GMV bro, 67k Cr EBITDA would be crazy ![]()

2 Likes

Zomato Q1 FY2025 Analysis: Key takeaways!!

Zomato’s core food delivery business continues to expand rapidly, while its quick commerce venture, Blinkit, is scaling up aggressively. The company is also making strides towards improved profitability.

Strategic Initiatives:

- Zomato is aggressively expanding its Blinkit quick commerce business, aiming to reach 2,000 stores by March 2026.

- The company is also exploring new business opportunities, such as the “District” platform for going-out experiences.

- Zomato is focusing on improving operational efficiency, including through partnerships with local store operators for Blinkit.

Trends and Themes:

- The food delivery market continues to see robust growth, with Zomato keeping pace with industry trends.

- Quick commerce is emerging as a significant growth driver, with Zomato capitalizing on the opportunity.

- Diversification into adjacent areas, such as going-out experiences, suggests Zomato’s ambition to become a broader consumer platform.

Industry Tailwinds:

- Sustained growth in the overall food delivery market, driven by increasing smartphone penetration and changing consumer habits.

- Rapid adoption of quick commerce, supported by rising consumer demand for convenience and instant gratification.

- Potential for further consolidation in the food delivery and quick commerce space, which could benefit established players like Zomato.

Industry Headwinds:

- Concerns about macroeconomic slowdown and its potential impact on discretionary spending.

- Increased competition in the quick commerce space, with the entry of new players and expansion of existing ones.

- Regulatory changes, such as the implementation of social security benefits for delivery partners, could impact operational costs.

Analyst Concerns and Management Response:

- Analysts express concerns about Zomato’s ability to maintain growth momentum in the food delivery business and the impact of a potential macroeconomic slowdown.

- Management remains confident in the company’s growth prospects, citing the resilience of the food delivery market and the company’s ability to adapt to changing market conditions.

Competitive Landscape:

- Zomato faces competition in the food delivery segment from players like Swiggy, as well as restaurant-owned delivery channels.

- In the quick commerce space, Zomato (Blinkit) competes with players like Dunzo, Zepto, and Swiggy Instamart.

Guidance and Outlook:

- Zomato expects to maintain a 20%+ growth rate in the food delivery business, with continued improvements in profitability.

- The company is targeting 2,000 Blinkit stores by March 2026, with a focus on expanding into new markets and improving operational efficiency.

Capital Allocation Strategy:

- Zomato is focused on maintaining a strong balance sheet and reinvesting cash flows into growth opportunities, rather than considering shareholder distributions at this stage.

Opportunities & Risks:

- Opportunities include further consolidation in the food delivery and quick commerce markets, as well as potential expansion into new business verticals.

- Risks include macroeconomic uncertainties, increased competition, and regulatory changes that could impact operations and profitability.

Regulatory Environment:

- The potential implementation of social security benefits for delivery partners is a key regulatory development that Zomato is closely monitoring.

Customer Sentiment:

- Zomato’s focus on quality of service, selection, and convenience appears to be resonating with customers, as evidenced by the strong growth in the food delivery and quick commerce businesses.

Top 3 Takeaways:

- Zomato’s food delivery and quick commerce businesses are demonstrating robust growth, with the company well-positioned to capitalize on industry tailwinds.

- The company’s strategic initiatives, including the rapid expansion of Blinkit and diversification into new business verticals, suggest a well-rounded growth strategy.

- While Zomato faces some industry headwinds, such as macroeconomic uncertainties and increased competition, the management team appears confident in the company’s ability to navigate these challenges.

7 Likes

I don’t know why you all keep focusing on blinkit, by zomato I mean only zomato.

Just look at amazon and flipkart, it has been a decade and a half and both companies are loss making. Even the Amazon from usa has thin profit margin in its core business and relies on AWS for major profits. Despite the fact that amazon is also selling its prime subscription and flipkart charging different types of fee such as cardboard fee, safety fee, some-new-name fee, etc etc apart from delivery and commission.

Ecommerce has a lot of downsides also especially in countries like India. Like in fashion segment women have high return rate. My own girlfriend’s purchasing behavior has convinced me that as long as customers like her exist fashion ecommerce is doomed. As she buys new dress every week and return them after 2-3 days of wearing. She has new dress every week. And I have noticed she is not some outlier, a lot of women do this.

I don’t think quick commerce will succeed in price sensitive market of india unless they start charging more than even kirana stores and rich people start paying for convenience (that too is doubtful as servants are affordable in india to bring ration from stores).

Or maybe one other way they can be profitable is increasing the order value. Such as minimum order value should be 10-15k. Even legends like dmart don’t want to sell milk or vegetables, bigbazar suffered a lot from such strategies, even today reliance smart sells spoiled and not-so-fresh vegetables that most likely ends up in trash (they literally think people will buy 2 days old dhania whose leaves look depressed for half the price?).

Maybe you guys are over optimistic on quick commerce.

3 Likes

Nice Perspective! Agreed to some customer behavior but I am sure Zomato would find some solution to these outlier behavior with related to food and quick commerce. It is has Platform moat and duopoly play. growing very fast due to demographic play, IMO the party will last at least 10 years.

1 Like

It appears a part of your view is based on your experiences, which do have some weight, but not necessarily can help understand a business, particularly one that provides services catering to crores or people or FMCG like companies. Having a different experience, and thereby having an opposing view to that of the majority is common, but the perception of the market participants is vital, unless those participants are just public, but, if institutions are also participating, they believe in the business, business model, or the changes happening in the business, not to the mention the fact that everyone is looking into the future.

And, despite the future looking optimistic, and a visible growth is seen, the valuation can be the spoilsport.

Not invested.

2 Likes

Flipkart started sending messages to high returners that their return is 5x times more than average and their next return will incur 150 as charge. My wife got it and she’s ordering and returning from my account ![]() . Some will use loophole but majority will reduce doing returns.

. Some will use loophole but majority will reduce doing returns.

Zomato, blinkit are not in fashion goods so there’s no concept of high return. So they’re better than even Amazon and Flipkart that way. We have to agree to one point that food delivery has become a duopoly though Amazon, ola, Uber, food panda everyone tried their hands on and gave up. With this moat, zomato and swiggy can gradually increase charges and fees just like how ola and uber did once they became duopoly.

2 Likes

bruh my girlfriend creates new account every month, she has even used and banned my account

also she changes the company every time, she orders from myntra, urbanic, newme, m&s, etc, etc. Companies that have not even heard of. Last month I got to know about newme and what fast fashion is. Every month or so a new company comes and she takes full advantage of that😂.

Once she gets banned (she rarely gets banned tbh) from all the companies due to high return rate, she uses new number either of friends or parents or sometimes create new sim. This strategy has been working for her from last 2 years without fail.

For those of you who think its just my personal experience just look at the return rate of fashion segment. Its manyfold higher than others.

1 Like

its a clickbait

if you read the whole article it says:

E-commerce is about 7% of our overall sales, Q-commerce is one-sixth of that and continues to grow.

HUL is FMCG company and as of 2024 93% of its sales comes from offline stores according to the same article.

You can already see they are not able to sell a lot from quick commerce. If you still have doubt then keep track of dmart shares, modern trade is emerging as the biggest threat to these quick commerce companies and dmart is not giving rosy hopes, they are delivering hard profits, even reliance is not able to compete with dmart without pumping money from oil refinery business.

I personally believe in investing in companies with atleast having some profit, I will never invest in something which is based on story and making lots of losses. If you got crores in your pocket to tolerate the risk then you can bet on quick commerce.

For now I will end this discussion. I am not getting any convincing argument that tells me otherwise.

1 Like

“E-commerce is growing faster than modern trade, and modern trade is outpacing general trade, a trend that seems secular. E-commerce is segmenting into different models, including beauty commerce, grocery commerce, and quick commerce. E-commerce is about 7% of our overall sales, Q-commerce is one-sixth of that and continues to grow,” Jawa told Moneycontrol.

@Divyanshu_Parganiha, it clearly says Ecom is growing faster than modern and general trade.

2 Likes

The communication is mainly of zepto but same has relevance with blinkit, very referesing talk, how QC changed habits. This shows opportunity of QC.

Disc: Invested and views are biased.

3 Likes

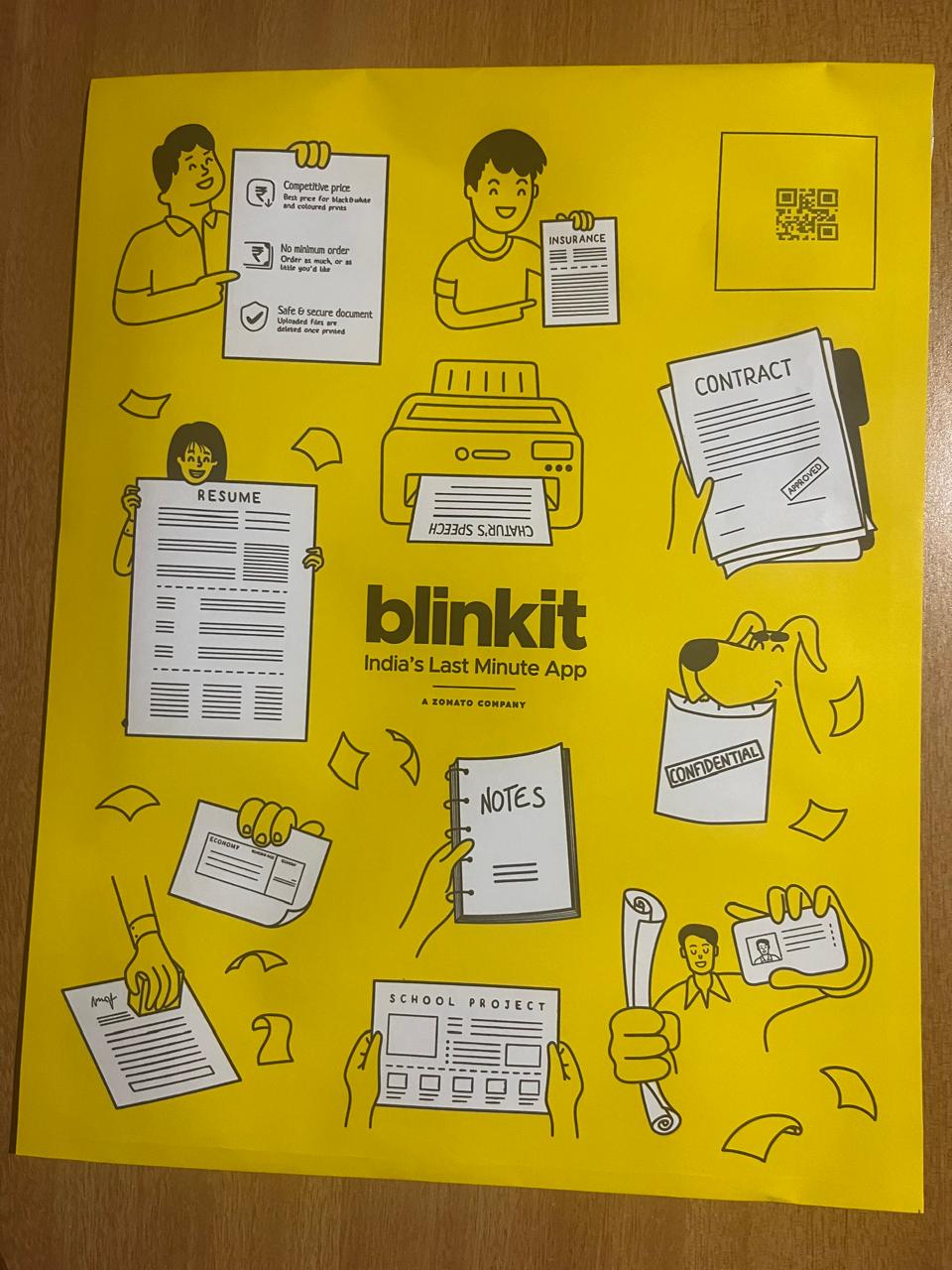

Blinkit now also delivering photo copies, this was the envelope in which they delivered the copies and as mentioned by them it was done in the most secure way without comprising the confidentiality of the document.

2 Likes

I have personally used their photo copy service and sometimes when you are in hurry its a life saver.

It takes me 20-25 mins to go to nearest photocopy shop while blinkit delivers in 10 mins. This might not contribute a lot to top line though.

7 Likes

I have used their printing services quite a bit - always a life saver. Their color prints in my area leave a lot to be desired - poor printing, missing ink colors. But black and white works great.

2 Likes

1 Like

How has he estimated that Zomato could have built the same itself for less than 200 crores?

2 Likes

Maybe he is wrong about the Rs 200 cr figure, but can one be comfortable with the valuations at which the deal has been done? Wanted to understand the viewpoint of fellow boarders.

(Interestingly, similar concerns about the valuation at which Blinkit was acquired were raised, however, Zomato management’s decision proved to be right.)

Disclosure: Invested at very low levels and planning to hold

5 Likes

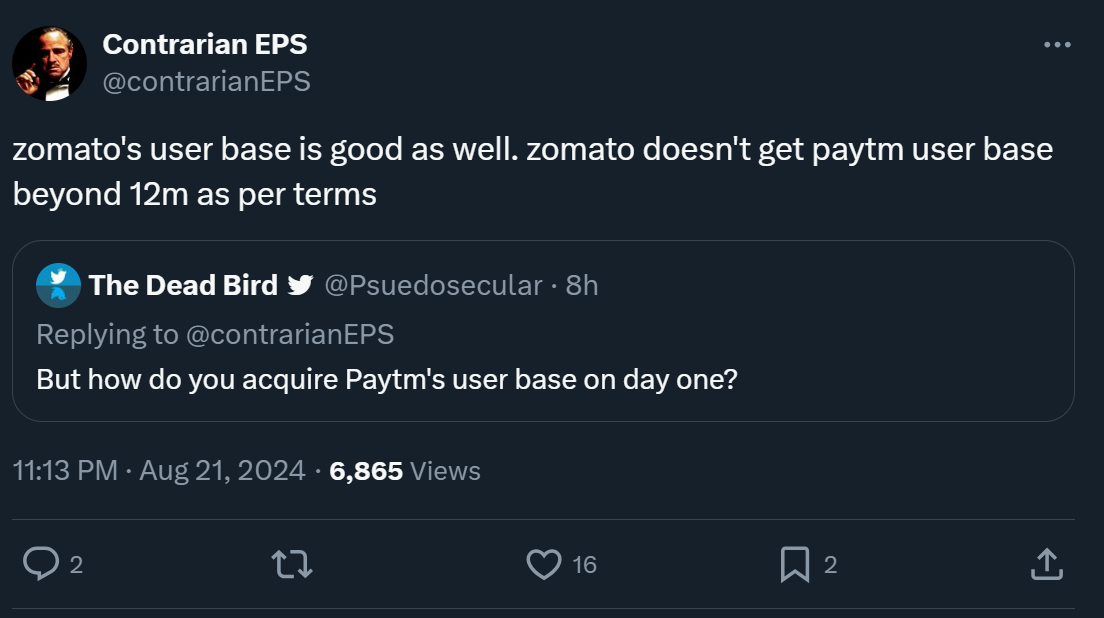

Contrarian EPS has provided valuable insights to many investors through his tweets. While his opinions are generally sensible and useful, particularly when it comes to traditional businesses. He has consistently held a negative view of Zomato since its inception. I’ve been following him for a long time, and he is not invested in Zomato.

Zomato, however, has a strong board, particularly with Mr. Sanjeev B, who holds the highest stake in the company.

Out of context, SB becomes board member of MMT. MMT paid him renumeration as board member, instead of taking in his personal account, he deposited it in to infoedge account, as he believes his all-time should allocate to infoedge.

Although mistakes can happen in business (such as the investment in housing.com by SB), overpaying for some assets is often less concerning. While it may appear that Zomato overpaid in this deal, strategic decisions in business sometimes require to take such deal. I believe there could be two reasons for pursuing a deal even if it seems costly:

Competitive Concerns: 3rd party, possibly Adani, might have been interested in the same deal. If that had happened, the market could have become more competitive with three players: BookMyShow (BMS), Adani, and Zomato. Now it’s duopoly with this deal.

Disruption Potential: I strongly believe BMS is vulnerable to disruption. Despite being in the market for a long time, their revenue has stagnated at around ₹800 crore (according to a CNBC report, although no specific source is available). Zomato’s CEO, who is one of the smartest entrepreneurs, likely didn’t want to wait any longer to make a strategic move.

Disclaimer: I am invested in Zomato, and my views may be biased in favor of Zomato and most new-age entrepreneurs.

My mistake: Eventhough invested around 50 and following it from IPO, couldn’t able to increase my allocation.

23 Likes

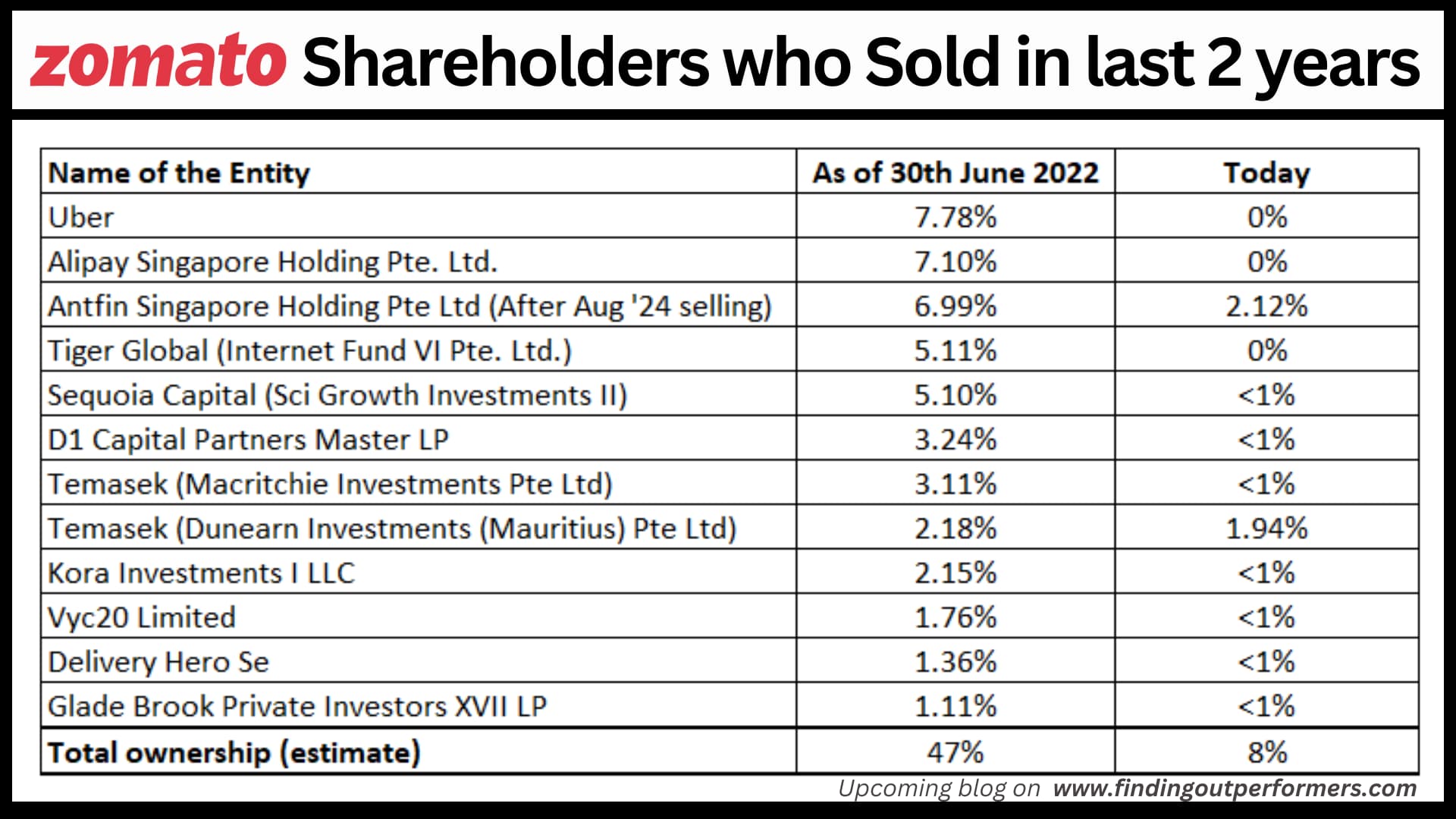

Even though Zomato’s value has surged 5 times from $5 Bn to over $25 Bn in the last 2 years, but I believe we are missing the biggest point!

The more relevant and most underappreciated fact is that the rise has happened when roughly 40% of its total equity was actually being sold by pre-IPO investors/owners in open market! Ownership of Uber, Alipay, Tiger Global Management, Sequoia and more have fallen to 0% or at below 1%. Just last week, Antfin sold its 2.12% stake in Zomato.

India has never seen a similar circumstance before, where a listed entity has continuous supply of shares being dumped in the market, adding to its free float, but the share prices doesn’t stop rising & goes on to become part of ‘Top 50’ most valued listed entity in the same time frame.

𝐐: 40% was sold, did the retail investors buy it?

𝐀𝐧𝐬: NO! The share of individual investors have actually fallen from 9.88% two years ago to 8.67% today.

Then WHO BOUGHT IT?

INSTITUTIONS! (The FPIs now own 55% of Zomato, includes Govt. of Singapore, Canadian Pension Fund, etc., and many domestic MFs which collectively own 13%) - Detailed analysis of this coming soon.

11 Likes