Yatharth Hospitals -

Q3 FY 25 results and concall highlights -

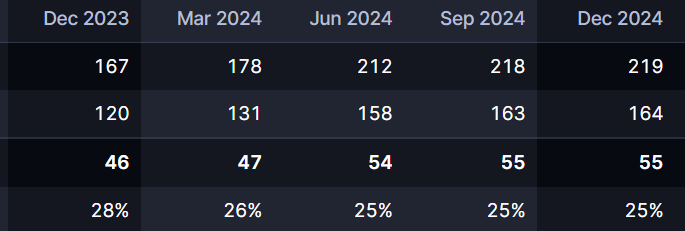

Revenues - 219 vs 167 cr, up 31 pc, led by operationalisation of Greater Faridabad hospital

EBITDA - 55 vs 47 cr ( margins @ 25 vs 28 pc ). Employee expenses were up at 42 vs 30 cr YoY. Other expenses were up @ 79 vs 58 cr YoY

Depreciation @ 17 vs 8 cr YoY

PAT - 30 vs 29 cr

Most of the additional costs relate to operationalisation of a new hospital ( greater Faridabad ) and the losses incurred thereof

Occupancy @ 60 vs 52 pc

ARPOB @ Rs 30.6k vs Rs 29.3k

Hospital wise revenue contribution, percentage contribution to total revenues -

Greater Noida - 66 vs 58 cr, 30 vs 35 pc YoY

Noida Extension - 79 vs 55 cr, 36 vs 33 pc YoY

Noida - 44 vs 43 cr, 20 vs 26 pc YoY

Jhansi - 18 vs 9 cr, 9 vs 6 pc YoY

Faridabad - 11 vs NIL cr, 5 vs NIL pc YoY

Top contributors ( therapy wise ) -

Oncology - 21 pc

Cardio - 12 pc

Nephro and Urology - 10 pc

Internal Medicine - 10 pc

Neuro - 9 pc

GI - 7 pc

Ortho - 6 pc

General Surgery - 6 pc

Gynae - 6 pc

Pulmonology - 6 pc

Paediatrics and Others - 7 pc

Company raised 625 cr in Q3 via QIP. Utilisation of QIP funds is as follows -

Debt repayment - 96 cr

Funding of recent acquisitions - 151 cr

Purchase of Medical Equipment - 217 cr

General corporate expenses - 140 cr

Total - 604 cr

Anchor investors in the QIP included - Kotak MF, SBI Life, Bandhan MF, Carnelian PMS, Taurus MF, Canara HSBC Life, Universal Sompo General

Update on acquisitions -

- Acquired 60 pc stake in a 400 bedded hospital in Faridabad. Built in 2 acres, Muti speciality, located in Sec 20. Operations to commence in Q1 FY 26

- Acquired 300 bedded hospital in Model Town ( 100 pc stake ), New Delhi. Located in a high per capita income colony, has a large catchment of residential and institutional clients. Operations to commence in Q1 FY 26

Once the new Faridabad and Model Town hospital goes live ( in Q1 Next FY ), Yatharth will become the 3rd largest hospital chain in NCR after Appolo and Fortis. At no 4,5 shall be Medanta, Paras Health

Occupancy levels @ current hospitals -

Greater Noida - 400 beds, occupancy @ 65 pc

Noida - 250 beds, occupancy @ 80 pc

Noida Extension - 450 beds, occupancy @ 60 pc

Jhansi - 305 beds, occupancy @ 50 pc

Greater Faridabad - 200 beds, occupancy @ 31 pc

Model Town, 2nd Faridabad hospital to go live in Q1 FY 26. Post their operationalisation, the total bed capacity will reach 2300 beds. Company aims to take this upto 3000 beds by end of FY 28 - via organic + inorganic routes

Company has appointed Deloitte as their Internal auditor - to manage risks, strengthening financial management

IT raids conducted on the company in 2023 and the IT department had frozen certain amount of money pending resolution of the case. However, company is allowed to use that money after obtaining permissions from the IT department. The company has been doing so and is being allowed to do so in recent past. Company does not fore see any significant losses / impairment from these events and is confident of a favourable resolution

Company expects this provisional attachment of Rs 60 cr with the IT department to get released in near future

A new hospital generally takes about 18 - 24 months to break even. Expect the same from the two new Faridabad and one new Model Town hospital

Greater Faridabad hospital is picking up momentum and is doing well in Q4 as well

It generally takes 2 yrs kind of time to complete an IT case in India. This case has been on for > 14 months now. Company expects a full resolution in next FY

Remaining cash on books will be used for brownfield expansions @ Greater Noida, Noida hospitals

As the new hospitals on online in Q1 next FY, expect further increase in Employees cost + Depreciation etc. However, at the same time - benefits from the Greater Faridabad hospital should start to flow in by that time

Qtly Depreciation rate for next FY should be around 20 cr wef next FY

In next 2 yrs, company expects to bring down the Govt business to less than 25 pc of the total business vs 35 pc currently. This should also help the company to accelerate their ARPOB growth

The new hospitals that the company is starting have a very low share of Govt business ( < 15 pc ) - should be ARPOB, margin accretive

Company expects to keep growing topline @ 25-30 pc rate for FY 26 as well

The new Faridabad and New Delhi hospital are expected to have ARPOBs > 35k

Business in Jan 25 was buoyant. Q4 is generally the strongest Qtr for hospitals in North India

Disc: holding, biased, not a buy/sell recommendation, not SEBI registered. IMO - once the IT hangover is over, the stock may be in for a re-rating