Zomato’s quick commerce business is now more valuable than food delivery, says Goldman Sachs.

Goldman Sachs is now valuing Blinkit at ₹119 per share at a $13 billion equity valuation. That’s higher than the food delivery business, which is being valued at ₹98 per share.

Zomato could also start subscription based service for restaurants where they provide the analytics of their own restaurants to grow and improve. This would also increase the buy orders from customers and further improve the sales for Zomato.

It’s a question of “when” rather than “if” by this time. The GMV is growing at close to 100% YoY and mind you this is in a subdued demand environment (Private consumption in Q3 was 2.2% if I’m not wrong). Q3 GMV was already 3.5k cr.

Q4FY27 GMV should be easily around 20k crs… or roughly equivalent to that of DMART’s at that point.

Infact, I forsee derating of a lot of horizontal retail plays in the market - Dmart, Reliance Retail, etc and re-rating of Zomato etc. DMART is trading at 90x multiple with growth of 15-20%. Surely a Zomato with rev growth of >50% & a hockey stick profit trajectory will be rated higher.

Blinkit has broken even. Q4 GOV was 4k crs out of which ~1800 crs is NCR only or ~45%.

NCR is growing at 7% QoQ and there’s still some space in dark store addition.

Store count should 2x in next 1 year and steady state EBITDA margins would be 4-5% of GoV

BLR and other cities will start gaining focus now.

No plans to reduce 20 rupee fee… focus on creating a service where consumers can pay (on comeptition with Zepto / Instamart as Blinkit goes to Mum & BLR)

Conservatively, Blinkit should 2x its GoV over the next year to around 20k crs. Underlying EBITDA being 800 to 1000 crs. Combined with Food Delivery, we’re looking at 2000 to 2200 crs of EBITDA.

Though actual EBITDA is likely to trend equal to Zomato’s EBITDA or around 1500 to 1700 crs for the whole year due to 0 EBITDA guidance on Blinkit.

Personally, I don’t mind the delayed path to profits because the hockey stick has become more acute now and I’m very confident that in metro cities, MT (Reliance Fresh, DMART, More, etc. etc.) will face the heat in key categories.

GOV taken for Doordash is the total value of orders completed on their marketplaces including membership fees related to DashPass and Wolt+. It does not include value of orders fulfilled through Drive, Storefront, or Bbot.

Doordash Drive is a platform that allows merchants to access a professional delivery fleet, without dealing with the logistics. Deliveries within 5 miles incur a base rate of $9.75 after that $0.75 per mile up to a maximum of 15 miles.

Doordash Storefront is a platform that allows customers to order directly from merchant’s website or social media. Merchants pay processing fees of 2.9% of the total transaction amount + $0.30 per order

Doordash Bbot is a platform that helps restaurants streamline in-store operations by allowing guests to browse menus, order, and pay using QR codes scanned at the table.

Do you have any opinion why are people happy paying a delivery fee here of 20 when Swiggy Instamart only charges 5 rupees (if you become a member of their loyalty program)? What is so valuable in ordering from Blinkit that the consumer is paying 4x delivery fee?

Blinkit has a much wider asortment and hence people have no option. The service isn’t bad, so that’s there. Lastly, the target audience that they are catering to may not care so much for the 20 bucks… they instead fatten the order (its my thesis), which is reflected in consistently higher AOVs for Blinkit.

Swiggy is still bleeding losses in its Q-Com businesss (FY25E EBITDA loss for Swiggy is likely to be around ~2400 crs) so I tend to think of their model of free deliveries as unsustainable.

Credit cards, UPI, Wallets and other bank offers makes the delivery fee go away like Onecard gives free delivery once a month, Cred UPI give cashback in range of rs.10 to 20, Simpl also gives free delivery option sometimes cashback too.

Also, the prices are actually lower even after delivery fee for some products. For example local general stores and shops in my area sell fortune oil packet for Rs. 125 -130, same goes for Rs. 117 on blinkit. Additionally, black A4 print cost Rs. 5 per page at my local print shop and blinkit does it for Rs. 3 per page plus the paper quality is far better. There are many such examples.

20 rupee fee is only applicable for small orders under 99.

5 rupee as handling charge is still there irrespective of order value. So it isn’t different from Swiggy instamart or even bigbasket.

Agree on better product catalog on Blinkit compared to counterparts.

The economics of the franchisee of quick commerce dark stores. Anyone can confirm? It does not look very lucrative. As per the tweet:

80 Lakhs is required to get a Dark Store franchise of a Q-Commerce company

All Q-commerce companies are running asset lite model by selling franchise of dark stores. Its difficult to reach a conclusion of when would a franchise owner gets its investment back & make money on the investment with so much competition to sell under 10-15 minutes

Mandates to get a Dark Store

Dark Store Franchise Fee: 8 Lakhs (One time)

Deposit 72 Lakhs for min 3000 Sq Feet warehouse

Minimum 20 Employee to be hired & their salary is on the dark store owner

Mandatory to prepare the order in less than 2 minutes

Allowed only 1500 orders per day, once exceeded a new dark store to be opened & split the orders

Avg commission per order given is 2.5-3%

All goods & expenses (Rent + Electricity + Cold Storages ) on the Q-Commerce

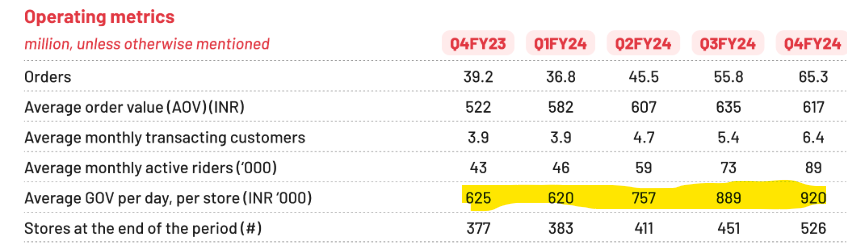

GoV per store per day (avg. Q4) = 9.2 lacs (mature stores would have upwards of 10 lacs)

Total GoV in a year = 33.58 crores

3% commission = 100 lacs

Salary + Rental (Annual) = 25 lacs + 25 lacs = 50 lacs ( i have assumed 6-7 employees… 20 seems too high)

Overheads = 15 lacs

Net income to franchise owner = 35 lacs

Some points to note:-

average GoV per store per day likely to be significantly higher for mature markets of Delhi. At 15 lac per day (assumption) for mature stores, net income bumps upto 60 / 70 lacs

GoV per store per day itself is trending up for the company

At current net income levels, payback period for franchise owners is under 2 years (even if I include deposit which is refundable)

As categories get added and Blinkit take rates go higher, some of it will percolate down to franchise owners, strengthening the model

Key Monitorable

For q-com to succeed, GoV for MT / GT have to reduce in key urban markets - NCR, BLR & Mum - so keep an eye out for SSSG for Dmart, Reliance Retail, etc… the SSSG has to show stagnation or decline - same for Amazon GoV

Sir, I implore you to read their financial statements.

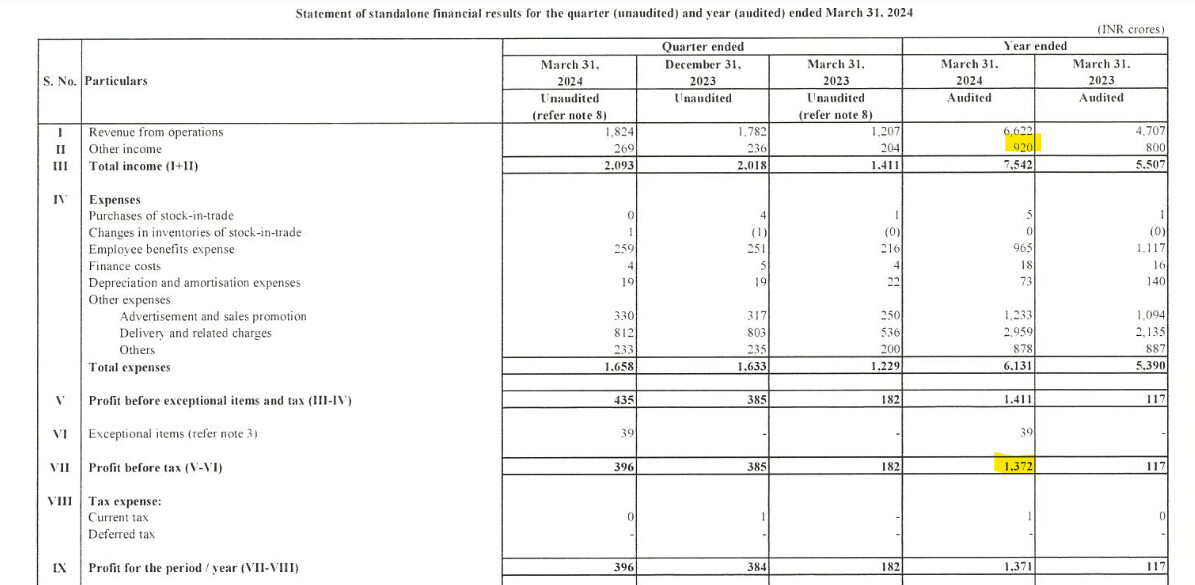

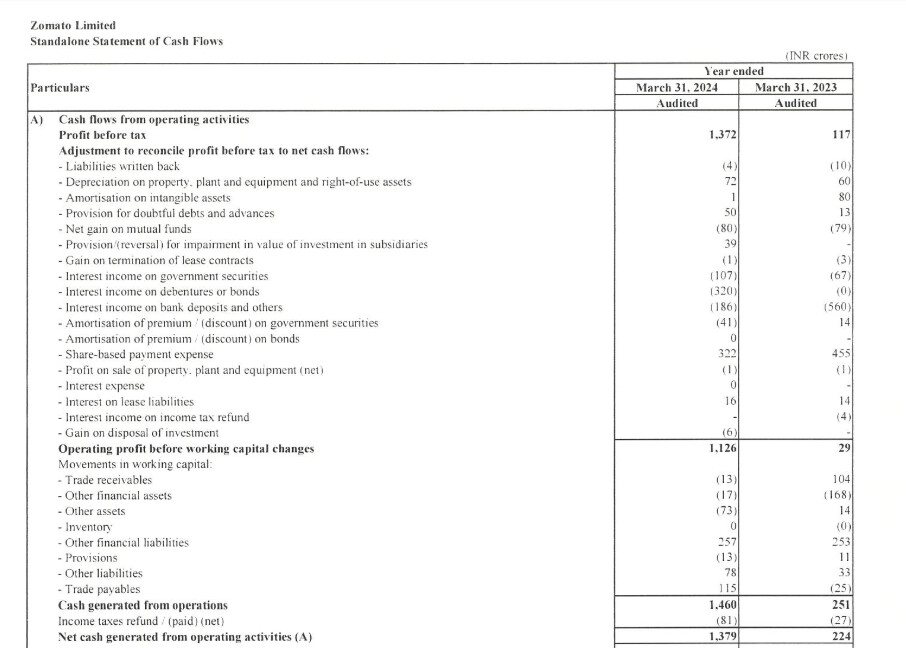

Zomato posted a standalone PAT of around 1400 crores and Q4 standalone PAT was ~400 crs. Even if you exclude other income (treasury), Zomato is PBT +ve with growing profit pools. See screenshot below:-

This isn’t correct. They’re going to open bulk of the stores in BLR & Mum and hence much of the GoV increase will come from these metro cities.

Also, how is TTM PE relevant? FY25E PAT is likely to be ~1500 crs or around 100x PE for a business growing its topline 40%+

Also, mind you, given the below par mandate, consumption is going to be back in focus… if Zomato can grow at ~25% (standalone) in a subdued consumption environment, the growth numbers in a conducive macro environment are anyone’s guess

Personally speaking, I don’t find Zomato expensive. It is just that market has better opportunities… but Zomato looks poised to deliver 100% return in next 2 years (40% CAGR)