Apart from having to maintain revenue and profit growth to sustain valuations, i think their relatively higher roce also contribute to valuations and i am not fully clear on that.

how their roce levels are relatively so high and are they sustainable. in the concal someone got technical with interesting Qs about construction process and machines/material used which i did not understand. But it could be the reason for their relatively higher RoCE. I guess some construction expert could explain this.

RoA is also high. Why? One Interesting point was that after a project is completed they could refurbish some of their assets and lengthen useful life. I didn’t understand this but this is what the mgmt claims. So they don’t have to buy new assets everytime. The opposite effect is that mgmt could be over estimating the useful life and understating the depreciation which will result in higher profit.

Agree that growth is a crucial factor in determining valuation but disagree on the valuation risk. When they have marquee clients, longevity of the biz is not in doubt unless some new risks emerge. I will consider valuation risk when the industry is on top of the cycle with the best margins and we are paying high PE. Real estate industry is down and margins are depressed but it serves specialized market and have good longevity. As long as they have good return ratios and good clients they deserve 20 PE atleast. I think the growth has to come from asset turnover. They plan to invest 75cr/year and 300cr of additional sales/year could be possible as they said 4x is achievable going forward. I think RoE above 20% looks sustainable. No room for valuation to expand and returns will be from earnings growth

Sure, one needs to accumulate it on down days to generate better than 30% CAGR. It is discounting current earnings but when I look at NBCC and feel this could surprise us in the private sector real estate.

i agree that valuations seem high and have been accorded due to the past growth rates and high roce’s. sustainability of these will be key to stock performance. currently, the company looks capable of doing so given sector tailwinds and past demonstrated execution ability.

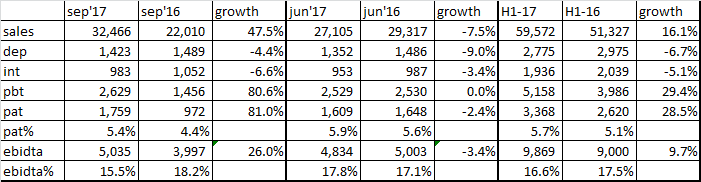

H1 is always slow for construction work due to monson season in India and management hinted about this on sept con call that’s why you see Dmart store opening is always slow in first half of the year . We need to wait and watch q3 and q4 result to get the better sense of future direction.

Original PE investor Paragon sold 3% stake to a new investor SocGen at 417. This is the same price IIFL gave as target price in their initiation report.

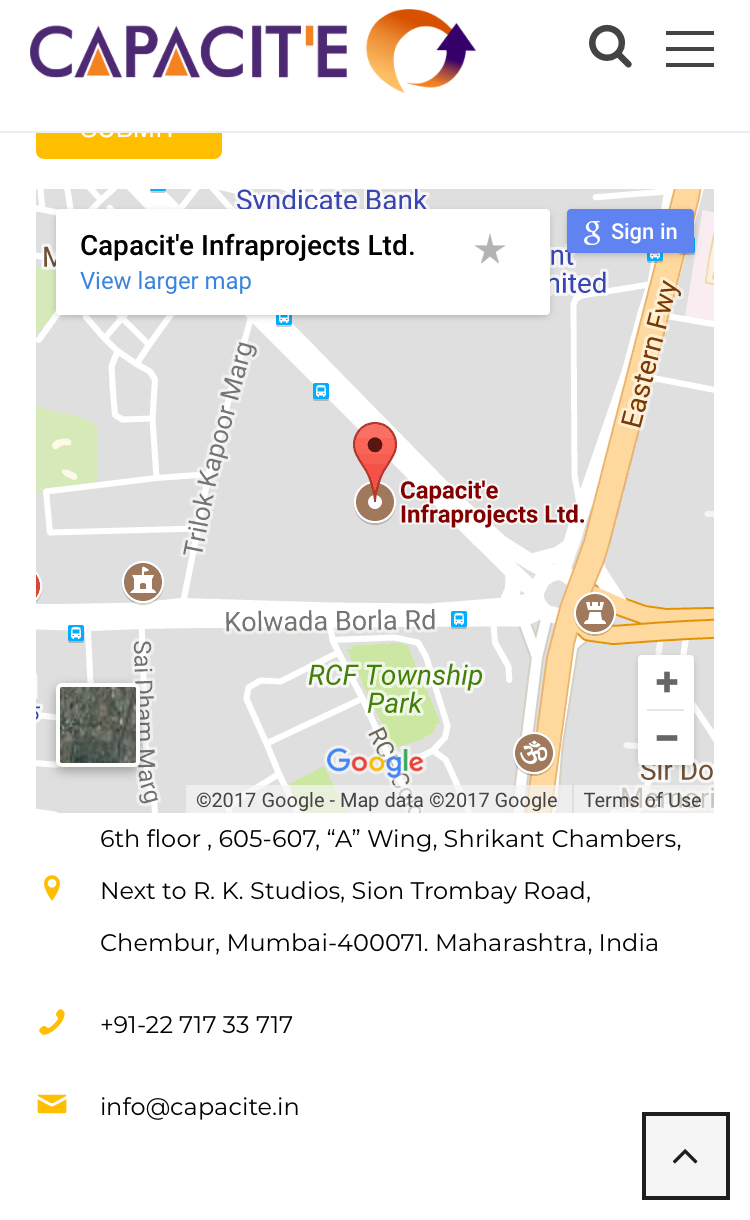

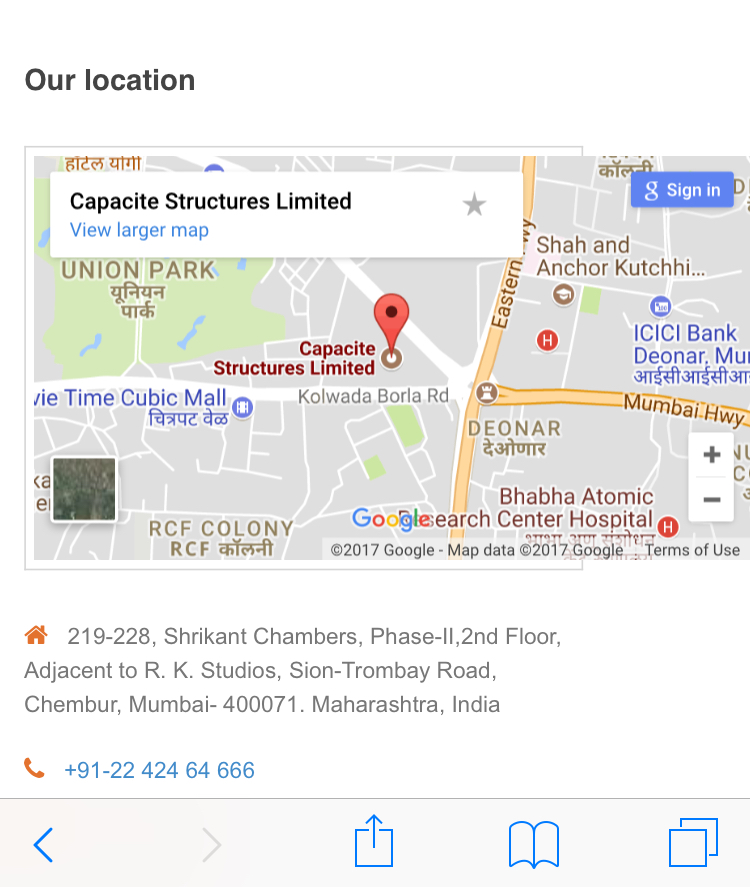

Is capacite structure part of the same company? Its named here including the MD

“It is alleged that Sanjay Kulkarni, Managing Director of Capacite Structures, approached a middleman, Rishabh Agrawal, having good contacts with public servants for bagging the sub-contract.”

As I understand, Capacit’e infraprojects is not involved in this scam. Name sounds similar and slightly surprising that they are at the same location and in a similar line of business. This raises lots of questions about the operating structure and influence of Pratibha industries’ promoters. The management has indicated willingness to venture into public housing projects and this event will require enplaning from them.

This is really confusing,the company named in the report (Capacite structures) has almost similar name,the logo too looks very similiar and located in the same building.

Both seems to have a connection with the prathiba industries.One possible explanation could be they were part of the of same team in prathiba and then decided to form their own entities.

Capacite were prompt in coming up with the explanation but this cloud will linger on for some time…

I think there is difference in line of business as Capacit’e structures in mostly into public infra/capital goods etc while the listed entity is into private housing projects so far. Their DHRP prospectus has given this as a risk factor. I think they should have got the name changed before listing.

I believe a great deal of credibility is associated with a name. If only changing the name for the sake of it would sort the problem than Anil Ambani would not have opted to retain Reliance name for his ventures. Almost all the stakeholders relate themselves with the older name of the company and in this case both the companies keeping the same name & similar logo viz “capacite infraprojects” & “capacite superstructures” despite parting ways is quite understandable.

Yes. They seem to have exited and societe generale along with Goldman sacchs have entered… In another news they have won a 365.5 crepe order from oberoi group recently… Awaiting to see their total order book and execution in q4 and whether they meet their guided top line

Have won another repeat order from Sea View Developers worth around Rs 162 Crores. Further latest shareholding pattern for March has been released and Paragon Partners are still the shareholders and have not exited. Order book is around 5500 Crore and provides a good revenue visibility. Now the only thing remains is Good execution and Working capital manegment.78366a6a-9409-4f46-b201-3ca16e98f2f3.pdf (113.6 KB)