Results as you mentioned is bad . Rising capex results more depreciation , The interest payment is increased , The increase in receivables and inventory made me worry and stopping me to enter in the scrip . The whopping fall of 86% in net profit Q4 on yoy basis also raise eyebrow Net Profit ₹ 2.43 crs from ₹ 17.73 crs dip is also most -86%

Regarding opening and Covid effect company had made filing with exchange

disc : Watching not invested Yet . This is not any recommendation of buy sell or hold

As we know that this quarter will be squashed - however due to ongoing border tensions and government of india and globally opening doors for chemical companies for India - your views on that? Most of the chemical companies in Shanghai closed due to government regulations and environmental concerns as on (2019) - we haven’t been able to see any twist in the story.

Chart of Malic acid as per USD : Growing at a steady pace of 5% CAGR annually

Whereas India grew up about 1.5%

Chart of Fumaric acid as per USD : Growing at a steady pace of 13% CAGR anually

Nitin the CHANGE is ONLY thing WHICH is PERMANNET IN NATURE . so small time tension won’t be affecting when one take long term views say more than two years … I am sharing my thought regarding the point raised by you . I may be wrong my perception but what I feel india won’t be the only country which will be tapping benefit from the closure / slow down of the chemical industry in the china . it may be a trigger but at the same time India need some structural reforms in order to absorb the diverged demand from abroad .

No doubt we have seen this happened in past if one consider the rise of IT , the rise of pharmaceuticals in the past but will that happen this time in chemicals space ? I frankly don’t know .

The API is kind of commodity and commodity companies most of the case does not enjoy the pricing power unless it is lowest cost producer among company’s global peers . we have god companies which can be game changer . but as a retail investor we must understand the scope of opportunity size and if company is growing it’s market share and increasing it’s capacity that too from it’s internal sources .

We have whiteness sometime when we want to check d/e ratio if a company is also rising debts and at the same time it also increasing the dilution of equity so in that case both numerator and denominators both increases , so flatly seeing the ratio alone wont help a retail investor , But one need to understand the numbers and operating cash generated by the company and how the company is returning back money to the retail customers . now

HOW to understand thus better so investor must find ratio of CFO / PAT it must be above 0.7 .

Human mind seeks to see the pattern and numbers in whole or easy ,multiple of 10 , 25, 100 or thousands . I am not different when I see some odd number in quantity i don’t find easy that’s the reason i made some top up made in the existing scrips in portfolio to look easy multiple. The reason above is not the actual reason but why i have made new investment as i have more conviction in the companies and now they offer me more margin of safety

Mayur uniquoters Limited

Rain industries

Chaman Lal Setia

disc; please do your own research before investing this is not any recommendation to buy sell or hold . i may be exiting or entering without intimation to forum . I am not any sebi approved analyst or consultant

Regards .

@yourraj What is your rationale in investing in Rain Industries. There are headwinds in terms of declining aluminium demand and increasing supply of CPC from China.

if you see the aluminum as a commodity it is cyclical when you buy near the base of cycle within 3 to 4 years it gave 2x to 3x return . You are right the price of commodity is no very strong but at the same time it is second most important engineering material used in the race of human kind . investing in rain initially due to a copy idea but later on I found good promotor sitting behind the driving wheel who can steer the vehicle very well in the difficult time . It has advantage of low cost producer and risk is geographically divided . They have done number of good things in the past …

Portfolio change

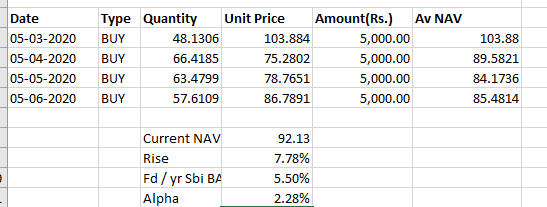

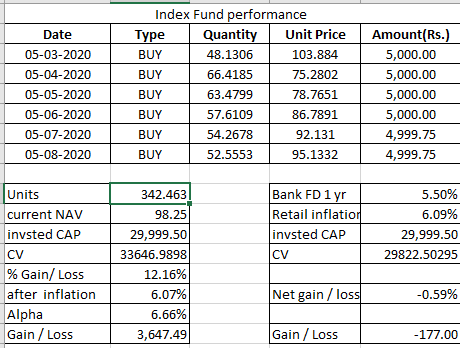

I have started some experimenting by investing automatic mode through SIP

Since April I had made sip in SBI index fund the performance is not too bad her is below illustration

Addition small tracking or putting a seed in the small micro cap company Lykis ltd … it has more FCF than its cap in last year and has a good portfolio of products .

Allocated proceeds of IOL chemicals in to Transpek Ltd around 8% of portfolio size . It is bet on the numbers rather than going deep in to AR’s .OPM >20% , improving debtors days , and inventory turnover ,

March 2009 to March 2020

cash reserve 44 to 333 (7.5x)

Reduction of debt is added feather

Gross block double 113 to 263 (2.3x)

investment fron 4 to 118 (29x)

share capital is not diluted

Sales 167 to 595 ( 3.5x)

Manufacturing cost 14% to 9%

Other cost from 20% to 13%

share price 48 to 1539 (32x)

So it is creating wealth for both share holders as well of the promotors

I was skeptical yet continued to invest because of below two things where number are not matching first is the Tax paid in cash flow statements Vs in balance sheet is not matching and secondly

The receivable in balance sheet is more than the receivables in cash flow @hitesh2710 could you please find your time me to understand these two things are these red flags ?

Regards

Disc; these are not any recommendation to buy or sell or hold or used the Strategy of index investing . Please consider these are learning and sharing activity . I am not any sebi approved broker or analyst

Portfolio change : one in and one out Eicher (is out ) (Being time bet made + 9% and moved the proceed to 3M India Limited ( is in ) - 2% of the portfolio – which I had planned long ago but waited for the correction to happen in the counter which is is added in permanent Portfolio . It has ethical business practices in the world and is steady compounder . I don’t know how this will move but still I am sure it will better than FD of the Bank in short term and will be good compounding scrip .

Monthly sip done index fund 5-7-2020 buy 54.268 units nav 92.13

Another change is been made in order to have better allocation small portions ( SBI CARD one lot of 19 ( sold at loss 5% )-----> Cant understand the business ( First ever allotted any IPO yet not convince about the business quality + ITC ( at gain 5% ) —> Too many products and subsidiaries I think I am not in position to understand the business so I left +Gillette ( sold at loss 11% ) + Bandhan bank ( no profit no loss ) --> may be adding some other day ) which were purchase in march is clubbed together and allocated in to the Shree cement ( 5% of the Portfolio current weight ) in the Long Portfolio but I don’t know I would be able to keep this long or not Lets just pinned as a timeline of investment and see how this will perform . bet is on he management’s better utilisation of the capital and moving to new territory middle east with improved margins . It has more EBITA Margins and growing capacity in eastern corridor … ( edit made 7-7-2020)

Disc : This not any recommendation to buy sell or hold I am not any sebi approved analyst

Portfolio change

one out one in : Solara Active Pharma Sciences Limited Out and Alembic Pharmaceuticals in

I don’t know why the Solara Active Pharma Sciences Limited Promoter holding showing pledging of the 50% of the stock held by the promoter group yet today it shoots to 8% high in a day . I checked the filing of the company at https://www.bseindia.com/corporates/shpSecurities.aspx?scripcd=541540&qtrid=106.00 .

Where it shows Whether any shares held by promoters are pledge or otherwise encumbered? as YES I couldn’t resist myself to walk out of the company as this is a big RED flag but in order to preserve the capital I exit .

I have exited from two more stocks :

a) Complete Exit from HDFC AMC it was very small portion of portfolio and reached the limit -25% :

b) Complete exit from Lykis : I bet on the promoter but when I red out the annul reports I found there are lots of reflags on the accounting polices . The company is promoted by famous Vijay Kedia . ( minor profit )

I had hard times learned the lesson that Preserving capital is also vital when the things are not clear in near future .

regards

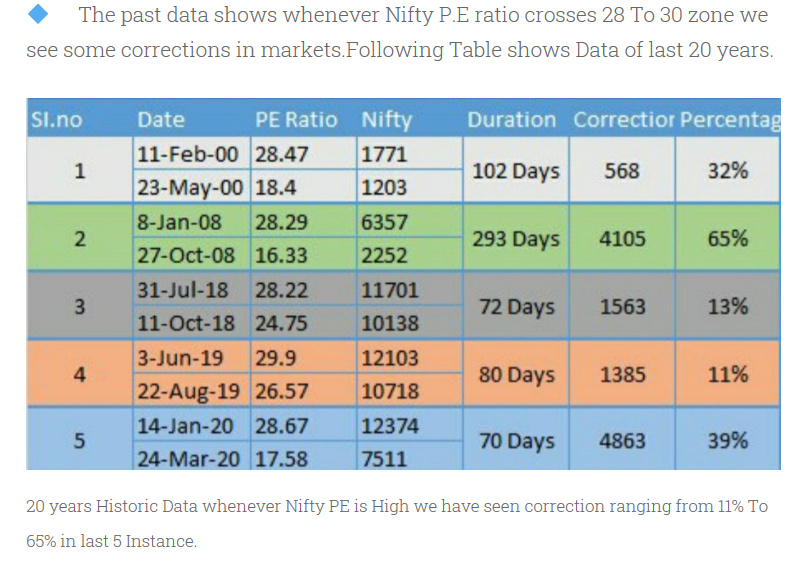

Near term correction is coming one must either sit tight on the stocks those having strong fundamentals or improving the top lines or take vacation from the stock market for sometimes . @dineshssairam could you please comment on below

Market has recovered too FAST and creating a bubble to burst .

On whole the sales are not improving the margins are squeezing.

The unemployment has risen much.

The interest rates are gone down.

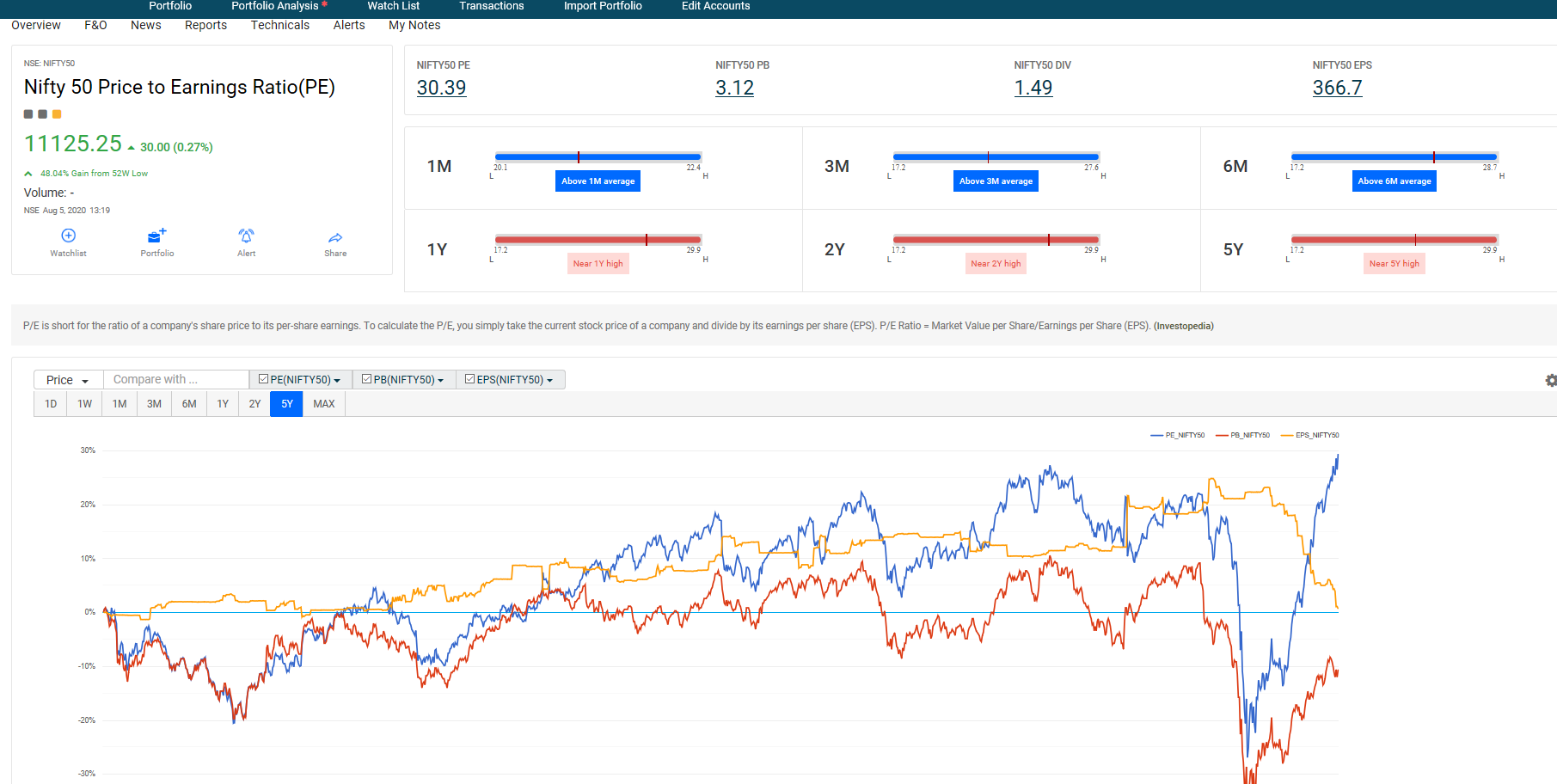

PE of nifty is risen above 30

The inflation is such a high that it is eating lazy money parked in the saving accounts or in the fixed deposits .

There is strong disconnect between market and the reality the earning are not growing and the most of the quality stocks became expensive

The FDI are taking out the money .

my notion is not to take any shortening of stocks but one must remained to be cautions and stay away from taking any tips or shallow dive while analysing the stocks ,

Sharing my index investment strategy performance

Disc: index investment is passive way of investing without any expense ratio and without any fund manger in place this may not suit to all .

I don’t follow Macros, so I don’t think I can answer the first question.

Regarding the second question, I don’t consider P/E as even a proxy for Value. It is too short-sighted.

In any case, I would say every investor should decide about being in cash / being invested based on whether or not he is able to understand the impact of the ongoing crisis on the fundamentals of the businesses he is tracking. I’m personally trying to understand this for many businesses I track/own. This is why I am in close to 65% in cash. I’m still invested for the remaining 35% because I either understand the impact or I think the impact will be limited. This position may change as and when I gather more information or I see a bargain.

Investing is a lot like poker. When we have a no-brainer hand, we should go all in. Conversely, when we are not so sure, we are better off just folding.

Bloomberg wrongly mentioned Chaman Lal setia moved in to ASM LIST

when I checked NSE website I found it is not chaman lal setia but LT Foods

source : list updated on 6th August 2020 https://www1.nseindia.com/invest/content/equities_surv_actions.htm

what may happen : it may lead to price decline in the scripe

one must check before taking any action as the scrip which moves in to ASM most of the time they plunges out

for more on ASM and how it works one can find the below resources : it is introduced from 1st June 2018 SEBI has Implemented ASM ( Additional surveillance Measures )

Disc : the files are shared for educational purpose . I am invested in Chaman Lal setia . this is not any buy sell or hold recommendation . I am not sebi approved analyst or broker

Portfolio change :

Additional portfolio by weight 3% in Bata india and 3% in Laurus Labs park additional money get from arrear rather investing in Bank FD Expectation in two years price rise 30%

Max time to play 2 year and minimum span 3 months

Max cap on investment : Not more than 5% of portfolio weight

**Exit criteria : a) 15% low from the purchase price or

*b) if price of entity rise than moving up the stop loss and realised at minimum of 15% if the market sharply dive .

Additional Buy : 10% after rise of 15% for first purchase and in second lot 10% of price rise 25% in short span i.e six months ) provided the growth in top line intact or in up trend more than 10%

Alternative strategy : Exit 50% if rise 100% within two years with if revenue or top line is not more than 10% annual growth

Trimming / Averaging / Allocation

Trimming positions in Chaman Lal Setia and in NGL Fine Chem and surplus proceeds are allocated to Bharat Rasayan and Swaraj Engine

How this this action help me

This reduce my excessive allocation in the both the businesses.

The rule of FIFO while calculating the Capital gain in terms of LT TAX is offset and almost the loss in former is offset by gain the later .

It reduces my average price of the scripes as do to initial year I bought the share price much higher due to lack of knowledge and without giving importance to various variable associated in the businesses dynamics .

Averaging can be establishing not only by additional buy but can also be achieved by offsetting the initial high price buys .

Future concerns :

The SEBI’s new rules are going to come in picture from 1st of September which in my opinion leads to low volume of transaction will takes place it was supposed to implement from 1st august but it is postponed till 1st sept 2020 .

so HDFC Bank , BSE as the major stack holders in CDSL also indirectly going to benefit with the CDSL will be lead gainer in terms of additional revenue from pledging of shares and revoking will going to take place . They have reduced the prices 91%

complete read ; https://www1.nseindia.com/corporate/CDSL_24082020145033_PressRelease.pdf

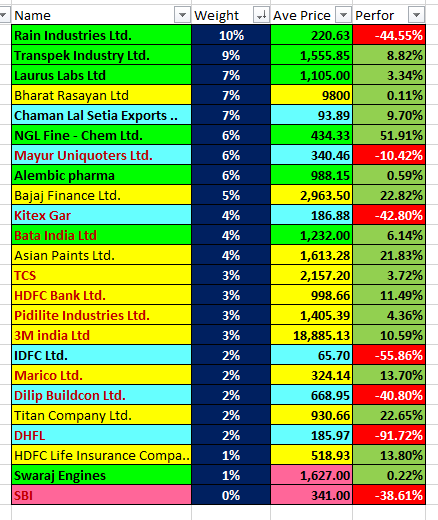

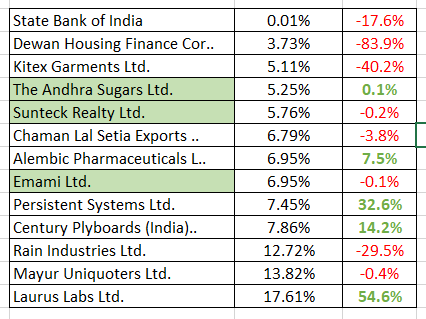

Current Portfolio

Averaging down scrip or adding positions to the front runners or is there any middle way ?

The averaging losers , Losers means not only the reduction in market cap but also comprises of the bad promoters / changing business dynamics / change in the political leaders or migrating in unrelated diversification with no or less exposure by the promoters / sharp practices by the business owners Strategy change:

This has been always a game plan to keep the winners and remove the losers. but sometime this is not suitable for all the situation if the scrip shoots up again. it happens most of the time when one sells the position the grass start growing on the other side. so what in my opinion one must take out the initial allocation capital from the running scrip so that they can run on their own and movement of the price does not affect your wealth and the retrieved capital one can allocate to the next probable company. this way one can create free capital. to allocate the funds in efficient matter

how one can do this

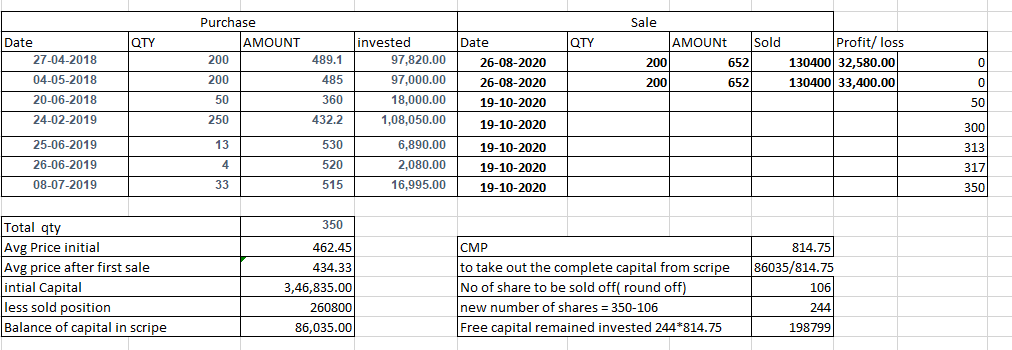

Portfolio change : sold completely the short time bets The company are best buys but I retrieve the capital to have more % of capital in case the market gives me chance. Made complete Exit from TITAN , 3M , Pidilite , Bata ,Marico , HDFC bank and Asian paints these are stable companies and are good wealth compounders . Partially sold NGL FINE chem and Laurus labs NGL fine Chem is now free running without any capital .

25% in cash WHY ? I am not an expert to time the market but the current rally of the stocks do not have any solid reason to back on find any fundamental reason the earnings are flat the capex stopped margins are eaten by receivables and in inventories , the growing market cause a cold pain in spine so I would take out the money from the market and sit a side and remain clam and wait on the side lines . I also have firm believe that even solid fundamental does not guarantee you solid return but a solid basis for compounding the wealth …

I was sitting on cash since last two months around 50% but it is hard as the KHUJALI continued … so today added more of century plywood and other three new scrapes…

Current Portfolio

New addition :

Andhra sugar :

Triggers why I choose the script : recent anti dumping duties on caustic soda and increasing blending of ethanol , Clean balance sheet lots of cash

Sunteck Reality :

Trigger : growing demand of real estate in Mumbai , Having huge pile of inventory in kitty however there are some delays in execution yet ethical promoter

3: Emami Ltd : can be turn around business betting on new generation Jockey Ms Priti A Sureka Haward alumini company started by two friends ( just like jai Verro) on the year of my Birth strong Ethical group

good point covered in the following report https://www.smifs.com/files/reports/637450891517948551_Emami%20Ltd%20-%20Initiating%20Coverage%20Report%20-%20SMIFS.pdf

As I observe experience and think to share

IMHO the market balloon has inflated and just need small trigger to prick the bubble . The Nifty PE ( which off course don’t represent whole market ) is all time high . Unemployment is at rate high . Huge money is offloaded to the equity market . One must keep some money aside to get the opportunities to enter in your equities of interest .

Second point I want to share the ground reality as I am constructing my home real-estate construction is on full swing thus leads to increased cost of labour and building materials e.g iron prises soar to more than 20% cement rises around 15% electrical fitting and fixtures ( conduits & wires have massive jump 30% . Bathroom fittings and tiles have also risen up … at the same time the Production utilisations are not risen to the same level the companies which has huge inventories will be getting benefited .

Third thing which I want to share is that I have observed huge rush in the banks the parking lots are getting full even you find difficult to park even your ACTIVA outside the bank . The financial banks are taking on each other and offering high interest rates on term savings and on saving accounts Bigger will become more bigger yet the service in some of the biggies in Private banks are messy and cluttered PSU Bank are cleaning their slates of NPA next few years they will recapture the market from private banks as the infrastructure and the dealing of the PSU banks has improved a lot.

Last mile logistics improve a lot thus improving two wheel sales Flipkart has improve over amazon ( I am customer of both ) .

Portfolio addition : taken 5% position in Himadari speciality . cash position reduce from 50% to 20% and want to increase the cash levels .

Disc: I may be wrong in my perception feel free to correct me . This is not any recommendation to buy sell or hold of any of the scrip hold previously or current . I am not any Sebi approved analyst

Wanted to know if u compared Andhra Sugar with EID Parry while taking this bet. Both have similar setup as in a sugar business plus other interests. Valuation-wise, in case of EID Parry - it is available at almost 50% discount to its holding value in Coromandel Int’l.

So precisely, what moved your needle towards Andhra Sugar and why not EID Parry?

Disclosure : - No investment. Analyzing EID Parry and Andhra Sugars