700 news bed capacity will definately be the growth driver in revenue, but PAT will grow with slower pace. I don’t see a big issue in cash receivables, it will come in account sooner or later.

4 Likes

Yatharth Hospitals -

Q4 and FY 25 results and Concall highlights -

Update on acquisitions -

- Acquired 60 pc stake in a 400 bedded hospital in Faridabad. Built in 2 acres, Muti speciality, located in Sec 20. Operations to commence in Q1 FY 26

- Acquired 300 bedded hospital in Model Town ( 100 pc stake ), New Delhi. Located in a high per capita income colony, has a large catchment of residential and institutional clients. Operations to commence in Q1 FY 26

Once the new Faridabad and Model Town hospital goes live ( in Q1 Next FY ), Yatharth will become the 3rd largest hospital chain in NCR after Appolo and Fortis. At no 4,5 shall be Medanta, Paras Health. Their total bed capacity will reach 2300 beds. Company aims to take this upto 3000 beds by end of FY 28 - via organic + inorganic routes

Highlights from Q1 + Q2 + Q3 concalls -

IT raids conducted on the company in 2023 and the IT department had frozen certain amount of money pending resolution of the case. However, company is allowed to use that money after obtaining permissions from the IT department. The company has been doing so and is being allowed to do so in recent past. Company does not fore see any significant losses / impairment from these events and is confident of a favourable resolution

A new hospital generally takes about 18 - 24 months to break even. Expect the same from the two new Faridabad and one new Model Town hospital

As the new hospitals on online in Q1 next FY, expect further increase in Employees cost + Depreciation etc. However, at the same time - benefits from the Greater Faridabad hospital should start to flow in by that time

Qtly Depreciation rate for next FY should be around 20 cr wef next FY

In next 2 yrs, company expects to bring down the Govt business to less than 25 pc of the total business vs 35 pc currently. This should also help the company to accelerate their ARPOB growth

The new Faridabad and New Delhi hospital are expected to have ARPOBs > 35k

Q4 outcomes -

Revenues - 231 vs 178 cr, up 30 pc

EBITDA - 57 vs 47 cr, up 23 pc ( margins @ 24.6 vs 26.2 pc - due increased employee, material and other expenses on account of operationalisation of Greater Faridabad hospital )

PAT - 39 vs 38 cr ( due accelerated depreciation and higher tax rates in Q4 )

FY 25 outcomes -

Revenues - 880 vs 670 cr, up 31 pc

EBITDA - 220 vs 179 cr, up 22 pc ( margins @ 25 vs 26.8 pc )

PAT - 130 vs 115 cr, up 14 pc

Q4 occupancy @ 61 vs 57 pc YoY

FY 25 occupancy @ 61 vs 54 pc YoY

Q4 ARPOB @ Rs 31.4k vs 29.2k

FY 25 ARPOB @ Rs 30.8 vs 38.5k

FY 25 - hospital wise breakdown of revenues -

Noida extension - 323 vs 214 cr

Greater Noida - 271 vs 234 cr

Noida - 181 vs 185 cr

Jhansi - 60 vs 36 cr

Greater Faridabad - 44 cr vs NIL ( has operated for 10 months in FY 25 )

Both Model Town and Faridabad hospitals should go live by end of Jun 25

Greater Faridabad hospital’s share of revenues from Govt schemes @ 20 pc. Similar trends should continue in the new Model Town and Faridabad hospitals - aiding ARPOB and margins

IP volumes up 41 pc YoY, Out patients volumes up 30 pc YoY in Q4

Therapy wise breakdown of company’s revenues -

Internal medicine - 19 vs 28 pc

Neurosciences - 11 vs 10 pc

Nephro + Urology - 11 vs 10 pc

Oncology - 10 vs 4 pc

Cardiology - 10 vs 10 pc

Gen Surgery - 8 vs 7 pc

Others - 31 vs 31 pc

Adjusted for the EBITDA losses in Greater Faridabad facility ( that’s natural since its a new facility ) - EBITDA margins in Q4 would have been 27 pc

Cash on books @ 530 cr - bolstered by recent QIP ( in Q3 )

Both new facilities @ Delhi and Faridabad should report EBITDA losses for first 12-15 months. The greater Faridabad hospital ( opened in June 24 ) has started to break even in Apr 25. Should report positive EBITDA in Q1 FY 26

Company’s cash business is @ 35 pc, Govt business @ 37 pc, Insurance business @ 28 pc

Company’s longer working capital cycle vs peers is due to higher percentage of Govt business vs peers

Effective tax rate for near future for the company should be 24 pc

ARPOB @ Jhansi hospital for FY 25 @ Rs 13.2k. Aiming for an ARPOB of Rs 15k from Jhansi

Capex lined up for FY 26, 27 @ Rs 300 cr each ( for the existing hospitals ). This includes ongoing capex in Model Town, Faridabad, brownfield expansion @ Noida Extension and Greater Noida hospitals ( adding 250 and 200 rooms to these 2 facilities ). Any inorganic acquisition shall be over and above this

Should be able to grow their ARPOB by > 10 pc in FY 26 ( organically + the upcoming hospitals are in high income areas )

Despite the incremental costs ( due operationalisation of 2 new hospitals ), company expects the EBITDA margins for full FY 26 to be around 24 pc ( because of ramp up in Noida and greater Faridabad facilities )

In general, breakeven ( @ EBITDA level ) occupancies for a new hospital is around 30-35 pc

ARPOB in case of international patients is generally 1.3 X of domestic cash business’s ARPOB

All of company’s hospitals are owned ( helps their EBITDA margins )

All of company’s future growth shall only be focussed on North India ( in areas where they have descent brand equity )

There is a descent scope for ramp in company’s Noida assets. Operational leverage gains in Noida + Jhansi + Greater Faridabad should help them offset the expanses involved in operationalising the 2 new hospitals

Should be able to grow topline @ > 20 pc for next 2-3 yrs

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation, posted for educational purposes only

10 Likes

Seems like a very conservative guidance. Both should break even within 9 months. Both of them are located in prime localities. Occupancy will climb in a jiffy if logistics are well managed.

3 Likes

Why their Noida facility is degrowing?

Usually in hospital business, once brand & trust is built there is no reason to degrow (Unlike hotel business where after few years property gets old & they can’t charge high or need to go for renovation.)

1 Like

I think, that’s because of some diversion of patients away from Noida to Noida Extension and Greater Noida facilities. Additionally, they r increasingly limiting the intake of Govt funded patients

1 Like

There is court case or something in news about illlegal transplant by the doctor of hospital in Indraprasth medical in delhi, is it true? What is consequences?

That issue is almost dead and buried ( IMHO )

1 Like

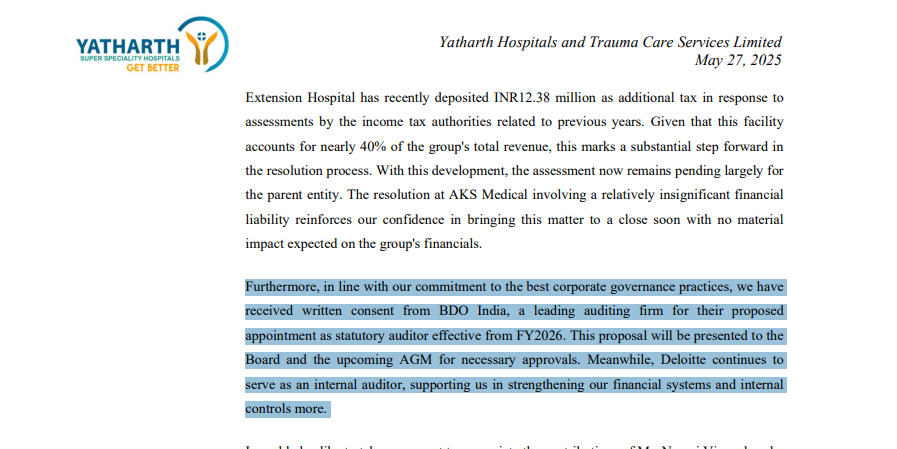

They mentioned changed in auditor from Deloitte to BDO, is this scheduled rotation or out of turn. It sounds out of turn because they did not mention it as scheduled rotation.

I think needs cautious look given the tax case and then auditor change.

1 Like

Won’t put too much thought into this.. Deloitte probably took a call that internal audit gives them more moolah and is more value add than statutory audit.

I think needs cautious look given the tax case and then auditor change.

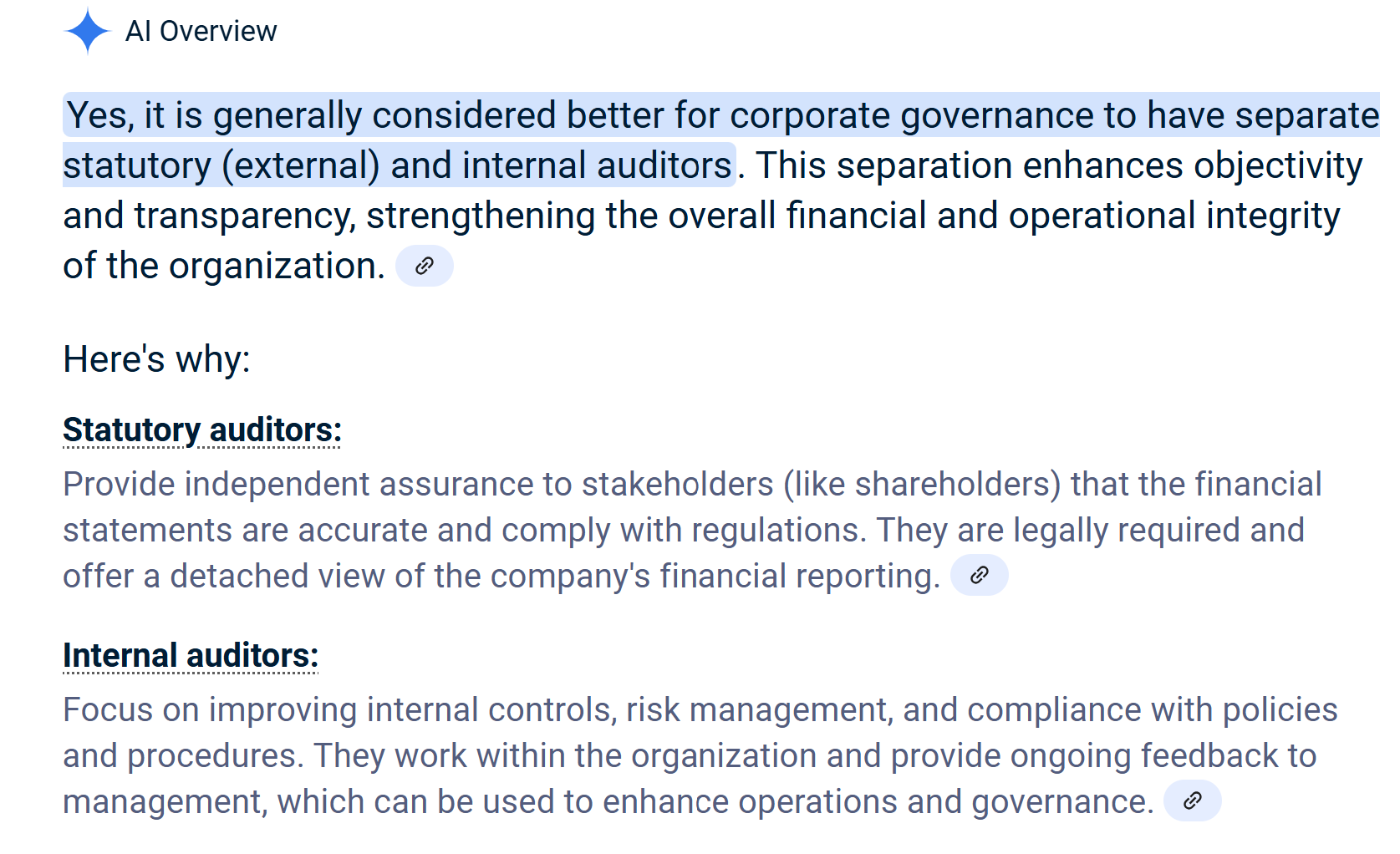

Isn’t it better to have different statutory and internal auditor .

2 Likes

My bad, I interpreted it as Deloitte was existing statutory auditor which is now going away.

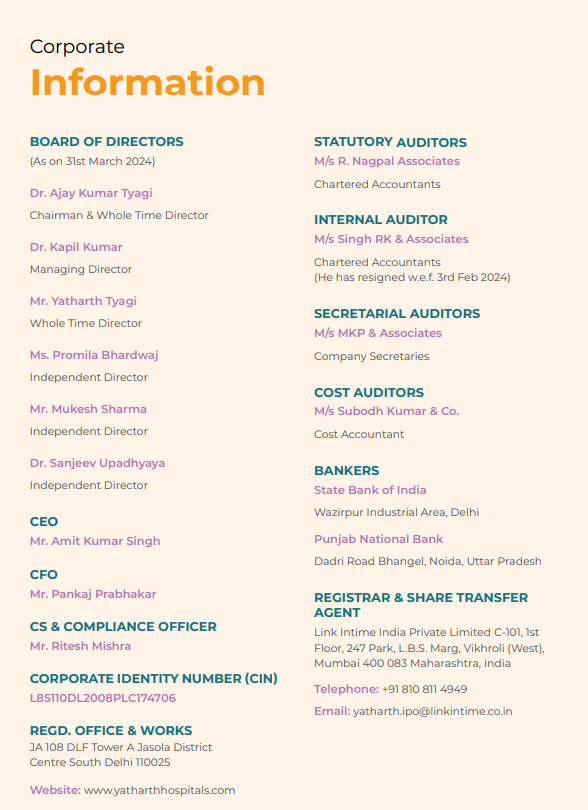

Current statutory auditor is Nagpal associates and now they are changing to BDO. Also internal auditor resigned, and Deloitte is now the internal auditor.

Not sure about the reasons, but both look like upgrade so does not look like concern.

6 Likes

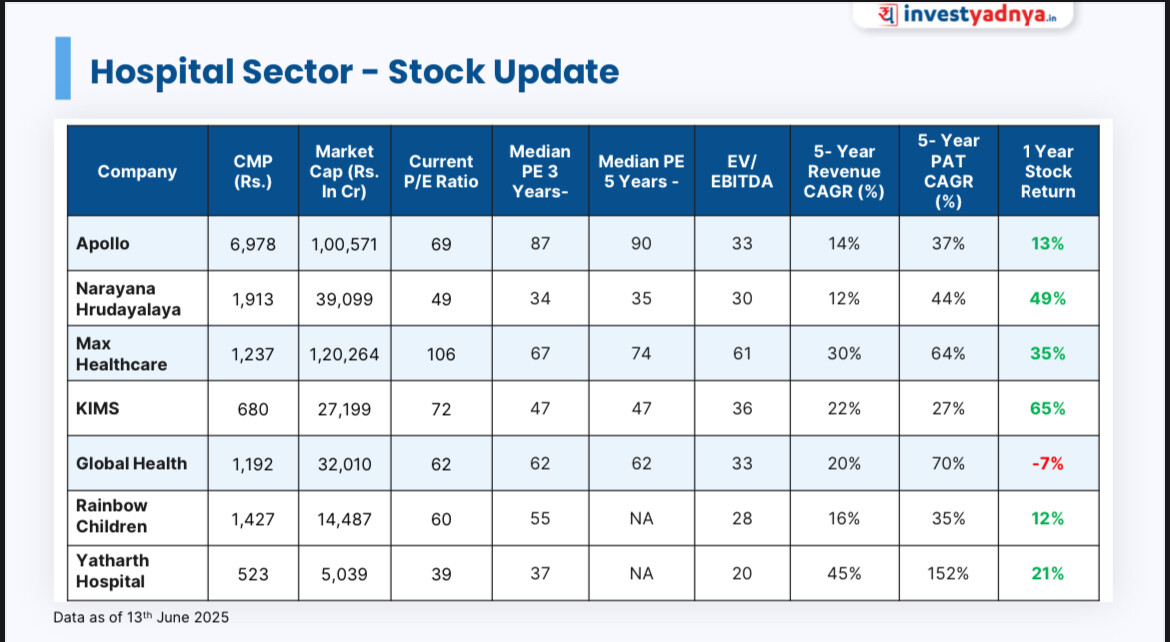

yatharth has the lowest ev/ebitda among all hospital and highest 5 year revenue and pat cagr. new faridabad contributed 9% of q4 revenue within 10 months of operations. revenue mix is improving with lower dependancy on gov schemes (only 20% in new hospitals)

source: investyadnya

disc: invested

6 Likes

Everything is looking good in the Fundamental aspect, but I have one serious question on their corporate governance because after the tax raid, they were mute and not much info on the tax raid is available, this might be a worry because I remember the same thing happened with GR infra, once the issue with corporate governance exist then no point in investing how much attractive the stock many be.

3 Likes

Few positive developments:

-

The Ramraja Hospital land dispute has been conclusively resolved as of June 30, 2025, with the Commissionerate of Sagar Sambhag confirming the Company’s rightful claim to the land. Link

-

Appointed Mr. Ashutosh Kumar Jha as Group Chief – Strategy, Mergers & Acquisitions (M&A), and Investor Relations, leveraging his healthcare experience to drive the hospital’s growth and stakeholder engagement. Link

6 Likes

Delhi Model Town hospital got inaugurated today

5 Likes

Good results.

Multiple levers for next 2-3 years:

- 300 bed Delhi hospital started in Jul’25, should start contributing in Q2 (ARPOB > 38,000, compared to current average of 32,400 on consol basis)

- 400 bed Faridabad hospital will get started by the Aug-end, should start contributing from Q3 (ARPOB for this too will be > 38,000)

- Brownfield expansion at greater noida hospital - 200 beds - will become operational in 2 years

- Brownfield expansion at noida extension hospital - 250 beds - will become operational in 2 years

- Mgmt has guided that they will complete 300-bed acquisition this FY

- Mgmt plan to add close to 1200 beds in 3 years, hence excl. brown field & current year M&A plan, they might 450 beds organically / M&A in 2-3 years

- Shifting to super specialty services which could contribute positively to top-line & bottom line

- Maturing of existing hospital would drive higher occupanc

- Appointment of BDO & Deloitte for statutory & internal audit will add to investor confidence in numbers

- IT investigation to get closed by the end of FY26

- Increase in Medical tourism, opening of Jewar airport, etc would be additional lever

- New hospital will have less reliance on government patients, hence bring down DSO

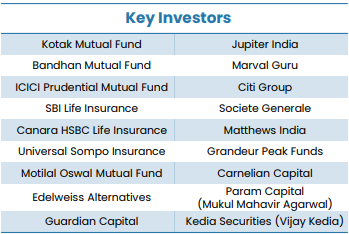

Latest investor presentation shows that Mr Vijay Kedia also have acquired some stake in company

12 Likes

The receivable days of Yatharth are at 123 days for Q1FY26, and it has been relatively higher as compared to other hospitals (roughly hovering over 100 days). This is happening because of the payor mix, which has around 35%+ coming from the government schemes, and those payments are not coming on time. The EBITDA/CFO conversion for March 2025 was at 68% (relatively lower compared to other listed hospitals), hence the low valuations. The key thing to track is the payor mix for government (management guided for 25% in 2/3 years), which will help decrease the receivable days and increase the EBITDA/cfo conversion rate. Once the street starts noticing these improvements, it will re-rate this company. i have been invested in Yatharth since 2023, and added some during the last big fall. Sitting on decent gains, will hold it and wait for the H1 balance sheet figures to see what the receivable and cfo numbers look like. For now, 700 beds are coming online. We should track the ARPOB and sales growth, and the EBITDA margin movement

8 Likes

Yatharth Hospitals – Q1 FY26 Highlights & Management Outlook

Strong Q1 Performance

Revenue grew 22% YoY to ₹257.8 crore; net profit up 38% YoY to ₹42.0 crore.

EBITDA of ₹64.5 crore with 25% margin, marking 13 consecutive quarters of growth.

Greater Faridabad hospital turned profitable within 12 months of operations; contributed ₹23.4 crore (~9% of total revenue).

ARPOB, ALOS & Occupancy

Group ARPOB at ₹32,395 (+6% YoY).

Noida Extension ₹39,830 (~70% from super-speciality services)

Greater Noida ₹38,377 (+9% YoY)

Greater Faridabad ₹31,393

Jhansi ₹13,500–₹15,000 range

New Delhi & New Faridabad projected ~₹38,000 (from Q3 FY26 impact)

ALOS (Average Length of Stay) deliberately reduced to increase patient turnover.

Occupancy in Q1 FY26: Noida 86%, Greater Noida ~67%, Noida Extension ~61%, Jhansi ~60%.

New hospitals to target 30–35% occupancy in first year.

Growth Drivers

Capacity Expansion: Current ~2,300 beds; +700 beds coming from new 400-bed Faridabad and 300-bed Delhi hospitals (both with robotic surgery and advanced diagnostics).

Oncology now 10% of group revenue (+50% YoY) and expected to rise to 15% in 2–3 years as new radiation oncology units go live.

Medical Value Travel initiatives in Africa, Central Asia, and Middle East to push international patient share towards ~10% of revenue in 2–3 years.

Management Guidance & Outlook

Margins: FY26 EBITDA margin expected around 24% ±1%, similar to Q4 FY25, despite new hospital drag. New Delhi & Faridabad will see initial ramp-up costs, but Greater Faridabad’s profitability offsets part of the impact.

Revenue Growth: Guidance maintained at ~30% CAGR for FY26 and beyond, supported by new capacities, speciality mix improvement, and international business.

ARPOB Growth: Management expects 8–10% annual ARPOB growth for FY26–FY27, driven by higher super-speciality contribution and improved payer mix.

Breakeven Timeline: New Delhi & Faridabad expected to turn profitable in ~15 months, in line with Greater Faridabad’s ramp-up.

Occupancy Targets: Mature large hospitals to reach 75–80% peak occupancy; Jhansi target 70–75%.

Long-Term Expansion:

Brownfield expansions at Greater Noida (+200 beds) and Noida Extension (+250 beds) to complete in ~2 years.

Exploring Greenfield/stressed asset opportunities in Ghaziabad, Gurgaon, and other large cities.

₹1,400–₹1,500 crore CAPEX over 3 years to add ~1,200 beds (Brownfield at ₹0.6–0.7 crore/bed; Greenfield at ~₹1 crore/bed incl. land).

3,000-bed target by FY28 likely to be achieved earlier, with scope for further scale-up.

I strongly suggest all members go through the full Q1 FY26 concall transcript — the management has shared a lot of detailed operational insights that go beyond the numbers, especially around occupancy strategy, speciality mix, and expansion planning.

7ab8d9eb-1bd2-4453-908e-09f54d9ab41f.pdf (1000.6 KB)

8 Likes