I am taking the liberty to add the extracted text from your handwritten notes. This will be easier to read for the community members. I can delete the post if you have any objection.

The Winning Methodology in Hospitals:

a) Capital allocation in such geographies where the ARPOBs can rise much more than healthcare inflation.

b) Matured hospital usually can’t drive your ARPOB (can only move in line with inflation).

c) Rising occupancy is must

- [Rev = ARPOB x no. of beds x occupancy x 365/90 days]

- If ARPOB and occupancy both are rising, then it gives a huge boost to revenue.

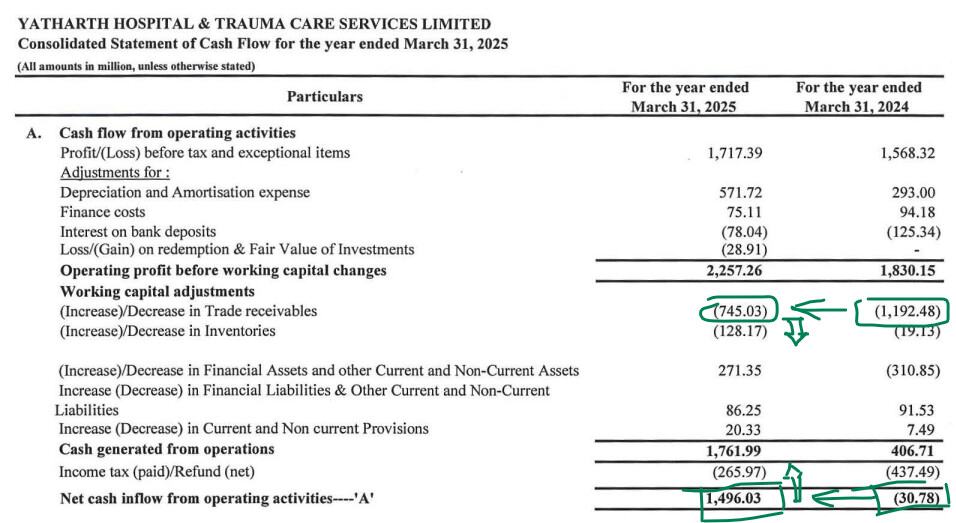

d) It is better to have a hospital with less govt scheme associated patients because the WC gets hampered due to high receivable from govt. (e.g., Yatharth).

e) Focus on ailments which have high growth and high margin (e.g., oncology).

f) It is generally seen multi-speciality hospitals have higher occupancy as compared to single speciality hospital (e.g., Rainbow). However this can turn.

g) Tier 1 player can’t offer the same services at same price in tier 2 city, whereas a tier 2 player can offer affordable services to tier 1 city and can also expect ARPOB to rise when shifting from tier 2 to tier 1.

- [If tier 1 player wants to capture growth from tier 2, he will have to lower down the ARPOB]

h) Brand value and perception matter a lot!!!

- (More than you think, no one will risk their lives in a mediocre branded hospital)

i) Having an asset-light model can help reduce capex burden and eventually will help to have superior return profile

- (e.g., hub-spoke model, leased land/buildings) Because hospitals are too capex heavy with good gestation period to break-even.

j) International patients give you high margin because usually hospitals charge a good markup to them. (Maybe 20%-25%)

- [Rev from them is still around 4-5% only]

k) To become a pan-India player from a regional or local player:

- It is important to make acquisitions at a good deal and turn it around well.

- (Because becoming a PAN India player organically is very difficult as it takes 2-3 years to set-up a hospital and another 18–24 months to break-even)

l) Usually when a regional player adds more beds in the same geography it can break-even faster (due to brand and operations being strong)

m) The best time to make an entry in hospitals is when majority of the capex is done and operating leverage starts to kick in

- [The valuation driver of hospitals can be operating leverage, because more or less the clients see much seasonality in hospitals, there can be some thought (try to understand where can the margin bottom)]

n) It is better to have a look on ROCE, which includes lease liability (Ind AS 116)

o) The unit economics changes a lot when you transform from local player to PAN India player (ROCE, asset turn can get lower in this transition)

p) Doctors play an important role to create brand/perception.

- So it is important to figure how can they retain them

- (e.g., Kims have doctor-equity model, Rainbow has exclusive contract for 2-3 years, etc.)

q) In the context of capex and break-even, it’s better when it comes to brownfield capex because a majority chunk of fixed cost (mostly land) is not in the picture. So via brownfield the expected ROX, ROCE can be very high.