Looked at Zaggle today, sharing my insights. It’s a little long so maybe get a coffee or tea first if you decide to read it ![]()

Revenue Broken Down by Type

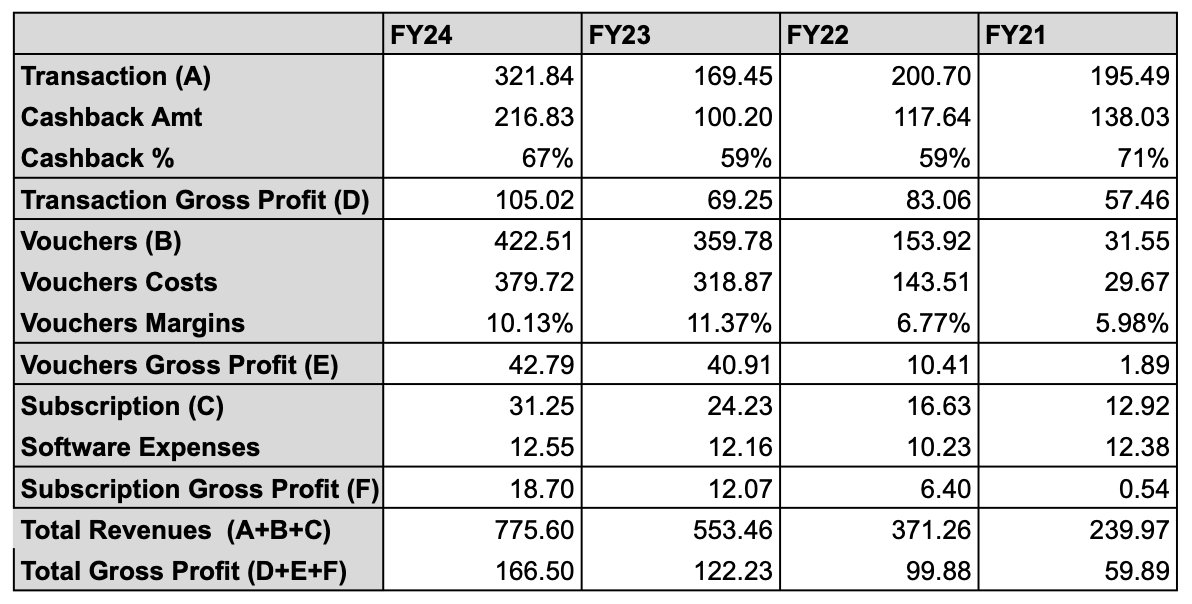

I compiled the revenue breakups and gross profits for each revenue stream from the DHRP and annual report of FY24.

Description of Revenue Types

- Subscription Revenues

- Listed as “Platform fee/SaaS fee/service fee” in Annual Reports.

- What they charge corporates/SMEs for usage of their SaaS app(s)

- Expenses directly related to it are put under “Other Expenses” in subcategory “Call centre & software support charges”. Not able to find the server costs but it might be the subcategory “Network charges”.

- It’s the lowest of all the three verticals (even in terms of gross profit)

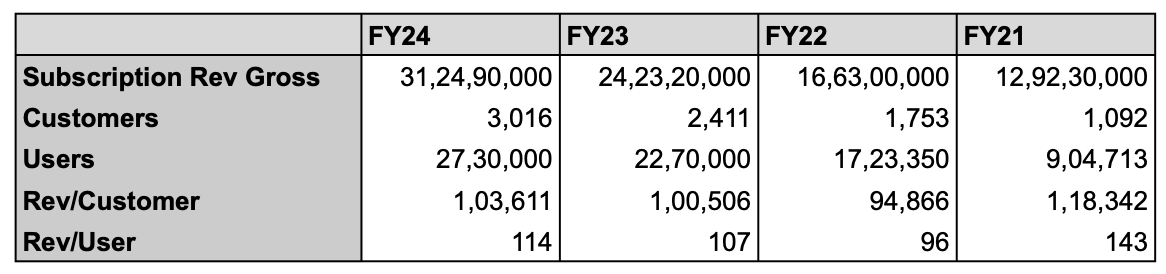

- Subscription revenue on per customer (corporate/SME) basis is ~Rs 1 lakh

- Subscription revenue on per employee basis is ~Rs 100

- There is no improvement in these figures over four financial years - for me, it shows that subscription/SaaS revenue by cross selling is not the focus but is just a lead generator for their cards and gift vouchers business.

-

Card processing fees Revenues

- Listed as “Program Fees” in Annual Reports

- Zaggle allows corporates/SMEs to provision prepaid cards or credit cards so that instead of employees spending using their own cards/UPI/cash and being reimbursed, they can just spend directly from the prepaid cards loaded by the corporate/SME.

- Significant amount of these fees are given back to the employee as cashbacks. See “Other Expenses” subcategory “Incentive/cashback”

- This is necessary as employees will always prefer to use their own personal cards if cashbacks are better and then take reimbursement from the company.

- However, if you look at FY22 and FY23 when cashbacks were reduced from 71% to 59%, this revenue stagnated and then declined. (195 cr in FY21, 200 cr in FY22, 169 cr in FY23)

- Official reason given by Zaggle for lower transaction revenue from FY22 to FY23 is the shift from online to offline purchases due to reopening (online purchases have higher transaction costs). However, I am skeptical here as they haven’t shared per transaction fees.

- IMHO, cashback going back up to 67% in FY24 is the main reason why they managed an almost 100% increase in revenues in this category (employee growth was 20% from FY23 to FY24 so that alone cannot account for it)

- Management has said that they expect to reduce cashbacks as they capture employees. However, I am skeptical here as Indians are very price sensitive and will not use these cards if their personal cards give better cashbacks

-

Vouchers Revenues

- Listed as “Propel platform revenue/gift cards” in Annual Reports

- Zaggle allows employees of corporations/SMEs to claim rewards as gift vouchers for food, shopping etc. This is analogous to your credit card’s rewards portal, except here the corporate/SME is buying these gift vouchers for employees as an incentive, bonus, to take advantage of tax exemptions etc.

- Since Zaggle goes out and buys this in bulk from the merchant (e.g. say Shopper’s Shop), they get a discount which is their revenue.

- This amount that Zaggle pays to merchants is listed as “Cost of point redemption/gift card” in the Profit & Loss statement of Annual or Quarterly Report.

- If you see FY23 and FY24 margins, it appears to have flattened out at 10-11% which is probably the maximum margin Zaggle can manage.

- IMHO, Zaggle has grown this segment very impressively. It’s gone from just 31cr to 422cr from FY21 to FY24.

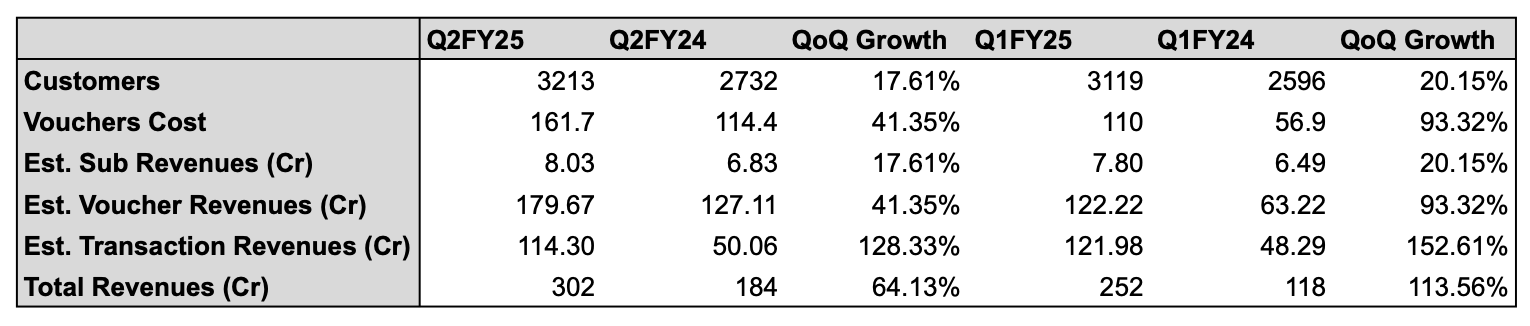

Figuring out this break down for FY25

Sadly, quarterly reports do not break down revenue by subscription, card processing fees and vouchers revenues. However, we can reverse engineer an estimate from

- “Cost of point redemption/gift card” which is listed in quarterly Profit & Loss statements. (Assuming that the margin of this segment is 10%)

- No of customers which are listed in quarterly investor presentations (We know that historical subscription revenue is approx 1L/customer and is unlikely to change)

- Total revenues minus (1) and (2) should give us Card processing fees (though, we can’t know what exact cashback % they’ve decided to go with)

Some other misc notes

- IMHO Zaggle is not a SaaS company. At 100 Rs/employee/year (which is nothing for a SME, let alone a corporate), they are pretty much giving away their software for free in hopes of capturing card processing fees and gift vouchers redemptions from employees.

- This isn’t really surprising - all corporates will already have software in place to manage and track employee spends - in fact, Zaggle seems to be targeting integration with existing workflows (e.g. SAP) rather than building an alternative

- Zaggle has highlighted their low churn rates (which are extremely impressive - they are equivalent to regular SaaS apps). However, IMHO this is a little disingenuous

- They are practically no costs for the corporate/SME (just Rs 100/employee/year)

- Their card vertical has to compete with every other card in a very competitive market e.g. there is nothing stopping an employee using their personal card for expenses so they have to figure out incentives.

- Both their card & gift voucher verticals are unlikely to be customer exclusive since it costs them practically nothing in subscription fees. There could be multiple platforms (e.g. Sodexo) with the employee having the preference to choose.

Inorganic growth through acquisitions

Acquisitions seem to be a core part of the company’s strategy. But these are extremely tricky. Generally, acquisitions are at very high multiples with the hope that cross selling will make up the difference

- Span Across IT Solutions - Paid 32 cr for a company with 4.73 cr in revenues. It seems to run a cleartax.com style product (https://taxspanner.com/). My guess is that they will use the emails of employees gathered from their prepaid card and gift vouchers to market it.

- Minority stake in Mobileware/84600 (~26%) for 15.6 cr. Seems like a pure investment play (minority stake, can’t cross sell to corporates or employees).

- US acquisition of expense management solution for which they diluted their existing shareholders by 9% - Extremely skeptical of this one as the US market is a played out market and it’ll be difficult for Zaggle to grow there.