Can some elaborate what note no-7 trying to say???

Couldnt find the results on BSE site as well as on Arrow GreenTech’s website. I was asking about the source where I can find the Quarterly report since it was not available on BSE site.

1 Like

Arrow_GT.pdf (329.1 KB)

These guys are saying another couple of quarters to comeback to the normalcy.

My understanding is that they booked revenues in earlier quarters in a subsidiary and in Q4 they had to reverse the sale as it was not accepted by the customer. Hence the “negative gross revenues”. It is arguable whether the correct accounting treatment is to reverse revenues or to write-off receivables as bad debt. Either ways, extreme bad news - one doesn’t know how to trust any number from management going forward

1 Like

They raised the invoice,but cash flow didn’t happen subsequently. Shouldn’t they report negative CFO than negating the revenue itself?

Should have been bad debts written off. But since it’s negative revenue… it further raises questions on their revenue recognition methodology itself.

Company has stated We would like to inform you that the Company has entered into Collaboration Agreement with Versarien Pic through its subsidiary company Cambridge Graphene Limited, covering a variety of the graphene products a-nd activities.

ba92b313-b2fc-4267-99e1-f431004760c6.pdf (833.0 KB)

Q4 results were terrible… how can a company report negative revenue.

- What r their revenue recognition policy?

- Why was a non acceptance of client treated as negative revenue, was that service to such client ever completed. How many clients does this amount pertain to. Can we get details of such clients.

- Why was such write off not treated as bad debts n instead company chose to reverse revenue.

- Are they expecting any more such write off?

- Is there any plans for monetizing patents / technology

- Why is there sudden de growht in subsidiary ?

7

As highlighted previously on thread, Arrow, at this point, appear more of hope then happening trade. I have booked my loss in March 2018. Depsite increase in price, I paid tution fees of 33% negative XIRR. My greed forced me to booked highest level of loss in my investment career. Imagine, that with less than 1% allocation in period of 9 months !!! I would not regret, if with this tution fees, I do not repeat such trade in future.

Discl: I am not SEBI registered advisor and investors shall do their own due diligence before making any decision. I still hold tocken tracking position in the company and my view may be biased.

5 Likes

I read the thread by random and red flags by @varadharajanr were good learning points. Investment by experienced investor @dd1474 was interesting.

Thank you @dd1474 for sharing your investment and exit. It helps in a sense that mistakes can be committed even by experienced investors like you (I should call it a silly mistake considering red flags raised by @varadharajanr)

Thank you @varadharajanr for the red flags which must have helped many in avoiding the stock.

4 Likes

Had met the management (promoter and newly appointed CFO back then) in 2016 and was not convinced with what promoter was telling me even by an iota. Some of the glaring red flags during our conversation -

- he could barely pronounce the product names

- couldn’t remember few of his about to be launched products

- When asked since you are in patent business, I am assuming you should be having good R&D department. I asked him if you have any PHD guys. He said none zero. Maximum qualification they had was BSC which was quite astonishing to me.

I couldn’t go beyond 30 minutes because I found him to be too confusing.

7 Likes

hi Dhiraj @dd1474

What lesson did you learn.

I am keen to know how you will avoid a company like this in the future

Their audited statements, quarterlies, etc had no signs of fraud as far as I tried to see

Thanks for your support and answer

Find enclosed my learning experience (more on errors) in FY18. Please note that this presentation my individual opinion and do not claim any authencity/correctness of data. I may enter/exit in the companies mentioned in the presentation in future subject to favourable risk reward in my opinion. All three companies named in presentation, I have invested in past. My bad experience may be due to my limitation, wrong entry/exit prices and these companies are as good/bad as any other listed companies in my opinion. The objective of this presenation is to highlight factors are considered for entry and exit rather then passing judgement of companies named in the presentation. Without name, the reader would not have been able to associate and hence I have kept the name in presentation.

Discl: I have tracking position in Arrow and Premco. Exited from Faze three. Investors shall do his/her own due diligence before making any investment decision.

Experience in investing FY18.pptx (614.5 KB)

5 Likes

@varadharajanr, @valueinvestorap, @dd1474 : I was just randomly walking through threads and reading about interesting posts. I came across this one. Not pointing fingers at anybody, but you guys have done such diligence over time. But centrum, a professional company initiating coverage in last September and price of stock and financial performance being where it is now , shows why retail investors like me should visit valuepickr. Thanks for all your work.

3 Likes

thanks for mentioning my post. you only had to turn their product to the back to find out it was not made in india but “made in taiwan” and the comapny didnt have even an FSSAI number which is a pre-requisite for any food/ingestible manufacturer in india.

when the company said they didnt have a FSSAI number, i became surer of my thoughts.

7 Likes

Now they are planning to raise capital via Rights. Issue price is 36 per share. Meeting finished in 30 mins.

Closure Intimation from Gujarat Pollution Board - https://www.bseindia.com/xml-data/corpfiling/AttachLive/53fe892d-108e-42ef-a10a-533973c0aa48.pdf

It was not functional since Oct 19 due to a fire accident.

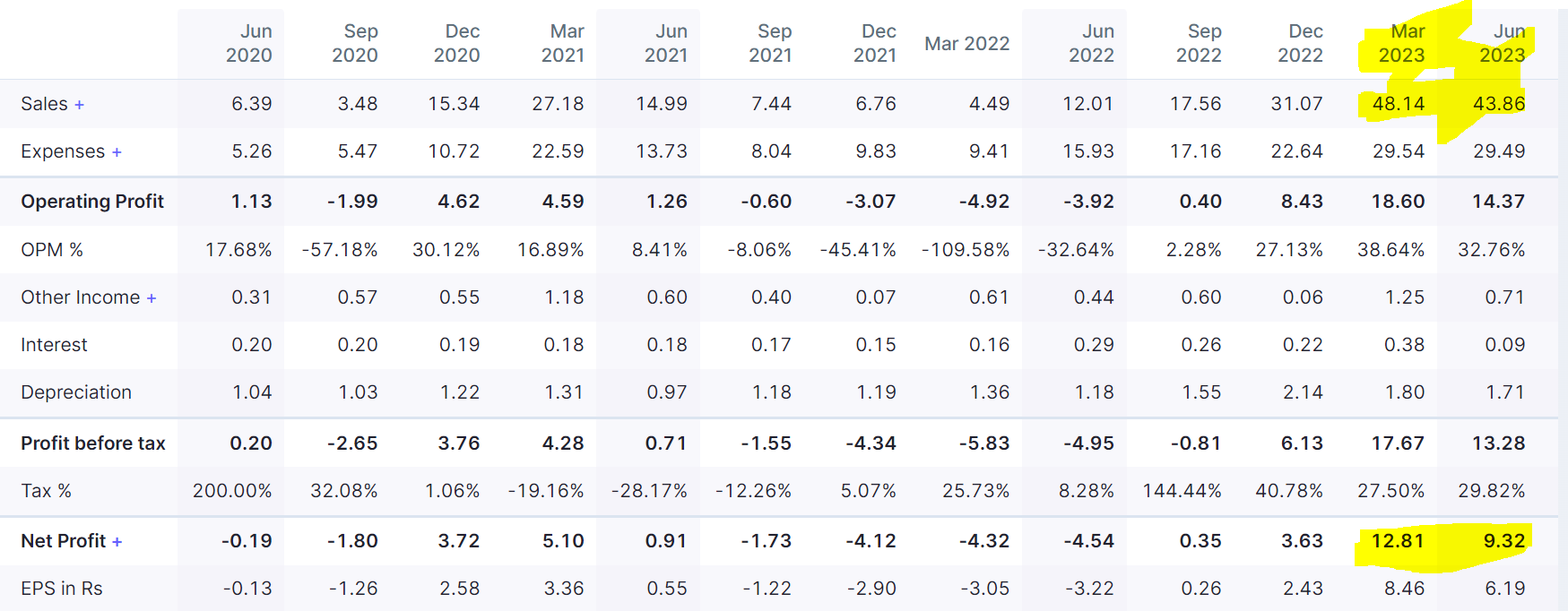

What is current view on company, after it came out with excellent March 23 qtr results.

Is March 23 qtr results sustainable? Or its just begining, results will improve in coming qtrs?

I think this company deserves a fresh look. Seems lots of thinks have changed in the company off late.

Key points

-

Recorded record Revenue and profit in Q4 and Q1

-

Contrary to earlier bulk of the revenues are coming from manufacturing and selling (Contrary to patent and license revenues earlier).

-

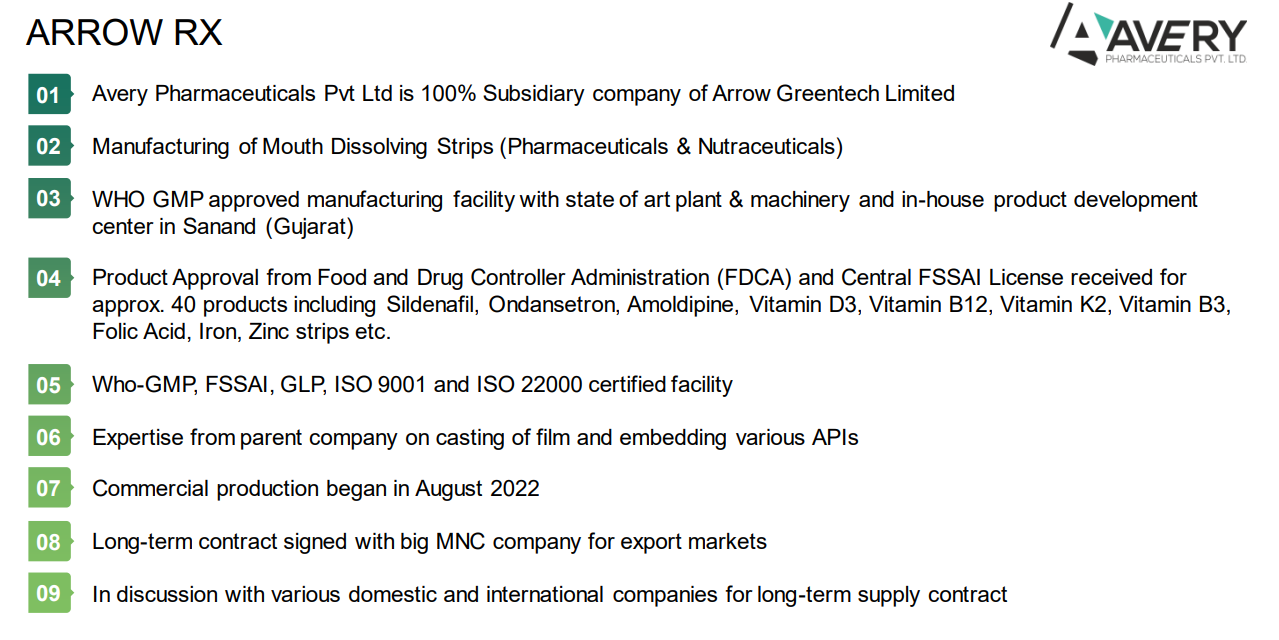

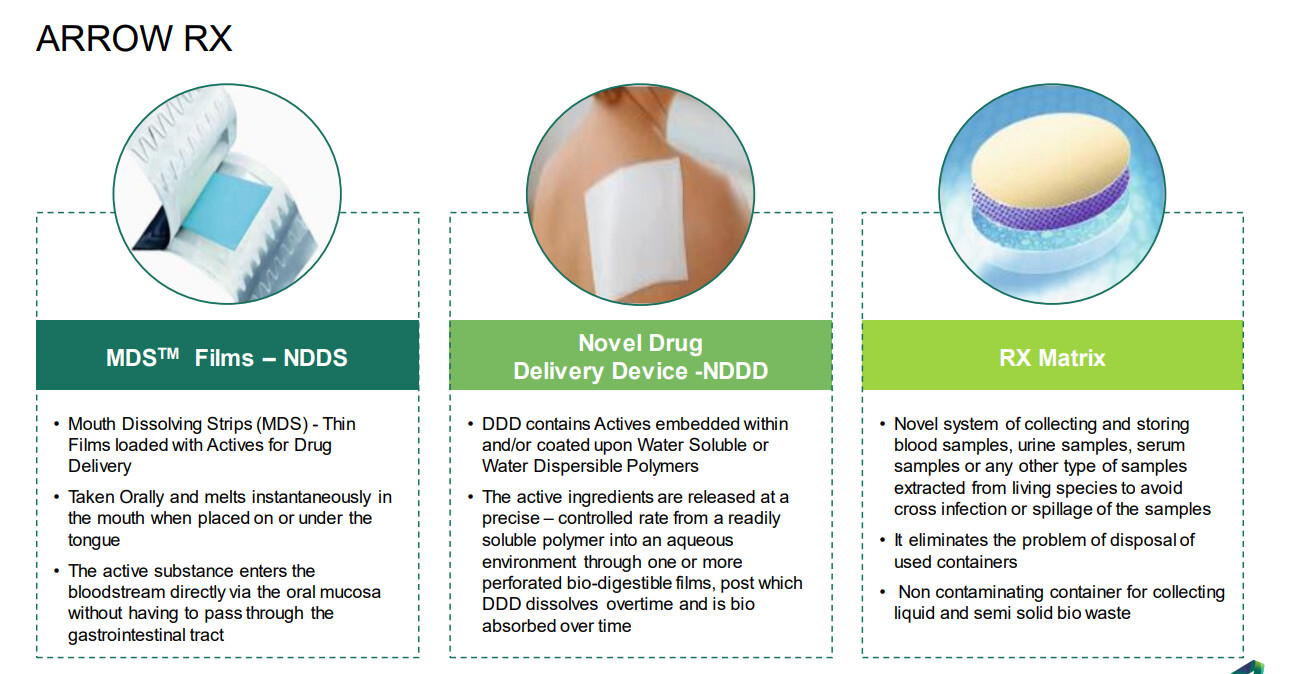

Have ventured into Mouth Dissolving Strips (MDS) through wholly owned subsidiary Avery Pharma. (The revenues are yet to materialize but seems lot of optionality’s in the pipeline).

-

Bulk of the revenues seems to be coming from Security products (Anti Counterfeit threads, passport security, brand protection etc) . 68 Cr Revenues in FY23 from this segment V/s 23 lakhs in FY 22 .

-

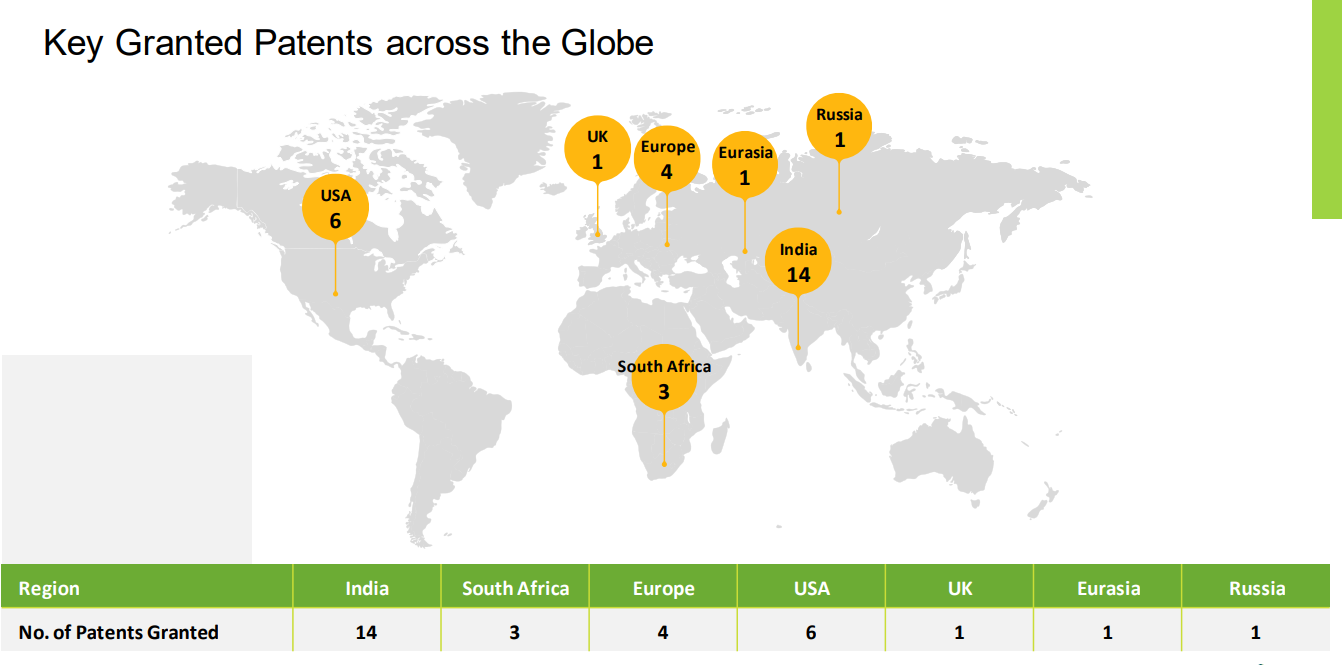

30 patents granted and another 28 patents in India and 8 foreign applications in the pipeline (Many of the patents are available in google patents on a cursory search)

-

Company coming out with a presentation after 2019 for the first time, shows the pic of the plants in Ankaleshwar and Sanand . Avery pharma is actively recruiting . (These were red flags as evident from this thread ).

Its Annual report and presentation is descriptive and concise. Posting the key points in Management discussion and Analysis . The items in italics is my assessment / thought (to be taken with a pinch of Salt ![]() )

)

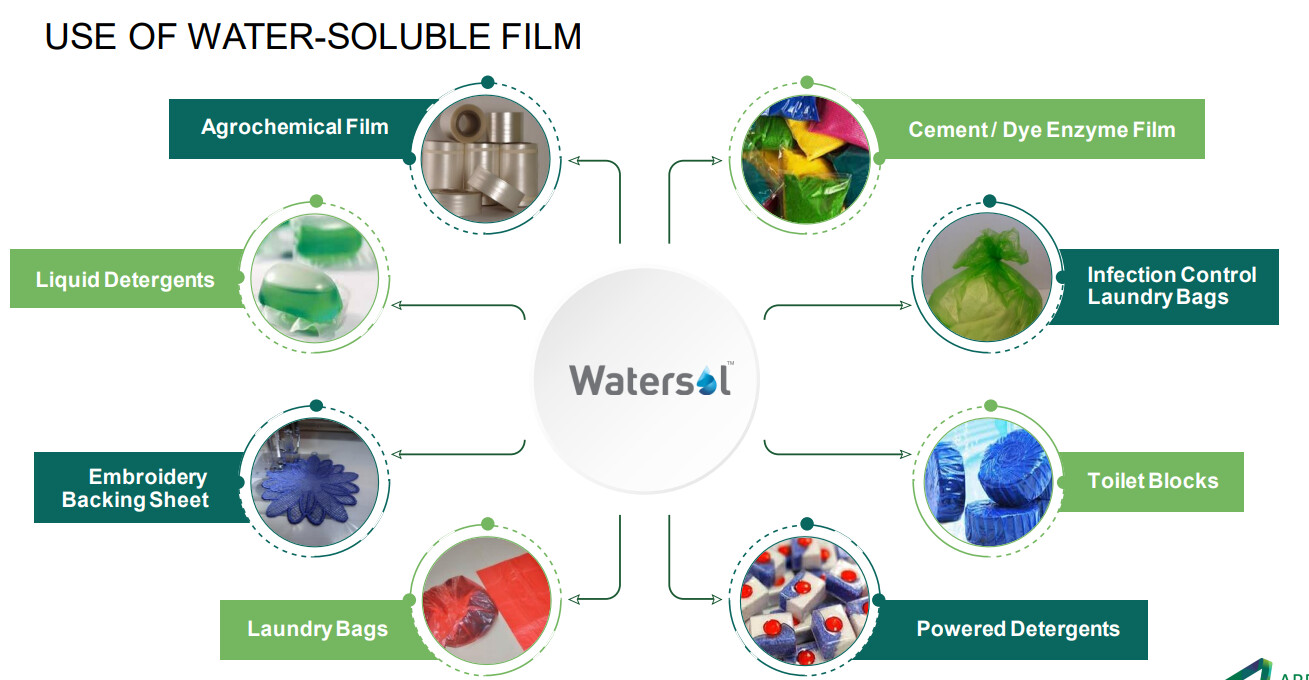

A. Water Soluble Film (Watersol®):

Arrow Greentech Ltd (AGTL) is one of the world’s leading manufacturers of cast water-soluble films. Water soluble film, the flagship product of AGTL, is marketed under the brand Watersol®. Including optimum capacity utilisation at the Ankleshwar, Gujarat factory,company is focusing on new business development through innovative applications across segments. This shall expand, and strengthen, our growth pyramid for the future. Watersol® films have versatile yet specialised applications across industries,including Agrochemical, Construction chemicals, Dyes & Pigments, Embroidery, Health & Hygiene, Industrial engineering, Water transfer printing, home care and many more.

AGTL’s PVA films are water-soluble, biodegradable, and customisable, making them ideal for various new product development applications. These properties enable the films to be used for innovative packaging for water treatment chemicals, swimming pool chemicals, concrete fibre, construction chemicals, and various inhibitors and repellents for industry and consumer use. AGTL plans to expand its capacity and product base by adding significant capital expenditure (CAPEX) in the coming times. This will activate other new business opportunities across geographies and business segments.

They have a plant in Ankaleshwar for Watersoluble films (WaterSol brand). This segment contributed to 23 Cr revenue in FY23 V/s 15 Cr in FY 22. This business is part of the green vertical and has opportunity to scale up due to the thrust towards enviornment /bio degradable etc.

B. Bio-Compostable Products (Bioplast®):

Plastic made from petrochemicals is not a product of nature and cannot be broken down by the natural degradation process. AGTL’s initiative into bio-compostable business is likely to be a game-changer in terms of alternatives to conventional single-use plastic packaging. Moreover, the machines being used to

produce conventional plastic films can also produce Bioplast (eco-friendly bio compostable) films by making small changes in it.This ensures no operational disturbances to plastic manufacturing company’s set up, assets, and skills.

AGTL has a technology for manufacturing the Bioplast film from Biotec, Germany that is compliant with the European standards -EN 13432 and ISO 17088. The final product is 100% bio-compostable, made from renewable plant resources (potato starch, polylactic acid, etc.), and has a diverse range of applications such as garbage bags, garment bags, industrial and commercial packaging, disposable dishes, straws, and food containers, etc

This product is mentioned as a trading item in the AR in the Notes , so I feel the plant and machines etc are yet to get commissioned.

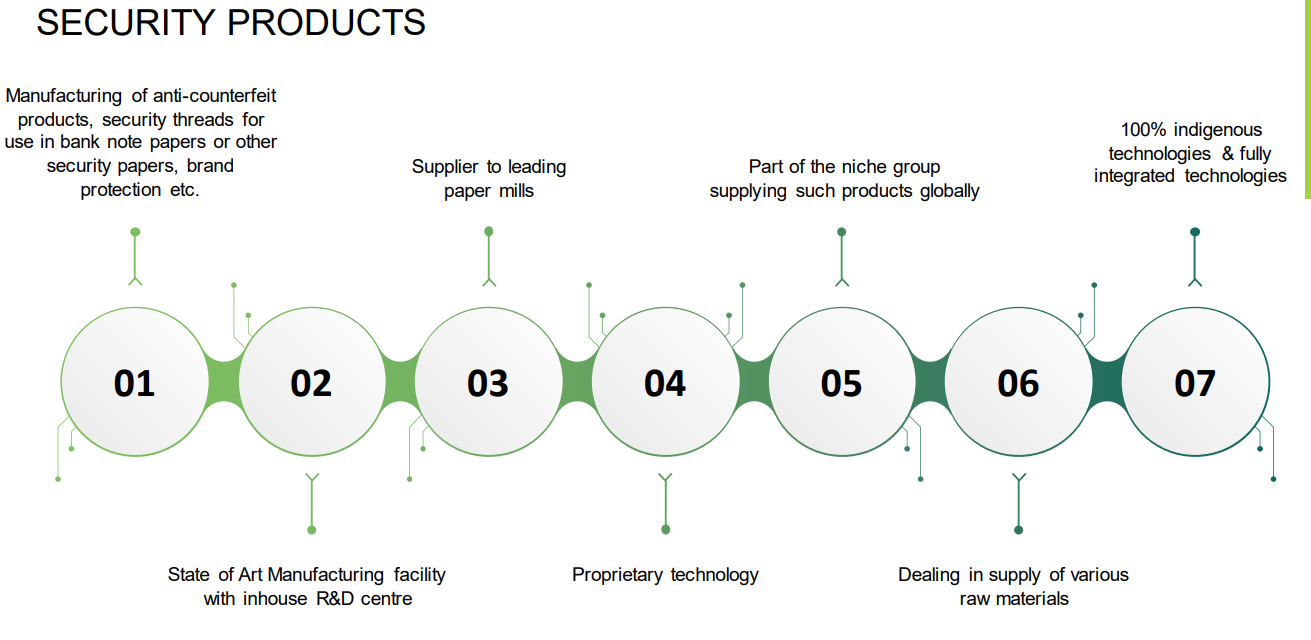

C. Security Products:

AGTL has an impressive patent portfolio of security products and brand protection. These patents are having an impact on various products—like Anti-counterfeit Threads, Passport Security, Brand Protection, Paper etc. AGTL investments are focused on high security elements related to Currency sector, with the viable option of adapting the technology for high value brand protection. Counterfeiting of high value products, including pharmaceuticals packaging will go a long way in promoting this segment of our company. AGTL has filed several patents and secured National and International grants to rights of claims, for atleast 5 patents, while few are

in examination phase. AGTL has invested in a high technology plant to manufacture Anti Counterfeit Thread and security films. It entails multiple facets of metalizing, demattalising, holography, nano printing, nano security element, functional, coatings, including embedding of machine readable taggants and lamination. Products are being designed to be fully embedded or windowed embedded in Security Papers, Tax Stamps and brand protection of high value perfumes, cosmetics, and pharma-vaccines etc., including track and trace management.

This segment seems to be the reason for a huge turn around in the company is the last year. This segment contributed to 68 Cr revenue from virtually nothing in FY 23 . While they are talking about plant was not able to figure out the same . Need to dig further …

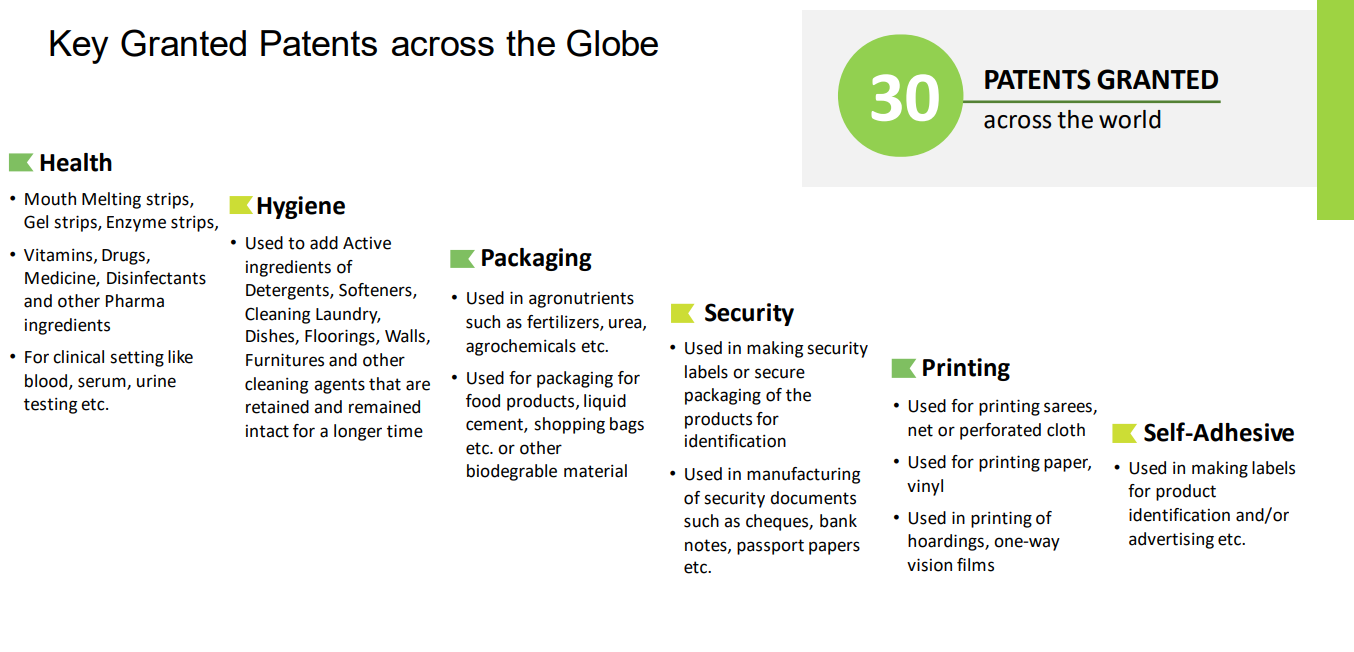

D. Patents and IPR:

Arrow has always upheld the belief in securing our markets through strategic filing of Patents in India and abroad via the PCT route. We maintain dedicated Intellectual Property Cells in Arrow India and in our various subsidiaries for this purpose. We are elated to inform you that our commitment to Innovation and excellence and our contribution to our country’s GII advance, has culminated in recognition by CII and DPIIT (Ministry of Commerce, Govt of India). Arrow has received the National IP Award,every year since 2019 barring year of Covid—2020 (i.e. received the National IPAward in 2019, 2021 and 2022 from CII.)

The patents and IPR seems to be a real strong point for the company . Most of us will be skeptical (and rightly so) that this is unlike a 500 Cr company. But these claims are verifiable. They seem to have a won accolades and some of it was listed in google patents portal.

F. Water soluble edible film – Mouth Dissolving Strips (MDS):

AGTL has invested in its wholly owned Subsidiary Company namely, Avery Pharmaceuticals Private Limited (“Avery Pharma”) for manufacturing of Mouth dissolving strips (MDS). Avery Pharma is a specialty pharmaceutical company bearing prestigious approval of WHO-GMP and other accreditations with GLP, FSSAI, ISO 9001:2015, and ISO-22000 Certifications. The manufacturing facility has a state-of-the-art manufacturing facility & German-designed machines to undertake dedicated

manufacturing of patented Mouth dissolving strips technology. MDS are fast-dissolving films that release API quicker than the other formulations like tablets, capsules, oral disintegrating tablets, chewable tablets, and liquid dosage forms. These films are formulated to self-dissolve upon contact with saliva, omitting the requirement of additional fluids for consumption. MDS are quick in action by releasing drug instantly. The strips ensure quick absorption and instant bioavailability of drugs. MDS is highly suitable for geriatric, pediatric, mentally challenged, bedridden,

mucositis, Dysphagia, veterinary. MDS offers irrefutable benefits like self-administration ease, without-water usability, Quick onset of action, non-invasive dosing methodology & patient convenience.

Avery Pharma has entered long-term collaboration and started commercials production for leading MNC with a novel & unique patentable combination of product for the Brazil market and is working on to launch multiple products in other markets. Avery

Pharma is also working on clientele-patented new product Development project under the Contract development and Manufacturing model (CDMO). At present Avery Pharma has 40 + products are approved under FSSAI and 10 + products approved under Rx. Avery has applied test license for more than 20 Rx products and soon will be completing with development phase for these products. Avery Pharma

has already filed a patent for two innovative products that are being commercialized in the market and few more innovative products are under the pipeline for patent filling. The research lab has also successfully developed a combination of API in MDS technology, loaded higher doses of drug above 100 mg surpassing the limitation of MDS technology. New developments are underway for sublingual and Buccal MDS technology.

Company is talking about tie up with MNC for Brazil market. Need to find out more . They are also talking about CDMO opportunity in MDS and even listed approved products . (40 products under FSSAI and 10+ under RX). They revenue from Arrow pharma is not added in FY 23 revenue. This can be a big addition going forward.

**Revenue break up for FY 23 **

92 Cr revenue from finished goods

10 Cr revenue from traded goods

2.66 Cr revenue from Patent income

Finished goods : Water Soluble films, Anti counterfeit products

Traded Goods : Bio degradable resins, Cleaning products

Valuation (Back of the envelope ![]() )

)

Market Cap : 550 Cr

Trailing P/E: 21

ROCE: 21

Price : Rs 358

** If they can sustain current quarterly run rate of 10 Cr then forward P/E ~ 14. **

With optionality’s of Avery pharma , Bio degradable plant etc coming in along with PE expansion this can create wealth.

Additional work to be done on

- Patents /IP monetization

- Customers and market for anti counterfeit products. Reason for sudden jump in demand.

- Reading Old ARs to understand the reasons for lull in 2017-2022. Perceived or actual governance issues.

4)MNC tie up for Avery MDS and CDMO opportunity. - Market for Poly Vinyl Alcohol films : Is there a tech advantage for watersol or its just a commodity . (Lots of WSF quotes available in Indiamart ).

- Research more on the high tech plant , products ,USP and markets for anti counterfeit products .

Disc: Not invested , tracking , might invest if building more conviction.

Apologies for a longish post ![]()

10 Likes

Appreciate your efforts Midhun.

Very detailed and informative data points.

Quick question why Avery pharma numbers not included in the consolidated figures.

what % of holding listed company has here.

2 Likes

Hi Shahid

Thanks for the kind words.

Avery pharma is a 99% owned subsidiary of Arrow. As per AR notes in 2023 they have generated just 36 lakhs revenue and 5.3 cr loss .

1 Like