Here is the latest portfolio

| Sr. No | Company | Sector | Capitalisation | Alloc % | Rationale |

|---|---|---|---|---|---|

| 1 | HDFC ASSET MANAGEMENT COMPANY LIMITED (XNSE:HDFCAMC) | Financial | Mid Cap | 12% | Financialization theme |

| 2 | BSE Limited (XNSE:BSE) | Financial | Small Cap | 8% | Financialization theme |

| 3 | AVENUE SUPERMARTS LIMITED (XNSE:DMART) | Services | Large Cap | 8% | Long-term retail play, debt free |

| 4 | HCL TECHNOLOGIES LIMITED (XNSE:HCLTECH) | Technology | Large Cap | 8% | Coffee Can |

| 5 | OLECTRA GREENTECH LIMITED (XNSE:OLECTRA) | Automobile | Small Cap | 8% | EV theme |

| 6 | DR. LAL PATHLABS Limited (XNSE:LALPATHLAB) | Healthcare | Mid Cap | 8% | Coffee Can |

| 7 | GODAWARI POWER AND ISPAT LIMITED (XNSE:GPIL) | Metals & Mining | Small Cap | 7% | Cyclical debt free & Value |

| 8 | DEEPAK NITRITE LIMITED (XNSE:DEEPAKNTR) | Chemicals | Mid Cap | 6% | Growth |

| 9 | ABBOTT INDIA LIMITED (XNSE:ABBOTINDIA) | Healthcare | Mid Cap | 6% | Coffee Can |

| 10 | ASTRAL LIMITED (XNSE:ASTRAL) | Chemicals | Mid Cap | 5% | Coffee Can |

| 11 | PSP PROJECTS LIMITED (XNSE:PSPPROJECT) | Construction | Small Cap | 5% | Asset Light business in construction |

| 12 | ADITYA BIRLA SUN LIFE AMC LIMITED (XNSE:ABSLAMC) | Financial | Mid Cap | 5% | Financialization theme |

| 13 | GATEWAY DISTRIPARKS LIMITED (XNSE:GATEWAY) | Services | Small Cap | 4% | Promising sector for future |

| 14 | Fsn E-Commerce Ventures Ltd (XNSE:NYKAA) | Services | Large Cap | 3% | Growth |

| 15 | LAURUS LABS LIMITED (XNSE:LAURUSLABS) | Healthcare | Mid Cap | 3% | Growth |

| 16 | INDIAN ENERGY EXCHANGE LIMITED (XNSE:IEX) | Services | Mid Cap | 2% | Growth |

| 17 | HDFC BANK LIMITED (XNSE:HDFCBANK) | Financial | Large Cap | 2% | Coffee Can |

| Stocks | |

|---|---|

| Top 5 | 45% |

| Top 10 | 76% |

| Top 15 | 96% |

| Market Cap | |

|---|---|

| Large Cap | 22% |

| Mid Cap | 47% |

| Small Cap | 32% |

| Sector Split | |

|---|---|

| Financial | 27% |

| Healthcare | 17% |

| Services | 17% |

| Chemicals | 11% |

| Technology | 8% |

| Metals & Mining | 8% |

| Automobile | 8% |

| Construction | 5% |

| Defensive | 25% |

|---|---|

| New Age/Theme | 11% |

Investing Objectives –

Return of Capital - ![]()

Beat BSE Sensex in terms of CAGR ![]()

Beat FD returns ![]()

Reach 15% CAGR ![]()

Beat MF(direct) returns (19% Vs 15% CAGR) ![]()

Changes -

- Sold off Titan & 60% of Laurus Labs

- Bought 7% of PF in GPIL based on this rationale

Notes -

-

BSE Sensex is performing slightly above in terms of returns

-

PF is down by 14% in Calendar Year 2022

-

The MF portfolio is more resilient than the stock PF as I did not deploy capital in MF after Dec 2020 but I still bought/sold in stock PF after Dec 2020. Ideally, if there is no incremental capital, I should have reduced my equity component as part of rebalancing exercise of my Equity: Debt ratio.

-

It takes a lot to drop a company like Titan, but like Charlie Munger says, investing is akin to Parimutuel betting. I see better risk-reward in the case of GPIL than Titan. Same is the case with reduction in Laurus labs.

-

Mid-cap and Small-cap indices have corrected a lot. I am contemplating on restarting SIPs in my existing MFs

-

Growth continues in Dmart & Nykaa. Avenue Supermart: a compounding machine? - #1958 by akash_das - Dmart revenue jumped 95% YoY growth. I don’t want to advocate BAAP(Buy At Any Price) but holding Dmart gives a sense of safety even though it always stays at high valuation. In the end, investing is about paying for the certainty of returns - predictability and sustainability of the earnings. I convinced myself to not sell it even though the stock was way overvalued when it was quoting at more than 5000 Rs as I felt staying put is more profitable for my PF in the long run and big corrections if any can be bought on dips.

-

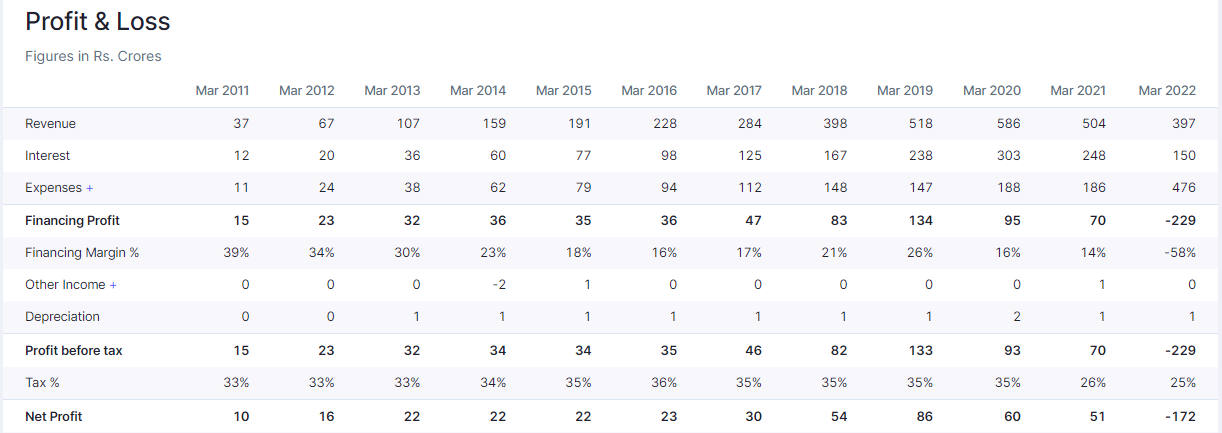

Long-term Investing in small/micro caps is very difficult. As I mentioned in the beginning of the thread, Muthoot Capital Services was selected as part of Coffee Can Portfolio stocks mentioned in the namesake book by Saurabh Mukherjea. That means, the stock displayed a consistent sales growth YoY and also ROCE for 10 years. Even then, the stock is now a fallen angel. The chance of it raising is very less as compared to its market cap of 276 Cr, it has a PBT of -229 Cr. I sold this last year as I could not convince myself staying on course with this even though, management is good, consistency in execution till March 2020. Especially, in finance sector, it is better to stay with leaders. The stock has fallen more than 50% from my sell price.

-

For a part-time investor like me, I see two approaches to make profit in stock market

-

Looking at index’s long-term PE or develop some other mechanism where we already track the company and get an estimate of normalized earnings and then enter when risk/reward is better. This PF thread explains this well.

-

Study a company in-depth, do extensive research and if the conviction is very high, enter at full force even in the middle of a bull market. The number of companies in the watch list should be very less and also conviction should be very high.

-

Based on the investing style, top-down works well with 1) and bottom-up with 2).

I am more of a top-down investor.

- Few years back, while I was working in Paris, having seen different regions of France, I asked my then French manager about what would have been the motivation of general public(not government) to leave this resource rich, beautiful and highly developed region and work in relatively tough climates & foreign conditions elsewhere during French empire. He is a wise man and thought for sometime and told me, the primary reason must have been about inflation, security of future and then of course the attraction of high lamps & services. Reading about high inflation these days, I remembered those words

Words of Experienced Investor -

@zygo23554 has explained about the last decade in investing in this blog and I found the below words worth reading again

From whatever experience I have as a money manager in India, I can tell you this -

At an annual pre tax return of 8.5% from fixed income, many investors will happily take that over the volatility of investing in the equity market.

The most likely outcome of buying and holding the headline benchmark index in India over a 5-year timeframe has been a CAGR of 10-12% p.a. Across the world, investing gurus and academicians agree that the equity risk premium is broadly in the range of 5-6%. From here one can do the math and see how a 12% p.a. return from equity isn’t very superior to a credit risk free 8% p.a. in fixed income on a risk adjusted basis.

Doesn’t mean one stays away from equity, it is still one of the only few asset classes that has been proven to beat inflation over longer time frames.

It just means that one should be more demanding of above average growth from businesses rather than happily pay up 50 PE for a 10% growth based purely on 5-year average multiples. Consider 10-year average multiples to demand a higher margin of safety from here, of course adjusted for changes in business quality over the timeframe.

For this very reason, valuation is an art and not just a science.