Sir will it not be risky for zomato to offer credit line/loans to restaurants as the failure rates of restaurants are high?

They have loads of data about the restaurants, and they will analyze all of this data and loan to worthy restaurants.

How many delivers a restaurant is delivering through Zomato, what items are these deliveries, cost of the items, margins on these items, are the deliveries increasing, are the high margin deliveries increasing, is there a seasonality element to the deliveries, are there any new restaurants opening up which are taking away some share of the existing restaurants which in turn has an impact on deliveries, who are ordering these deliveries, are they ordering from other restaurants too, and a few qualitative things can be added to, who owns these restaurants, what kind of name they have, do they have debt etc etc. Of course, this could fail and end as a cash burn.

Some thoughts, no investment, using their service.

1 Like

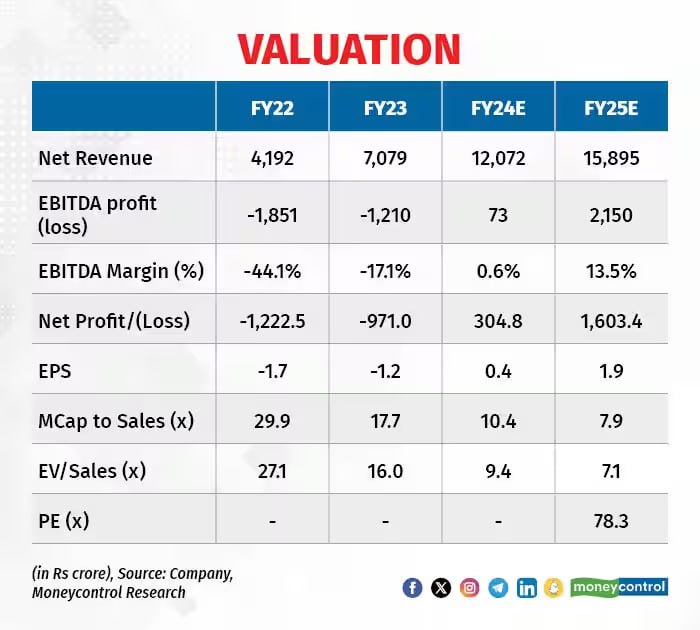

In case Zomato starts giving loans to restaurants, those loans will be secured by the cash that goes to them through Zomato, it will be holding that. But I believe its all about thinking too much from now. As of now they have majorly 3 business and we should try to calculate the earnings from them. I believe FY2025 Zomato will be ending between 2000 crores to 2500 crores of net profits and looking at the valuations that D-mart and Reliance retail is getting at this growth Zomato can also get a 100 multiple.

Disc. Invested and views may be biased.

7 Likes

Wow, do you think they can get to 2-2500 cr net profit by FY25! I can not imagine that but if that really happens, then yes PE 100 or more than that is very much possible.

I suppose today results will give us an idea.

3 Likes

2 Likes

Company issued ~1500 crores of ESOPs in last 1.5 months, they will have a drag of around 700 crores in next 4 quarters… I still feel 1500 to 1800 crores of PAT can be done by end of FY2025…

4 Likes

Notes from Q3FY24 deck -

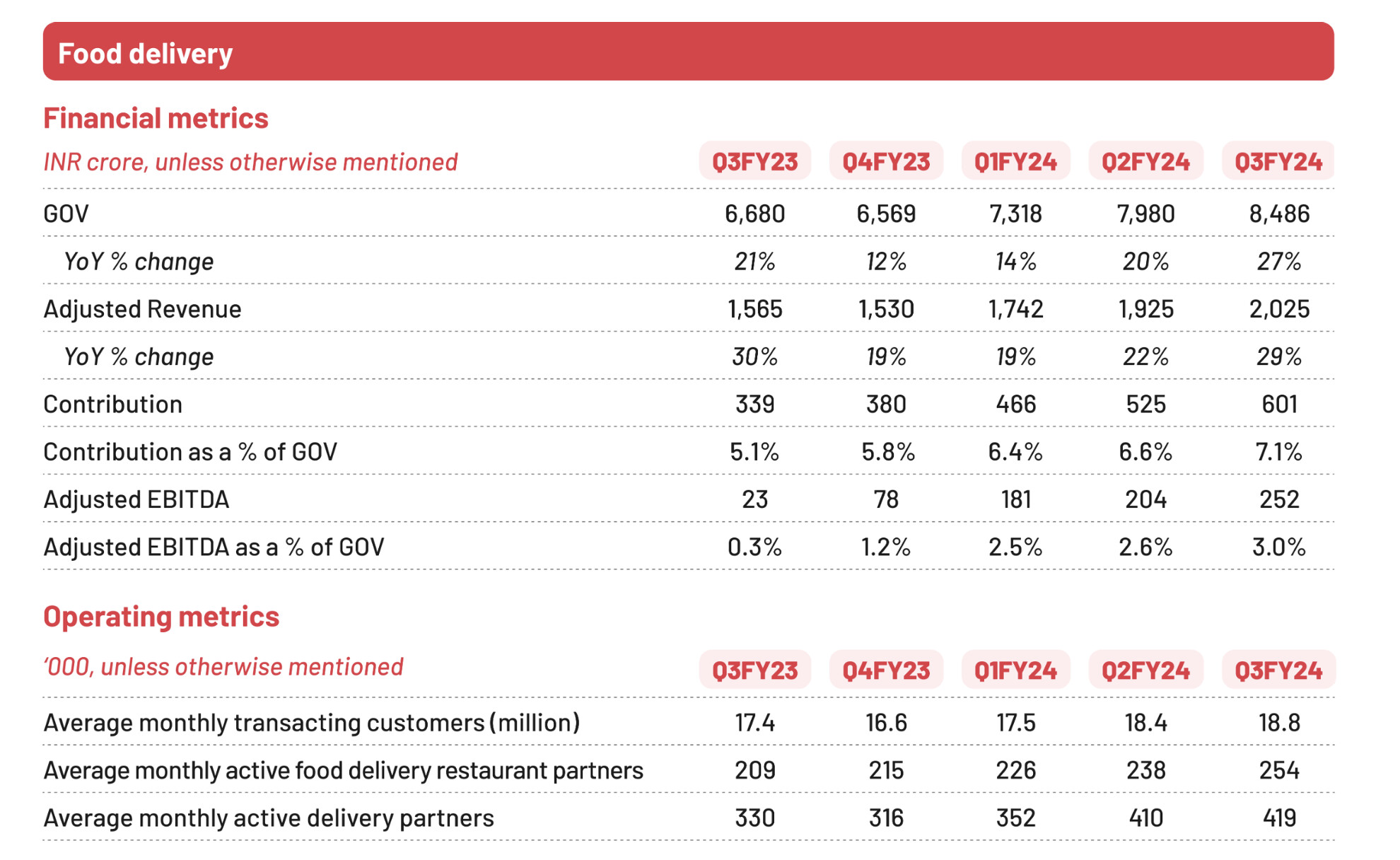

- GOV across B2C businesses grew 47% YoY (13%QoQ) to 12886 Cr.

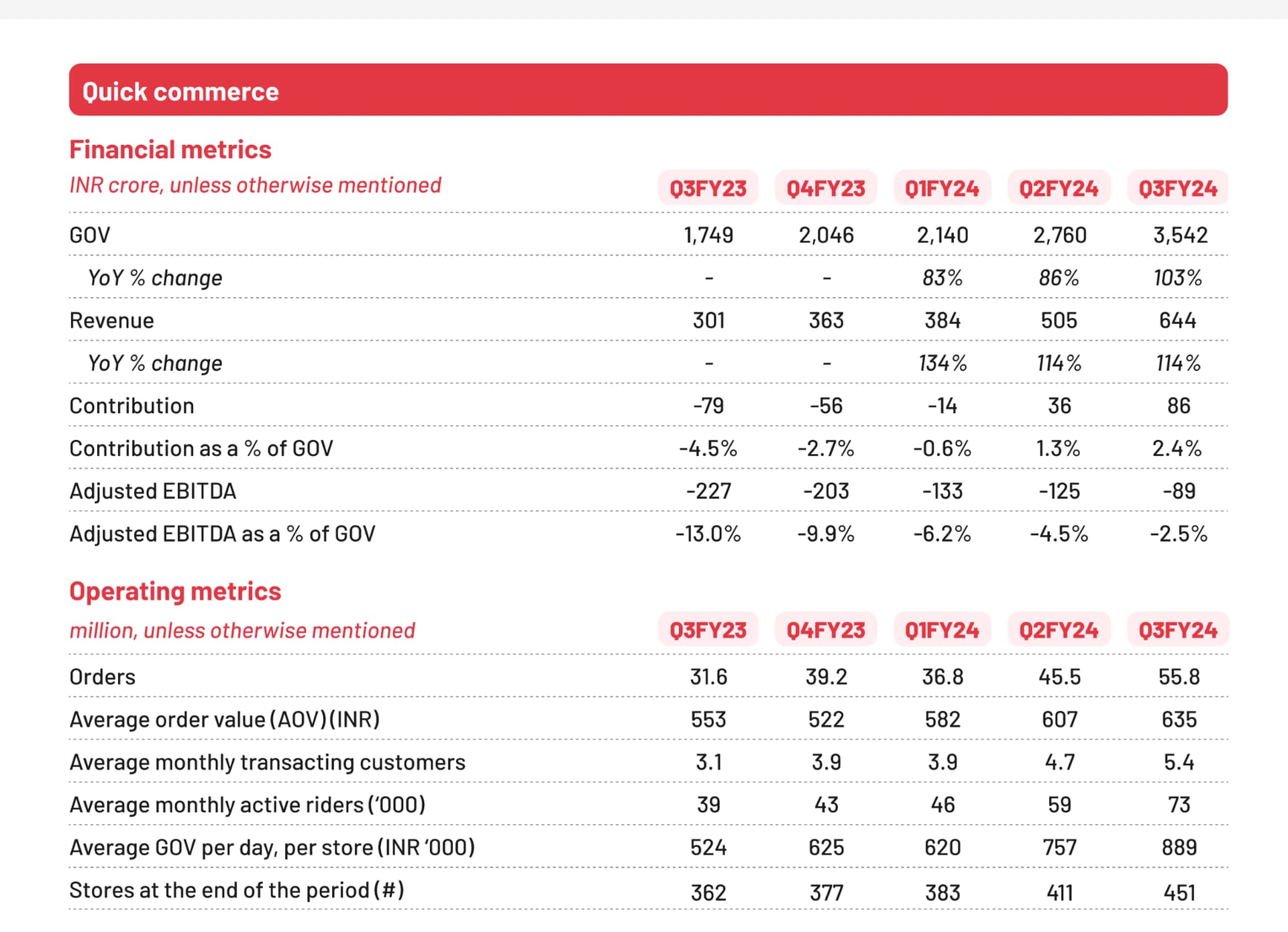

- Food delivery GoV grew 27% YoY while Blinkit GoV grew 103%

- Expect Food delivery GoV to grow 20%+ from here on. On Blinkit, Adjusted EBITDA breakeven may happen on or before Q1FY25

- Demand environment in discretionary consumption was muted and hence Food delivery GoV growth of 27% was below Zomato’s expectations but still higher than most of restaurants in the space

- Food delivery growth is there because it is still under served from supply standpoint. The monthly active user base has grown 20% YoY and also new restaurants have come under coverage

- Zomato Gold is still in testing phase and is being used to acquire/re-acquire customers. Customers switch between loyalty programs of Swiggy and Zomato based on who is offering lower pricing

- Despite drop in Zomato Gold pricing, contribution margin rose to 7.1%. This was because of increased ad-monetization which is leading to increase in ad revenue per order. Introduction of platform fee has also helped in margin improvement

- Blinkit GoV growth of 103% YoY was driven by -

- Robust uptick in demand due to festivals and occasions in quarter (77% increase in no. of orders)

- Less stock outs and adequate delivery partner availability were ensured

- While most of GoV growth was order volume led, it was also led by higher AoV as Blinkit has added higher ASP categories like electronics, festive needs, home decor etc. (15% increase in AoV)

- Also added 40 net new stores this quarter, taking store count to 451 (~10% increase)

- Despite increase in store count, average GoV per store per day grew 17% reflecting healthy SSSG growth

- 90% of GoV in Blinkit comes from top 8 cities so the growth there has to be high to maintain high GoV growth. While Overall business GoV grew 28% QoQ, top 8 cities grew 26% QoQ

- Close to 70% of stores in Blinkit are CM positive and 20% are above 5% CM and hence growing pool of contribution profit is making them to add new stores while maintaining expansion in CM margins

- In Q4FY23 it used to take 5.8 months for a store to do 1000 orders per day, now it takes 2 months as there is stronger product market fit in the business. This has led to faster breakeven

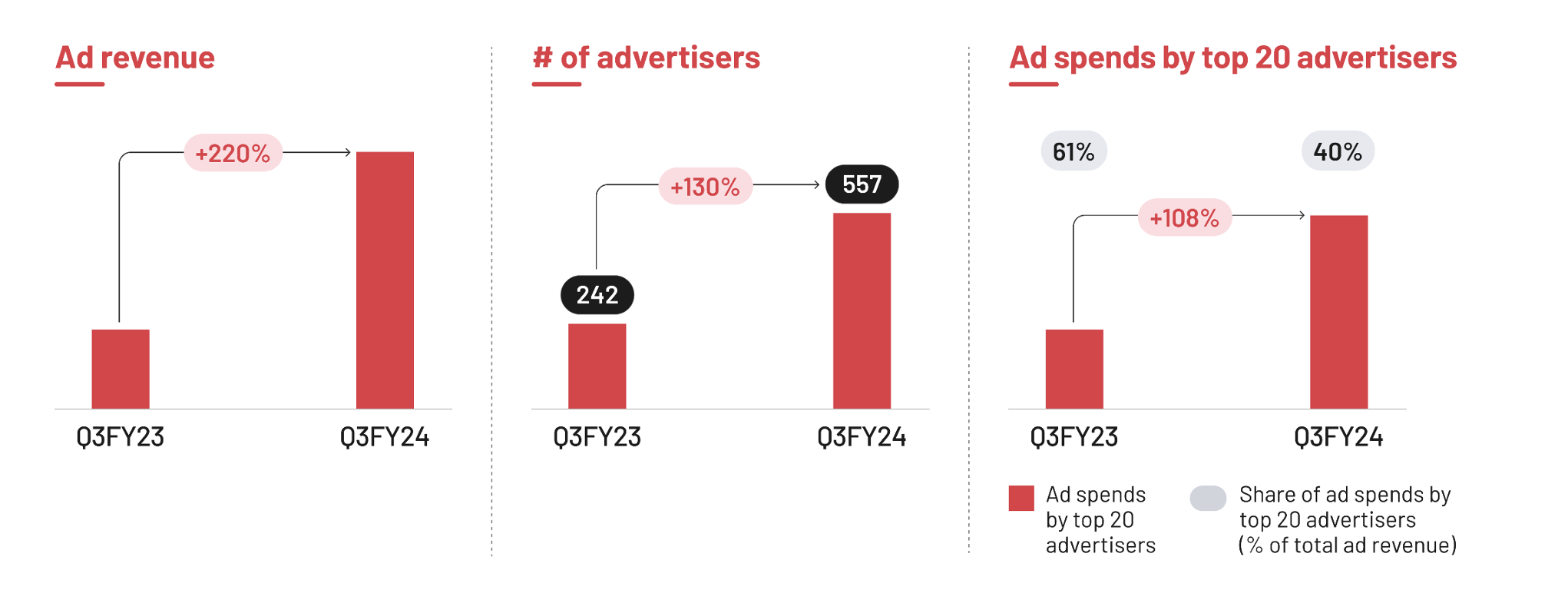

- Ad spends on Blinkit have grown 220% YoY vs GoV growth of 103%. This is because brands get higher RoI on ad spends on Blinkit and hence they are spending more here.

13 Likes

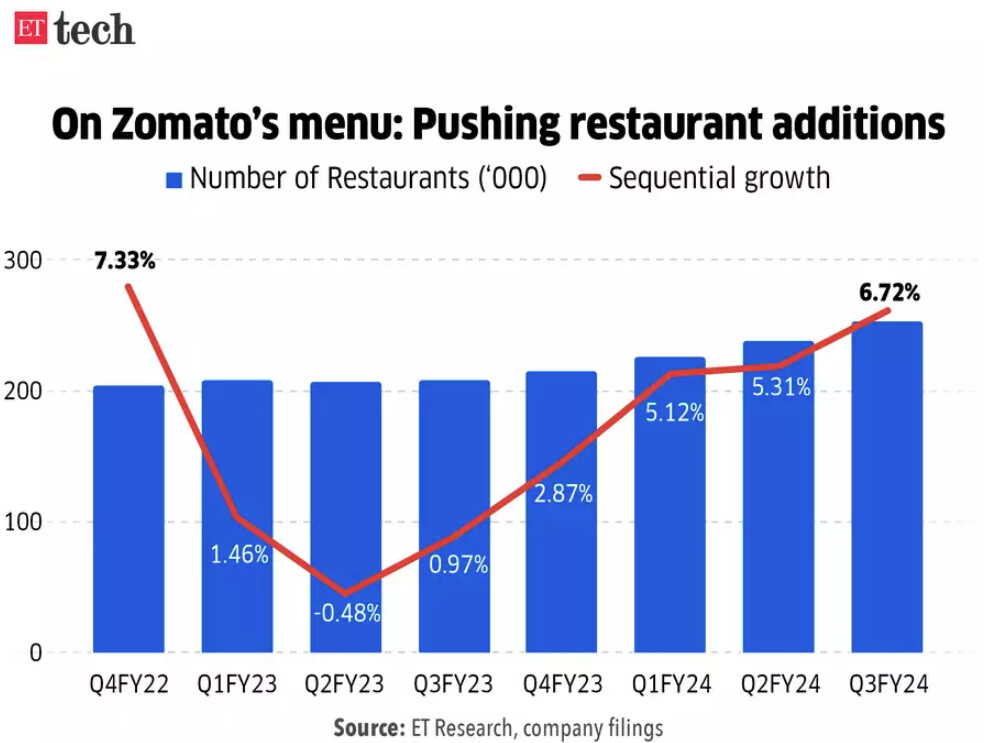

- Restaurant additions on zomato’s platform has been a significant contributor to the 27% YoY growth in GOV.

- Significant portion of new restaurants it added to the platform were cloud kitchens.

3 Likes

2 Likes

4 Likes

5 Likes

2 Likes

1 Like

https://x.com/Rahul_J_Mathur/status/1761778261946777652?s=20

Blinkit is expanding it’s Franchise Owned Franchise Operated Warehouses. Asset light way to expand. A welcome step.

4 Likes

What are some of the optionalities that Zomato can look at 2-3 years from today? It is clear that next 2 years, it will earn record profits and I’m sure in next 5-6 years, Zomato will be among top 5 cos in terms of profits because of TAM expansion and new age innovative company

2 Likes

In their recent presentation they mentioned adding pre cut / pre prepped semi finished products in their hyperpure business. Given their strong brand, they could easily sell these to end consumers as well I think.

1 Like

Well I’m trying to see things from the point where by end of March’25, Zomato would have close to 14.5k cr on their books. What would they think would be the future growth engines besides existing business?

What are the plays which is a natural extension to their existing business?