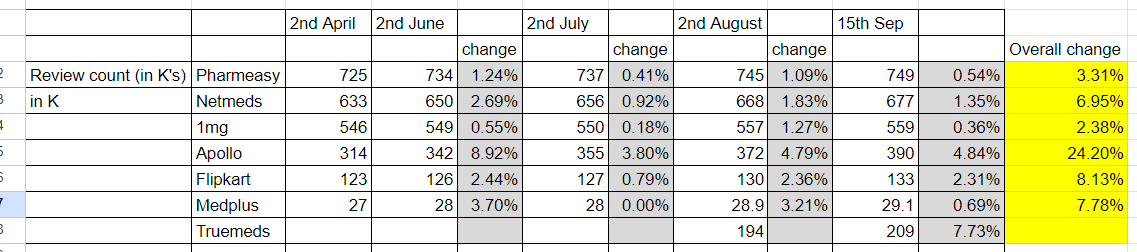

I was trying to collate some play store data about where the incremental interest is going on for online players vs omni channel players. This data cannot be directly correlated with sales, but this can give some indication

1 Like

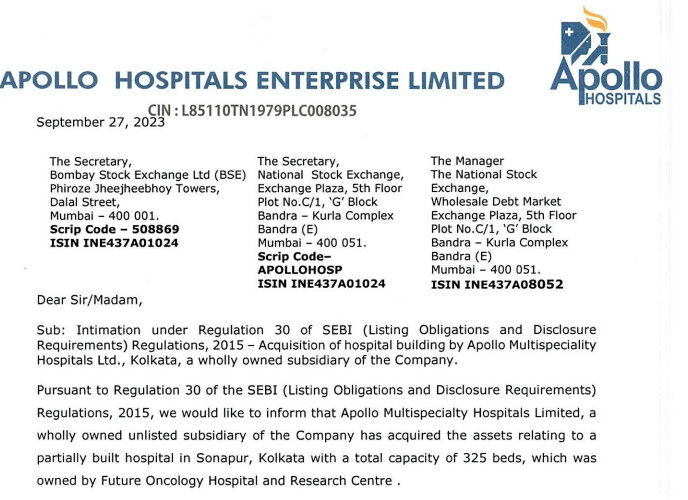

Acquisition oncology - partially completed hospital in kolkataa 300 odd beds

hi all…Is there any thread of Max Healthcare on Valuepickr? Pls guide me to it or if somebody has discussed in detail in some private thread?

2 Likes

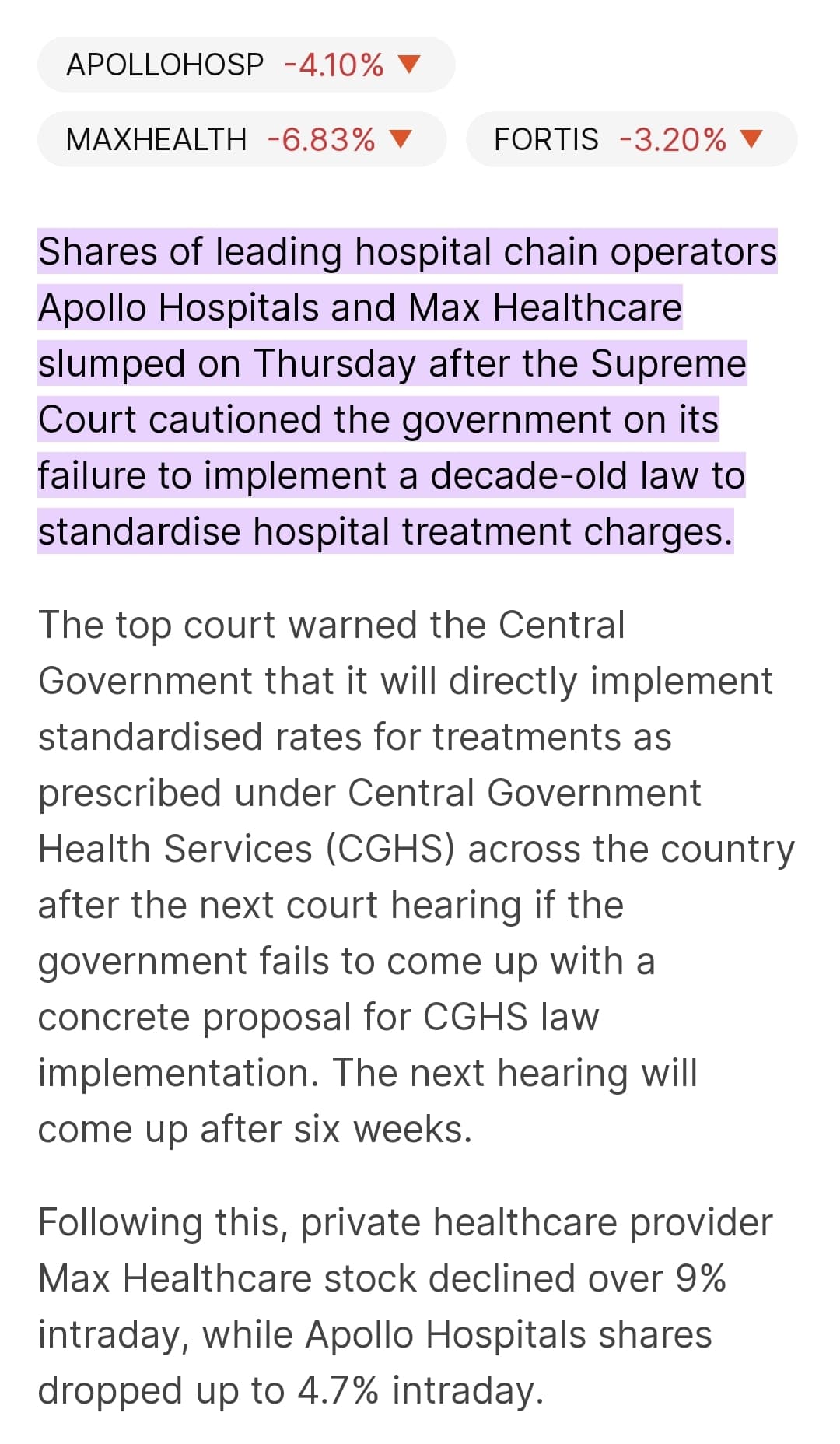

Today One of my portfolio holding, Max Health care was down by 7% . Above is the reason for it. If any of our group members are holding hospital stocks, what is the way going ahead? Will this standardisation rates be a reality ? And Supreme Court is talking of implementing it in 6 weeks, is it a great threat for hospital companies going ahead? How we should look at this?

3 Likes

2nd order impact : “Bhai max cover insurance buy krni ki zarurat kya hai ab firr”

More or less regulations are ok but capping things will lead to hospitals and medical setups figuring out workarounds.

Stunt cost and bypass surgeries are already capped to large extent thnx to modi. But Medanta mostly charges u an extra 1-2 lacs for invasive procedures (eg laser angioplasty) Till last year that was not covered with insurance and it does make sense to do if as a patient u are well to do.

Plus private capex is much needed in the hospital space so they might need to weigh that too vs just being populous.

Just playing the devils advocate.

Also, whats the potential impact on Narayana as they mostly do specilised treatments/surgeries? Current fall in NH share on the back of this development offers good margin of safety, given the company is consistently growing at 20% EPS and valuation (EV/EBITDA) appears reasonable vs peers.

Any thoughts?

1 Like

At the moment the valuations look way too stretched. With the bed additions still a year away; I am confused if we should even monitor the company and add at lower prices. What valuations will be justified. Any inputs will be valuable.

To me anything above 2x the PEG ratio seems totally unjustified even for large companies and even in bull markets. I am confused if I am missing something. It would be great to get some inputs.

2 Likes

Large caps and that too hospitals should not come cheap in markets. Also, please remember the Apollo 24x7 stake sale that is being discussed widely - if that sees the end of the tunnel then monetisation will help balance sheet. Also pharmacies have been doing well. So optionalities are there and folks might be valuating at SOTP and just not standalone.

The return ratios of Max Healthcare are better than Apollo hospital…How you value the current valuations of Max healthcare? And also going ahead, which business model is on superior growth trajectory???

It seems they have to merge their retail pharmacy business and Keimed - their distribution business to take funding from advent. Apollo issue is their CG - your pharmacy buys medicine from distributed company who is separate entity owned by one of your promoter.

2 Likes

Off topic or maybe not - are there any regulatory barriers for Q comm players to enter into medicine delivery?

1 Like

Interesting… They need license like netmed or 1mg, I don’t think there is any challanges. But TAM may not be very attractive and SKU may be too high.

In general online selling of medicine (pharmeasy like) is not that succesful vs general online selling (Like flipkart), the reason is proximity, medicine is availble nearby store and those are plenty.

Best selling items for Amazon / flipkart are: Clothings, Fashion items, Wall decoration etc. Whereas Q com sells most like condoms, banana etc. With that mindset, medicine will be Q comm target areas.

Interesting to think more…

1 Like

I know acute medicines are high margin business… what better than Q-comm to supply meds? If its just a license, they could always get it. But I see no reason why meds shouldn’t be a logical expansion in next 2-3 years for Q Com players.

EDIT - just noticed that Q-Comm is also selling a lot of nutracueticals… zincovit, shelcal etc and painkiller meds - Crocin, Saridon, Disprin, etc. I’m not sure why they can’t also do limited asortment of popular meds. Take rates are far higher in this segment if I just go by gross margins of MedPlus etc (19/20%)

EDIT 2 - Just read the Blinkit acquisition letter by Zomato and they did mention OTC Pharma as a natural extension. So, I guess there would be some overlap there for sure.

Sorry but i think TAM has always been attractive + Zomato/Blinkit can’t deliver medicine.

Also, for some medicines u need prescriptions which is a hassle to carry everytime around when going to buy medicines physically. Even though online medicine is solving a smallish problem but still i think its a super attractive proposition for a ailing person living in a nuclear family who eventually has to be looked at by one person in the house at that time. So online medicine deliveries are somewhat a essential for some segments of the society.

Also, when it came to Apollo Pharmacy, they are actually doing a great job at creating physical touch points or locations near residential areas. So the business model is anyways a good one. Plus addition of distributors from time to time is also going to help in reaching economies of scale.

Also, given Apollo is a omnichannel play already vs others like 1mg etc so it makes a 100% sense for them to tap the online piece. Ppl can have other views which is invite sincerely.

2 Likes

Can anybody help me understand the deal between Advent and Apollo healthco where if they made so and so return, management of the healthco will receive some incentive.

Management in concall said, if they achieve 2.5x, advent will share 0.6% of market cap to management and for 4.5x, they will share 0.8% of market cap. As per my understanding advent will share their ownership or proceeds from the sale of their share to compensate management and there will no dilution in overall shareholding. So this deal has no impact to other 88% shareholders

Is my understanding correct

1 Like

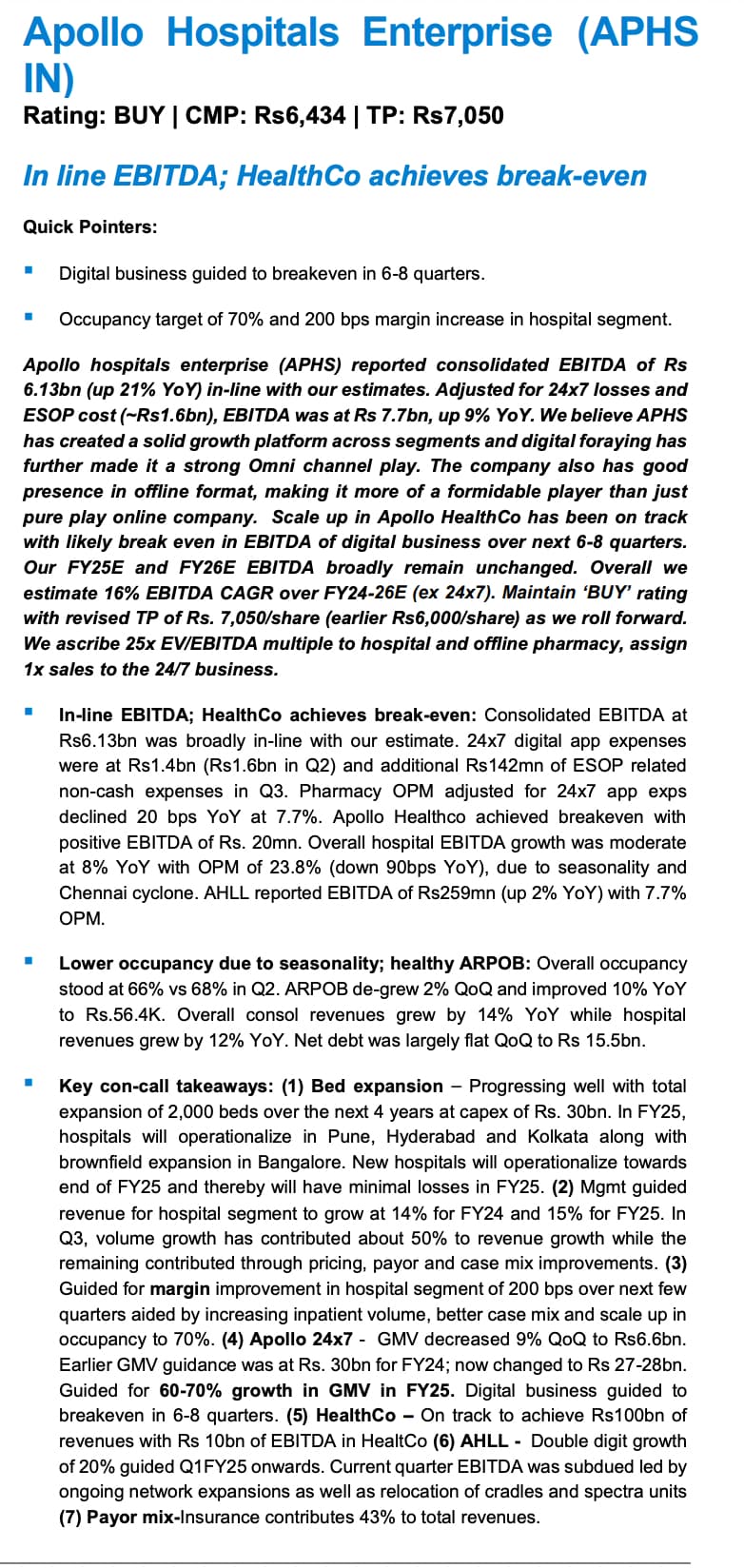

- Consolidated revenue at ₹5,842 crore in Q1 FY26 (+14.9% YoY; +4.5% QoQ), driven by broad-based growth across healthcare services, retail health & diagnostics, and digital health businesses.

- EBITDA ₹852 crore (+26% YoY; margin 14.6%, +130bps YoY), supported by cost controls and higher mix of complex/specialty care; PAT ₹433 crore (+41.8% YoY, +11% QoQ). EPS: ₹30.10.

- Healthcare services revenue ₹2,935 crore (+11% YoY), EBITDA ₹718 crore (+15% YoY; margin 24.5%, +83bps); PAT ₹384 crore (+18% YoY).

- Retail Health & Diagnostics (AHLL): Revenue ₹435 crore (+19% YoY), EBITDA ₹40 crore (+31% YoY; margin 9.3%, +90bps), PAT loss narrowed to ₹8 crore.

- Apollo HealthCo (Pharmacy & Digital): Revenue ₹2,472 crore (+19% YoY), EBITDA ₹94 crore (up from ₹23 crore YoY); achieved PAT ₹57 crore (PY: loss). Platform GMV ₹682 crore (+23% YoY). 1 million new users added. Online pharmacy transaction growth +42% YoY; transacting users +36% YoY.

- Omnichannel pharmacy and digital business demerger underway; targets ₹25,000 crore revenue and 7% EBITDA margin by FY27. Demerger completion timeline: 18–21 months. Digital yet to break even, management expects breakeven by Q4 FY26.

- Bed capacity at 8,030 as of June 30, 2025. Occupancy 65% (vs 68% YoY; -300bps), inpatient volume +3% YoY, ARPP (Average Revenue Per Patient) +11% YoY. New capacity: 700+ beds in FY26; plans to add 4,300 beds, capex ₹7,600 crore over 5 years. Four new hospitals to be operational in FY26 (Delhi, Pune, Kolkata, Bengaluru).

- International patients revenue share: 7%. Healthcare margins improved 89bps YoY; complex/surgical mix and focus on specialty care cited as drivers.

- Bed addition/expansion cadence: Mgmt reaffirms 4,300 beds by FY30, ₹7,600 crore capex.

- Omnichannel demerger—value unlock timing: Mgmt targets 18–21M completion, expects 7% margin at ₹25,000 crore by FY27; digital break-even by Q4 FY26.

Composition scheme has been approved which will demerge the Pharmacy and Digital Health from the Hospitals business.

Hospitals going through a heavy CAPEX cycle as well [8300Crs of which 5400Crs are remaining to ve spent in the next 5 years]

Will this unlock value for the company?

45% revenue comes from the Pharmacy and Digital Health while 55% comes from Hospitals.

1 Like

Below are back of the envelope calculations on valuation of Apollo businesses.

Note: Numbers used are ESTIMATES to arrive at BALL PARK VALUATION range.

| Hospital / Healthcare | Min | Max |

|---|---|---|

| EBITDA (cr) | 2700 | 2800 |

| EV/EB | 29 | 32 |

| Valuation (cr) | 78300 | 89600 |

| Disgnostic + Retail Health | Min | Max |

|---|---|---|

| EBITDA (cr) | 155 | 175 |

| EV/EB | 25 | 30 |

| Valuation (cr) | 3875 | 5250 |

| Pharmacy & Digital Health | Min | Max |

|---|---|---|

| Sales (cr) | 9100 | 10000 |

| P/S | 1.0 | 1.2 |

| Valuation (cr) | 9100 | 12000 |

Combined Value of Entity could be ~Rs91,000cr - Rs107,000cr. Current MCap is ~ Rs102,000cr.

SEBI Disclosure: https://www.bseindia.com/xml-data/corpfiling/AttachHis/b05b3d6e-7db9-49cd-8065-1553478d4543.pdf

Latest Deck: https://www.bseindia.com/xml-data/corpfiling/AttachHis/4430a828-14c2-4c64-8cff-b68f1a2904f1.pdf

Disclosures: No Investments. Not a SEBI registered analyst. Above post is for discussion purpose only. Please do your own due diligence

1 Like