The translation for the first link is that some employees have stolen the insulin injections supplied by palepu pharma to Apollo

Though below response highlights its some other issue but company do have related party transactions and this needs to be taken with cautious. Mgmt provides reason in calls that they do it on arms length basis which audited by reputed lawyers but we should always take management response position with pinch of salt. A risk is a risk. Disc : Invested

Management has said that next 6 months they will try to reduce pledged shares as much as possible. Also, the pharmacy deal should give them cash and let us see how they use it. Further, Debt would peak out in Dec and with capacity utilization picking up, This should come down going forward but need constant monitoring unless comes down to comfort levels

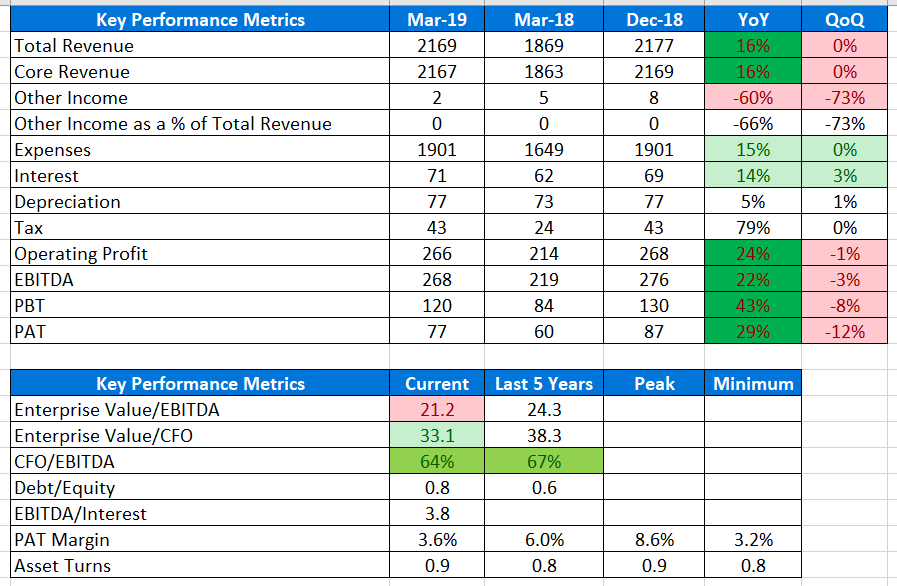

Good results due to operating leverage story, expansion growth drivers in hospital, store expansion and store operating leverage based pharmacy and reduction in losses of AHLL continues. Company posts high double digit topline and bottomline growth.

Key Takeaways from call:

- High single digit growth in matured hospital and double digit growth in new hospitals

- Navi Mumbai hospital worked at 150 bed and is EBITDA positive . Plan to take it to 200 bed this year

- Good improvement in store level profit like revenue per store, inhouse brand sales leading to overall improvement in pharmacy margins. Margin growth + 400 new stores led to ribust growth

- Fixing issues in some AHLL hospitals along with revenue growth led to better margins and reduction of losses. Trend to stop for Q1 FY20 due some annualizing expenses and then management further expects same trend to continue from Q2

- Debt has peaked out. 200 cr of promoton capx pending. Also, annually, there would be 200 cr of maintenance capex and 250 cr of working capital needs.

- Management expects to bring down debt from 3200 cr to 2500 leveraging cash generated from pharmacy sales, cash flows and some deals which they are expecting to finalize in a month

- Management also plans to bring a strategic investor for proton therapy and create a separate SPV to separate P&L and balance sheet items

- improvement in ARPOB due to improvement in case mix driven by CoEs

- Pledge has reduced by 10% from 78% to 68% and management expects to get rid of pledge in a year post loan reduction due by methods mentioned

- No major capex planned further and expect operating leverage story to continue

- Waiting for more regulatory clarity on digital pharmacy

Q4-FY19-Earnings-Update.pdf (1.3 MB)

4 Likes

One must ask if 100% of revenue is accounted as we can easily verify it by visiting the hospital. I use this hospital for regular outpatient visits and every alternate week, they force cash payments. The bills given during these forced cash payments are not computer generated and look like generic bills that don’t even have bill number.

1 Like

Another crook Promoter

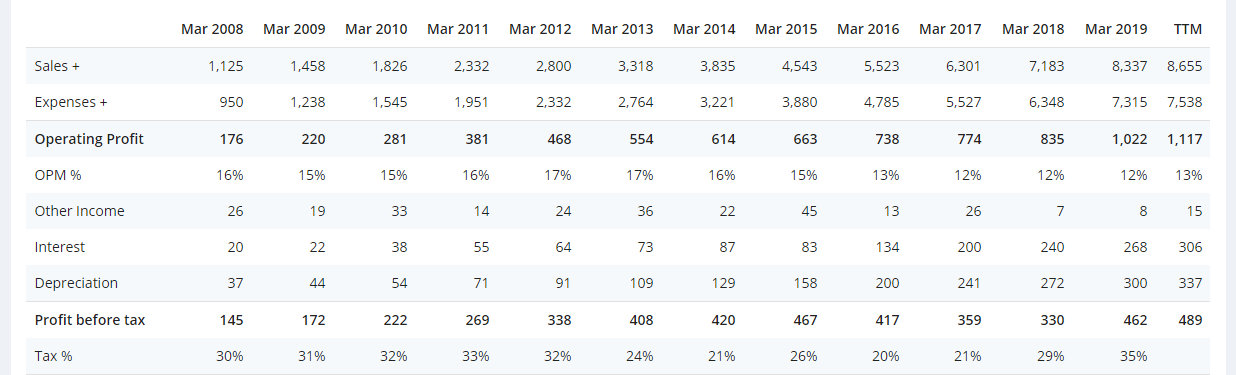

Apollo’s back on track by doubling its bottom line in FY19

I think Apollo Hospitals would be one of the best bet in Healthcare after latest Tax Cuts.

As per Screener data it 35% Tax in FY19.

Along with this few other positives for this company are:

-

Promoters positive intentions to bring down pledged share percentage.

-

HDFC Apollo Munich Buyout

-

Pharmacy Front end spin off

-

Management focus on improving the ROE on existing investments rather than new Capex.

-

Structural Transformation in health care sector in India.

Disc: Not invested yet. But tracking closely. Keenly interested in Apollo Pharmacy rather than Apollo Hospitals.

What you guys think about online competition in pharmacy ? I used to buy from Apollo , recently I have started buying from netmeds , 1mg they are providing good discounts compared to apollo .And get door delivery. My family spends monthly 5-6 k so the discounts really matter , I think it would same for everyone with elderly parents.

I know the discounts might not be sustainable from online but like the amazon , flipkart dont know how long they can burn money.

Many concerning observations in this report.

https://multi-act.com/a-healthcare-company-high-on-accounting-steroids/

Disc. No position.

4 Likes

Initiating Coverage report by HDFC Securities.

2 Likes

Highlights of Q4FY21 result and earnings call

AHEL’s net sales declined 1.9% YoY but grew 3.9% QoQ to Rs28.9bn during the quarter.

Hospital segment revenues grew 10.2% YoY and 7.1% QoQ to Rs15.4bn with recovery in the regular business. This was also supported by improvement in ARPOB with stable occupancy of ~63%. However, COVID-19 cases have seen a sharp jump in Apr-May’21 due to the 2nd wave. This has pushed occupancy as high as 71% but the average realisation for COVID-19 patients is lower.

TN region sales grew 5.7% YoY to Rs5.6bn driven by higher ARPOB despite lower occupancy ratio due to absence of international patients. o AP & Telangana region sales grew 19.4% YoY to Rs3.1bn due to higher ARPOB on improving payor mix despite lower occupancy.

Karnataka region sales grew 6.4% YoY to Rs1.9bn with rise in regular patients and sharp jump in outpatient volumes.

Other regions sales grew 6.3% YoY to Rs2.0bn due to higher ARPOB on improving payor mix despite lower occupancy.

Significant subsidiaries/JVs/Associate revenues grew 6.1% YoY to Rs5.3bn with rise in regular patients and sharp jump in outpatient volumes.

Proton Cancer Centre, AHEL’s oncology unit, is witnessing continuous demand from domestic patients. Revenue improved 12.8% QoQ to Rs309mn. The company believes that it can achieve an EBITDA of Rs500mn and Rs1bn from this segment in FY22E and FY23E respectively.

AHLL segment saw healthy recovery with revenue growing 25.8% YoY (+6.7% QoQ) to Rs2.1bn. Apollo 24/7 witnessed strong traction and it was able to funnel more patients into AHLL, particularly the diagnostic segment. The company is targeting a revenue of Rs3bn in FY22E and Rs5bn in FY23E from the diagnostic segment.

New hospitals reported a revenue growth of 30.1% YoY (+12.4% QoQ) with an EBITDA margin of 15.1% during the quarter.

Pharmacy business revenues declined 17.7% YoY to Rs11.2bn However, adjusting for the demerger and high sales post lockdown in Mar’20, growth stood at 10-11% YoY. Company is targeting an addition of 300-350 stores in FY22 with high double digit growth supported by Apollo 24/7.

Company has vaccinated ~45% of the total private vaccinations in the country till date and expects to vaccinate an additional ~8-10mn people in the next few months. Despite price-caps, Apollo expects some margin.

Company has reorganised its segments; Apollo 24/7, backend pharmacies and pharmacy retail business into a new department called Apollo HealthCo. It will be an omni-channel healthcare platform integrating its online and offline services.

Currently, it has 10mn customers which is expected to rise to 80-100mn by FY25.

Potential revenue from this segment is ~Rs2.5bn by FY25. Company has invested ~Rs2bn and expects to invest ~Rs1-1.5bn in the near term.

Source ICICI SEC

1 Like

The main business of hospital is human business. But Apollo seems to get out from this rat race by diversifying into Pharma and Diagnostic businesses. I think this then will help mitigate the high attrition rates that hospitals face.

Healthcare - Medical tourism to come back in a big way now

Apollo Hospitals - Online pharmacy business grew 3 times in H1FY23 & is expected to maintain high growth trajectory. As the overall occupancy is just 68% there is a significant room for growth. However, for the medium-term, company is in an investment phase & plans to add 2000 beds with a capex of Rs 3000 crore.

1 Like

The 2000 beds will be added over three years. Its a strong group - immediate improvement may come from occupancy rates going up, international patients coming back to pre-covid levels, case mix leading to improvement in margins, expansion of diagnostics business etc. Even then, given RoCE of about 14-16%, company commands a high PE (~72-75) basis trailing twelve months EPS. One wonders if the company will be able to achieve enough growth to justify these valuations.