Through out this market fall, Britannia industries is looking pretty interesting. I have not reached the level to put a detailed analysis on this script (Who knows. I may put it soon). This particular stock shows good resistance.

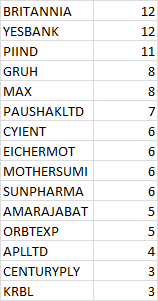

I have readjusted my portfolio. Once i had 50+ companies in my portfolio. I have concentrated it in the recent correction. I have come out of many minor holdings and reinvested it. Below is my latest portfolio. Views are most welcome.

BRITANNIA 13

PIIND 12

YESBANK 12

MAX 8

AMARAJABAT 6

CYIENT 6

HINDPETRO 6

LICHSGFIN 6

SUNPHARMA 6

FINCABLES 5

MOTHERSUMI 5

APLLTD 3

KRBL 3

PAUSHAKLTD 3

I am trying to do a basic check on all the stocks I own. Please correct me if I have missed any basic parameters.

Company: Cyient

Pros:

Zero Debt

5 Yr sales growth: 23.48%

Profit growth: 15.56%

ROE: 17.83%

Current price < Intrinsic value

Net cash flow: 192.52

Consistent dividends. Last year: 25.43%

Cons:

Low promoter holding.

Being a Mid cap, ROE is comparatively less(10 year ROE for TCS: 44%.If compared, TCS has given far better returns. I am not able to find any advantage in Cyinet over TCS apart from better sales. Can someone please help to find if there are any?)

Dhina because you are not looking at the business. Cyient is an Engineering Tech Company and TCS is service based. Recently they apart from giving Engineering Softwares they have started manufacturing electronics on which their softwares would work. I work in an engineering tech company and what my understanding is that, the sector never goes out of business because other businesses need them to run and there is very less competition in the domain (my company’s product just has 2 other competitors and sadly it is not listed so I can’t buy its share)

Thank you @kanvgarg123.

Cyient develops electronic components as well as software for them. So this is not a typical software outsourcing company ( like Infy, TCS), if I understand correctly.Manufacturing would differentiate it, though design and software solutions would be similar to TCS.I am trying to find its direct competitors. Screener.in shows IT service companies as it peers. I checked in moneycontrol as well. But again it lists service companies. Could you please help me in finding its direct competitors?

Thank you very much for helping me.

By the way, Cyient posted good Q2 results today.Share price shot up by 7%.

Pros:

Zero Debt

5 year sales growth: 16.09%

5 year profit growth: 28.38% (Which is increasing every year).

5 years ROE: 42.68%

Improving margin

No pledging, promoter holding high

Pays 30%+ of profit on tax

Branding power, comes up with new products both for elite and mass.

Cons:

PE @ 67.53

Rate of profit growth is much higher than the sale growht. is this because they are increasing the price every year?

If not Could some one please explain me why?

I am not able to find any discussion here on Britannia. May be beacuse not a typical valupickr stock.

I think you should look at their website to get the idea of it. It’s name is cyient.com Also one of the biggest driver for the growth in future could be the aircraft maintenance business which they acquired recently (Frank and Whittney). It is a high margin tech business for which there are very few companies in competition. If they make that big then sky would be the limit for the company.

Britannia is great story of what good management can do to a relatively mediocre company. Till 2012-13, this company and its stock was considered average. Promoters (Nusli Wadia from Bomaby Dyeing) were more busy in fighting their JV partner Danone and company was lacking focus in the market. It was “also ran” company in the area dominated by ITC, Nestle, Parle etc. Varun Berry’s (ex Pesico, Unilever) arrival on the scene changed things a lot. He started de-cluttering the product portfolio and brought in concept of “Power Brands” which increased focus on key brands. They strengthened supply chain, appointed more dealers, added more points of sale and used operating leverage of the company. Their operating leverage (read - better asset utilization) is the reason they are able to generate higher profit growth.

Going forward, it would be interesting to see how much more market share they can gain as competition is getting fierce and operating leverage gains would have limited upside. Further growth would come from capex which could put bit of pressure on bottom line in the short run.

The company has shown consistent growth over years.

The financial numbers looks good.

Risks:

The stock has corrected upto 33% due to Ranbaxy merger issues.

The company also informed that sales/profit will remain flat for this year due to

one time payments related to Ranbaxy merger. From what I understand,

these are one time issues and the growth might be muted for the next two quarters.

The company should be back in track from next financial year.

I have all the respect in the world for Sun Pharma and all that Mr Shangvi has achieved. However, simplistically, there are really 2 large issues on the table for Sun:

the Ranbaxy merger and

the Halol facility

As regards the former, of course there are challenges in making many of the Ranbaxy facilities USFDA compliant, but if anyone can do it, it is Shangvi - he has after all done 19 acquisitions for Sun thus far (India and outside India combined). It is also true that largely the acquisition has been reported to be quite synergistic by independent analysts.

The Halol facility is what is worrying analysts the most. For 2 reasons: firstly, its been a while since the issue was raised, and yet this has been hanging fire - not resolved satisfactorily by the company (if any industry expert has details as to exactly what are the issues that have been raised and what is the reported status on that, that would be wonderful). Secondly, I think the larger issue is the Indian pharma vs. USFDA per se… And what I mean by this is: if big companies like Sun and Dr. Reddy - with all the expensive resources at their disposal (and with such high stakes), are facing such issues (some reported to be as basic as data availability and documentation), how easy are the resolution to such issues anyway? Ergo, is it possible that Indian pharma is so bad that they have been either been conjuring up data or not having any reliable data at all? Alternatively, is there any truth to the conspiracy theories that USFDA is gunning after Indian pharma (for reasons that need not be documented)?

Clarity on the above 2 items is quite essential before plunging onto Sun as an investment idea.

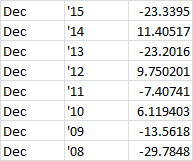

Results are out and the stock has hit lower circuit. I compared December quarter sales with previous quarter in the past. This is how it looks. Lets see how this is going to be. I will continue to hold this.