Company Name: Apollo Hospital

Investment Rationale:

- Valuation mispricing due to multiple factors

- Operating Leverage play to come

- Few hidden better quality businesses under cover of hospital business

Investment Horizon:

Medium term. The one argument for long term holding could be value unlocking post demerger of pharmacy business

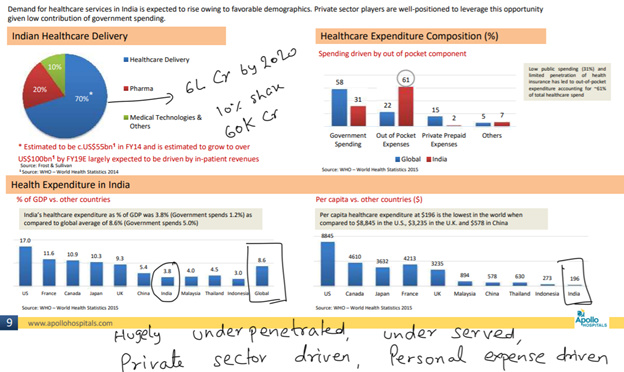

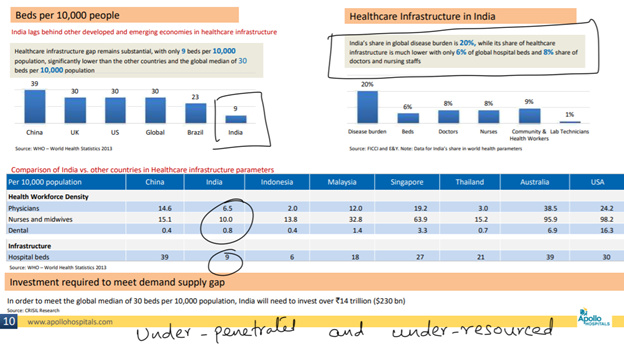

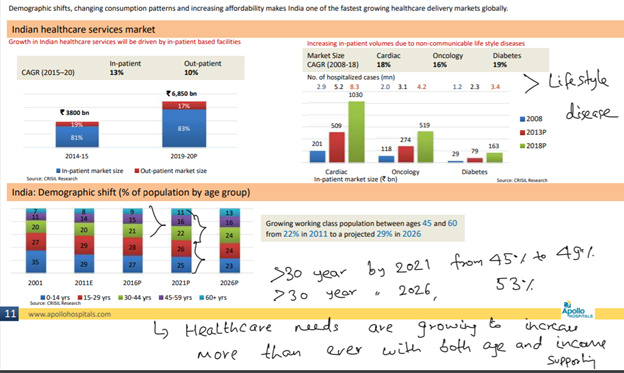

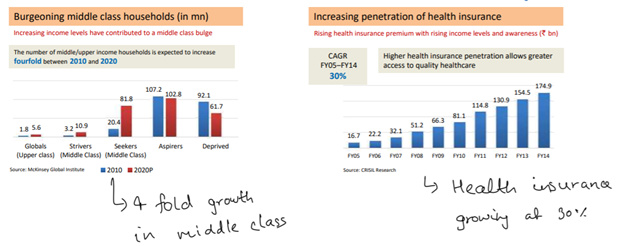

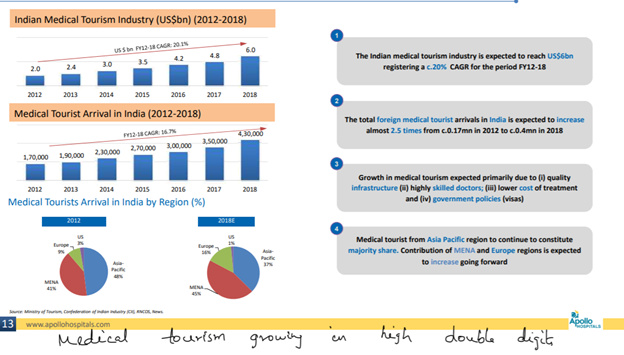

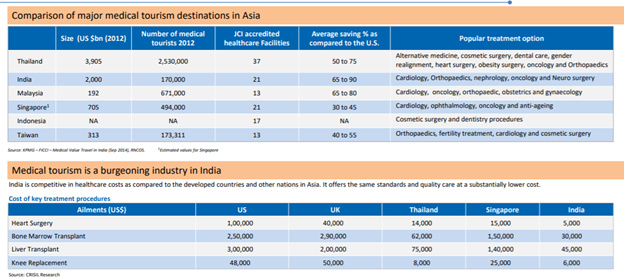

Related Market Size Opportunity:

About Business:

Apollo Hospital is one of the biggest player in overall healthcare value chain offering multiple healthcare services highlighted below

Businesses with scale:

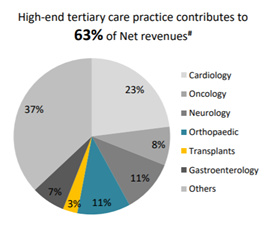

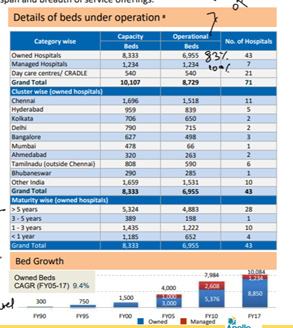

- Hospital: 10,000 bed capacity spread across 70+ hospitals

- Pharmacy: 2500+ pharmacy stores across the country

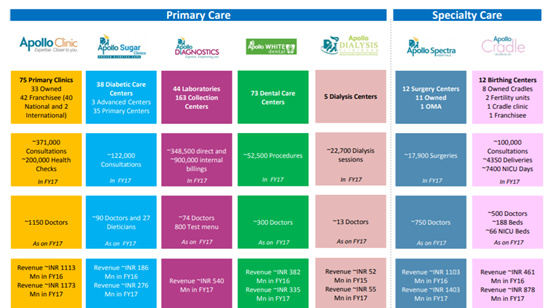

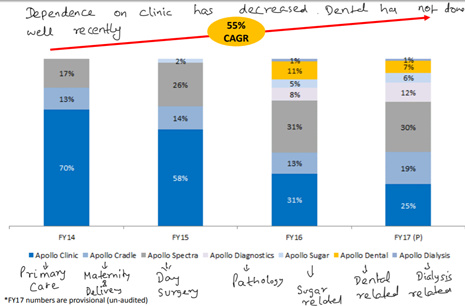

Businesses in nascent stage:

- Apollo Clinic: Primary clinic

- Apollo Sugar: Sugar related specialized healthcare services

- Apollo Diagnostic: Pathology related specialized diagnostic services

- Apollo Dental: Dental related specialized healthcare service

- Apollo Dialysis: Dialysis related specialized healthcare services

- Apollo Spectra: Specialty center for low turnaround surgeries related healthcare service centers

- Apollo Craddle: Maternity and child birth related healthcare services

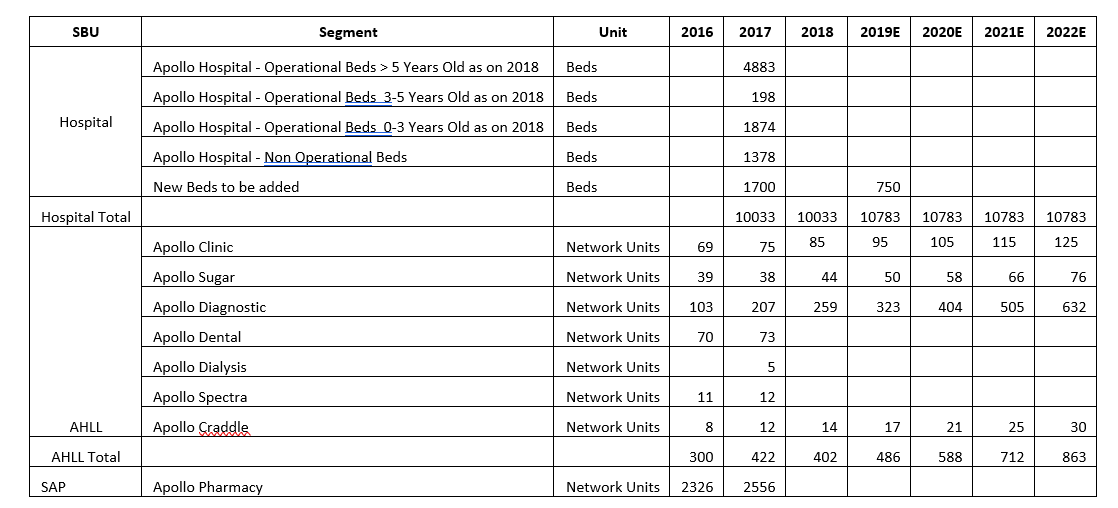

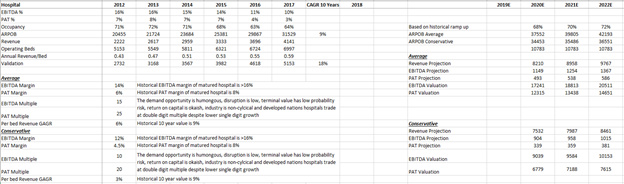

A brief of business operations and scaling plan (based on low to average value of management plan over next few years):

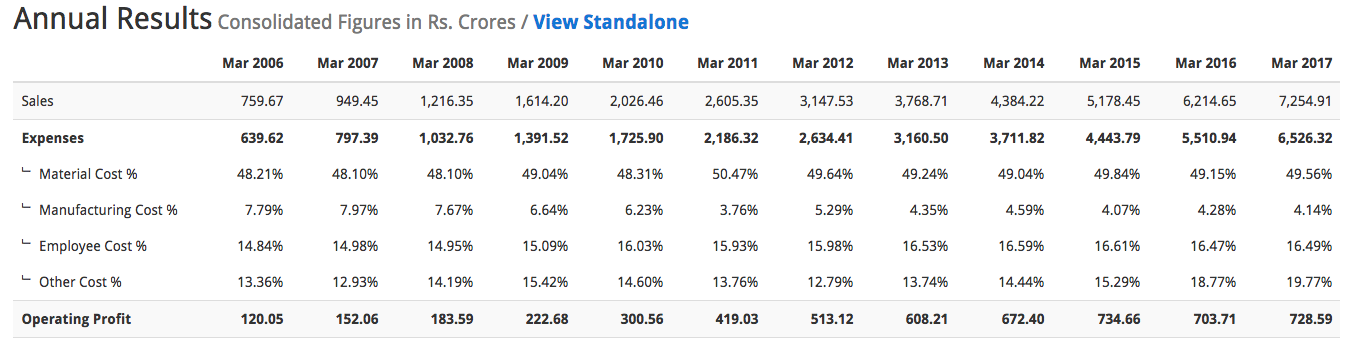

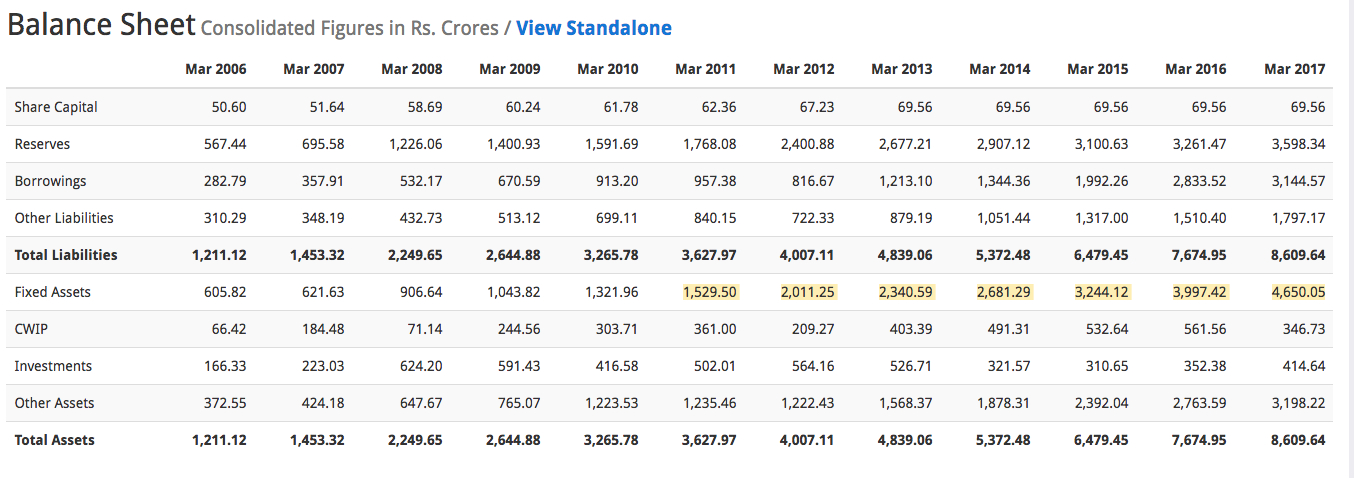

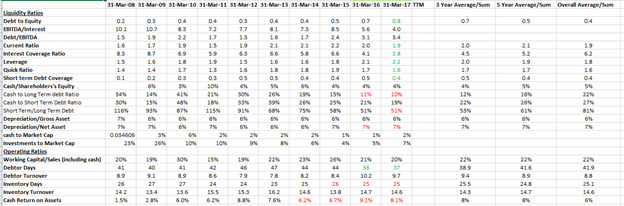

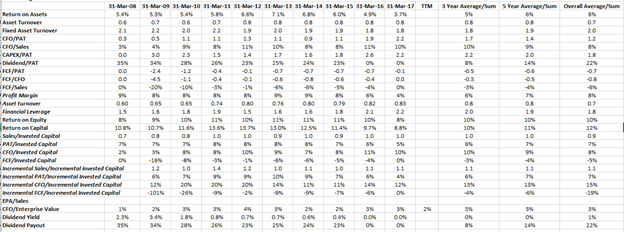

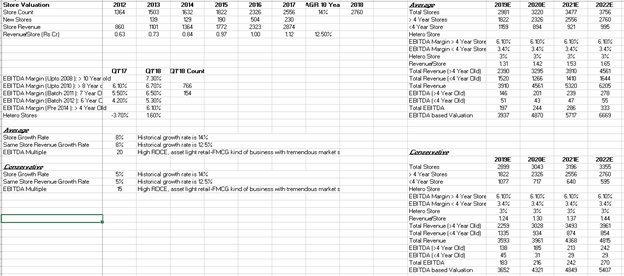

Historical Operational Performance and Related Information:

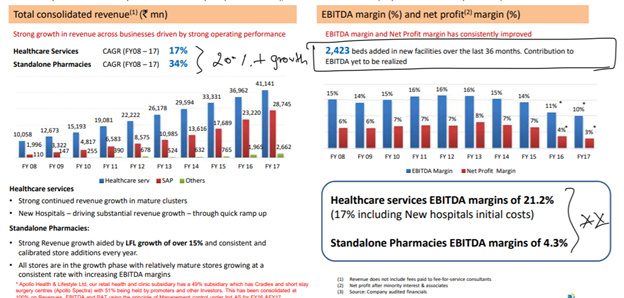

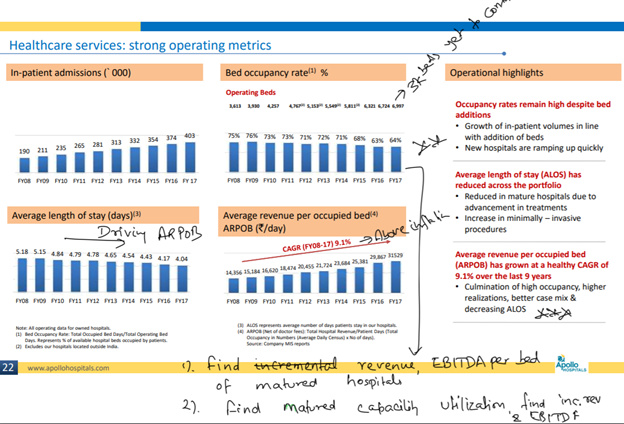

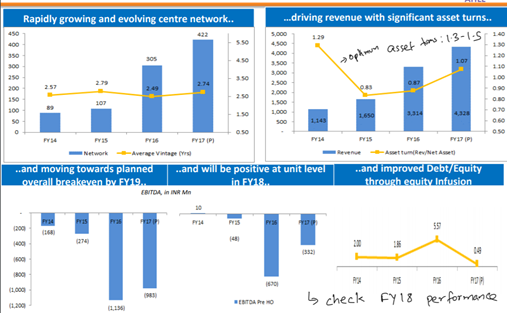

Hospital Business:

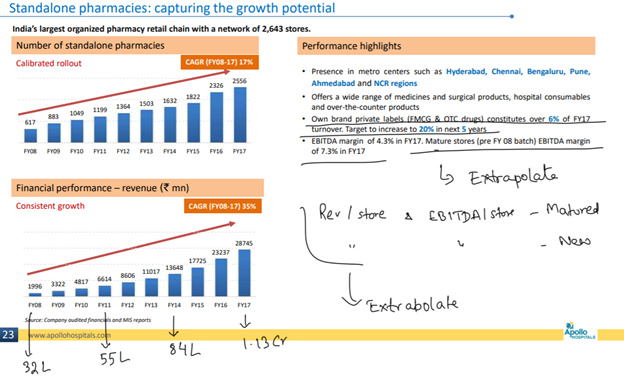

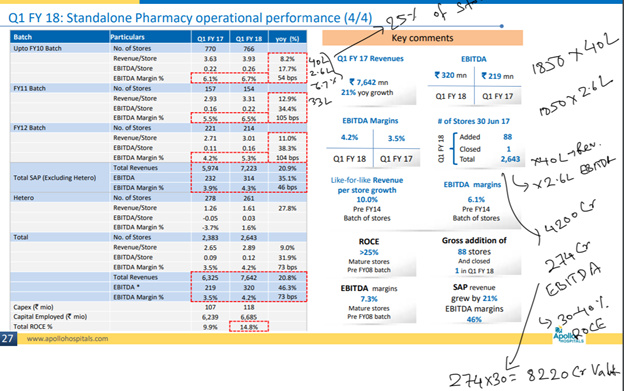

Pharmacy Stores Business:

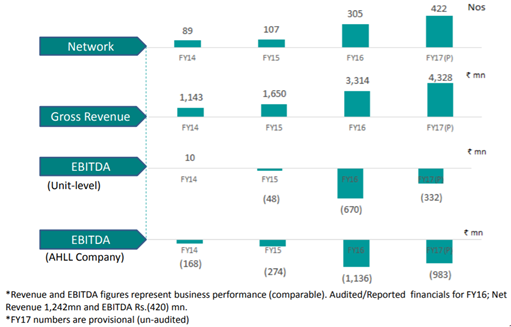

Apollo Health and Lifestyle:

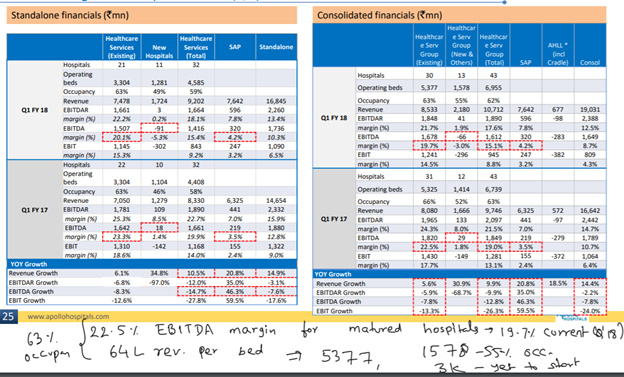

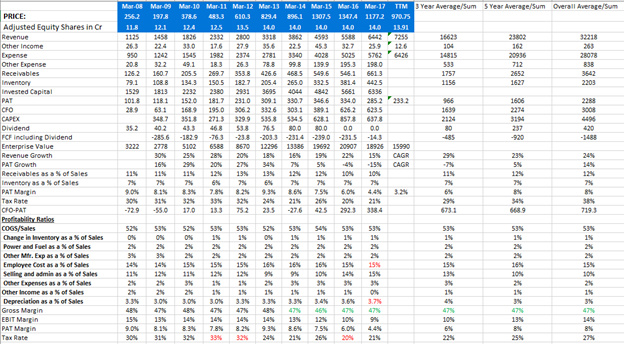

Historical Financial Performance Overall:

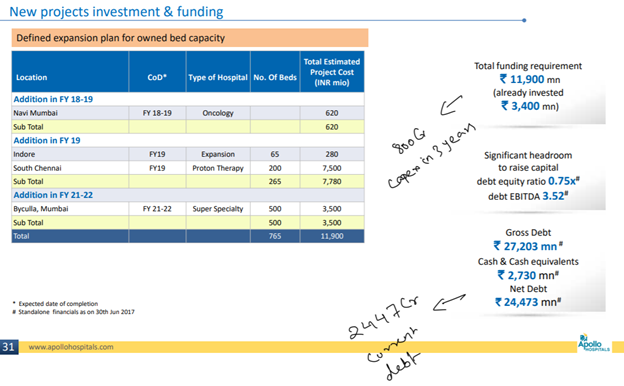

Capex Plan

Valuation Rationale:

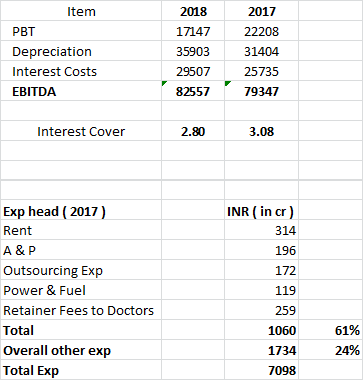

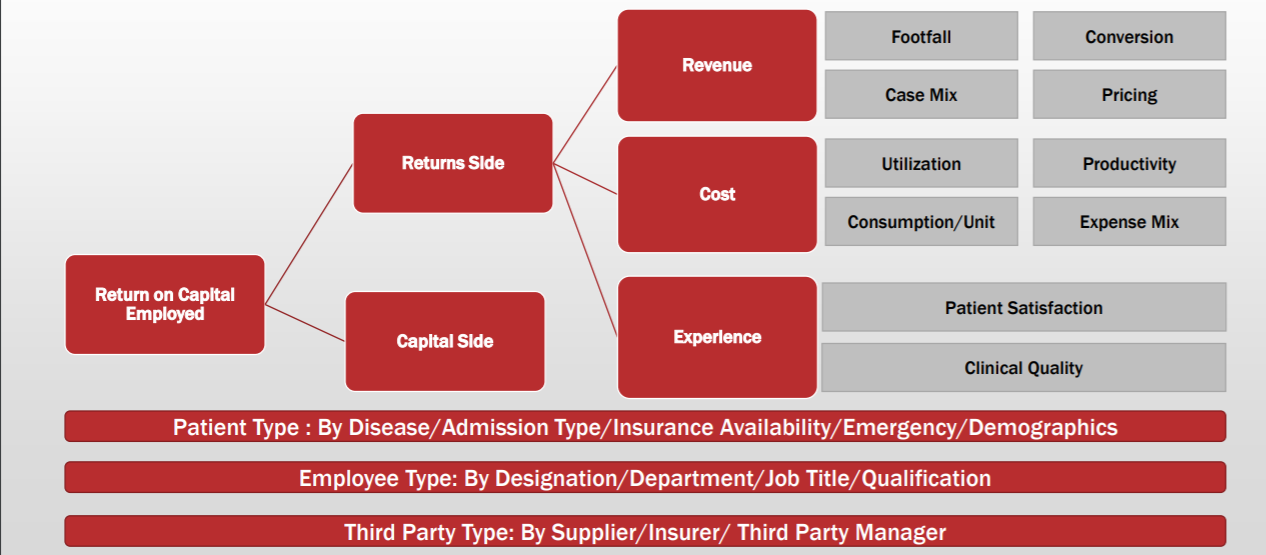

- Return on Equity and return on capital employed seem to be depressed due to:

Hospital Business:

a. Margin reduction from 8% to 3.5% due to:

i. Capex expansion related front end expenses

ii. Additional interest

iii. Accelerated depreciation

iv. Capex is yet to contribute to revenue

v. Regulatory headwinds leading to price reduction

Pharmacy Business:

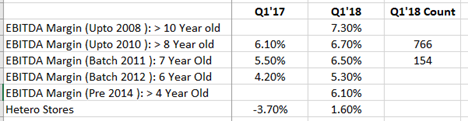

i. Revenues scale up as stores get older

j. Margins scale up as stores get older

k. Last few years of aggressive growth of new store opening

• However, from all the above information presented, hospital business looks like okaish business on return on capital basis and pharmacy business looks ab excellent one with 25%+ ROCE once stores mature

• Demand is not an issue for both the business

• Pharmacy business is yet only a south India predominant one growing at 25% and huge scope for growth

• Management has said that they will focus on getting maximum out of capex done and hence now focus would shift to return on capital generation through better margins, revenue and asset utilization

Hospital:

Pharmacy:

AHLL:

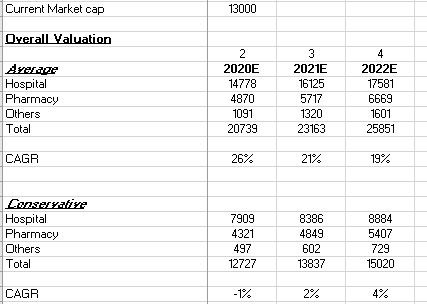

Overall Valuation

Valuation Assumption Highlights:

- The average case assumptions have been taken conservatively at 20-30% lesser than historical one and conservative case at almost 40% lesser

- As AHLL is still in nascent phase, valuation has been done on a price to sales basis with range between 1 and 2

- As no major growth capex is envisaged post 2018, this would lead to reduction interest cost by debt repayment as well as reduction in depreciation rates which means additional scope for margin improvement and hence ROE and ROCE. All this has not been considered in any of the scenarios

Why this could turnout a good investment

- Valuation comfort

- Brand name and ecosystem building across healthcare value chain from customer 360 perspective

- Low risk on terminal value

- Demand is not an issue for years to come if supply model could be managed

- Multiple levers for growth (but at a cost)

- All capex done and margins suppressed due to front loaded costs and regulatory headwinds. Benefits to be reaped

- Buy when fearful. How long regulatory headwinds can last : till few crumble → When few will crumble → When business models cannot take pain → Can regulation/public sector manage quality healthcare if private sector crumbles → High probability no

- Operating leverage/Margin Improvement due to:

• Increase in capacity utilization

• Reduction in ALOS

• Improvement in Case Mix

• Post Capex expense reduction

• Possible reduction in debt if no further expansion

• Slowness in accelerated depreciation

• Better Asset Turns

Why it could turn out to be a risky investment

- Multiple new businesses are yet to prove on profitability and currently in capital infusion mode

- Regulatory headwinds could make whole sector bleeding for unknown period

- Corporate governance issues/Political affiliations (raids in connection with political leaders)

- Inability to pay debt when balance sheet is stretched and P&L is under headwinds though a EBITDA/Interest of 4 looks ok, Debt to EBITDA deterioration from 1.5 to 3.4 is little worrying. Considering, no further major growth capex for few years, this should improve from here bt needs a tight watch

Things pending:

- Yet to do a complete due diligence on management behavior to minority shareholders including warrants allocation etc.

- Competitive analysis on an operational and financial level

Disclosure:

Accumulation done in last 7 days as a part of hospital sector buy. Invested in Apollo, NH and Max India (NH is being more of a long term bet as of now)

Related Documents:

Annual Report and Investor Presentation Notes:

Business Analysis and Valuation Excels:

Apollo Hospitals (1).xlsx (164.7 KB)

APOLLO.xlsx (25.8 KB)