect premium collection.

The company believes that its technological capability coupled with focus on innovation puts it in a good position to maximize the tremendous potential of protection and retirals opportunities. This should help the company to sustain robust performance across market cycles.

The persistency ratios continue to trend strongly across most cohorts. While 13th month persistency healthy at 87%, while 61st month persistency was improved to 52% compared to 51% in FY2018.

The value of new business (VNB) grew by 20% to Rs 1282 crore. The company has recorded industry leading New business margins (post overrun) of 24.6% in FY2019 from 23.2% FY2018.

The company has witnessed decline in solvency ratio at 188% end March 2019 from 192% end March 2018 on account of investment into subsidiary. However, the company has sufficient capital for strong growth for next three years, while the company do not expect fresh capital raising for next three years.

The AUM of pension fund subsidiary jumped to Rs 5170 crore end March 2019, showing sharp increase of 102% over March 2018. The company is the fastest growing pension fund manager under the NPS architecture. The market share of the company has increased to 26.7% end March 2019 from 21.4% end March 2018, among private pension fund managers.

The company has infused capital of Rs 116 crore in its reinsurance subsidiary in Q3FY2019. The company has registered growth of more than 100% in revenue to US$ 4.3 million for FY2019, while the company also registered net profit for the first time in FY19 after operating for three years. It currently offers reinsurance capacity in UAE, Oman, Bahrain, Jordan & Egypt.

The employee base of the company has increased to 19500 employees end March 2019.

update

March being financial year end sees a surge in insurance products sale as part of Tax planning .Things normalize in april.

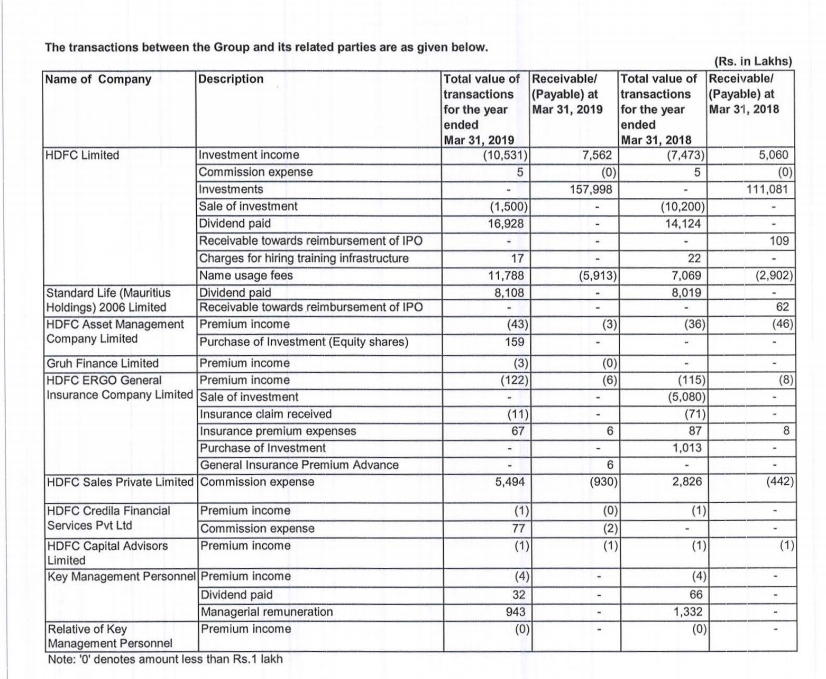

Related party transaction disclosure.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/f37c37d6-8f23-48d9-8c43-4984d2196038.pdf

Insurance is a relatively very under penetrated industry in India with a seemingly long runaway ahead with more people getting knowledge about it , these companies are expected to grow and take market share away from LIC in the long run.

Good performance by HDFC life

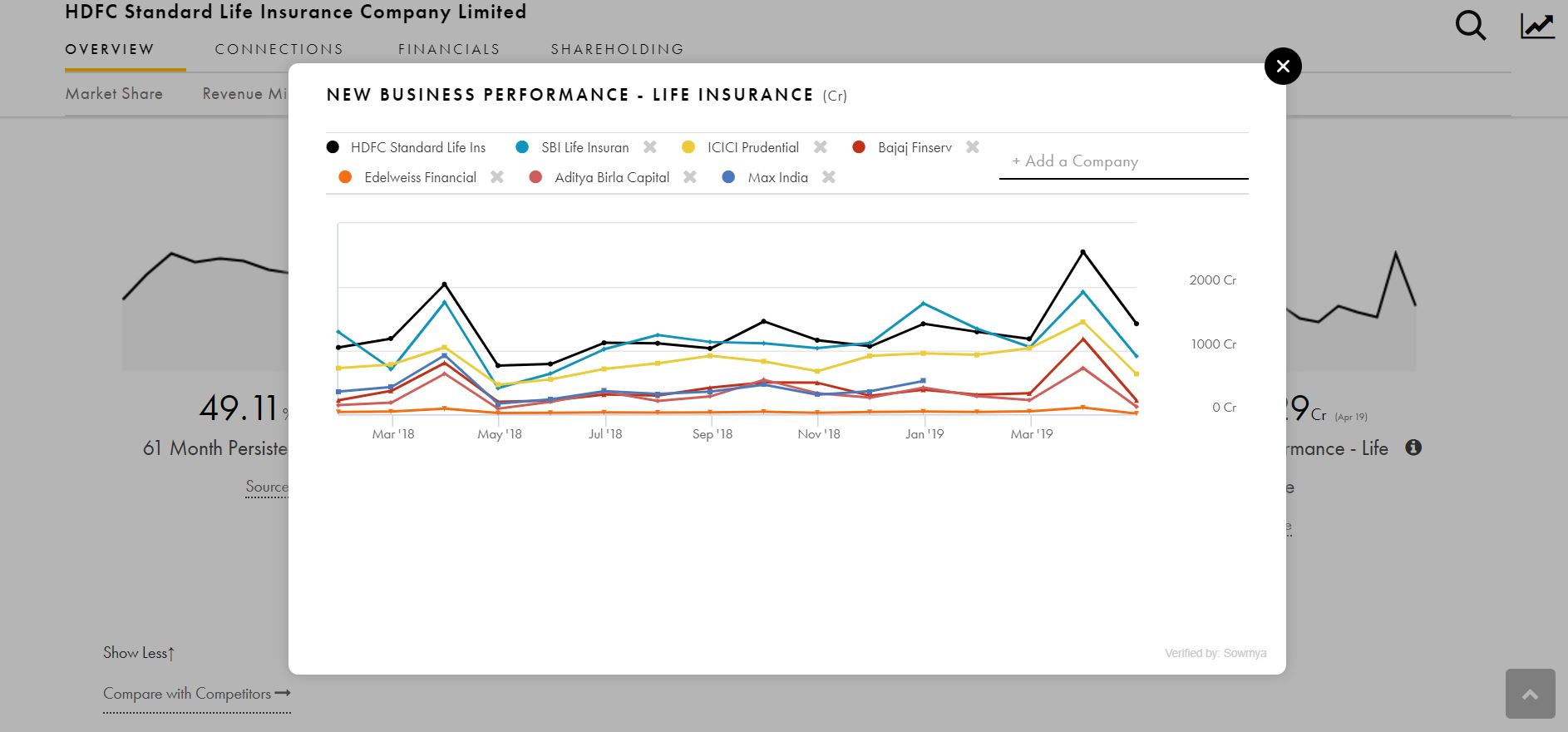

HDFC posted a strong growth in its market share, which rose to 9.24 percent in May 2019 from 7.07 percent in January 2019, a gain of 217 basis points (bps)

HDFC Life’s premium in the month of May grew 52 percent and stood at Rs 1,201 crore. The growth compares to an average premium growth of 31 percent between January and April 2019.

I think reduction in TER for Mutual funds leading to higher push for life product for commission by bank … that’s personal opinion may be wrong

Thanks

Ashit

52% Growth in May was partly due to Single Premium Annuity products sold - Which would not be apple to apple comparison.

Link to todays interview of Ms Padalkar attached.

@rupeshtatiya

Excellent presentation on HDFC Life in VP Goa meet

Really appreciate your work

In your presentation you mentioned that price to EVOP is close to PE ratio based on some reports from analyst who track insurance in international market

Can you please explain more in detail about importance of this ratio

Thanks

Ashit

Can you please share the presentation? Thanks