Dear @suru27,

Point noted.

What ever you said has been been absolutely right, and corporate hospitals were able to generate some profit till now but I only want to stress the point that with the upcoming legislations in various states( Delhi, Taminadu), national medical commission bill, modicare insurance schemes the whole scenario is going to change… The new regulations are going to tilt the balance heavily in favor of smaller establishments.

The corporate hospital business is inherently inefficient business for hospitals for following reasons

- Moat:The only moat they have is quality of care and experienced doctors… With capping of surgical and procedure costs, they are going to loose the moat as there is no differential pricing for various surgeries in New proposed legislation with regards cost incurred for maintaining quality. I am an anaesthetist so I can give you examples in anaesthesia… For a small surgery like laproscopic cholecystectomy the cost of anaesthesia procedure in a small nursing home can be as low as Rs 1000 while the same in a corporate hospital would be Rs 15000/… The smaller nursing can charge Rs 5000/ for anesthesia (400% profit) while the corporate may not be able to charge more than Rs20000/(33% profit)… Of course there would be huge difference in quality of anaesthesia care…The smaller hospital is not giving proper anaesthesia but what we call jugaad anaesthesia…Bigger hospitals may not be able to drop standards for fear of litigations, as they are dealing with different class of people… believe me the most difficult people to handle is those belonging to upper middle class who would come prepared (with Mr Google as there guide), with lots of complaints and questions with regard quality of healthcare but behave poorest of the lot when it comes to payments.

- Smaller establishments can pick and choose profitable procedures and surgeries while bigger corporates may not be able to do that.Smaller establishments will simply refer sick patients(unprofitable) to tertiary care hospitals, while tertiary hospitals can’t refer anywhere, they must admit and treat all patients.

3.Bigger hospitals need to maintain unprofitable support specialities, while smaller nursing came either outsource them or get services of inexperienced non specialists doctors.

There are numerous other reasons which I can go on and on.

Just go through all the proposed legislation changes while keeping in mind above reasons and you will get all the answers you need.

The next 5 to 10 years are going to be extremely difficult years for corporate hospitals. This mindless consolidation forced upon by the government will take time to settle into a more meaningful consolidation… The government must realize that you cannot settle costs of healthcare merely on popular demands of people.

Lastly many people think that corporate hospitals pay huge salaries to doctors so some of these legislations can bring the costs down by bringing salaries down… Actually speaking these hospitals pay huge salaries to only a few dinosaurs(which our Indian society has created), while the rest 99% of doctors are paid very poorly, so there is no way you can reduce their salaries any further. Unless the mindset of general people who created these dinosaurs changes. The mindset of people from South India is a lot better, so corporate hospitals in South India are far more efficient… I don’t want to start North vs south debate ( Myself i am a North Indian)

7 Likes

Apollo Hospital is indeed the leader in healthcare companies in India. There is lot of transactions going on in healthcare companies. Although I initially bought Max India only for Health Insurance, I am not able to understand is Healthcare a good long term investment from India perspective? With companies struggling to make profit, investing in best doctors, research and equipment will add to the woes, perception issue is another thing.

One thing I am not able to understand is why some big PE firms are on the buyer side. Apart from current low valuation, what other good they see in healthcare companies as long term investments that we are unable to see?

Reading all this, I am sad not only as an investor but also as an Indian looking at where the healthcare is heading. I have huge respect for Dr Reddy who created Apollo a lot…as the first man who bought quality heathcare to India. He struggled to create Apollo, government approvals, etc etc. He did that when he saw people in need had to go abroad and only the super rich could do that…he brought world class facilities to middle class and upper middle class in India itself…he created the best for India…I do not think this should be destroyed by policies. I think India needs Apollo, Max and fortis…India needs this quality…I felt bad when came to know that the best stent which is dissolvable is no longer available in india…ultimate losers were patients…middle and upper middle class and poor class people who turn middle will be ultimate losers if more Apollo, max and Fortis do not come up!

I think these hospitals need strong management to rethink the model. Max said in annual meeting that this year was a reset. I believe that these hospitals are not to perish but stay, quality is to stay…and improve…health insurance penetration and comprehensive insurance covers is one thing that will drive it and secondly more satellite clinics model for main hospitals can be a change of business model…sooner or ater government will realize and most importantly people will realize that they need this quality

2 Likes

Q1 results out. As expected operating leverage kicking in. Good revenue growth and margin expansion in a challenging market . Looks market too responded to result with some good spike

Will post concall notes in few days

1 Like

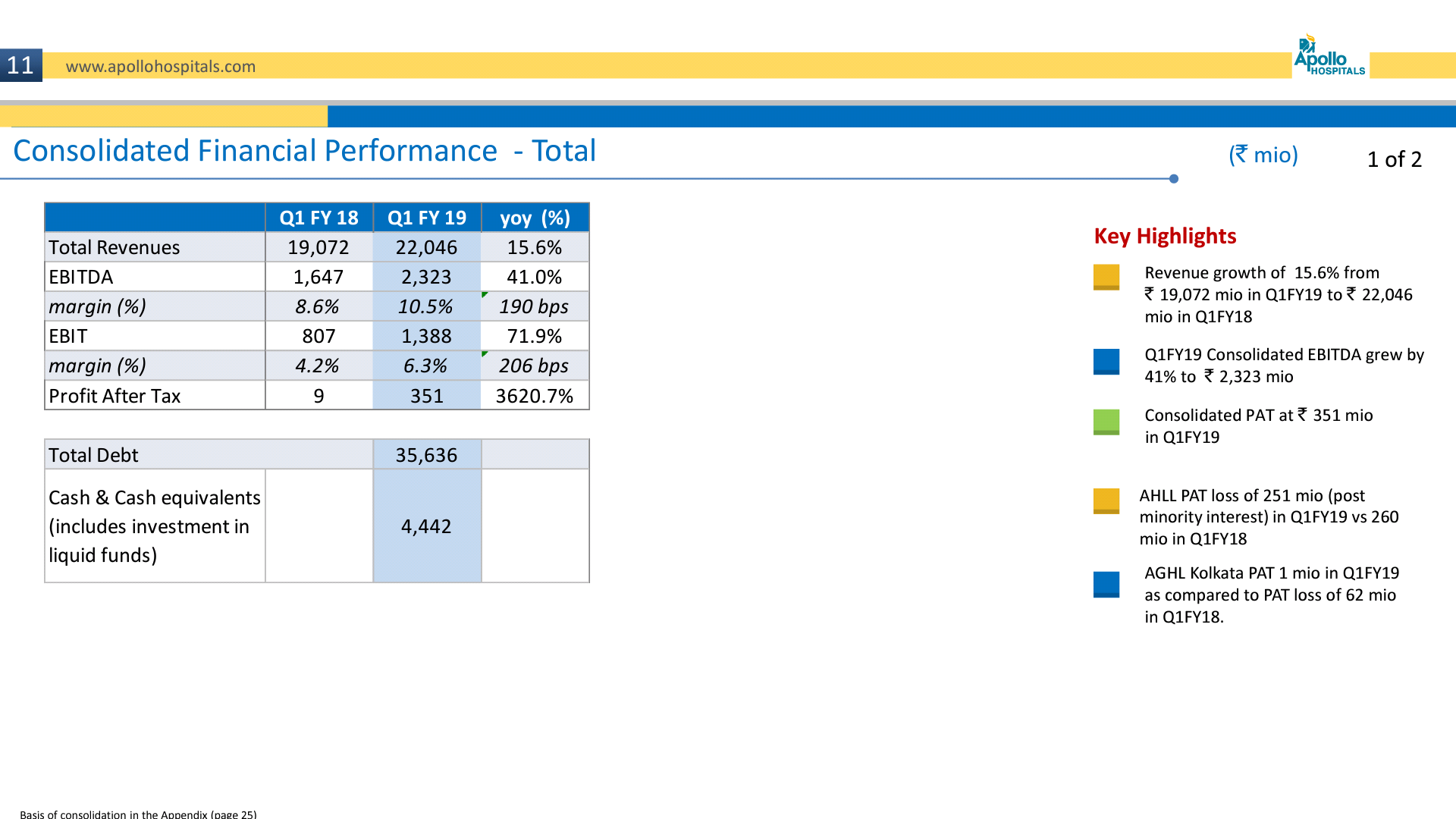

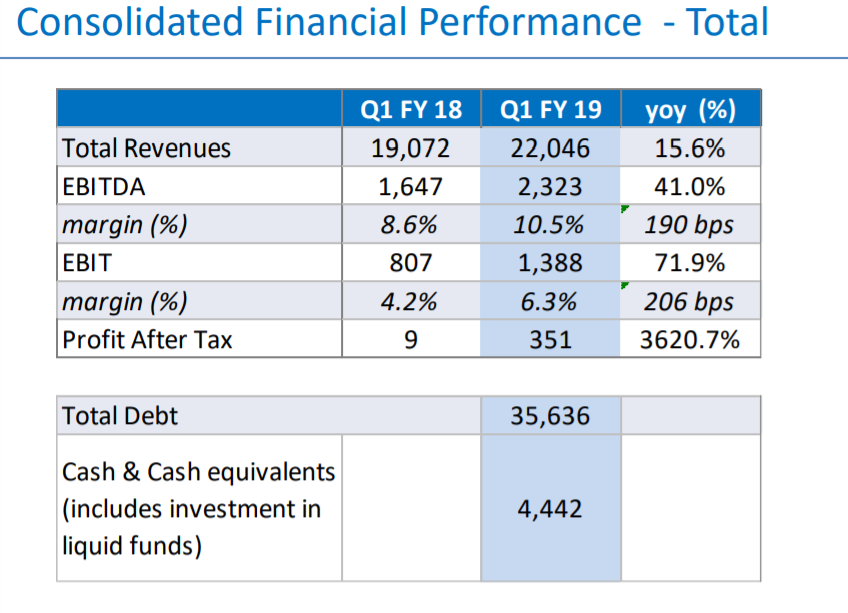

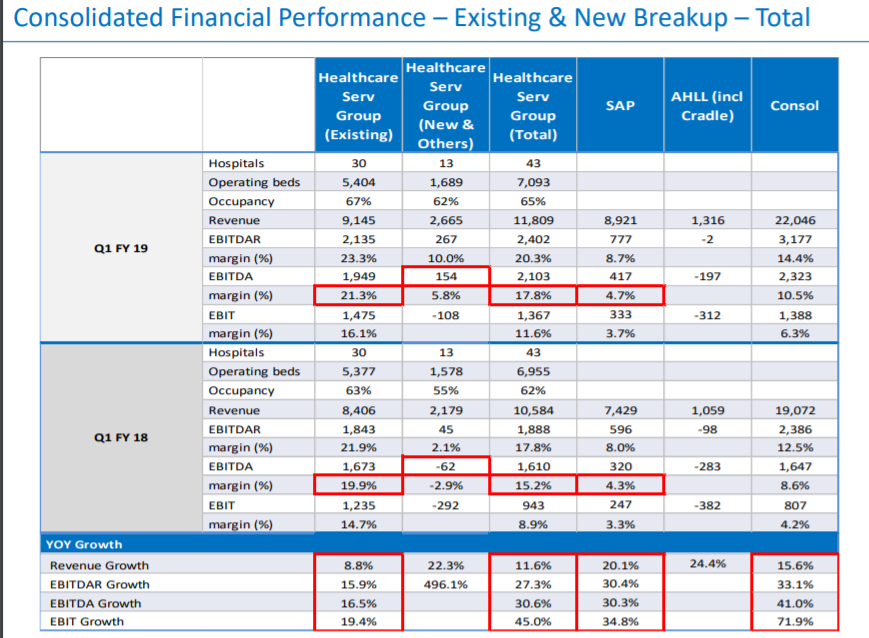

Q1 Performance Snapshot:

Q1FY19 Consolidated Revenues of 22,046 mio (up 16% yoy) Q1FY19 Consolidated EBITDA of 2,323 mio (up 41% yoy)

New Hospitals reported an EBITDA of 154 mio in Q1FY19 as compared to an EBITDA loss 62 mio in Q1FY18

Q1FY19 Consolidated EBITDA margin at 10.5% as compared to 8.6% in Q1FY18

New Hospitals revenues grew from 2,179 mio in Q1FY18 to 2,665 in Q1FY19, growth of 22%.

Stand Alone Pharmacies (SAP) reported Revenues of 8,921 mio, growth of 20% (26% adjusted for GST). SAP EBITDA at 417 mio (4.7% margin) in Q1FY19

69 hospitals with total bed capacity of 9,834 beds as on June 30, 2018

43 owned hospitals including JVs/ Subsidiaries and Associates with 8,353 beds

13 Day care/ short surgical stay centres with 267 beds and 8 Cradles with 280 beds

5 Managed hospitals with 934 beds.

Of the 8,353 owned hospital beds capacity, 7,093 beds were operational and had an occupancy of 65%.

The total number of pharmacies as on June 30, 2018 was 3,085. Gross additions of 73 stores with 9 stores closure thereby

adding 64 stores on a net basis in YTD June 18.

Partners with a strong clinical team and acquires 50% equity stake in 330 bed ‘Medics Super Specialty Hospital’ in Lucknow

Concall Details:

- No other investment required for lucknow hospital and it is operational from day 1

- Spectra is at 50%+ utilization by bed and 35% OT utilization (at 50% OT utilization will break even) and operating leverage yet to kick in. Should break even by this Q4 and craddle by Q1’20

- Diagnostic yet to kick in fully and some roll out cost yet to be kicked in

- Looking to break even at 1st half of FY20 and plan 65-70 cr EBITDA by this year end

- Excluding Navi mumbai among new hospital, only Nasik is not EBITDA profitable as on date. Navi Mumbai is also EBITDA profitable from June’18. It is just that margin is low as of now and should improve with double digit growth

- Expect to make new hospital businesses do 6% margin which will make it 20%+ ROCE but next 3 year target is to reach 12-13% ROCE and old hospital to maintain 18-20% ROCE

- Complete focus is on operating leverage and ROCE improvement

- From FY20 to 23, no major expansion plan except proton therapy (Rs 350 cr remaining capex) and all cashflow should help to strengthen business

- Conscious decision not to take patients where tariff level is below certain level and it has helped to improve ARPOB

- For Navi Mumbai, as of June’18, 140 beds are occupied

- Will be participating selectively on Ayushman bharat based on ability to do it a profitable basis, mostly in tier 2 and tier 3 cities (50% of others capacity)

- For chennai segment, international patient segment has contributed to growth and resulted in better ARPOB

- Proton therapy to start in Dec’18-Jan’19

- Glenicals has shown improved performance but with current govt in place should take 2 years for complete revival

- In AHLL, no further expansion till profitability is established though no guidance on exactly how much EBITDA margin

- In Karnataka region, some low paid corporates were removed to ensure margin and volume degrowth in mysore due to competition. Except mysore, all other places, there has been volume growth

- Number of beds in tier 2 and 3 will be capped for Ayushman bharat

- There are lot more attractive deals in the market available right now due to turmoil going on. We have almost finished our geographical footprint expansion not anything significant expected in near future though we can see on a case to case basis

- A facility will be impaneled for Ayushman bharat and not at bed level

- In pharmacy, looking at 20% growth for future and at the right time, we will monetize it. Also, looking at a digital strategy to increase customer base through online mode.

- On debt level, only 350 cr of proton pending and that would be the peak and after that it will start coming down

- Preparing for digital venture on pharmacy to compete with online model

- In 300 bed old hospitals , work on 18-26% EBITDA margins

- The guarantee amount of doctor keeps coming down as hospital matures

- In Chennai, ALOS is 3.2 and 30% of procedures are day care and working at 62% utilization. Mother and child moved from main hospital to mother and child and hence little lesser utilization else would have been 66%

- Proton facility unit should take 18 months to break even at equipment level and hospital at 2 years. Losses should not be more than 20 crore in the beginning

- Reoccuring capex is around 55 crores.

- Rs 90 crore for lucknow is fully paid

- 3% price increase taken

- For this year, Rs 150-170 cr maintenance capex and 300-350 cr growth capex for proton therapy

Personal View: Most of the points related to operating leverage which were made during initial thesis seem to be playing out:

- New hospitals EBITDA and overall utilization and margins improving

- Debt peaking out

- AHLL losses reducing

- Glenicals slowly improving

- Navi Mumbai reaching breakeven

- Pharmacy continues to improve margins and return on capital along with growth

- Overall, positive growth in revenue and profitability

Expect the momentum to continue with slight bip in dec-mar quarter when final leg of capex will be done which means more interest and depreciation and technically not being strongest quarter but then the new hospitals should start contributing significantly by then

Disc : Invested and added more in last 90 days

4 Likes

I did a presentation on Apollo Hospital at Tamilnadu Investor Association (TIA) 20-20 event at Chennai. Here is the deck. Not much changed after from some better understanding of company, its risks, Q1FY19 developments and valuation in last 2-3 months as reading more and more about it

1 Like

Apollo hospitals is not so much mispriced considering that a) it has a large analyst following, b) fact that RoCEs are low and were low even at their peak, c) an overhang of regulations which is not going to go anytime soon considering the populist governments we have and d) the unique high real estate value and high interest rate scenario in India where cost for doing business is high enough for many heavy real estate dependent businesses to earn good IRRs.

For an serious investor on valuepickr devoting time to thoroughly study multiple stocks, there are multiple better avenues to look for. For a newbie wanting some exposure to a quality company in healthcare however, it can be one of the many small bets.

PS - on a separate note, such businesses require a huge capex from time to time for upgradation apart from high growth capex, hence a focus on EBITDA as opposed to PAT or atleast EBIT is also a mistake as depreciation is a very real cash cost.

3 Likes

Interesting! One thing I fail to understand…when healthcare (hospital) business is not so great, why PE giants having mad rush to buy hospital chains in India? As far as I know PE investors look for very high CAGR in their investments, even on medium term basis…

Being a PE investor myself in my previous avatar, I can tell you my reason for the same - most of the PE investments in India is growth investing and they hardly care about cash returns etc., private healthcare in India is having enormous potential to grow and this growth attracts them as such secular growth possibility is not present in many areas. At the same time to grow at high pace you need a lot of fresh equity capital which is what PE guys are able to provide. So its an ideal match.

But then private equity in most cases is like playing the game of musical chairs - they are investing in the hope someone else would buy from them at a higher price. I think the reality of this would ultimately be disappointing to many especially in the tertiary healthcare investments which is very long gestation and high capex. Other segments of healthcare including healthcare insurance are arguably much better avenues. That is also the reason why RJ is putting his capital (3-4k crore) in buying a health insurance company and not a tertiary hospital - its just that the economics of this business is not that great (as exhibited in one of previous boarders presentation where RoCEs were peakish at just low teens inspite of Apollo having market dominance since ages).

Note again - I am not saying that apollo is a bad idea, I am just saying there are many better ideas at this valuation of apollo - 3-4x book given its RoCE profile.

12 Likes

Thanks for your thoughts! I liked your musical chair concept very much. As far as i remember RJ put money in Fortis which is into tertiary care and diagnostics…am i missing anything as you mention health insurance?

Also i completely agree with you on all points. I was attracted to health insurance business so ended up buying max india, realized later that health insurance is still small part of revenues, and problems with its healthcare business were such a drag i never expected it to fall so much. Demerger listing was another valuation mismatch. Overall i havr had a bitter investing experience in healthcare so far. I held Apollo in small quantities but sold it as it did not include in surance business back then.

I felt government regulations and related issues also caused long term derating ang negative sentiments on the sector.

Apollo Hospitals to divest front-end pharmacy business

Apollo Pharmacy Ltd (APL) will be a wholly-owned subsidiary of Apollo Medicals Pvt Ltd (AMPL) in which Apollo Hospitals Enterprise Ltd (AHEL) will have a 25.5 per cent stake.

The other three investors in AMPL, are Jhelum Investment Fund 1 with 19.9 per cent stake, Hemendra Kothari (9.9 per cent) and ENAM Securities Pvt Ltd (44.7 per cent).

1 Like

Have you looked at pharmacy business sale and impact on your valuation assumption . If I am not wrong they have sold 75% stake in pharmacy business for Rs 500 odd crores .

They say they are holding back backend operation which accounts for 85% of value ?? . Is being distributor of higher value than being a retailer ?? … Not sure how economics is being worked out here …

Disc : Sold off my small tracking position .

@Investor_No_1 Fortis is a special situation with a live open offer at 170 bucks a share. Its a T20 match for RJ for which RoCE doesn’t matter. In any case Fortis investment by RJ has been made mostly around 130 Rs a share which is around 1.25x of BVPS compared to 4x at which Apollo trades.

On the other hand, the way I understand it, RJ is putting money into Star Health Insurance for the long term. It is the test match where the RoCE’s matter. As Munger says, in the long run the return to the equity investor closely mirrors the return profile of the business itself.

The difference between the two above is what you are missing. RJ is one man army - day trader, short term speculator as well as long term investor.

2 Likes

Exclusive distribution to 3000+ pharmacies would be beneficial than running those retail outlets but not sure how they are purchasing the drugs. Whether they are the distributors or purchasing from distributors. Not much info available on that front. If more disclosure regarding that 85% is available, we can able to make some decisions

1 Like

There is a backend and front end (thats how they call it). Backend is the whole logistics, supply chain and procurement. Front end is the retail stores. On an expected 5% stable margins, approx 1% is kept by front end and 4% by backend. The 75% sell has been done for front end and as per management, 85% of profitability will be retained and after sell of 15% of profitability, they have raised 500 cr approx will which be used either to reduce debt or to expand pharmacy. Also, looks like deal is structured such a way that they can later buy after a certain IRR to current buyers. In terms of valuations, pharmacy overall business was valued around 5000-6000 crs which looks reasonable. Now, we must keep in mind the risks associated in terms of transfer pricing and all which has been existing from long time and we can only trust management.

Now coming to results, this is 3rd quarter of turnaround in profitability and company did 29% pat growth with both hospital and pharmacy doing well. Also, i think this is peak of debt and going forward debt reduction should help in further operating leverage playing out.

Disc : Booked partial profit recently

1 Like

Thanks for clarification . I logged out of stock much early ( @ 1100 odd ) as I was not able to build position as price ran up too fast for my comfort and other opportunities opened up.

Any reason for booking profit so early ??

One more company with Corporate Governance Issue… Management pledged shares by 5 percent recently which were largely due to the unwinding of KKR instrument which was closed out in January.

1 Like

Based on the links, it seems they are purchasing they are purchasing heavily from related parties. They themselves are capable for purchasing directly from the respective companies and can earn better margins. Why are they choosing the related party route? Is there is any specific advantage (as we talk about backend operations)?

Thanks