Yep, that is true & hence he is not classified as a Promotor. But this is common across new age companies look at Paytm, Cartrade Tech. etc

So, Why is the promoter (who is not currently the promoter) working for company?

Just for Salary?

I mean, such a huge company they have built and they hold nil shares now - that means he is just working for the salary.

Is there any agreement or such with the FIIs that he can take back the shares?(Rumors in the market)

If there is an agreement where will the money come from? - the company will have to pay out of its profits (like buyback)

I am very much confused.

1 Like

There are certain nuances needed to be understood here:

Nature of the business i.e. food delivery is tough, they had to burn a lot of money to acquire customers, nudge them to order, make them habituated to keep ordering. Infact they still make looses if you remove treasury income.

Now all these cash burn/looses had to be funded, & the PE/VC’s of the world funded them by taking stake in the company. This is why the stake is so low.

Nonetheless current stake (5%) is valued at approx. Rs 4,500 Cr.

& I am sure salary he would be drawing is much lesser than the value of the stake.

3 Likes

See, the thing is that the promoter’s 5.5% stake was before the IPO.

Now, at present - (as per screener data) - he does not hold any share - If he has then it will be less than 1%.

I got a very interesting data while going through their prospectus-

2 Likes

3 Likes

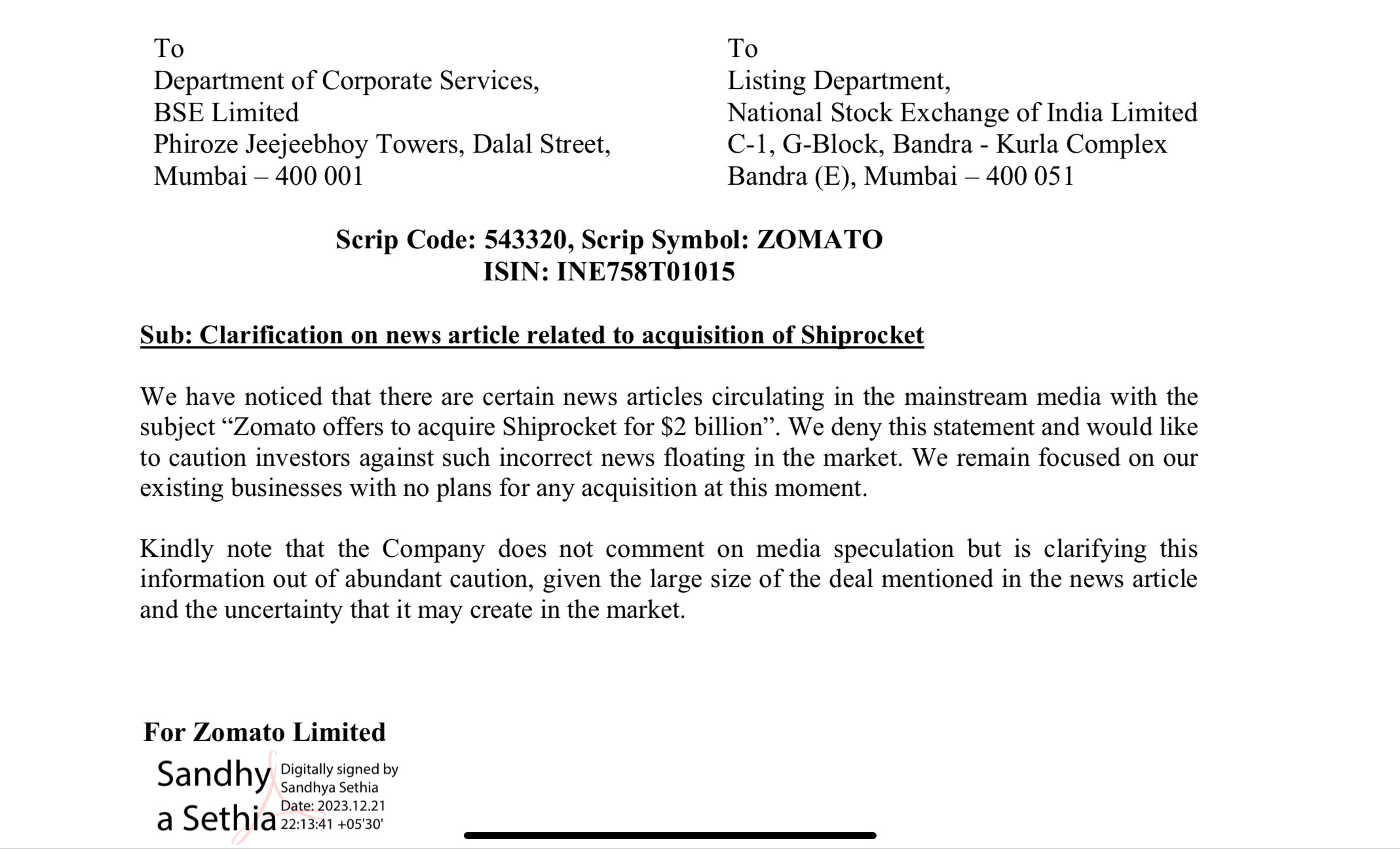

Zomato has offered to purchase Shiprocket @ $2B

If we read in conjunction with their [Xtreme service] which is launched to take advantage of their 3.26 lakh delivery partners, shiprocket could give ready revenue with little incremental cost (fuel cost will be there). Even if we assume 25% of Shiprocket’s last year revenue (250 Cr) to start with, that’d leave Shiprocket as an entity to be profitable.

In October, Zomato launched its hyperlocal delivery service Xtreme to leverage its two-wheeler fleet of over 3 lakh executives, marking an entry into third-party logistics space. The company has onboarded platforms such as Tata 1MG for this service.

[Oct 2023] ShipRocket raised $11M from McKinsey @ $1.23B valuation (flat valuation).

[Dec 2023] I suppose they are trying to pre-empt purchase before tribe’s $75m investment into shiprocket

2 Likes

1 Like

1 Like

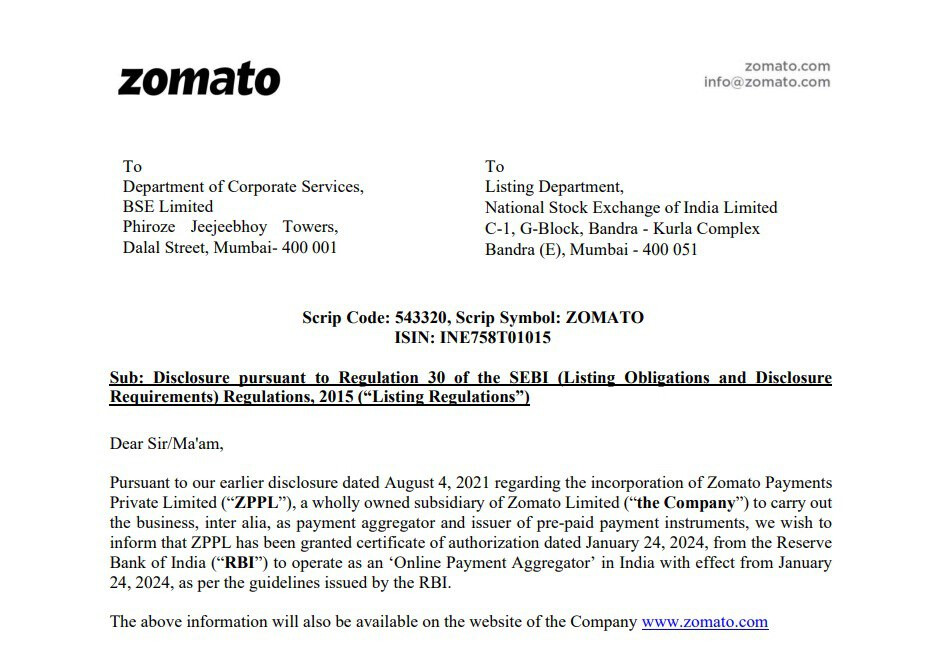

Hi @siddybee . Thanks for the write up on the blog. I am trying to understand the impact of the payment aggregator license that Zomato has now.

I guess it will help zomato to optimize the costs, there by increasing the profit to an extent. It may also be able to onboard new customers who will use its payment aggregation interface.

But any idea on the magnitude of impact we may be able to see?

(Disc. Not invested)

Though restaurants listed on ONDC , they do not have delivery boys. Zomato , swiggy will not integrate their apps in ONDC.so little threat of ONDC to Zomato.

We are focusing only on food delivery business. this business will grow slowly. But hyper pure organics is nearly monopoly business growing very fast , Blinkit a quick commerce business will fetch revenue more than Zomato in cooming months

Hey @SP2022 - here’s my take on the potential impact on obtaining the payment aggregator license.

Who is a Payments Aggregator?

Like the name suggests, they are aggregators. They connect online merchants with banks to process payments.

So, in our case – let’s say you order something from Blue Tokai Coffee on Zomato and you make the payment on the platform. Zomato will act as an aggregator, collect all the payments pertaining to Blue Tokai and then settle it in Blue Tokai’s account.

What’s the hassle with the license?

Until recently, PAs were not regulated by RBI. But due to some issues with customer onboarding, KYC etc, RBI decided to step in to decide who got this license. Existing players were allowed to operate as PAs and got the in-principle nod from RBI.

But, if you were a new player – you had to get this license before you could start your operations.

Becoming a PA lets you handle the funds for the merchants on your platforms and allows you to build financial products on top of it. PAs can offer early settlements to select merchants based on their business volumes, which is a form of credit. They can offer term loans as well by partnering with NBFCs and banks.

What’s in it for Zomato?

After obtaining this license, Zomato will serve as a Payments Aggregator and issuer of prepaid wallets (Zomato Pay). As per several sources on the net, they don’t want to become a standalone fintech player - but use this PA license to provide various offering within it’s ecosystem.

Zomato has a cash chest of > 11,000 CRORE and they could rotate that capital to make money.

Some services I am assuming it could provide would be:

- Loans / Extended credit lines to restaurants / HyperPure clients

- BNPL to Zomato users

- Zomato powered credit card

Management commentary in the upcoming quarters should provide better insights on this to see just how BIG this opportunity could be, because Zomato could easily replace players like SIMPL and cross sell various financial services to it’s diverse set of partners / customers.

Sources:

7 Likes

Thanks a lot. Looks like Zomato could be at the verge of unlocking multiple revenue streams

1 Like

I believe if they use the PA on all of their platforms, the PBT can increase by 50 bps to 100 bps. Credit card can’t be issued by PAs, you have to tie-up with a Bank or yourself have a banking license to issue credit cards in India, NBFCs can’t issue credit cards.

The same is with BNPL you have to tie-up with a bank or NBFC to do it.

Yes Amit, that is correct.

- For credit cards, it could tie up with a bank to issue co-branded credit cards.

- For BNPL / micro credit / loans to partners – it already had set up an NBFC called Zomato Financial Services Limited. Now, I am not aware if all the regulatory approvals to start lending money have been obtained or not. Management commentary on this should help us understand better.

Cannot comment on the PBT increase before we see what kind of traction it can actually build using the PA license.

1 Like