Hello yourraj bhai.many ace investors are investing in companies when price to sales is 0.20 or 0.25.your views bhai.

Hello yourraj bhai.in this example of buying 100 rs note at 25 rs or 30 rs how can one know that note is actually worth 100 rs (I am refering to company).is price to book value is helpful in knowing value approximately.

Sohan ji

Price to book value is a good matrix to follow .The book value has limitations we come to know only when the company is filling returns may be quarterly or annually .

You question is valid as how one can assertion the note is actually 100 Rs or not . The book value usually carry historical cost of the acquiring the asset less the depreciation. But the replacement cost in current time may be higher.so one need to find out the replacement cost of the existing assets . The value of some of the items which one consider in the balance sheet may be exergated . e.g the inventories may not be taken as 100% it may be taken 60 or 70 of 80 % of the value mentioned .

As Sir WB always says the price of equity of slave of Earning in long term so one must stick to the Basics business main Paisa hai ke nahi Ye business Paisa kaise Banata Hai and Kitni dear Iska High Margin Rahega .

There are three things which drive the price 1 Forgien Money Inflow 2 the Fundamental and 3rd is Sentiments . Out of these three Most important is Fundamental and the environmental forces under which the company is working it may be internal or external along with explicit attention to the eithcal considerations of the Mangment That shape the business and affect the human and company’s behaviour and judgment.

One need to read the fine prints in the notes how the company has arrived at the book value …

It is worth mentioning that many of the company’s competitive advantages that create moats are not typically are accounted for the Book Value and it can be inflated by accounting convention like goodwill .

I highly appreciated questions but book value alone should not gives the credit worthiness of an equity .

Regards

1 Like

Thank you youraj bhai.your views on low price to sales ratio companies. example 0.25,0.20 or even less

New addition in the Portfolio Marico Ltd … stock corrected today .it is a debt free , high roc high margins .i am betting for the management integrity .The entry is small

one can visit the thread Marico Limited (NSE: MARICO)

1 Like

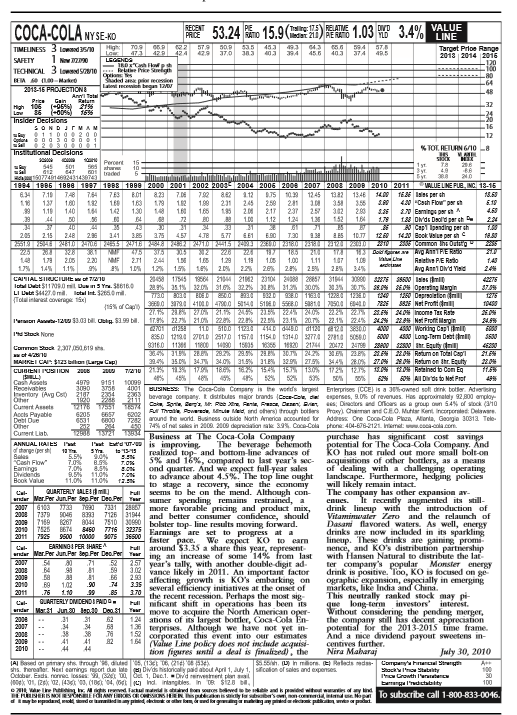

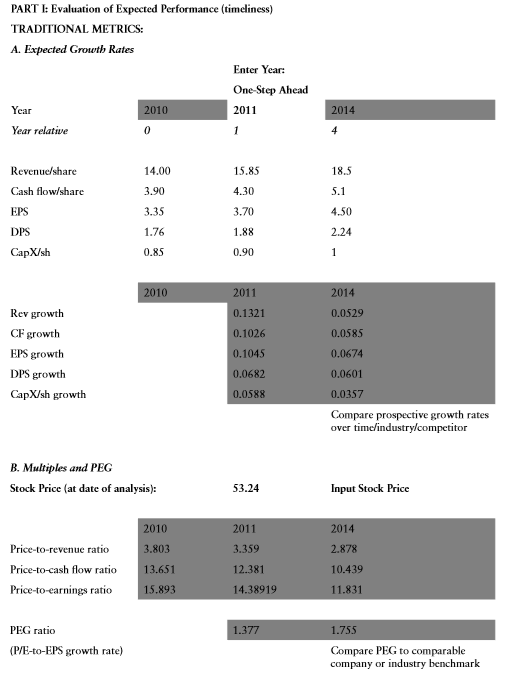

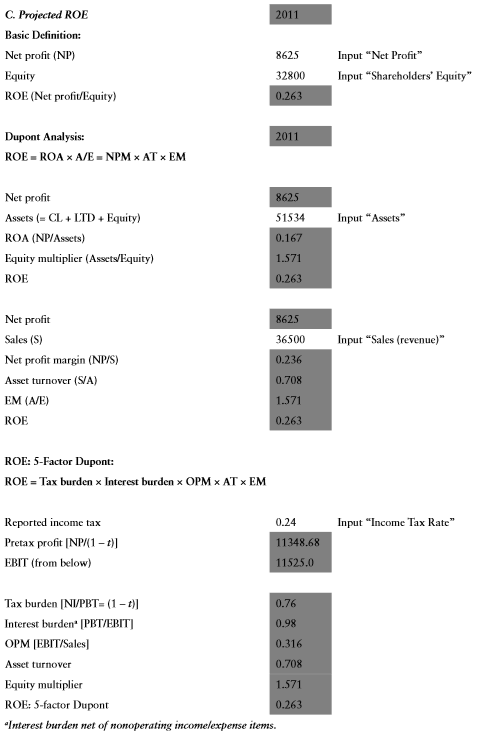

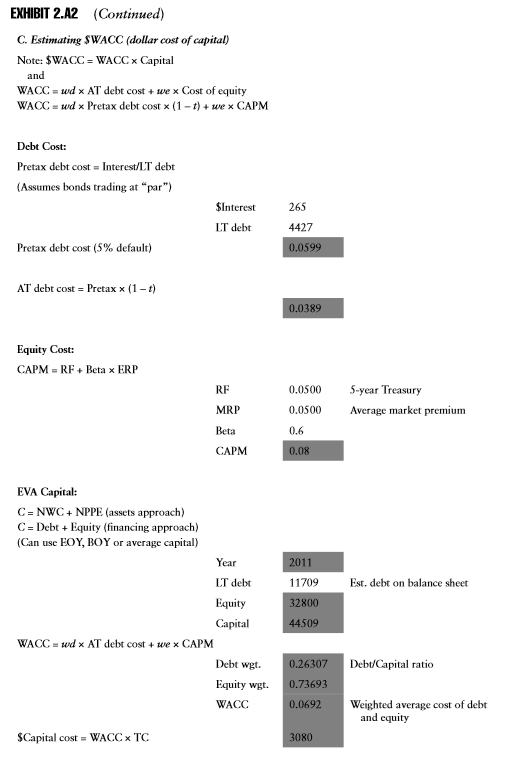

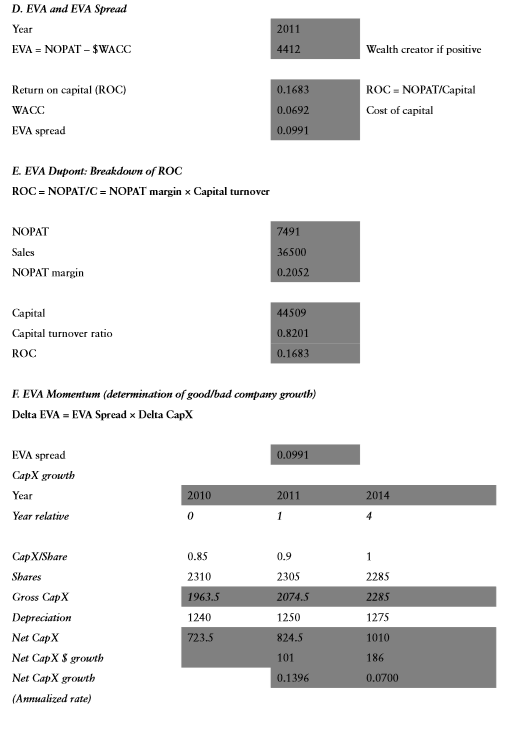

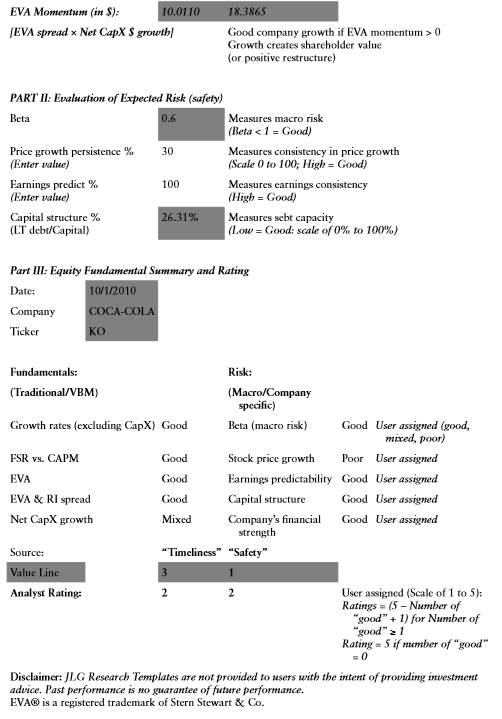

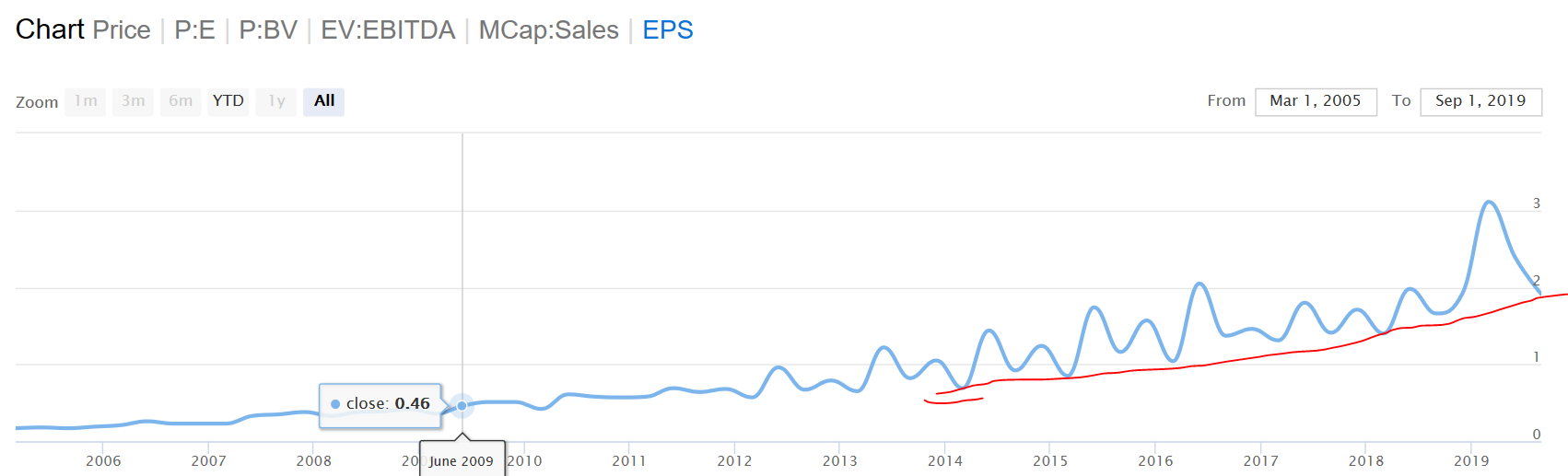

i come across a template and worth sharing

data source value line company coca cola

analysis

if administrators find the content is not suitable they can remove the content

Disc; this is not the ONLY model for equity Valuation .One should consult their advisors before investing in to any equity .The content is shared for education and learning purposes

Ref : Equity valuation and portfolio management book by Frank J. Fabbozi .Book is a good read

Regards

It was available cheaper than current price few months back. We think this is a a steep discount only because it fell 6% in a single day. I don’t know the name for this bias but sure seems like one.

2 Likes

thank you sir

why i entered now

it is mean line basis it is not very good and accurate but you can assured that you are not buying at extreme valuations . You are right It was available quite low a few days back but i missed due to lack of funds as i am fully invested

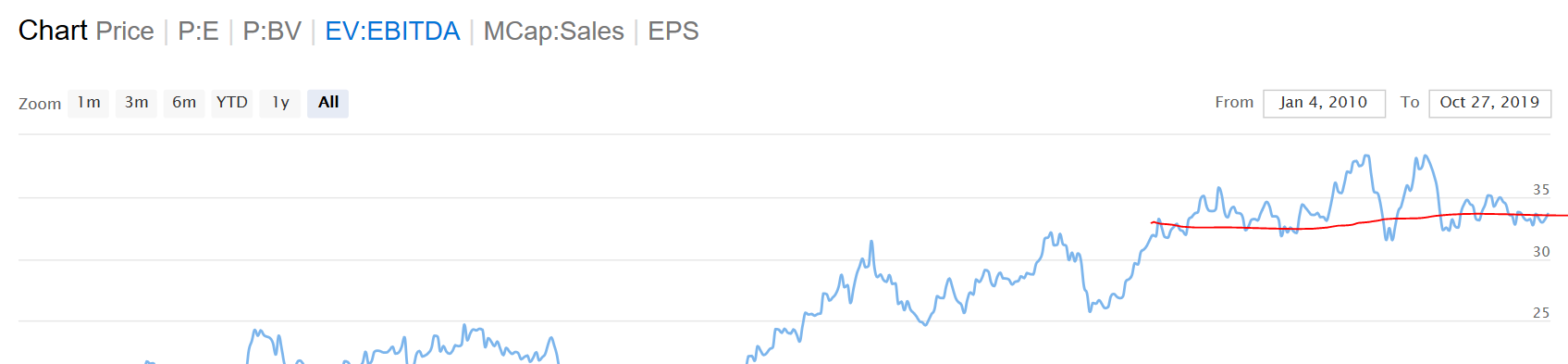

data Rate star EV-EBITDA

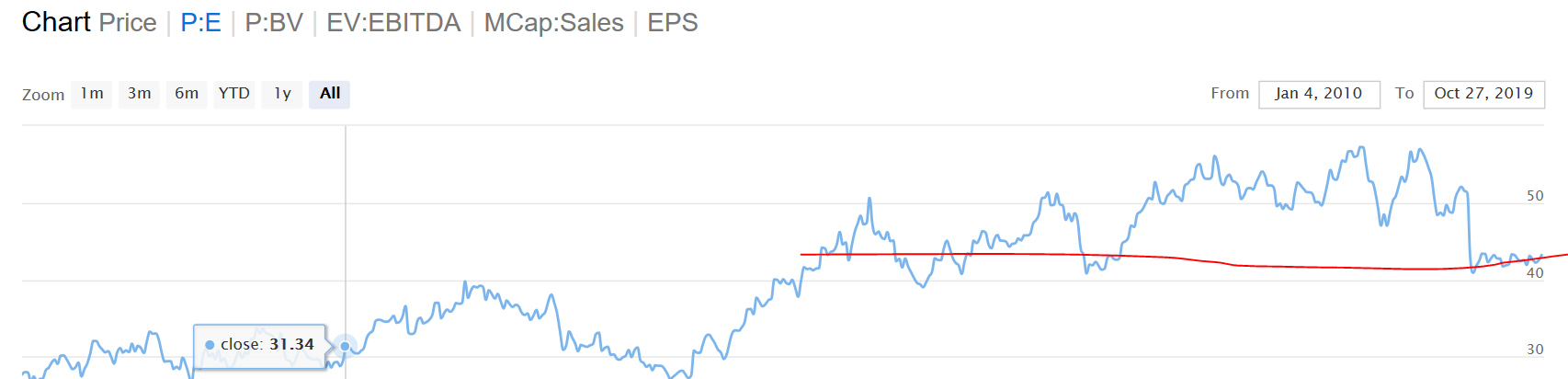

P.E expansion or contraction

Market cap to sales

EPS

i am not good a free hand drawing on computer

cash conversion cycle is negative it means they have advances in their hands

Altman score shows the financial stability

the best is THEy are HELPINg STARTUPS if interested you can watch videos at i love their scale up programs .https://www.youtube.com/channel/UCFB0Ayc4tKoAvkNBLVdK40g

for a good company for long term . It has good logistics / good brain behind operations / the Dhaka operation is working very good buy matured . The products are unique and now they are leaders in their segment .MNCS usually ignore the segments in which they are operating

- Product should be affordable and solve some problem

- it should be within the reach of customers ( good networking )

- the companies which help others to achieve their goals

It is OK to Miss some points but when you realised it is the company which you wont sell unless integrity issues comes on surface …

regards

2 Likes

Sir are you following company demergedfrom marico

Sohan ji could you please elaborate do you mentioning the Marico’s Bangladesh unit ?? I have found a good coverage on that You can see it below however it is very old

1 Like

Sir I was refering to marico kaya which is in health and beauty sector

Old investment wisdom Time tested Sharing Notes from the Book ARt Of investing : by a wall street broker

-

Changes and innovations are of continual occurrence.

-

Something good always comes to him who waits with money in his hand.

-

Thousands and thousands of dollars have been lost by the neglect of this simple precaution. “I didn’t read the paper”

-

When so many seductive baits are offered; so many nets and traps, contrived and constructed by clever brains and cunning fingers, are spread for the capture of those having money, is it surprising that the careless and credulous are victimized, and even that the sagacious and prudent should sometimes be taken in? Nevertheless, for the losses they have sustained, investors, as a rule, have themselves chiefly to blame. The mistake made, in nine cases out of ten, has been the purchase of cheap securities. The hope of realizing a little more than ordinary interest, by buying paper at a discount, has proved to be the rock on which unnumbered capitalists have split.

-

By what rule or rules is the investor to govern himself? No formula can guarantee him absolute safety. One thing, however, he can properly count upon, viz., that he must expect to pay a fair price for a good security—one that will return him no more than a moderate interest on his money. If he wants to speculate, and is willing to take risks, that is another thing.

-

The investor may pay too dearly for safety. There are securities which, compared with others that are to be had, sell at prices much above their real value. The reason is that everybody knows them to be good, and investors who don’t want to take the trouble to investigate, or are afraid to trust both their own judgments and the counsels of their friends, are willing to pay extra prices for them. But there are plenty of others that may be had at lower figures, which are just as good. There is no reason in the world why the investor should not get at par all the paper he wants that will yield him six per cent, interest, and be as safe as any property can be under human supervision.

-

Securities, in the long run, must stand upon their merits, and purchasers have merely to follow business principles as taught by the canons of common sense.

-

In seeking investments, and especially long-time investments, there are several things to be taken into account. There is not only the question of the kind of security to purchase, but the question of the time to purchase. There are opportunities to be looked for as well as pitfalls to be shunned. It is during periods and seasons of depression, when securities are forced upon the market, often to be sacrificed—and they are certain to come if waited for long enough —that the shrewd investor finds his richest harvest. That, however, can not be said of the ordinary investor. He usually buys when securities are up and confidence is unimpaired, and becoming frightened as market values go down sells when they are at the bottom, and holds his money to reinvest in something else no better, and probably not as good, when the tide has turned.

-

As a rule, the best time to invest is when others are unloading. In money matters it is never safe to follow " the crowd." Nor is it safe (which, however, is little more than the expression of the same idea in another form) to purchase a security when it is on the " boom." A peculiarity of our money market, conservative as it is popularly supposed to be, is that it is constantly changing its favorites. Its offerings come in waves.

-

One thing the investor would do well never to forget, viz., that there is always plenty of good securities in the market. No one with money need ever fear that others will get all the solid investments, and, in the apprehension that there will not be enough of that sort to go round, put up with an inferior article. Don’t let him choose what is not altogether satisfactory, under the impression that nothing else as good or better will offer. If he does so, sooner or later he will regret it. Something good always comes to him who waits with money in his hand.

regards

2 Likes

Sohan ji please don’t call me Sir , I had seen to kaya but not closely following it

Regards

1 Like

How did you calculate profit as 16% and what is the exit price you assumed? What happens if the shares fall to Rs100 from 116 for example?

My guess - recency bias

2 Likes

My inputs

i) Isn’t it averaging at lower price, which is NOT recommended by majority of long term investors

ii) How many times do you recommend to average it down (using same formula… I understand n1 & p1 will get appended with each piece of investment)

iii) What is the protection (or exit policy), if price keeps on declining

iv) What is the re-entry level … for n2 & p2… do you recommend at drop of certain percentage points or time based

v) What is the exit policy, if price moves above p2 & p1?

1 Like

Sir appreciated you reply . I want to add that This is for complete Exit from Scrip Where you find your basic hypothesis went wrong due to wrong Perceptions or taking wrong variables while making your investment rationale and it is Fatal to remain in the stock . On that case you don’t want to come back to scrip or purchase again .It is well suited to Cockroachy Stocks but you realise late .Best suited to the company where the fraud happened or some management is found non ethical…Some may stay in those as this is individual call but my perception is get rid of the stock as soon you find the reason.

Averaging can be good or bad one should not follow rules blindly why in my opinion one should strongly avoid the averaging in bear or recessions time where the fundamentals do not support the price .But can opt for averaging where one have conviction and the fundamentals are good and on top of that the market is going to from mean position to the positive side …

Regarding last if price move above your purchase than one should use either time based target or risk return ratio . And it should be continuous moving upward with moving stop loss …

Another good model of exiting is MEA i.e Mean extreme average. In which one take last 100 day or three months extreme up and bottom positions and set realistic target as per ones risk appetite to exit … very rarely discussed and one of the oldest methods…

Please correct me if my opinion is not match with you

Regards

2 Likes

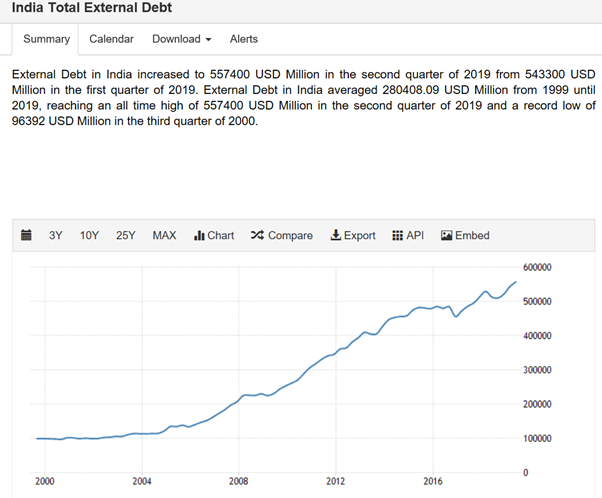

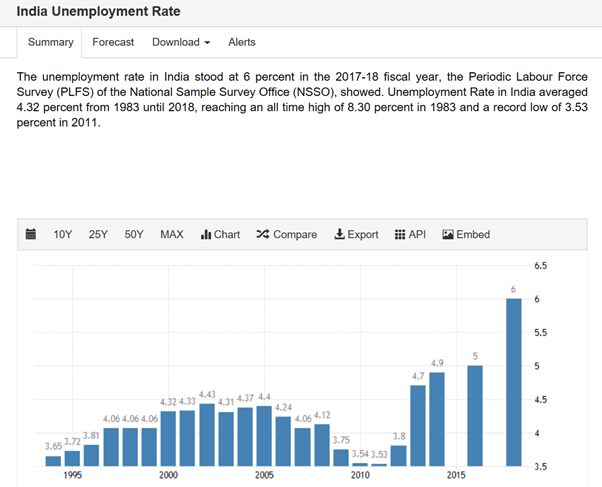

I had collected some data that look disturbing though it wont effect in very short terms but the bubble is forming

Households Debt in India increased to 11.70 percent of GDP in the first quarter of 2019 from 11.30 percent of GDP in the fourth quarter of 2018. Households Debt To GDP in India averaged 9.83 percent of GDP from 2007 until 2019, reaching an all time high of 11.70 percent of GDP in the first quarter of 2019 and a record low of 8.70 percent of GDP in the third quarter of 2012.

The economy is shrinking at alarming rate unemployment is rising debt is rising … I am my be total wrong in my perception but this the inference I got from the above data

consumer spending is increased … if it is from cash than it will e alright but if the spending is from the credit than one must be cautious because we are borrowing from future earning … we are owe the price to the service or goods provide which we must discharge otherwise there will be decrease in the future earning thus lower the future earning of the individual … it can give rise to increase in the interest rates … and the credit disbursement will be tight … in light of that economy may be in bad cycle … be alert and stay cautious about the choices one make while investing … we have also witness at large there is contraction of earnings there are some exceptions no doubt …

Debt is asset for the lender and liability for the borrower . he must discharge his due to honor his promise to pay … but recent defaults by ILFS , DHFL p&m bank … in my locality local cooperative HINDU BANK ( pathankot ) depositors are not able to withdraw their own money … so the situation is rising of and may be headed towards bad cycle …

be invested but with cautious and with intelligence

if a credit is use for consumption that is bad but if used for increasing productivity it will be boon provided the borrower return the lender within speculated time frame .

regards

5 Likes

Peter Lynch in daily life …- Stock Selection …

I am sharing my experience I was using several creams for some Eczema and doctor recommend me a cream which has substantially help me since then i had recommend that to some of my friends . it help me in fungal infection i am not a doctor . but that suited to my skin .Most of the feedback was very good . (Disc: don’t use the medicine without prospection of doctors ) when I found the cream I was using on and off . the manufacturer is Abbott … I had started may be 6 7 years ago … but not curious about the company since I was not investing then and I found it is product of ABBOTT , I am talking of LOBATE -GM … when out of curiosity I checked on screener and than I found the VP thread is existed since 2015 I say OMG … what a holi miss I have done … lesson learned apke ass pass bahut kuch hai grass is growing every where you need to eye for the growth and sound companies .I had find in same manner a company called FDC limited ,

Disc : i am not invested in both the companies but certainly interested Abbott has grown in price and valuation so much I am waiting to come to my range of valuations

2 Likes

Management analysis security:

It is vital to check the remuneration to director promoters over the past several years especially the change in remuneration wrt to change in profits/revenues it is a good matric

Check % increase remuneration of PAT and check the % increases in the PAT during that year.

It is utmost importance how company allot preference shares to the promoters because the promoters have a privileged view of the business and business environment in which he company is operating i.e trend or market , the forward locking contract of raw materials, overall global trends in the market , the can know beforehand than the minority shareholders about the price fluctuation ( which is a common and global phenomena ) in the raw material or the end products over the minority shareholders.

What to look for: in the years where the company is making loss what is the cumulative interest on the preferred equity which will be paid in the year where the company make the profit

Observations: the sequence of events surrounding the modification of terms and conditions of the preference shares and their subsequent redemption at a significant premium does cast doubts on the shareholder friendliness of the management.

Annual report Reading TIP :

One should not run through one must read section of the annual report which carries Market and Competition risks.

Capital Allocation discovery TIP

Sweat equity is really sweet? A good management can make a huge difference to the fortunes of the business over the long-term. And most of the professional investors want that the management should be Competent and there is no harm if they paid themselves a sweat equity as a reward it may be through rise in salaries (monetary) or via sweat equity (non-monetary) benefits. Check the person to whom company is providing benefits that

- How long they are associated with the company?

- What has they done in order boost the revenue of the company?

- What competency they are bringing to the organisation?

Unusual Matrix :

“Cash is real; profit is an opinion” financial saying

- Check historical sales profits dividend paid 10 years

- Look for the cash flow from operation (CFO) and the Free Cash Flow (FCF) of the business .

- Look at the cash spent by company in purchase of fixed assets After eliminating the numbers form any group or sister entity.

- Check if any cash required for CAPEX does it come from additional borrowings including borrowing from sister concern or group entity

- Buy back is good only and only IF it comes from cash within that cash from the RESERVED POOL IS USED if the buyback is coming from the borrowed funds than that will be a BOG RED FLAG. It should not be from the money in the form additional borrowings from banks UNLESS the absolute and real interest rates are just a few point above zero.

- Section 68(2)(d) of Companies Act 2013 and Regulation 4(ii) of SEBI (Buyback of Securities) Regulations 2018 says that, “A company is prohibited from buying-back its shares if the debt/equity ratio of the company exceeds 2. “

regards

1 Like