Yatharth Hospitals -

Q1 FY 26 results and concall highlights -

Revenues - 257 vs 211 cr, up 22 pc

EBITDA - 64 vs 54 cr, up 18 pc ( margins @ 25 vs 25.3 pc )

PAT - 42 vs 31 cr, up 35 pc ( due sharp reduction in interest costs and higher other income - both due to QIP )

Corporate level operational metrics -

Occupancies - 65 vs 61 pc

ARPOB - 32.4 k vs 30.5 k

IPD volumes - 19 k vs 15 k

OPD volumes - 1.05 lakh vs 0.87 lakh

IPD revenues - 228 vs 188 cr

OPD revenues - 29 vs 23 cr

Q1 FY 26 vs Q1 FY 25 revenue split ( hospital wise ) -

Noida Extension ( 450 beds ) - 34 vs 38 pc

Greater Noida ( 400 beds ) - 30 vs 33 pc

Noida ( 250 beds ) - 20 vs 23 pc

Jhansi ( 300 beds ) - 7 vs 5 pc

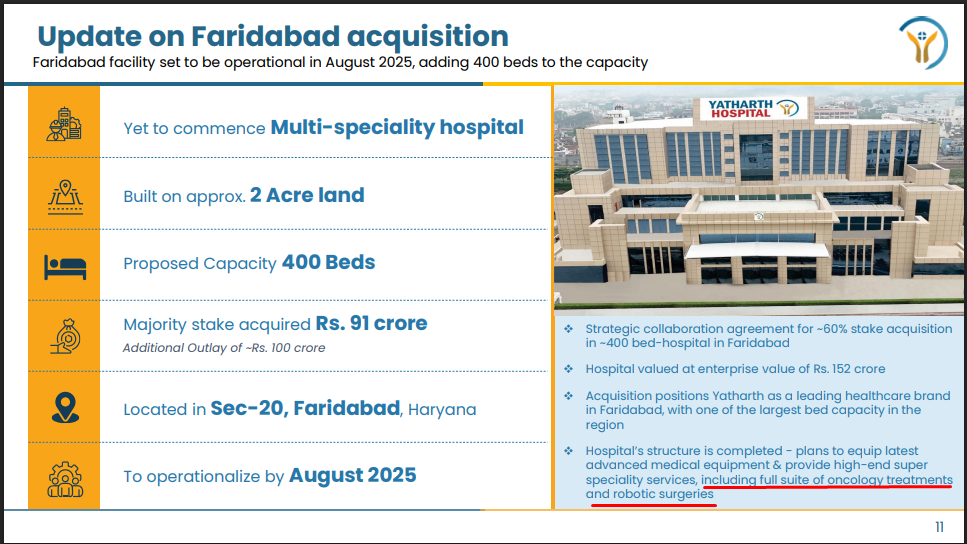

Greater Faridabad ( 200 beds ) - 9 vs 1 pc

Total bed capacity @ 1600

New Delhi hospital inaugurated in Jul 25 and Faridabad facility is set to open in Aug 25 - combined shall add 700 beds to the group’s capacity

Greater Faridabad hospital turned net profit positive within 1 yr of its opening ( its ARPOB was Rs 31 k )

Jhansi hospital’s occupancy improved sharply to 59 from 45 pc LY. Similarly, Greater Faridabad Hospital’s occupancy saw a sharp surge from 10 pc LY to 55 pc

Company aims to add another 750 beds - through a mix of inorganic acquisitions + brownfield expansions over next 2 yrs - taking the bed count to > 3000 ( including the New Delhi, Faridabad facilities going live in Q2 FY 26 )

New Delhi’s ARPOB should be in line with their Noida hospital. Their Faribabad facility’s ARPOB should be in line with their Noida extension facility

Company estimates that both Delhi and Faribadab hospitals ( 2 new openings in Q2 ) should turn PAT positive in 15 months time

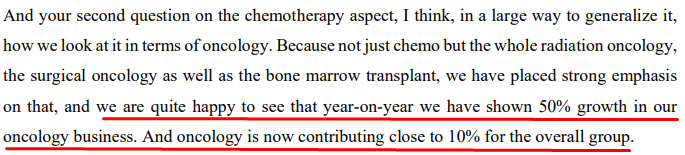

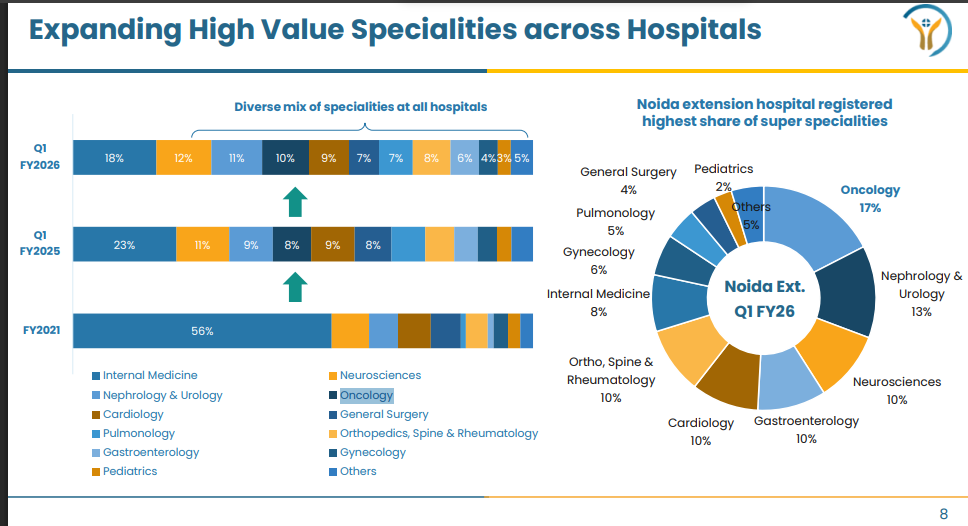

Oncology now contributes to > 10 pc of company’s revenues. Should trend higher going forward

Payor mix - Govt business mix is down from 40 to 35 pc over last 15 months ( this is a key monitorable - should come down going forward otherwise the working capital cycle and ARPOBs suffer ) . Rest 65 pc is almost equally split between insurance and cash business

Cash on books @ aprox 300 cr ( very comfortable position for the company to be able to even go for an inorganic acquisition )

Greater Faridabad hospital’s Govt Payor mix is much lower @ around 20 pc . Company expects similar trends for their new Delhi and Faridabad hospitals going live in Q2

Looking @ 8-10 pc ARPOB growth at corporate level for this year and next FY

Greater Noida + Noida extension - brownfield expansion should now begin ( post opening of 2 new hospitals in Delhi ). Aim to add aprox 250 beds here ( combined ) by FY 28

Cumulative capex for next 3 yrs projected to be around 1400 - 1500 cr - this should take the total beds beyond 3000 beds which they aim to hit by FY 28 ( including acquisitions + brownfield expansions ).

Guiding for an approximate topline growth of 30 pc for FY 26

Noida extension, Greater Noida - peak occupancies should be around 75-80 pc. Company is inching towards it. In coming 1-2 yrs, should be able to reach there

Company is targeting - their new hospitals at Delhi + Faridabad should get empaneled with Govt and 90 pc of Insurance companies within their first year of operations

EBITDA margins should be around 24 pc for Q2 and Q3 ( vs 25 pc for Q1 ) due to the expenses that are going to be incurred as the two new hospitals go live - not a meaningful contraction ( imho )

Greater Noida + Noida extension brownfield should cost them aprox 175 cr. Have earmarked 300-350 cr for inorganic acquisition inside next 1 yr. Rest of the money ( out of budgeted capex of 1400 cr, shall be spent on Greenfield expansion or another acquisition )

Debtor days for FY 25 was around 125 days. By end of H1, this should reduce to aprox 117-118 days

The brownfield expansion @ Greater Noida and Noida extension should go live within 24 months from now

As the govt business comes down below 25 over next 2-3 yrs, receivables should show a further decline

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation, posted for informational purposes