These are personal experiences and even these will vary. The unavailability of items can happen. If an order consists of 15 items, and 2 or 3 items are unavailable, I think, customers will place orders for the available items, and look for the rest elsewhere. What good is a service w.r.t technology and delivery time, if items are not available in required proportion? More so when there is competition.

Used Blinkit, satisfied with the service. No position in Zomato, interested in the business.

Sure, agreed. Just spotted an interesting coincidence that might be true, prima facie. Of course, will need data to back it up- especially a comparison between the catalogues over time.

I also have faced this issue of non availability of small quantity products and this was the case most of the times. So, I looked at the other apps like Swiggy Instamart, Zepto and Big Basket now to find the same product of small quantity and to my surprise, I could not find it in other apps too. I have purchased bigger size products than required just because of the quick delivery and convenience. I think this is the strategy followed by all the grocery delivery apps available in the market. I used these apps in Hyderabad and not sure about the other cities though.

I also observed that there would be generally 1-2 rupees price difference as well in these apps on the higher side compared to the regular grocery delivery apps like Big Basket Supersaver etc. I still go ahead and purchase the products on these platforms knowing that the price is high just because it is just few bucks more for me Vs the convenience and quick delivery. I think this point was already discussed here earlier.

Going forward, I feel that these two points will become the key differentiators for these quick delivery apps to increase their revenues and profits.

Smaller Qty not available, its a part of Human Behaviour / Psychological Re-programming. First by making you used to the platform and building a dependency. textbook business model. (making you buy more and increasing the Gross Order Value. ) Something I would say on a similar lines for selling large qty at COSTCO (US Wholesale).

Analysing per my buying behaviour , I used to buy 1 Nissan Cup Noodles earlier 1 as the single quantity was available with 1-2 price discount than local retailer. But now a days i see packs of 2 with in total 2-3 price discount. So i end up buying more and the intake of the items has increase from 1 bi-weekly to sometimes 2 weekly, (now for couple of weeks no order of Nissan Cup Noodles)

The only thing to wait and watch is the adaptability to this model. If this gets deep rooted in India. The next phase in parallel I would say is to watch tier 3-4 cities, make them buy in small / usual / daily quantities. then transitioning.

Any thoughts on the results?

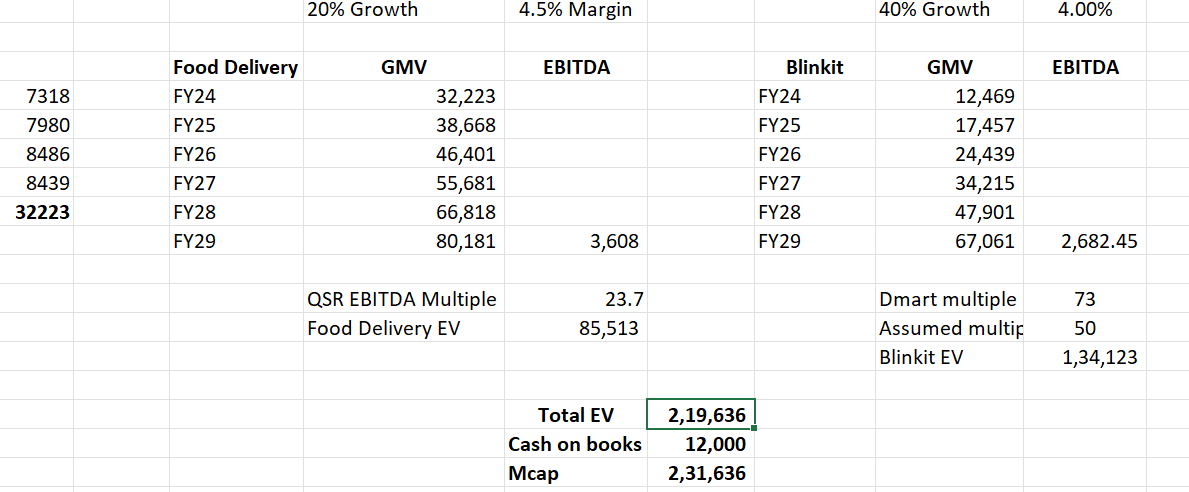

The story is going Zomato’s way, they are able to show the growth and EBITDA growth and the bull market is rewarding them for it. I am starting to worry about the valuation, it is at a PE of 384.

I did some basic maths and here is the summary:

A

Revenue

C

D

E

F

Zomato

Blink it

Going out

B2B

Total

2024

₹32,224

₹12,469

₹3,225

₹3,172

₹51,090

2025

₹38,669

₹19,950

₹6,450

₹6,344

₹71,413

2026

₹46,403

₹31,921

₹12,900

₹12,688

₹103,911

Adjusted EBITDA

Zomato

Blink it

Going out

B2B

2024

3.30%

-1%

0%

-4%

2025

3.70%

1%

1%

0%

2026

4%

3%

2%

4%

Profit at EBIDTA level

Zomato

Blink it

Going out

B2B

Total

2024

₹1,063

-₹125

₹0

-₹127

₹812

2025

₹1,431

₹200

₹65

₹0

₹1,695

2026

₹1,856

₹958

₹258

₹508

₹3,579

Assumptions

Food delivery grows at 20%, Blink it at 60%, Going out at 100% and B2B at 100%

All Adjusted EBITDA are assumptions

Now even if PBT (Profit at EBIDTA) grows the above assumptions and 2 year forward PE is around 80. I am trying to get my head around if this is correct and if yes is the valuation is justified.

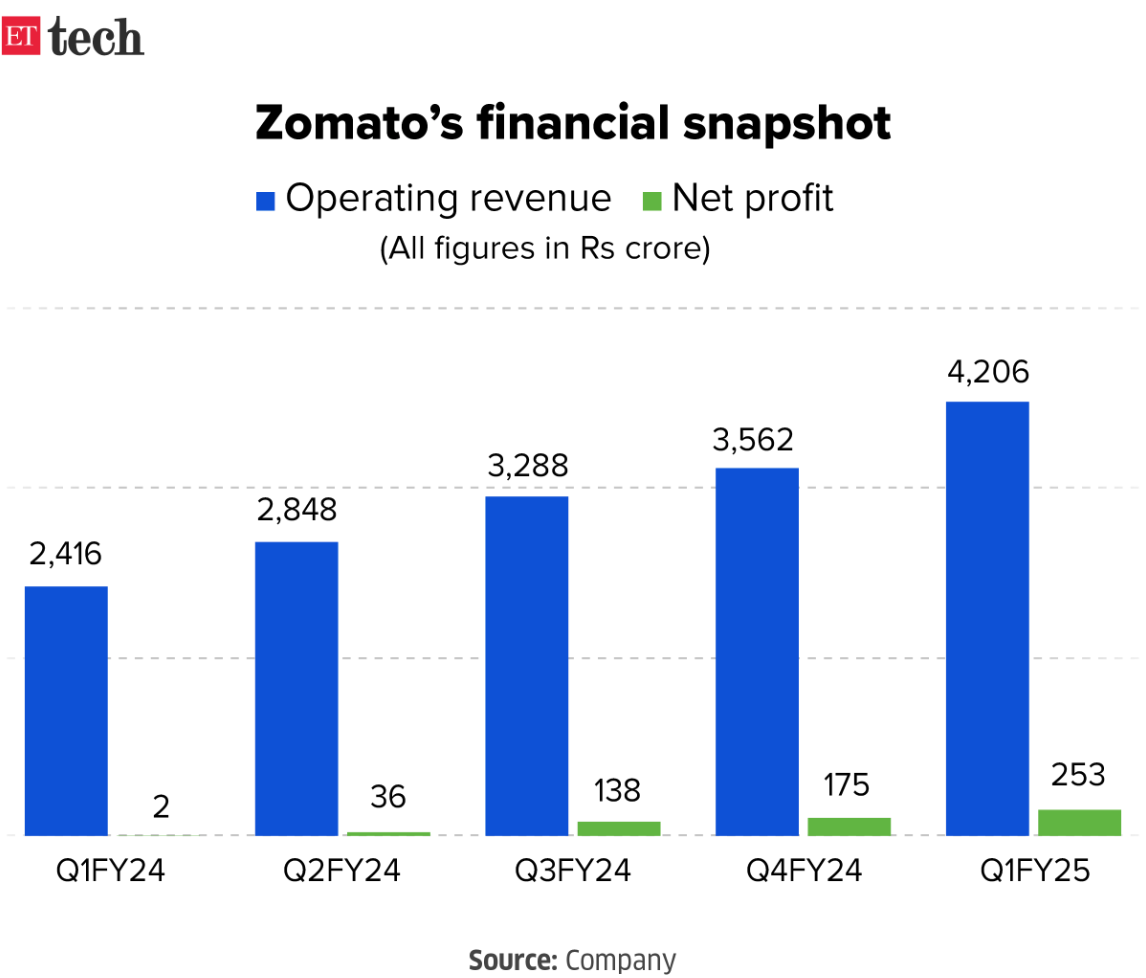

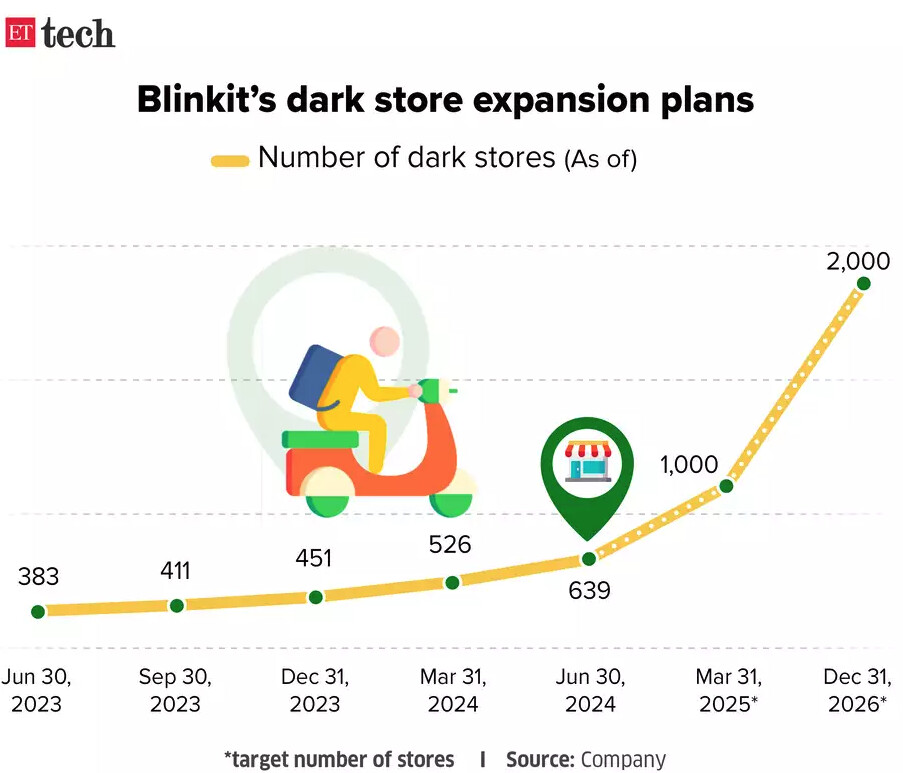

Zomato has come out with good numbers in Q1FY25. Food delivery Gov grew 27% with margins of 3.4% and Blinkit GoV grew 130% at breakeven margins. Blinkit added 113 stores on base of 526 in the quarter (~20% growth)

The key points I am tracking from my earlier post here -

KPIs

Expectation

Reality

Food Delivery GoV Growth

20%+

27%

Blinkit Gov Growth

70%

130%

Adj EBITDA Food Delivery

4-5% in 2-3 years

3.40%

Ad. EBITDA Blinkit

Can reach Food delivery numbers

-0.10%

Store Count Blinkit

1000 by FY25

New target of 2000 by FY26

In Q4FY24 letter, management said there will be pressure on margins in blinkit business due to rapid expansion in stores but on positive note the margins have improved QoQ despite expansion.

Also management gave target to have 1000 Blinkit stores by FY25, now they have given 2000 as optimistic target by FY26. This is 3x growth from current number. Today average GoV per store per day is 10 Lac. This number has increased despite rapid expansion in last year. Even if this sustains at 10L and 2000 stores are online by FY26, GoV can be 60-70K Cr. At 2-3% Ad. EBITDA margin (less than management’s vision), Adj. EBITDA from Blinkit can be 1500-2000 Cr in FY26 itself. This is upward revision to myestimates earlier when I was estimating GoV to be 1000-1500 Cr from Blinkit in FY27 - Add to this 2000-2500 Cr of Adj. EBITDA from Food delivery, total Adj. EBITDA can be 3500-4500 Cr in FY26 and they might end up beating my FY27 estimates of 4000-4500 Cr Adj. EBITDA

Beat my expectations - standalone PAT Is 470 crs. I had predicted 1700 crs of annual PAT from the standalone biz for FY25. At this rate, food delivery is likely to cross 2k crs.

FY26 consol PAT in my view looks upward of 4k crs very easily as Blinkit would start scaling up by H2FY25 and showing up in bottomline.

Also broader trend seems to be worrying for Reliance Retail / Birla Retail etc.. they’re taking share away from these stores for sure apart from kiranas (though Zomato would deny it for political correctness)

D - had exited but tracking since this trend has macro implications

If their EBIDTA is 3500-4500 (3600 is what I am getting based on the numbers I shared above) Cr then the current 2-year forward PE comes between 52-67.

Its always complex to find what is justified or not. BTW, Dmart has similar EBITA of 4000cr and market cap of 3.1 lakh crore. Their growth is also significantly lower. not sure if that helps.

I am unable to estimate the market size of business of zomato. Some say it’s the total size served by restaurants and mess services (also now they are planning to deliver on trains).

But I argue that these people will not pay for such commission fees and delivery charges then they say “I am willing to pay extra for convenience”. Personally, I never want to pay for commission bcz I can get another chicken piece or a can of red bull with my food for the price of commission.

Thus, zomato is only for people who don’t care about commission which reduces the market size significantly. I am pretty sure only upper middle class (and richer then them) would order from zomato on regular basis. People who buy from dominos or starbucks every week are real customers of zomato. Others might order only once in month or bimonthly.

Also not to forget the cart food sellers in every nook and corner of the city. If someone need cheap food instantly then they will buy it from nearby dosa or egg roll or momos cart.

I am very enthusiastic about e-commerce and a big customer of amazon and flipkart (almost one parcel every week if i take average with per order spending more than Rs1500 on average). Meanwhile I have only ordered from zomato twice in last two years with order value of 500 and 1000 resp.

Looking at the revenue of dominos, cafe coffee day, barbeque nation and other food franchises and taking commission of 20-30% of revenue I have estimated the profit of zomato that can be generated from commission is around 2500Cr at saturation (considering 50% market share). Lets say they get another 500Cr from ads, subscription, etc. So for a PE ratio of 30 the valuation becomes 90,000Cr (11 Billion dollars).

Also blinkit is a total waste of money in my opinion. There are kirana stores everywhere for instant small purchase. For bulk purchases there is dmart. People will get out of their house for buying milk, bread and eggs anyway so they will also visit kirana stores also. Rich people have servants for this purpose. I don’t see blinkit anywhere in this. This business will is only an expense which will reduce the above estimated figures.

What do you guys think on estimation of market size for zomato.

Most of the people in my society use milk basket, bb daily, fresh to home. Very few go out in the cold mornings for milk. (I’m in Bangalore and global warming missed us).

Yesterday I bought an item at 250 in kirana store. The same was available at 235 in swiggy instamart. Now Flipkart is also joined this quick commerce race. Kirana shop may not do delivery in 10 minutes. They have resource crunch. But blinkit, zepto, swiggy insta all do guaranteed delivery in 10 to 20 minutes even if it’s raining.

This is the kind of argument we used to have 2 years back. Quick commerce have clearly proven these wrong, there is clear market for quick commerce apps.

I think it is really difficult to estimate the market size. I see zomato growing its revenue in 2 ways first the market (food and dining) itself will expand. As GDP per capita increases share of expenses on food and dining will increase. Another is that zomato will eat the share of dine this has already happened in tier 1 cities and slowly seeing this in tier 2 cities as well.

Most of the people in my society use milk basket, bb daily, fresh to home. Very few go out in the cold mornings for milk. (I’m in Bangalore and global warming missed us).

bigbasket doesn’t sell fresh items, I have ordered fish, prawns and raw foods (including vegetables) and 1 out of 4 times they come spoiled (once a basa fillet was so bad it had changed color due to bacteria). Moreover, the price is also high as compared to offline seller.

Not sure about milk bcz its not available in my area but given the track record of bigbasket I would not order milk from bb either. And then there’s tetrapack of amul taza (and other dairy companies) which has a shelf life of 6 months for people too buzy to buy daily.

Yesterday I bought an item at 250 in kirana store. The same was available at 235 in swiggy instamart.

And regarding kirana store I would say no one cares about price if you are purchasing for instant use, let’s say the maggie or shampoo stock from your dmart’s purchase is over then you will go to kirana and purchase one small packet for that evening only and you won’t care if its 5-10rs expensive than dmart bcz you are going to dmart anyways every 2 months or so. Also swiggy will charge delivery fees which is more than the kirana store available within 200-300m of your house.

I mean if quick commerce is able to give same service for offline prices then its fine but they are charging commission on top of delivery and despite all that the food is substandard.

Also, its impossible that a person will never step out of his house within a week. He will go out to drop children to school or gym or bus stand or to repair some household item, etc etc.

We can estimate that also, dominos (jubilant foodworks) has sales growth of 13% per annum (taken average of last 10 years), you can see that in screener.in, similary cafe coffee day has negative sales growth of -7% for same period, for barbique nation its 11% per year taken average for 5 years.

Lets assume zomato also has excellent management team as that of dominos and give them 13% sales growth then also the valuation of 2.5 lac crore is nowhere to be seen.

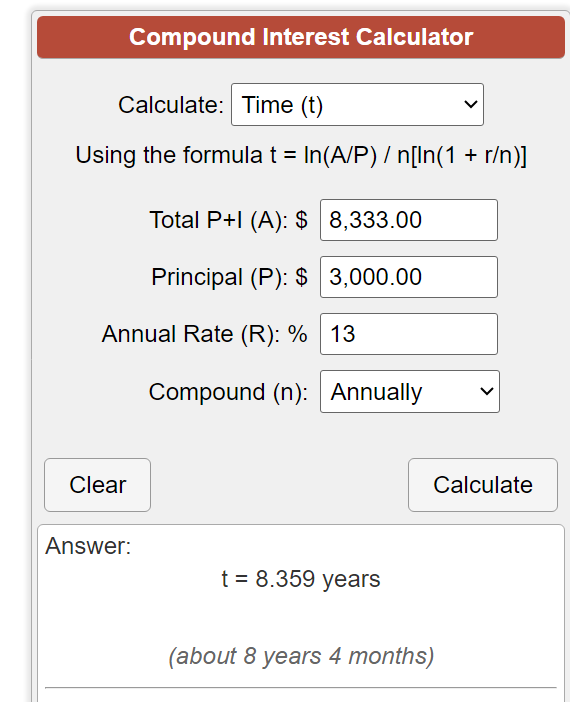

According to my estimates (I have estimated the current valuation of zomato, not the future, assuming if it had tapped the whole market) zomato’s valuation is 90k Crores assuming blinkit doesn’t incur any losses. That too when zomato had tapped the whole market. Zomato doesn’t even have 3000Cr profit today and its valuation is already 2.5lac Cr. For 30 PE ratio it needs profit of 8333.33 Cr profit, that is even more than market potential of 3000 Cr today. It will take 8 years 4 months for market potential to become 8333Cr at 13% sales growth.

And god knows how many years it will take more to tap the whole market potential itself. Overall, I don’t see zomato crossing 2.5lac Cr valuation in next 10 years with PE ratio of 30.

If the order is above Rs. 99, delivery is free in swiggy insta, at least for now. And if a person can get it in 10 min at a lesser price, why wouldn’t he/she order it instead of going out and buy?

Agreed, fresh items cannot be guaranteed fresh in delivery. But that’s applicable to ordering from kirana shops as well.

And many times the kirana shop upsold me things (sending 1. bigger packet, 2. expensive brand instead of what was ordered over phone). Also they take their own sweet time to bring it.

Even a person who steps out of home 5 to 10 times in a day would love to avoid stepping out 11 th time. At least that’s me .

Also it rains most of the evenings in Bangalore so swiggy insta works for me well.

And given the revenue increase in quick commerce yoy, it looks like there are more lazy guys like me to tap into.

This is a very unidirectional view. You should look at the industry growth. Based on the estimates “Dining Out” growth is expected to be 10-12% for the next 5-6 years (just google it and you will find any articles). While these companies (dominos, CCD) have not grown look at the number of restaurants and cafes around you, the shear number of restaurants has grown so they have taken growth from these companies (look at the growth of cafes, growth of La Pinooz pizza to name a few). Food delivery growing at 20% is easily possible for the next 5 years (this is also what management has told).

Also, the calculations include only food delivery profits. I believe Quick Commerce is going to be a bigger market than Food Delivery (I spend more on instamart and blinkit than food delivery). You should bake that in your calculations.

10-12% growth of dining corelate with 13% growth rate of dominos. I have seen dominos open new stores in many places in my tier 3 city. One outlet just got opened near my house at 400m distance and that is not some shopping mall or airport or railway station, its just a regular market place. La Pinoz is not good so I don’t track that. Even new shopping malls are opening which will have atleast 1 dominos outlet.

And food delivery is growing at 20% bcz market potential is not yet tapped and market potential is 3000Cr as of 2024 after which growth will come down to 10-12%.

And regarding ecommerce I don’t have much interest in that. I see it only as a threat to zomato, better to get rid of it asap. Or at least separate it so that it doesn’t affect zomato.

Food delivery won’t grow @ 20% YoY for next 5 years? We are in a subdued macro consumption environment right now. PFCE has been growing at 4-6% for last 4-6 quarters. Zomato is doing 25% growth in that environment. Imagine once RBI starts cutting rates?

Blinkit won’t grow @ 40% YoY? Its growing at 80%+ right now and taking away share from other channels (MT and E-Com) in key categories - groceries, consumer staples, and BPC goods. Speak with any category manner for traditional e-com or MT and they’ll tell you.

Levers that Blinkit has to accelerate growth - category expansion & geo expansion. There is enough headroom to grow. And they’re growing while their existing network of dark stores increases throughput (see the trend of GMV per store trending up from 620k in Q1FY24 to 956k in Q1FY25).

On top of it you have the joker - 12k crs cash which they can deploy to acquire EPS accretive businesses. Paytm live event deals that Zomato is in discussions with.

So, I’m curious what’s the core antithesis?

EDIT - Mindyou, Blinkit is likely to 67k crs of EBITDA in FY27 itself as per me. So there’s a lot of upside still left.