So I finally got some time to think about valuation of Zaggle ![]()

Financial Projections

I collated assorted management guidances to build a future picture of how the financials will play out.

Summarizing all the management guidance below

- 58-63% sales growth for FY25. Taken 59.5% sales growth to calculate FY25 sales (Q3FY25 Concall)^

- 9-10% FY25 EBITDA margins, 10-11% FY26 EBITDA margins, longterm EBITDA margins of 15-16%. (Q3FY25 Concall)

- $1B revenue guidance by FY30 so I’ve projected out what a sales growth pathway from FY25 to FY30 with 8000 Cr target might look like (Q4FY24 Concall I believe)

- PAT margins are calculated by from FY24, FY23, FY22 average differential of 2.25% between EBITDA and PAT margins

- Shares outstanding assumes 0.56% growth in shares outstanding due to ESOPs and no further equity raises (based on 0.42% growth in shares outstanding from Q3FY24 to Q2FY25 - ignoring Q3FY25 due to big bump in shares outstanding due to QIP equity raise)

^Wanted to take midpoint which would have been 60.5% but accidently calculated midpoint at 59.5%. Too lazy to update and retake screenshots so I’ll leave it as it is because it doesn’t make much of a difference.

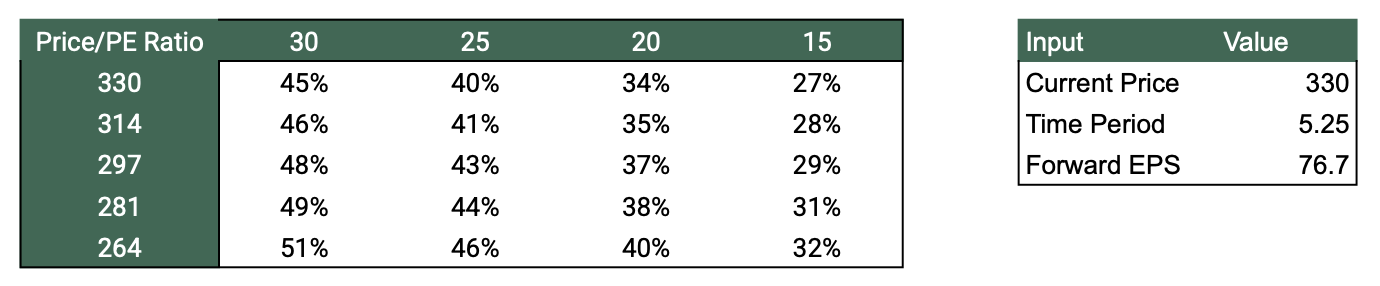

So what kind of returns can you expect in little assuming you hold to FY25 results? I’ve tabulated the returns below for different CMPs and PE ratios at which it will trade at.

So you can expect 27% to 51% returns depending on your entry price and the PE ratio at FY30. Not bad ![]()

But what if guidances don’t play out?

Management guidance is always the best case scenario, especially so far into the future (5 years!). I’ve projected out three scenarios below

Hit margin guidance but miss sales guidance

Instead of 8000 cr in sales, I project 4000 cr in sales by FY30 while keeping margin expansion pathway constant.

Gives us an projected EPS on Rs 38.35 in FY30.

At CMP of Rs 330, return would range from 27% to 11%. Not bad actually.

Hit sales guidance but miss margin guidance

Keeping sales guidance of 8000cr, I project margins settling at 12-13% instead of 15-16%

Gives us an projected EPS on Rs 59.33 in FY30.

At CMP of Rs 330, return would range from 21% to 38%

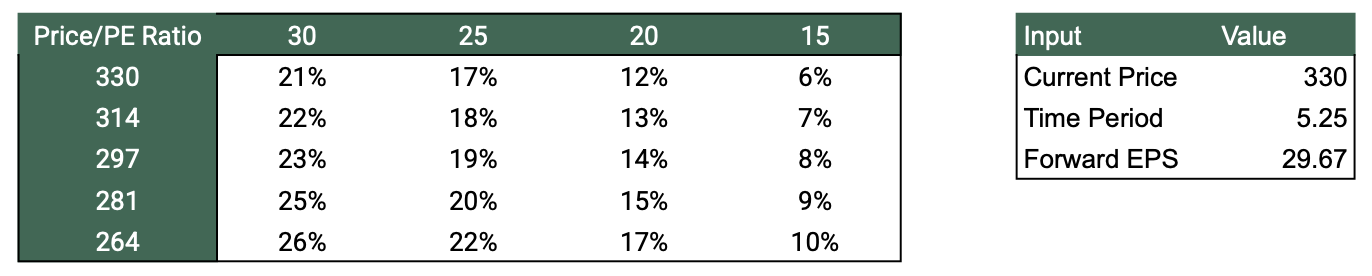

Both sales and margin guidance miss

I project sales to grow to 4000 Cr and margins settling at 12-13%

Gives us an projected EPS on Rs 29.67 in FY30.

At CMP of Rs 330, return would range from 6% to 21%

Final Words

Based on personal experiences in the software industry, I remain skeptical of management targets of 8000Cr in sales and margin targets of 15-16% by FY30.

However, even the reasonable worst case scenarios aren’t so bad. If Zaggle is still growing sales at 18% in FY30, it should command plausibly trade at a PE ratio between 20 to 25 which would give a return of 12% to 17%.

Not much safety but any outperformance from worst case scenario would likely result in market beating returns from CMP.

Disc: No positions yet but planning to take up a position when it stops hitting LCs ![]()