The FY24 PAT is INR 351 Cr. FY25E PAT of INR 1,500 looks highly unlikely given they’re rapidly expanding Quick Commerce + Food Delivery margins have stabilized. Most of the growth looks baked into the stock price.

I doubt that, I think the valuations look very frothy. And competition is quite intense. It would be very difficult for Zomato to deliver a 100% return from here. Just my opinion.

FY26 consol PAT is likely to be around 3400 crs - 2400 crs (food delivery) + 1000 crs (blinkit)

On that basis, the stock is what 50x FY26? not expensive for a duopoly business in a high growth industry

Hell Dmart trades at 100x despite 12% growth… same with all fmcg cos

What’s the backup working for these numbers? I don’t think management has guided these numbers - do you have a hypothesis on how PAT will be INR 1,500 and INR 3,400 crore in FY25 and FY26 respectively?

FY25 I’m not sure because of Blinkit, otherwise Food Delivery PAT is already at 1800 crs odd run rate (Q4 PAT was 396crs)… losses from other verticals may take the console number to around 1000crs

FY26 onwards, Blinkit should start reporting profits (post expansion phase of FY25), assuming 2% PAT margin on GoV, we get around 800 crs profit (assuming 40k cr GoV by FY26). Food delivery PAT (assuming 25% growth) should be around 2250 crs. Total consol PAT of around ~3100 crs.

Note - above is conservative, because they have guided for 4-5% stable state EBITDA margins on GoV. The actual PAT margin may not too low from that guided number… but still I’ve assumed 2% on GoV. Further, while a 4x GoV growth has been guided, I’ve taken a conservative 40k cr as GoV when it can be higher since macro easing is likely in the following few months.

Also you can read any of the analyst report and these are the rough assumptions… infact most numbers are higher since we’re in a subdued macro environment and in all likelihood, Zomato should go back to 30%+ Rev growth & 31/32% PAT growth on FY25 base, which itself is likely to be atleast 25%

EDIT - Income on treasury may reduce since global rates are likely to come down… Zomato consol has a huge other income component as of now… in either case, Cash is a huge optionality in the business since they’re now generating upwards of 250 cr every quarter

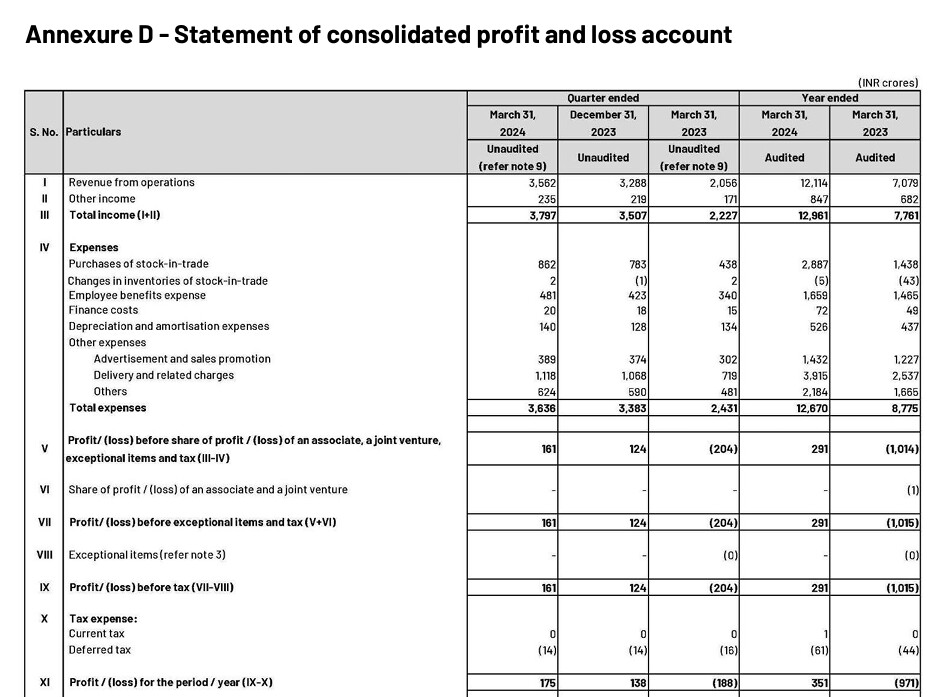

Q4 PAT for the whole business is INR 175 Cr (including a deferred tax credit of INR 14 Cr) and not INR 396 Cr. Q4 Adjusted EBITDA for Food Delivery biz was INR 275 crore, but this is not PAT. - where is the PAT of INR 396 crore being taken from?

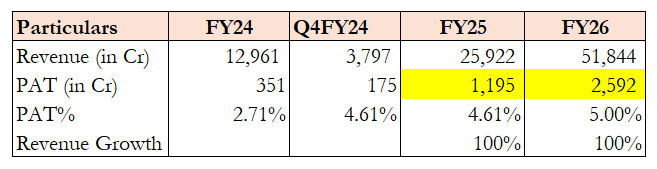

Let’s forget about all the adjusted EBITDA terminology and look at the hard numbers. For FY24, Zomato’s PAT % is 2.71%. For Q4FY24, Zomato’s PAT is 4.61%. For our experiment, let’s say that Zomato is able to maintain this PAT % for FY25 and able to achieve 5% PAT for FY26. Here’s a table of how the PAT would look like even if Zomato’s doubles it’s revenue YoY. I am not even taking 30-35% growth. I am taking 100% growth.

With expansion in Blinkit, HyperPure, Going Out – Capex is going to be high which would result in higher depreciation. FY26 PAT of INR 3,100 is extremely difficult to achieve.

Sir, what is the point if you don’t look up basic numbers? My previous posts have said standalone PAT was 396crs. I’m not going to post screenshot, you can check the standlaone FS for yourself. Standalone business refers to Food Delivery, which I used synonmyously in my previous post. Q4 PAT was 396 crs and the business is already at roughly 1700 crs ARR. Much of it is due to high other income, but the gap is expected to narrow as business grows sustainbly.

Adjusted EBITDA to PAT bridge is given in every shareholder letter and you can check how broadly the numbers are same since other income cancels out ESOP expense and rental expense etc… Given how they’re generating cash, I only expect it to inch up.

If you don’t see the fallacy in using the same PAT estimate for the next year, then its disappointing. Blinkit itself has broken even in March. So, Q1FY25 margins even on a console level will be higher due to normal trend up in Zomato and near 0-0.5% margin in Blinkit

Sir again, how much capex? Blinkit itself is asset light due to FOCO model. Going out is built asset light. Hyperpure - granted is an asset heavy business. But how much capex? Total capex is not likely to be more than 600 crs in my view. That’s not a huge number in any way.

In any case, the beauty of markets is differing opinions. If its frothy, don’t buy or sell / I find immense value in these valuations right now given its a large cap.

Ravi - your analysis is on point. I didn’t consider the Standalone PAT, was looking at the consolidated business.

I am being a little conservative with my estimates, since it is anyone’s guess where the PAT % would land up and I still feel a PAT of INR 3,000+ crore would be difficult to achieve in FY26. Analysts are generally quite aggressive in their estimates, so I always take that with a pinch of salt, however would love to be proven wrong.

Guess we will analyze the quarterly #s to see how things go.

But, I appreciate the analysis and this back and forth that we had. I enjoyed it!

Zomato has started Everyday offering in my area (Rohini, Delhi). I ordered just to try and it told me 2.7 lac orders today (mind you I ordered breakfast). So taking an avg of 7 lac orders per day, AOV of 100 bucks, this is 7cr per day or 210cr per month.

Not sure how revenue works, since this is not with restaurant partners, but directly with home owners. Assuming a higher take rate (say 30%), we get to around 70crs per month of added revenue.

Plus there is cross sell assuming a lot of these orders would be to new customers (need to watchout for MTU growth).

Overall looks positive if they can scale up the offering. I’ve taken conservative numbers.

EDIT - 14th June update - ordered dinner via Everyday and it showed 13.3 lac orders today… so assuming 13L everyday, we’re looing at around 13cr per day or 390crs every month in GoV. Personally feel, Everyday can scale up 3x from here easy given the pricing and offering.

I think, it was Groffers India Pvt Ltd earlier. During COVID, we ordered few items 1-2 times, but mostly they were unable to deliver all items. So we switched to Big Basket.

Customer Care is the most neglected parameter on some of these platforms. So all players will not be winners over 10+ years.

People talk about convenience factor of online delivery. However, online delivery also suffer higher rate of dissatisfaction in case of missing/damaged items.

I have been flip flopping in my head several times about the growth vs valuation of Zomato. On one hand it looks optically expensive and on other hand sheer growth numbers coming out of Blinkit especially prompt me to rethink again and again on the business. So I did some more work to come up with what is the thesis and anti-thesis going in my head -

Thesis

Food delivery GoV growth expected to be 20% for 2-3 years

Food delivery Adj. EBITDA to be 5% in medium term

So in 3 years, GoV can be 60K Cr with 3000 Cr Adj. EBITDA from food delivery

Growth to be driven by expansion in serviceable areas majorly, leading to increase in MTUs, ordering frequency and AoV increase will be other minor drivers.

Blinkit GoV is currently 12500 Cr

Zomato is planning to increase stores from 526 to 1000 in FY25

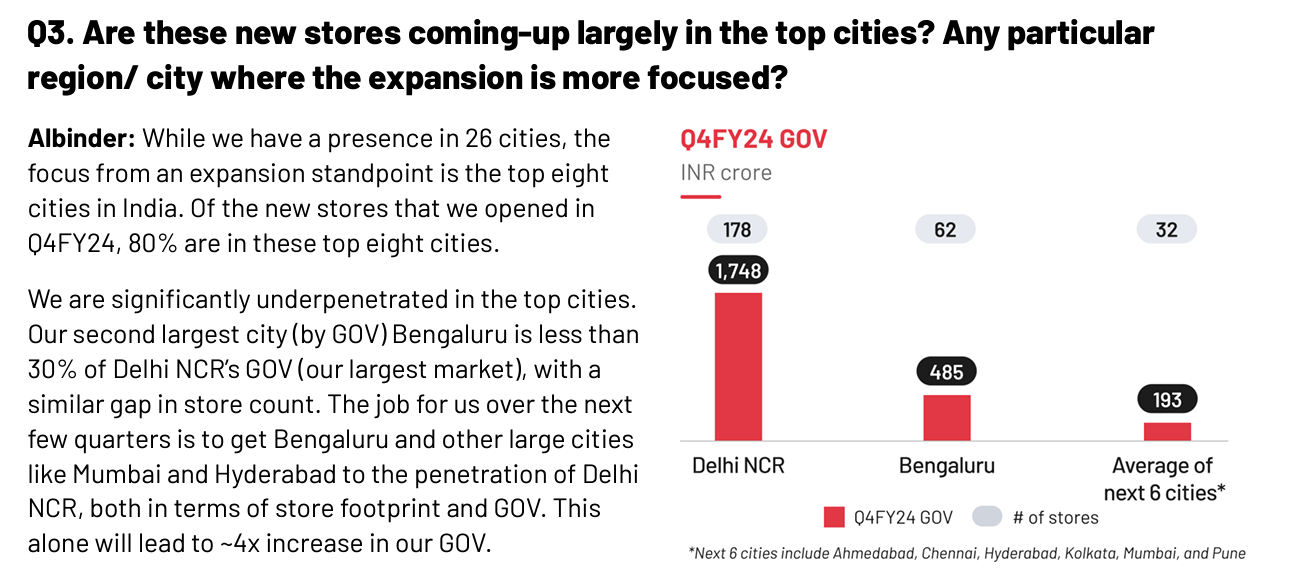

GoV growth rates have been 80-90% driven by increase in orders (SSSG + geographical expansion) and AoV growth. Going forward geographical expansion in top 8 cities ex-Delhi is going to be key driver. Drivers for GoV growth -

Dark store massive expansion 85% in FY25 itself

SSSG growth rates itself can be 15-20% as they reported 17% SSSG increase in previous quarters

Delhi is 40% of business and if other top 8 cities have to match the GoVs, then overall GoV can become 4x.

While it is hard to come up with precise number of GoV growth in Blinkit, but give above info it can be anywhere 60-70% (15% SSSG + 50% expansion led)

So the GoV of Blinkit can be 50K Cr atleast in 3 years

Management says that in steady state adj. EBITDA can be 4-5%. But if we assume there will be some part of network ramping up in 3 years, lets take 2-3% as adj. EBITDA. This means 1000-1500 Cr can come from Blinkit as Adj. EBITDA

So Zomato should do atleast 4000-4500 Cr adj. EBITDA in base case. (I have not assumed other businesses contributing anything for now)

Now this Adj. EBITDA should largely flow to bottomline. Assuming 25% tax rate, the PAT could be 3200-3400 Cr. (Tax rate may be lower due to carry forward losses)

Now question is, for a doubler, it should have 340K Cr MCAP by FY27. This means, it should have 100 PE in FY27 for the money to double from here on. I think if all plays out well by FY27, there is no doubt there will be clear margin expansion story with steady topline growth pending from there onwards as well. It could very well be 30-40% bottomline growth story 3 years out in FY27. Why would not market then give 100 PE to such consumer company growing PAT at 30-40%? Plus we don’t know optionalities that can come on radar as well with such large cash generating business.

Anti Thesis

Competition in Q-commerce as E-comm players are entering into it. I think this is primary reason for such high and quick dark store expansion as Zomato wants to acquire customers asap in top 8 cities of India.

Take rates deterioration in food delivery or Blinkit

Market not allowing enough margin expansion headroom at some point

Poor capital allocation calls and bad use of so much cash from the business

Misaligned objectives of management and shareholders

Swiggy vs Zomato for CY23. Numbers taken from Prosus’s KPI datasheet for CY23. These are consolidated numbers (QCom + Food Delivery)

I’m not sure how will Swiggy ever make money for its shareholders. It requires significantly higher scale to achieve profitability akin to that of Zomato

Hello. Would like to start off by saying I haven’t gone through the discussion in detail, and have briefly perused it. But, had some interesting updates in their operational metrics, which I would like to discuss the viability of. The crux of the argument is that the AOV for blinkit and other QC brands (Swiggy, zepto etc) have increased in the last two years, paving the path to profitability. The fixed cost took up a smaller percentage from the AOV, and improved unit economics. In my view, this was a crucial key to unlock the myth of sustainable quick commerce.

The importance that I place on QC is because I feel it would take over the food delivery business in the next 6-8 years, and investing in zomato should be looked as an investment in an industry of that ilk. The report that details their AOV and unit costs can be found here, was an interesting read! Apologies if it’s been mentioned before https://www.jmfl.com/Common/getFile/3278. Now, the question I have is motivated from recent orders I had placed. I’ve been ordering vim/chips/shampoo/soap from blinkit for a while now, and for the last 2 quarters the availability of small quantity SKUs in each category are getting harder to find. As someone used to the convenience of delivery within 10-20 min, I gave in and ordered a 500ml vim rather than 100ml, a big bottle of shampoo rather than a travel pack (which is what I intended). Is blinkit doing this on purpose? Making only the larger quantity versions available to synthetically drive AOVs? And, how would this impact the long run AOV?

Would appreciate everyone’s thoughts on the same. And, is there any way the average prices of the catalogue of blinkit’s offering over time can be found? Thanks