Capacit’e Infraprojects is a Mumbai-based construction company and is coming up with Rs 400-crore initial public offering on September 13, with a price band of Rs 245 to Rs 250 per share.

Objects of the Issue:

The objects of the Issue are:

- Funding working capital requirements;

- Funding purchase of capital assets (system formwork); and

- General corporate purposes

Company Information:

Company Strengths:

-

Exclusive focus on construction of buildings in major cities

-

Large Order Book with marquee client base and repeat orders: As of January 31, 2017, we have an Order Book aggregating to ₹ 40,490.74 million, with projects spread across major regions in India, including the MMR, NCR, Pune, Hyderabad, Bengaluru, Chennai and Kochi. Our Order Book, as at January 31, 2017, is 4.75 times the consolidated revenue from operations for the financial year ended March 31, 2016 and consisted of orders for construction of 11 Super High Rise Buildings, 19 High Rise Buildings, six Other Buildings, 14 Gated Communities and one Villament.

-

Experienced Promoters, Directors and management team:

-

Ownership of modern system formworks and other Core Assets: We have the capabilities to undertake building construction projects using modern technologies including temperature-controlled concrete for mass pours, self-compacting free flow concrete for heavily reinforced pours and special concrete for vertical pumping in Super High Rise Buildings and High Rise Buildings. We use different types of system formwork owned by us including, automatic climbing system formwork, aluminium formwork, table formwork, composite panel formwork (consisting of vertical panel and horizontal panel formwork systems) to meet the varying construction needs of different types of buildings. Each kind of building requires a high degree of skill, scale and speed to complete. We believe that implementing a variety of technology options available to us in construction of buildings allows us to reduce construction times.

As at December 31, 2016, we had a consolidated net block of fixed assets (excluding capital work in progress) amounting to ₹ 2,506.69 million, including ₹ 2,136.83 million of Core Assets constituting 85.24% of our net block of fixed assets. -

Access to skilled workforce: As of January 31, 2017, we had 1,688 employees and 10,678 contract laborers across all our projects.

-

Debt to Equity is at 0.51.

-

Promoters hold more than 50% stake.

-

We have received an ISO 9001:2008 certification for our quality management system. Further, we have also received an ISO 14001:2004 certification for our environmental management system and an OHSAS 18001:2007 certification in respect of our occupational health and safety management systems.

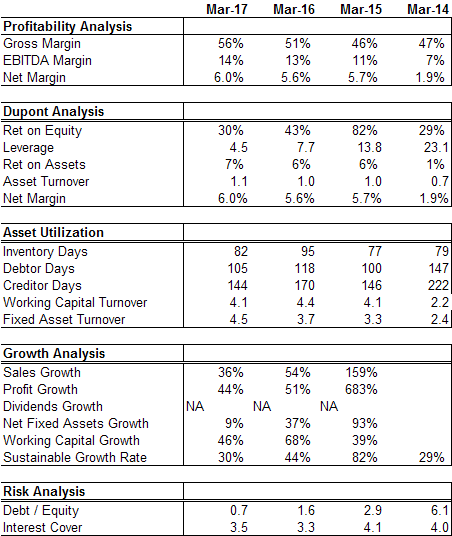

Financial Performance:

EBIDTA:

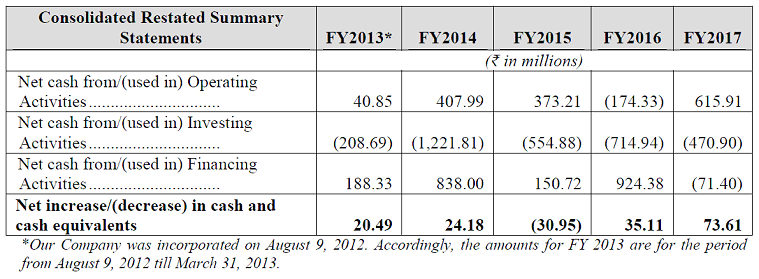

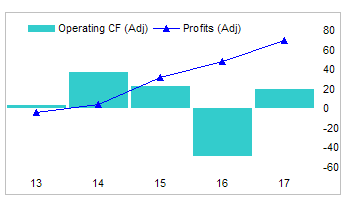

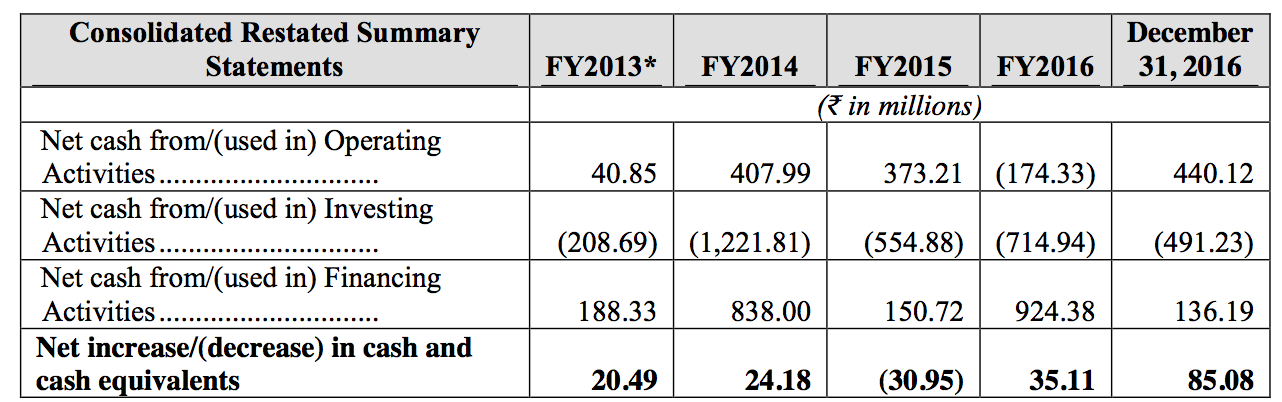

Cash flow:

Management Salaries:

- Mr. Rahul R. Katyal: 8.53 Million PA

- Mr. Subir Malhotra: 8.53 Million PA

- Mr. Rohit R. Katyal: 8.83 Million PA

Company Strategy:

- Continue to remain focused on building construction

- Expand in the mass housing segment

- Expand our presence in cities with high growth potential

- Undertake projects on a design – build basis

- Increase our focus on and execute greater number of projects on a lock-and-key basis

- Bid for, and undertake, projects in the public sector

- Capitalise on changes in the construction industry that will arise on account of the implementation of the RERD Act

Risks:

- Manpower:Our business is manpower intensive and we are dependent on the supply and availability of a sufficient pool of contract labourers from sub-contractors at our project locations. Unavailability or shortage of such a pool of contract labour or any strikes, work stoppages, increased wage demands by workmen or changes in regulations governing contractual labour may have an adverse impact on our cash flows and results of operations.

- Delay in delivery: We may be subject to liability claims or claims for damages or termination of contracts with our clients for failure to meet project milestones or defective work, which may adversely impact our profitability, cash flows, results of operations and reputation.

- Dependence on sub contractors: We face certain risks relating to our reliance on sub-contractors and third parties for supply of raw materials, non-Core Assets and for providing certain services in the construction of our projects that may adversely affect our reputation, business and financial condition. Failure by our sub- contractors and third parties to adhere to regulatory requirements may subject us to penalties.

- Price fluctuation of raw materials: We are dependent on the availability of and prices of steel and ready-mix concrete. Any lack of availability of or upward fluctuations in the price of steel and ready-mix concrete or our ability to pass on any increased costs of raw materials to our clients may have a material adverse effect on our business, cash flows, results of operations and financial conditi

- Client concentration: Projects awarded from certain clients contribute a significant portion of our Order Book. As at January 31, 2017, projects awarded by our top five clients, based on our Order Book represented 36.80% of our Order Book. Further, as at January 31, 2017, our top 10 clients contributed 58.29% of our Order Book.

- Geographical concentration: Our operations and revenues are geographically concentrated in the MMR. Our Company’s projects in MMR accounted for 73.50% of the Order Book as at January 31, 2017. We also have projects in NCR and Bengaluru, which accounted for 9.58% and 5.89% of the Order Book as at January 31, 2017, respectively. Consequently, we are exposed to risks emanating from economic, regulatory and other changes in these locations which we may not be able to successfully manage and which in turn may have an adverse effect on our revenues, cash flows, profits and financial condition.

- Government regulations: Our clients operate in a highly regulated environment, and existing and new laws, regulations and government policies affecting the sector in which they operate could adversely affect our business, financial condition and results of operations. Any failure to obtain licenses and approvals by our clients, could adversely affect our business, financial condition and results of operations.

- There is outstanding litigation involving our Company, our Directors and our Promoters, which if determined adversely, could affect our business and results of operations. Amount involved in roughly 300 million spread across 2 cases.

- We have substantial working capital requirements and may require additional financing to meet working capital requirements in the future. A failure in obtaining such additional financing at all or on terms favourable to us could have an adverse effect on our results of operations and financial condition.

- Our business is capital intensive and we may require additional financing to meet capital expenditure requirements in the future, which may be unavailable, which could have an adverse effect on our results of operations and financial condition.

- If the Indian real estate market weakens leading to a slowdown in construction activities, our business, financial condition and results of operations may be adversely affected.

Source of the Information: SEBI | Capacit'e Infraprojects Limited

The IPO is reasonably priced at 24 PE and the company looks like a good long term bet.

Disc: Planning to invest in IPO.