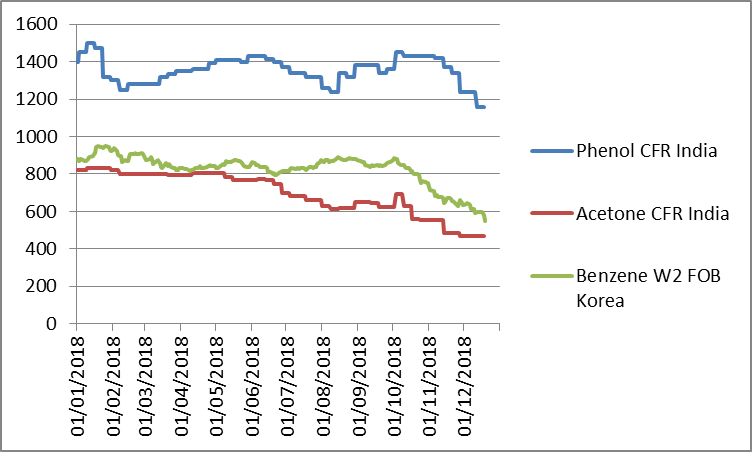

A month old article but important note : “Domestic prices been on a steady decline after local producer Deepak Phenolics Ltd (DPL) started up its phenol/acetone plant”. Need to see if the new supply will suppress prices for the long run, or the market will adjust. Prices have slightly recovered from the Dec low in January though.

Excellent results. The new phenol plant has been operational for 2 months now and they have achieved a turnover of 321 cr from it. Looks all set to achieve projected sales of 2000cr /year from the new plant in fy20. The standalone business has also performed very well.

Hi,

Few concern on standalone result. Traditionally H2 is good compared to H1. But despite good performance from performance product segment qoq the sales is flat,even it is same case q2 compared to q1. Need to get reason for the qoq sales decline (may be crude price factor would have been played on Q3 but why q2 sales flat ). Last concal I asked this question mgmt said H2 we see good improvement .if anyone else has know the reason for same?.

Still I am hoping mgmt could do @ consolidation level 4500cr sales by 2020.

Revenue grew by 23 % to 457.8 Cr from 371.6 Cr same quarter last year

EBITDA grew by 36 % to 71.7 Cr from 52.7 Cr same quarter last year

EBITDA margins grew by 150 basis points to 15.7 % compare to 14.2 % same quarter last year

PBT grew by 56 % to 48.1 Cr from 30.7 Cr same quarter last year

PAT grew by 55 % to 31.6 Cr from 20.34 Cr same quarter last year

Depreciation grew by 14 % to 13 Cr from 10 Cr same quarter last year

EPS stood at Rs 2.32 per share compare to Rs 1.56 per share same quarter last year

Domestic revenue grew by 29 % to 293.1 Cr from 227.4 Cr same quarter last year

Revenue from exports grew by 10 % to 153.3 Cr from 139.7 Cr same quarter last year

Segmental Performance

Revenue from BC segment grew by 12 % to 204.9 Cr compare to 182.3 Cr same quarter last year. BC segment contributed 49 % to total revenue with EBIT margin of 14.1 % . Growth in the BC segment was a result of firm realisations supported by improved product mix.

Revenue from FSC segment grew by 21 % to 148.4 Cr compare to 122.4 Cr same quarter last year. Fine and specialty segment contributed 33 % to total revenue with EBID margin of 43.1 %. Capacity expansion for established products and backward integration initiatives have enabled the Company to drive volume growth which, combined with firmer realisations in select products, has resulted in strong growth in top line for the segment

Revenue from FP segment grew by 50 % to 100.1 Cr compare to 66.7 Cr same quarter last year. Quarterly revenues from the PP segment crossed the milestone of Rs. 100 crore and now contribute 22% of overall revenues against 18% in Q3 FY18. EBIT margin strongly increase to 18.2 % from negative -1.9 % same quarter last year. Favourable demand supply trends have resulted in improved realisations driving a solid performance in the PP segment.

Balance Sheet

Total Debt stood at 498 Cr at the end of the Dec 2018 translating in Debt-equity ratio of 0.47 and consolidated debt to equity is 1.32 to 1 which is very comfortable

Key Highlights

Phenol acetone plant commissioned on 1st November 2018 has already ramped up to capacity utilization above 80 % within three month of commissioning this has resulted in addition of Rs 321 Cr to the consolidated turnover in Q3 of FY19. Plant is delivering positive EBITDA and PBT in the first quarter itself .

Succeeded in replacing bulk imports of phenol and acetone in local market

Succeeded in making pharma grade acetone and also making export of acetone.

Achieved production and despatch of approx. 75% of avg. capacity utilisation showcasing robust logistics

Seed marketing efforts in pre-commissioning phase have firmly established DPL in leadership position

Well placed to improve market share even with current global market led volatility.

Outlook

Company will be growing between 15-20 % on top line level going forward

Committed 1% increase in EBITDA every year and will achieve it YOY

They purchased 75000 shares from open market in tranches, on 25 and 26 and purchased 22000 shares yesterday. For such disclosures, you can refer to BSE website.

That works out to 1.7cr against a market cap of 3100cr roughly in real money, hardly worth advertising

Even if lot of people buy on that news and share price increases, that 1.7cr is put to good use as promoter holding is much more

What about the outcome of IT raid on company. I would prefer not to be a major part of any company(through investment) with corporate governance/promoter integrity issue.

Disc : reduced 80% holding after IT raid incident.

Performance chemicals division mainly OBA - optical brightening agent stole the show because of supply crunch of DASDA which is its raw material and who price increased drastically in last few months. Deepak produces DASDA and uses it to produce OBA too.

Deepak phenolics the big project of DN has now started contributing meaningfully having operated fully for March quarter. Maximum impact likely to be felt in consolidated nos of 2020 when it will be operational for full year.

Company provides presentations and conducts regular concalls for those interested in digging deeper.

In recent interview by deepak Mehta to CNBC mentioned Deepak nitrite aspires to do 1 billion dollar revenue by FY22. Their current earnings of 2000cr from base business and it can grow 20% per year so FY22 it can generate 2500cr and another 2000cr from phenol so around FY 22 they can generate 4500 cr . I am not sure what are all other avenues there for Deepak to get this additional 2000cr in next 2 years. Till now they mentioned only very limited growth plan like venturing into new pharma intermediate and debottlenecking existing plant and phenol derivates.with these plans I am not seeing they can achieve this target.

1 billion is an aspirational target. When he said that he probably meant 6500 cr by fy22e. (Usd gaining strength). Don’t think we should take it at face value.

4000-4200 cr looks possible with all cylinders firing by fy20e. If they manage to attain this, would be amazing.

This is a growth hungry management, and have proven their prudential risk taking capabilities with phenolics.

I would keep an eye on their BS, as he in the interview didn’t commit on decreasing leverage. They will reinvest everything, which comes with its own set of risks.

Also I am keeping an eye on consolidated margins. Expecting 15-16% EBITDA with phenolics plant operating at optimum utilization.

Anti-dumping duty on Acetone should also help their cause.