i want to add in @SlownSteady though well covered by him. It is the unemotional attachment with the scripe as soon as your stop loss arises just sell it .There are so many stocks are available . It hurt me when i copdied someone else idea ,because i dont’ know at what price they have entered as @hitesh2710 ji mentioned understanding of Key variables exist at the time of entery and how it will change with time frame .The company is expanding it’s expertise somtime back @basumallick has mentioned keep an eye that the company is expanding the ditch which keep them apart from their key competitors and maintain their competitiveness and at what stage is the company NOW … What are the sources of past and current growth . .(NOT exact words this is what i understand about he MOAT ) and how long will it going to last .

Never loss the capital is achievable but as of now i haven’t achieve it . It depends in mow much depth you have studied the dynamics of the sector and How your company behave under the FIVE Porter Forces …

Till now i only know that you an only control the PRICE your are paying for any stock .are you paying for Past or current growth at premium or at discount . when i look my journey backwoods i found i have made purchases near the Top. I was too much obsessed with legend’s stories That i think it is easy to make money in Market . This is the biggest Mistakes i have done . Nothing comes easy .

I thought buying a book on stock market it is waste of money but ilearn it very hard way so i start investing in ME first before more allocation of funds to the Stocks . I am promptly booking the profit after 30% or 50% to me the least book profit should be double the Current Fixed deposit rate + 5% to cover the mislleneouse expenses . if Bank offer you 6.6% than my profit booking 13.2+5% i.e 18.2% in my case i make it 30% WHY this is due to the reason that i have to pay short term gain tax which is roughly15% of your earning ( MAY be i am greedy ![]() ) and keep moving the stop loss if initially you have 15% of stop loss and your sock moves to 10% up than i may be exiting at 5% if my stock moves to 25% than i will move my stop loss to 10% as soon stock falls near to 10% i will exit .

) and keep moving the stop loss if initially you have 15% of stop loss and your sock moves to 10% up than i may be exiting at 5% if my stock moves to 25% than i will move my stop loss to 10% as soon stock falls near to 10% i will exit .

i thanks to Vp forum menbers and seniors @hitesh2710 @phreakv6 @Mehnazfatima @Agarwala @Capsule91 @devaki.tripathy @PE_Ratio That i learn Technical analysis which i thought that is was of time .But these are excellent tools which one can decide entry and exit time along with the improving or bad fundaments . Golden cross over is very good .study or MCAD .RSI ,ADx along with Boliger Bands

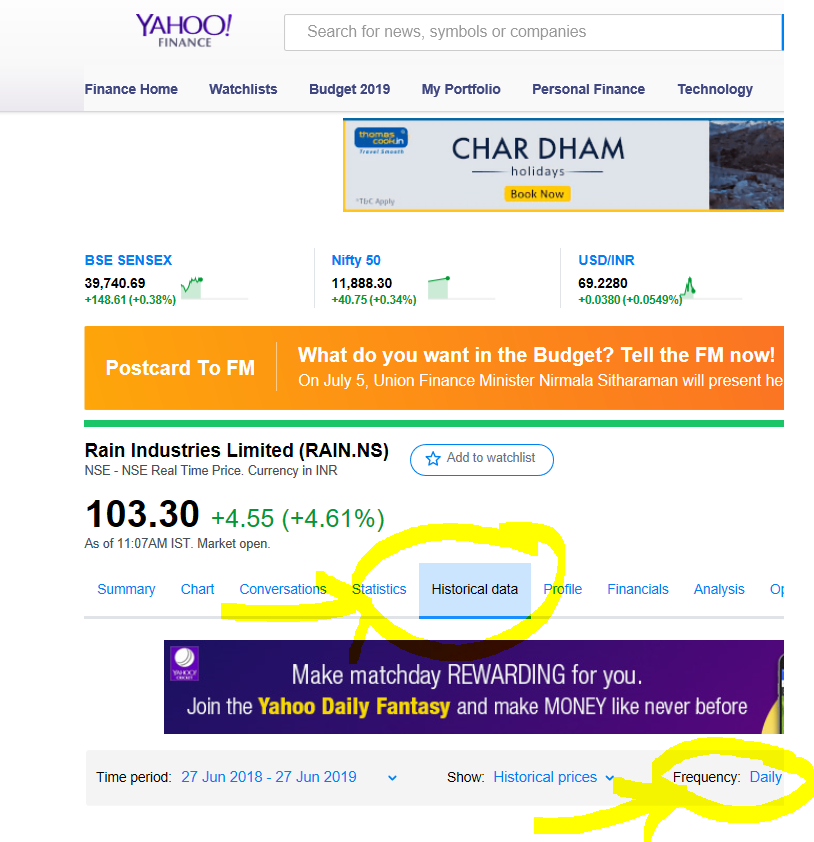

( VOLUME study is must all with these which i check in the yahoo finance )

coming back to Filimy QUETION DHANDO KA GNDOOO CHOKROO… Rule no 1 NEVER LOOSE MONEY … it depends on YOU >>>>>> HOW much safety of margin you have taken while making your purchase … NOTIONAL LOSS MAY BE sometime became REAL if YOU decide … YOU and YOUR behaviour is very important( almost 90% )

Thanks for visiting the thread i am learning and welcome the views