Importance of Facts Figures triggers and rules in creating wealth

Facts:

The installed capacity ( IOL or EPL has good capacities but will this will help in short term or in long term , ultimate product is have how much NPM ) .

Manpower (routines / modules generated by IT company or API created by any pharma company how much these skill set can be reutilised to develop new product or service question must be asked or looked for does they always start from scratch or generate from already found themes ).

Management past decisions and allocation of resources ( delegation of powers by Motherson sumi in the acquired companies , Piramal’s acquisition of old companies where they delisted the company made me to exited from DHFL at the last bounce of dead cat ) .

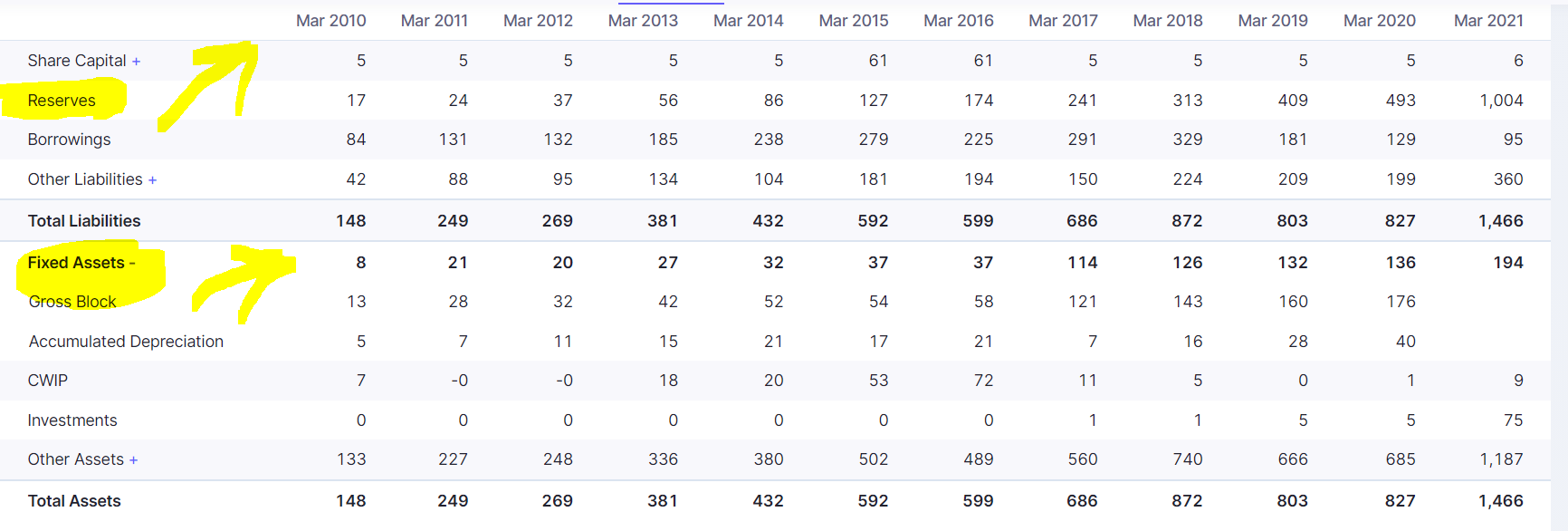

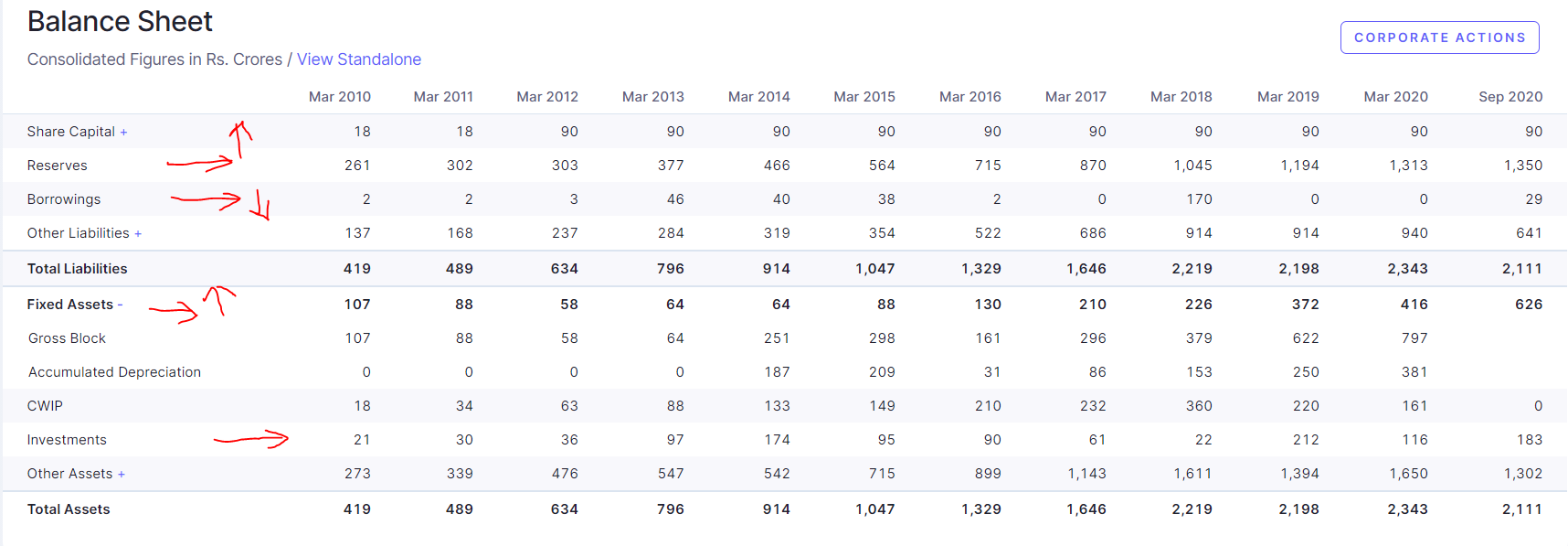

Need to investigate in to the Surplus as it may have provisions of contingent liabilities; the lawsuits and the pension

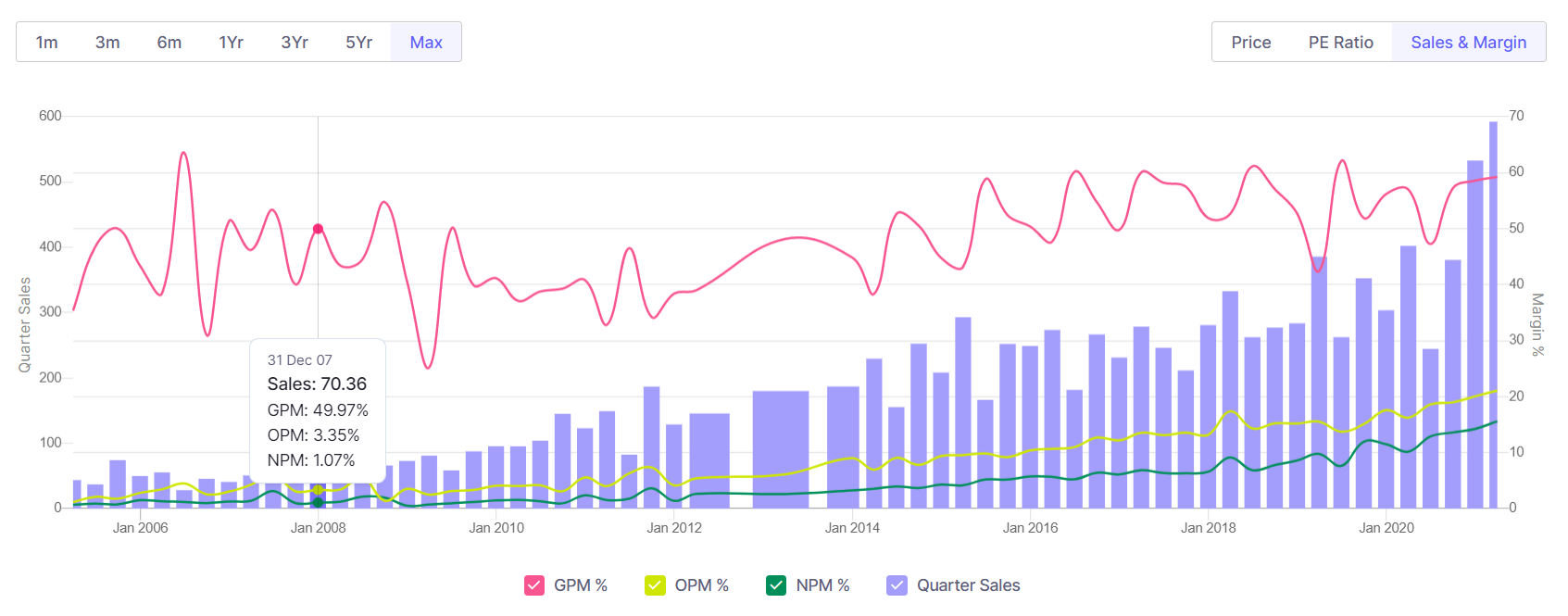

When management says We have increased market share it sound GOOD check does they cut the price to improve the volumes of sale this will reflected in lower OPM and NP .

major share in domestic and international markets (check should be made to determine for demand contraction or expansion and how a company is faring in the dynamics of the business ).

Figures

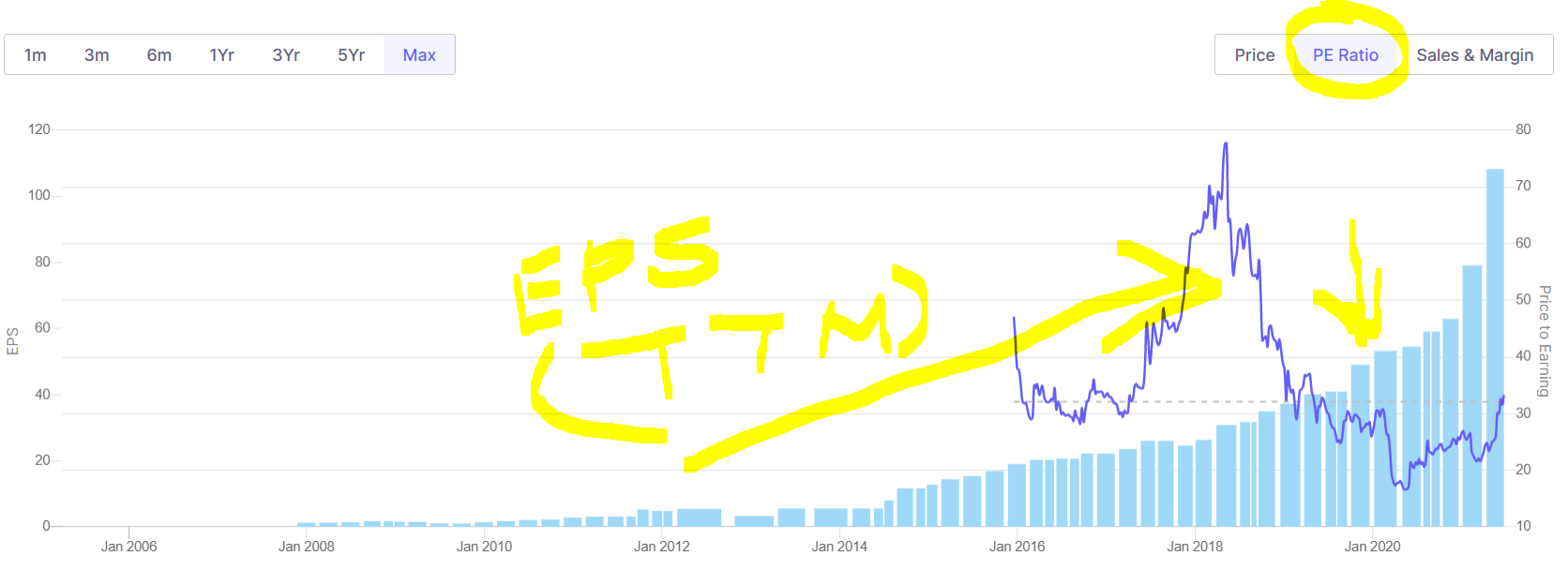

The charting of price movements, ADX, RSI, crossing of 50 SMA on 200 SMA , is stock is moving above 200 SMA , is stock is making new highs of 52 week

Analysis of working capital , debt & fixed cost , *Working capital, also known as net working capital (NWC), is the difference between a company’s current assets, such as cash, accounts receivable (customers’ unpaid bills), and inventories of raw materials and finished goods, and its current liabilities, such as accounts payable. [Even if the company has no debt or negligible yet the more amount is tied in the inventory or high receivable thus result of high loss due to opportunity cost ]

Triggers

Is there any changes in the govt policy like dumping duty , additional export benefits, state excise or taxation exemptions or legislature changes ( e.g blending of ethanol and incentive or increased minimum support price ) ., capex is near completion ( some state offers better incentivised tax structure in order to support the industry in their state to improve the employment and growth of the state ( pharma in baddi barotiwala ( Himachal ), Vapi -Ahemadabad -Badodara( Gujrat ) , improved infrastructure e.g gas pipes or relaxed norms for pollution , Elephants can dance but only a few those are in circus.. those big blue chips which constantly increasing their basket of offering with improving margins can able to move faster than their peers good example are Britania , Pidilite , Asian Paints … but most of the cases in big companies’ high margin business income support the low margin business ( best example is ITC ) . We as retail investors sometimes failed to estimate the claims which may arise in future e.g due to prolonged smoking Ciggrate companies sometime susceptible to damages this happen in pasts in develop countries …

Always has question which sector will be the darling of the street next time for that one need to learn about the dynamics of the market and how to find NEXT APPLE in that sector. For that we must check the global index movements… usually the sector which is boring and often out of flavour of market give rise to selection of good compounders ( at this time hotel / aviation / engineering / housing are leggared ) so making invest is one thing and sticking to that bet is is more crucial we always jump to book the profit and keep the lose making …i had kept DHFL even up to 91% loss but at last managed to sold at 59% loss … which is almost 1/10th of my portfolio

Rules

One must sticks to YOUR OWN created rules ( You only know YOUR risk appetite ). No expert is 100% correct … Timing market is very very hard and it is next to impossible on all the occasions …

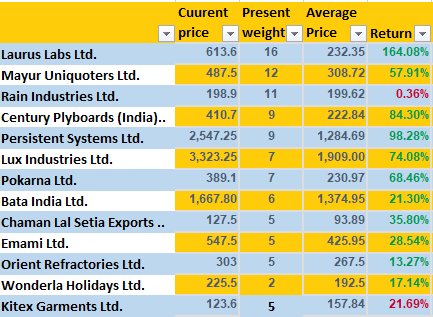

Set you max bet per stock e.g 15 to 20% Set you max bet per sector may be 25 to 30% Set your return or time stamp on your investment to get exit ( it doesn’t mean one must exit at set target one must read the concall and evaluate the prospects of the company it happened that I was once 60% down in rain industries ( lots of stuff happened in three years one must visit the tread in second company Chaman Lal Setia 63% down yet I was just lucky and able to convince myself that in long term the will survive and they do … but it can’t be universally applied to all the firms so YOU and YOUR Decisions are supreme to create YOUR wealth .

Put the money in trenches and exit should be also in trenches …

Diverse or confined portfolio / Blue chip or small cap or mid cap / Short term investment or buy & hold strategy

As long as they are up and running doesn’t make a huge difference in long run but one must understand HoW equity price getting rerated … it is Expected returns of the share holders and mostly big players or ace investor participation in that company make a huge impact on price movements e.g MF , DI , FI , ANALYST call for buy and sell can lure the investors and call for action from these fund house create a lots of churn in individual portfolio which make a huge difference in long term but it is true that 100% analyst are not sure what they are suggesting and often not able to live to their own TARGET if they would Why they cant have 100% allocation in that stock only ? why average MF has more that 20 positions in their holding ? why they have multiple schemes hybrid , equity , debt . small cap , mid cap or blue chip or nifty …

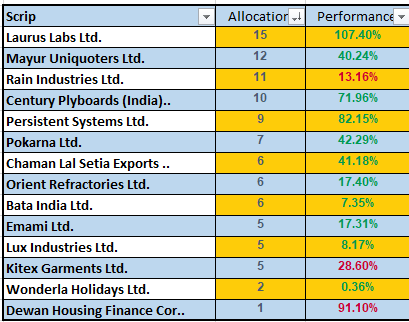

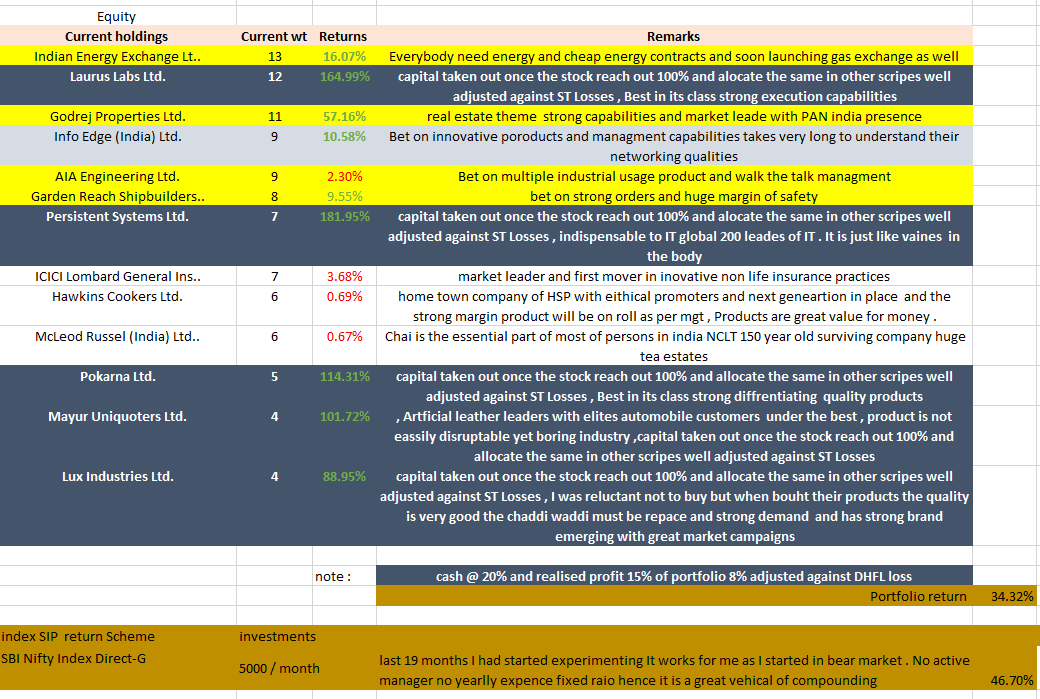

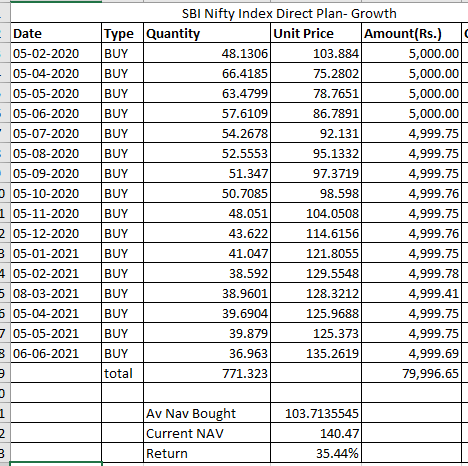

I share my own investment which I had practiced during last 16 months by investing in small chunks on regular basis

i am not advocating this is perfect way but ,most of time it remove personal biased and return are in high nineties of the percentile of the whole companies

portfolio

Disc: this shared for learning and not any company mentioned above should be treated as recommendation to buy sell or hold , i may or may not inform the forum before buying more or sell any of my portfolio companies . i am not any sebi approved analyst or broker one must consult registered practitioner / broker before making any investment decision

.

.