FY’26

PAT 135

PE 70

Market Cap 9450

Here are some projections I made, please let me know what seems unrealistic, I have tried to be extremely conservative

Projection seems unrealistic because the company is eyeing some inorganic growth also and as per reports in media which may impact nonlinearity in P&L statement. We may see additional 100 cr in numbers in future if acquisitions are successful.

Spend management business has tremendous opportunities in india.

Recently the MD talked about education sector opportunity for zoyer business including fastag… These 2 verticals itself 6000 Cr market for Zoyer.

The biggest overhang presently seems their capital allocation policy -With Recent Qip money i thought they will look for Us firm acquisition. But inc42media article showing different picture like 3 acquisitions in near term. fully on domestic?? No clue about that…

as of now it seems indian market presently offers ample of opportunities for zaggle. I am worrying like if they take both us and indian market at same time they may not get solid foot on at no place.

These are my 2 cents. Happy to hear from you guys.

Listed as “Platform fee/SaaS fee/service fee” in Annual Reports.

What they charge corporates/SMEs for usage of their SaaS app(s)

Expenses directly related to it are put under “Other Expenses” in subcategory “Call centre & software support charges”. Not able to find the server costs but it might be the subcategory “Network charges”.

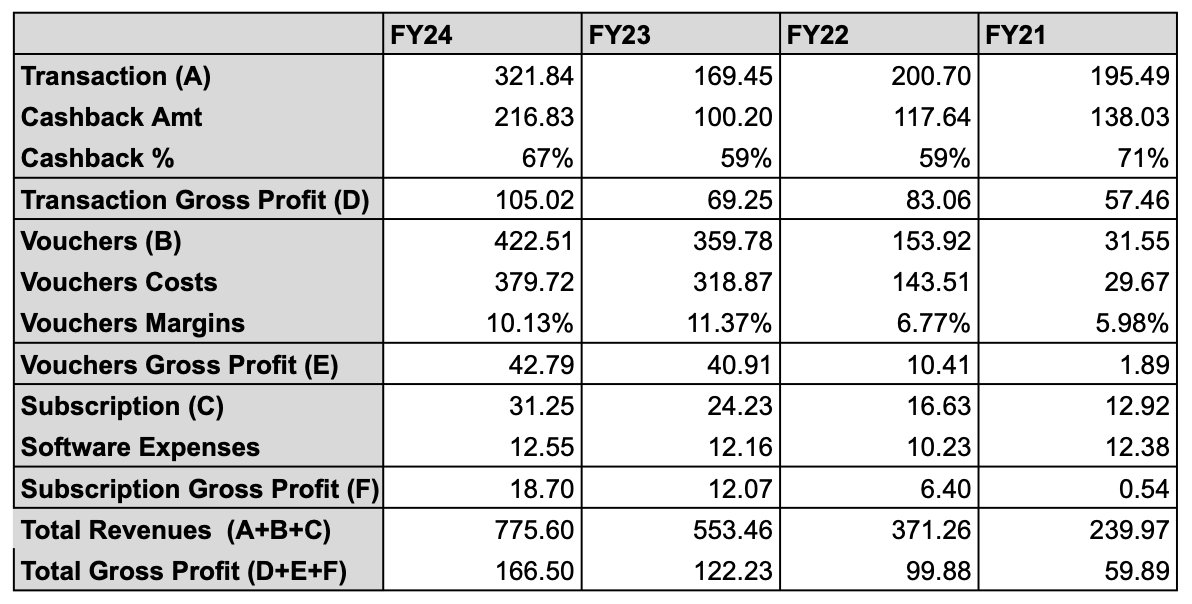

It’s the lowest of all the three verticals (even in terms of gross profit)

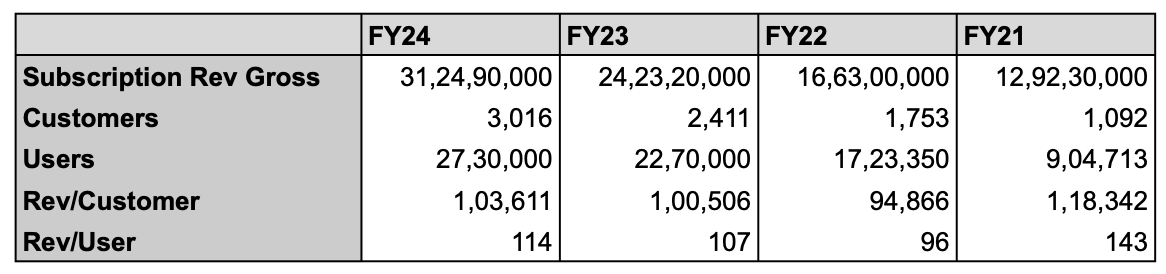

Subscription revenue on per customer (corporate/SME) basis is ~Rs 1 lakh

Subscription revenue on per employee basis is ~Rs 100

There is no improvement in these figures over four financial years - for me, it shows that subscription/SaaS revenue by cross selling is not the focus but is just a lead generator for their cards and gift vouchers business.

Zaggle allows corporates/SMEs to provision prepaid cards or credit cards so that instead of employees spending using their own cards/UPI/cash and being reimbursed, they can just spend directly from the prepaid cards loaded by the corporate/SME.

Significant amount of these fees are given back to the employee as cashbacks. See “Other Expenses” subcategory “Incentive/cashback”

This is necessary as employees will always prefer to use their own personal cards if cashbacks are better and then take reimbursement from the company.

However, if you look at FY22 and FY23 when cashbacks were reduced from 71% to 59%, this revenue stagnated and then declined. (195 cr in FY21, 200 cr in FY22, 169 cr in FY23)

Official reason given by Zaggle for lower transaction revenue from FY22 to FY23 is the shift from online to offline purchases due to reopening (online purchases have higher transaction costs). However, I am skeptical here as they haven’t shared per transaction fees.

IMHO, cashback going back up to 67% in FY24 is the main reason why they managed an almost 100% increase in revenues in this category (employee growth was 20% from FY23 to FY24 so that alone cannot account for it)

Management has said that they expect to reduce cashbacks as they capture employees. However, I am skeptical here as Indians are very price sensitive and will not use these cards if their personal cards give better cashbacks

Vouchers Revenues

Listed as “Propel platform revenue/gift cards” in Annual Reports

Zaggle allows employees of corporations/SMEs to claim rewards as gift vouchers for food, shopping etc. This is analogous to your credit card’s rewards portal, except here the corporate/SME is buying these gift vouchers for employees as an incentive, bonus, to take advantage of tax exemptions etc.

Since Zaggle goes out and buys this in bulk from the merchant (e.g. say Shopper’s Shop), they get a discount which is their revenue.

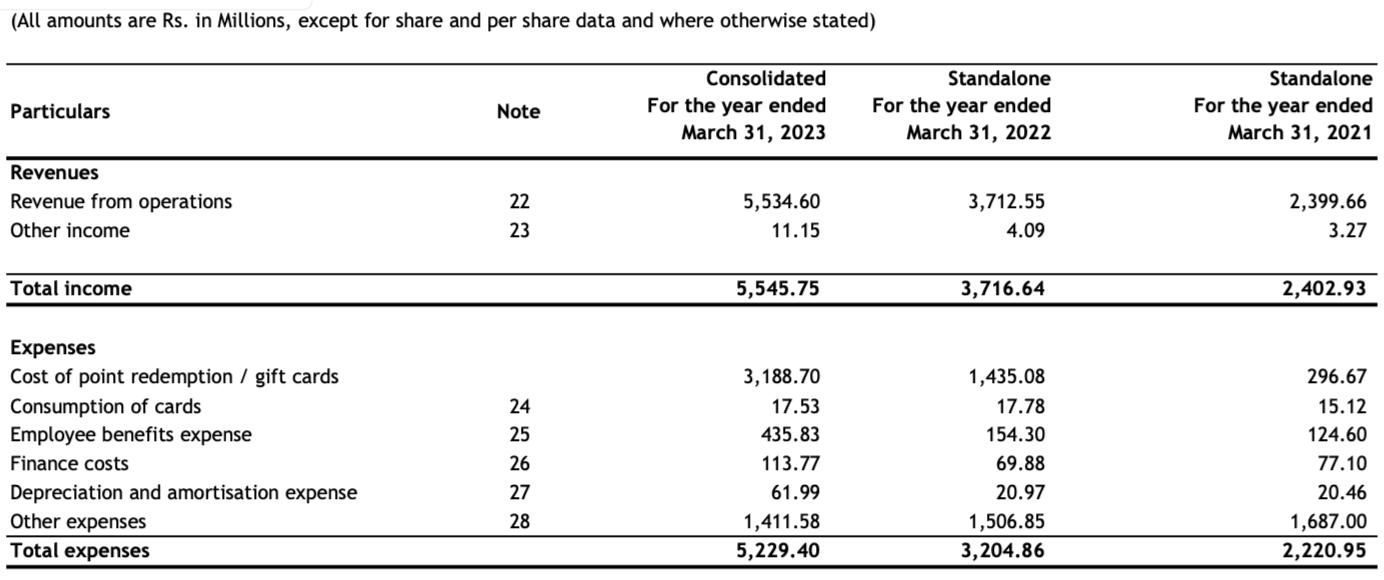

This amount that Zaggle pays to merchants is listed as “Cost of point redemption/gift card” in the Profit & Loss statement of Annual or Quarterly Report.

If you see FY23 and FY24 margins, it appears to have flattened out at 10-11% which is probably the maximum margin Zaggle can manage.

IMHO, Zaggle has grown this segment very impressively. It’s gone from just 31cr to 422cr from FY21 to FY24.

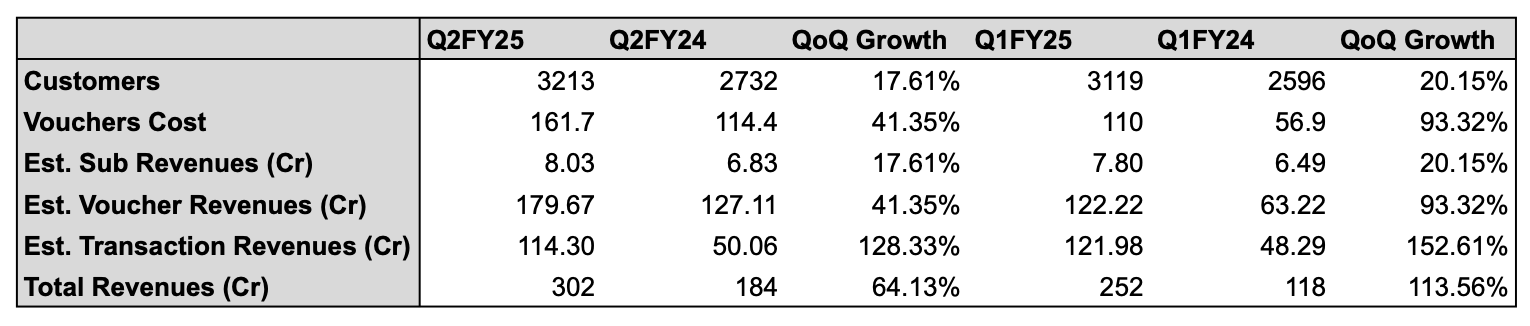

Figuring out this break down for FY25

Sadly, quarterly reports do not break down revenue by subscription, card processing fees and vouchers revenues. However, we can reverse engineer an estimate from

“Cost of point redemption/gift card” which is listed in quarterly Profit & Loss statements. (Assuming that the margin of this segment is 10%)

No of customers which are listed in quarterly investor presentations (We know that historical subscription revenue is approx 1L/customer and is unlikely to change)

Total revenues minus (1) and (2) should give us Card processing fees (though, we can’t know what exact cashback % they’ve decided to go with)

IMHO Zaggle is not a SaaS company. At 100 Rs/employee/year (which is nothing for a SME, let alone a corporate), they are pretty much giving away their software for free in hopes of capturing card processing fees and gift vouchers redemptions from employees.

This isn’t really surprising - all corporates will already have software in place to manage and track employee spends - in fact, Zaggle seems to be targeting integration with existing workflows (e.g. SAP) rather than building an alternative

Zaggle has highlighted their low churn rates (which are extremely impressive - they are equivalent to regular SaaS apps). However, IMHO this is a little disingenuous

They are practically no costs for the corporate/SME (just Rs 100/employee/year)

Their card vertical has to compete with every other card in a very competitive market e.g. there is nothing stopping an employee using their personal card for expenses so they have to figure out incentives.

Both their card & gift voucher verticals are unlikely to be customer exclusive since it costs them practically nothing in subscription fees. There could be multiple platforms (e.g. Sodexo) with the employee having the preference to choose.

Inorganic growth through acquisitions

Acquisitions seem to be a core part of the company’s strategy. But these are extremely tricky. Generally, acquisitions are at very high multiples with the hope that cross selling will make up the difference

Span Across IT Solutions - Paid 32 cr for a company with 4.73 cr in revenues. It seems to run a cleartax.com style product (https://taxspanner.com/). My guess is that they will use the emails of employees gathered from their prepaid card and gift vouchers to market it.

Minority stake in Mobileware/84600 (~26%) for 15.6 cr. Seems like a pure investment play (minority stake, can’t cross sell to corporates or employees).

US acquisition of expense management solution for which they diluted their existing shareholders by 9% - Extremely skeptical of this one as the US market is a played out market and it’ll be difficult for Zaggle to grow there.

Good assessment. I agree that Zaggle is not a SaaS company. They just report a very small percentage of their revenue as the software/SaaS fee. It is unlikely to increase exponentially (unless they venture into newer geography, which will come with other challenges) despite the flurry of new contract wins over last few months. Having said that, I think there is lot of scope for their program fee to go up non-linearly. While there is no compulsion of the employees to use the corporate credit card, I think the employers would want their employees to use it since it is integrated to the expense management and the reconciliation is easier. In the firm I work for, we use SAP concur and our employer recommends using only the corporate credit card which eliminates the ‘leaks’.

Coming to future growth, I think Zoyer is finding lot of new use cases and I think Zaggle is doing well to promote it amongst the MSME companies. They offer petty cash management, fleet management and now they are exploring the fee management from the educational institutions. Forget the overseas market, even in India there is a huge untapped market with almost zero competition.

In the same interview Raj has given the consolidated growth guidance of 2x the FY24 revenue by FY26 (which is very conservative as they will reach 55-60% of this target in FY25 alone). Raj went ahead and gave the FY27 growth guidance of 80%.

They are also planning multiple inorganic opportunities which will add new levers of growth. They aim to do 5 acquisitions with the QIP money and the money that was left from the IPO proceeds. Some of the areas that they are exploring includes Fasttag, card system companies that integrates with Point of Sale (PoS) and a company specialising in accounts receivable solutions (Same area in which Zoyer operates).

Their aim is to become a 1bllion dollar revenue company (more than 8x from the current levels within 5-6 years) and I think it will be interesting to see what the future holds.

My only worry about Zaggle is that despite the profits the cash flow from operations has remained negative, hopefully with scale this will change and we will see more sustainable growth.

Thanks for taking the time to read my analysis! You do raise some interesting points, some of which I agree with and some I disagree

I agree Program Fees/Transactions and Gift Vouchers can be scaled non-linearly. If you look at the latest quarter (third table in my analysis), customers have grown ~18% while revenues have grown 64% and vouchers cost have grown ~41%. Since its unlikely that subscription revenue would have grown non-linearly, we can safely assume transactions have grown non-linearly as well. So yes, they are executing quite well.

Thanks for sharing the guidance nos - I think 55-60% by FY25 and 2x by FY26 will be easily achieved. 80% growth in FY27 (which would be more than FY25 and FY26 growth) from a much bigger base in FY26 will be their real test as that will depends on their acquisitions and new products, transactions and gift vouchers will be unlikely to get them all the way there.

Regarding Zoyer - I am going the not impressed route. It’s a free product (you can sign up for it on zoyer.zaggle.in) and there are actually dozens of SaaS apps for expenses management, fleet management, vendor management, educational institution management etc. These SaaS apps range from huge targeting multinationals (SAP, Salesforce etc) to small inexpensive apps (e.g. Expensify, Classpro etc). The app itself is not that impressive (very few features, quite buggy, no mobile apps). The only thing it has going for it is its free and clearly the goal is to make money from transactions within the app (e.g. like the inward remittance option).

Regarding negative OCF, I wouldn’t worry too much about it. People get too fixated on profits and cash flows for early stage tech companies but their gross profit margins are good (see table one) and you have to spend on product development & they’ve decided to spend a lot on acquisitions as well . Once they reach a more mature stage with less product development and acquisitions, it’ll move to positive.

Definitely keeping a close watch on Zaggle, its an interesting company to track.

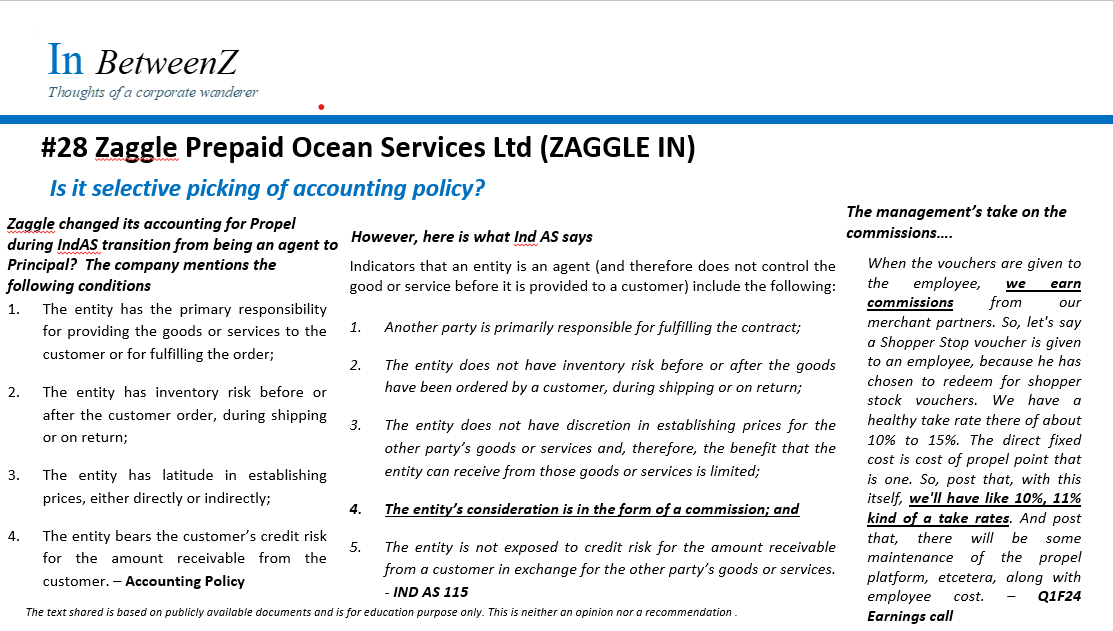

Wasn’t this due to change in some revenue recognition policy ? I remember they went from net revenue to gross transaction value, that’s why there was also a fall in margins accordingly

According to their About Us section on their website, they launched the gift voucher platform (Propel) in 2019 so FY21 was probably their first full FY of the gift voucher platform.

Whatever change they made, it probably was before they filed their DHRP I guess. The text is mostly arguing that its disingenuous for Zaggle to report the entire value of the gift voucher as revenue, instead they should just report the commission they get from the merchant.

Earlier they also guided that in 3 years time their margins will reach mid-teens which means the profits will grow at even faster rate. If they reach anywhere near these targets, there will be significant wealth creation along the way for shareholders. I also think they have to further dilute the equity to acquire the companies to achieve this target. At some point I hope they generate enough cash to redeploy that back to the business to pursue the growth journey in a more sustainable way.

In terms of guidance we can focus on FY’25 for now which should be around 55% plus on both Topline and Bottomline.

For FY’26 management has not given any specific guidance, although they have guided that FY’26 should be double of FY’24, I believe they can do much better than that.

Based on my analysis we can have 50% plus growth in FY’26 over FY’25 in both topline and bottomline but I would like to see Q3 FY’25 numbers before coming to any conclusion, also let us see what management guides.

I believe that the Zaggle management is trustworthy and are interested in creating long term value for all stakeholders.

Based on the number of order wins they have had over the last 2-3 months, they seem to be doing really well.

To some extent agree on your thought!!!

But Two of the strategy

Business makes profitable and generate enough cash ~ say 15-20% EBITDA margin and then after grow organically as well as inorganically (e.g. Sundaram Finance, Caplin Point etc.)

Growth at Initial level either organically or inorganically and then after large profit will be coming

Either one strategy is workable IF Management is good and deliver the result Plus NO issue on Corporate Governance!!! The Zaggle under the Second category because they are seeing some kind of Opportunity, TAM, few players in the market!!!

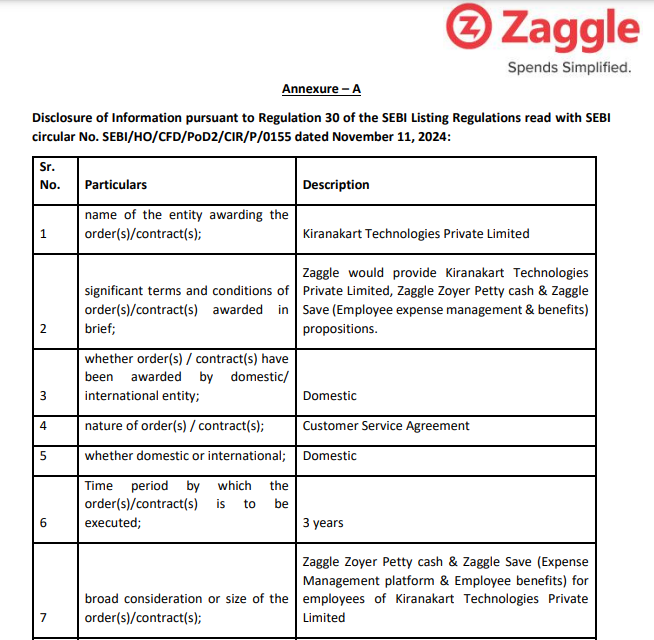

Found the below article on pressreader in which Raj Narayanam reiterated the plans to 3 acquisitions by the end of FY26 in merchant card software, FASTag and accounts receivable domains. While they had zeroed in 5 companies initially, they have dropped 2 of them. Out of the remaining 3, they are close to signing the term sheet for one of them and they are doing due diligence for the other 2 firms. If all the 3 deals go through it will add 600crs to the topline. There is no clarity with respect to the margins, but hopefully it will not dilute the margins of Zaggle a lot. You can read the full article using the below link.

I can answer this from an online payment collection perspective, most payment gateways enable prepaid cards by default. For example, when bigbasket contracts with Razorpay to enable online payments, then Razorpay’s default setting will be to enable prepaid instruments (PPI cards) such as Zaggle. PPI cards can have higher MDRs and merchants (bigbasket) have the option to disable prepaid cards. So low margin businesses such as utility bills or grocery businesses may disable prepaid cards or pass on this cost to customer.