Stock generally remains in pressure after QIPs aided by the negative sentiment in overall market and a softer quarter upcoming. As far as fooling is concerned how will the management fool them? there’s nothing which was revealed afterwards and valuations I think the funds which applied for the QIP are good at it.

The tax related filing on 17th December is one key reason for stock downturn. ( QIP not so much IMO). Today even Ambit dropped coverage on the stock as it was unable to quantity impact of tax on Yatharth financials.

However, it is still unclear how much it will impact.

The other things happening in the company look okay to me .

- The H2 FY25 should be good if we go by company guidance.

- The recent acquisition of hospital may be positive to neutral. Can’t say really.

- QIP leads to clean balance sheet as there won’t be much debt I feel.

- With current balance sheet, the company looks well poised for strong top line and EPS growth over coming 3-4 years.

Just sharing my thoughts. I can be wrong.

Disclosure: invested

4 Likes

No the tax news was already digested IT department frozed just 70cr back in oct 23 and half of the amount is already released, the only issue that could happen is the land case for jhansi hospital that got stay order from the high court

2 Likes

Key concerns raised by Ambit:

- IT Proceedings:

The Income Tax Department conducted raids on Yatharth Hospital in October 2023. Recently, authorities attached several properties and equity shares in three subsidiaries under Section 281B of the Income Tax Act. - Uncertainty in Financial Impact:

Ambit cited its inability to assess the potential financial impact of the IT proceedings as a reason for dropping coverage, adding to investor apprehensions. - Delayed Disclosure:

The company disclosed the IT-related developments in December 2023, after completing a Rs 700 crore Qualified Institutional Placem

1 Like

Can you mention the source ambit didnt update with their official handle neither pranshant nair did and yatharth had already disclosed before even the qip was opened

there are soo many errors firstly it says dec 23 then it says raising 700cr(625cr actually) and placement completed on dec 19 while the placement closed on 24th and even if we consider 19th which is not true btw it is still before they filied about the tax notice that was 17th

there I had mentioned

Never get attached to your investments. I don’t know what better way I could have tried to highlight both fundamental issues with the company like constant equity dilution, debt repayment by funds raised thru QIP and dishonest management.

This was 2 days before the announcement of another QIP of 700 Cr. on 1 Nov. 2024 and after looking at the issue size, it was the end of story for me. The company would have easily touched 10,000 Cr. market cap had they not done another QIP and if market didn’t lose its momentum but it does not matter, at the end fundamentals win. I had exited my position long back after I realized it was not the gem I was hoping it to be.

Even after sharing the basic fundamentals that were not in the favor of the company investors on the forum were still defending it with all kinds of made up logic. Everyone can check the thread around Sept last year, for the discussion over fundamentals and logics used in defence earlier.

Even now someone mentioned that the balance sheet would be clean because of less debt and more funds raised in QIP and quotes like “bhaav bhagwan che”, now who wants to argue with that.

Sharing few more interesting points I came across…

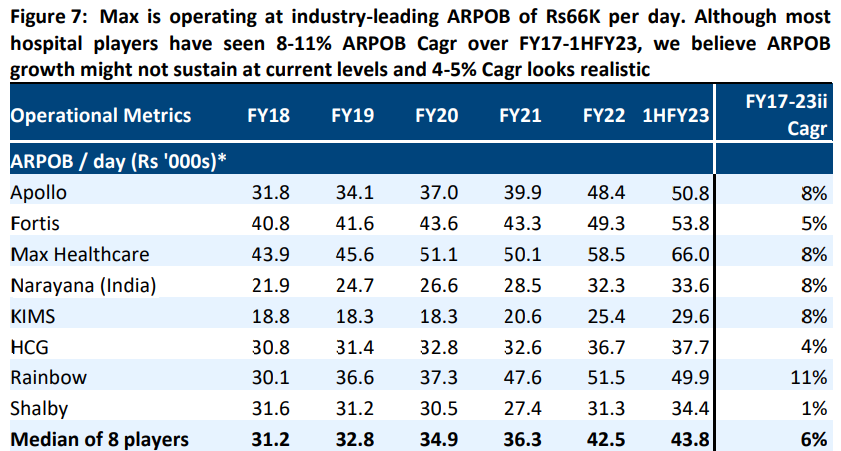

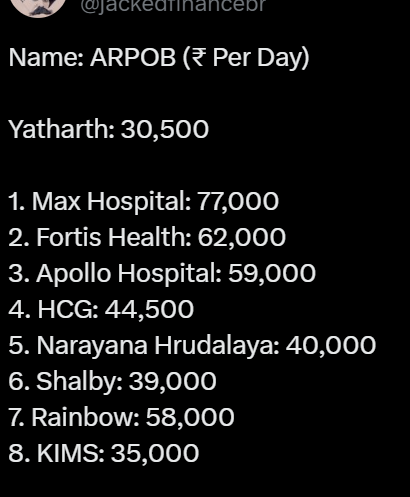

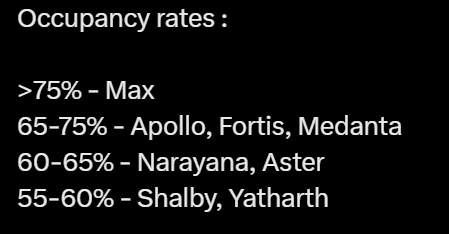

Capex per bed + ARPOB + Occupancy rate

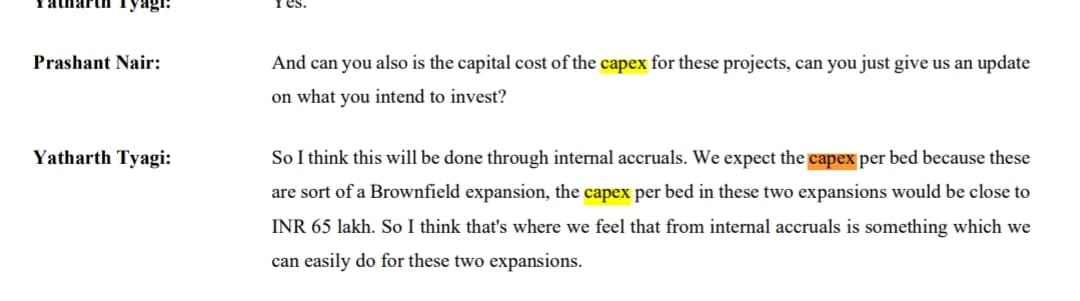

1. Capex per bed - This was a little shocking for me that their Capex per bed was around 65 Lakhs, because earlier I was under the impression that their Capex per bed was one of the lowest in the industry.

- In comparison to other hospitals, capex per bed is very high. Considering other hospitals can charge premium and generate a much higher ARPOB and occupancy rates.

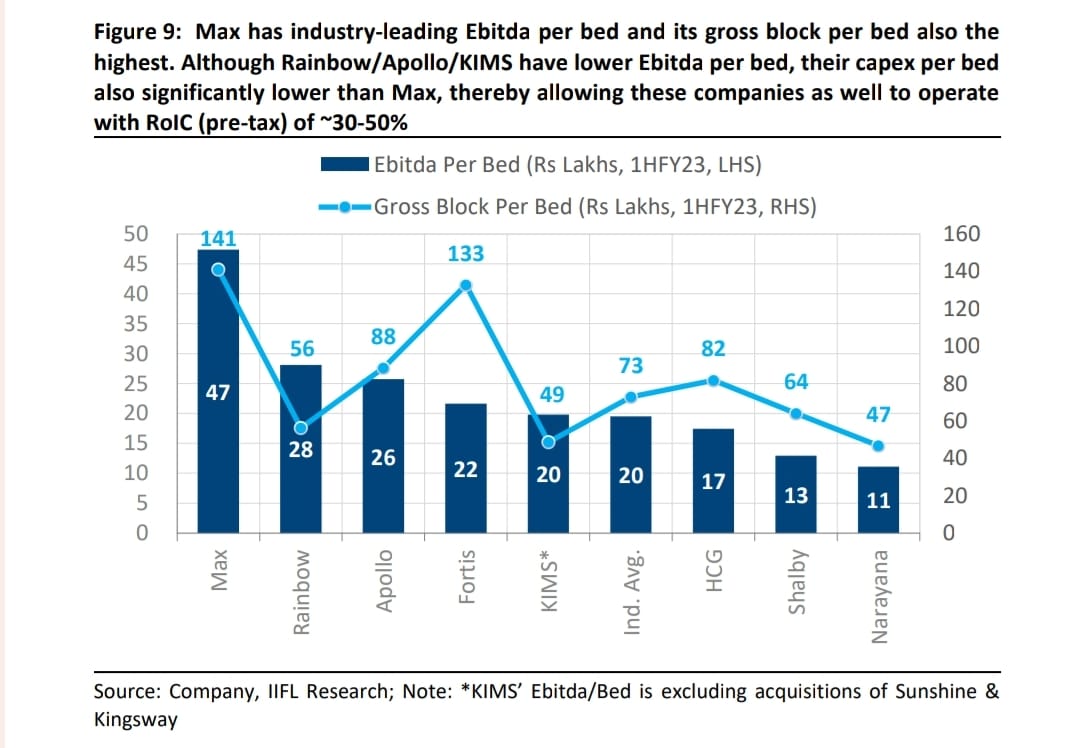

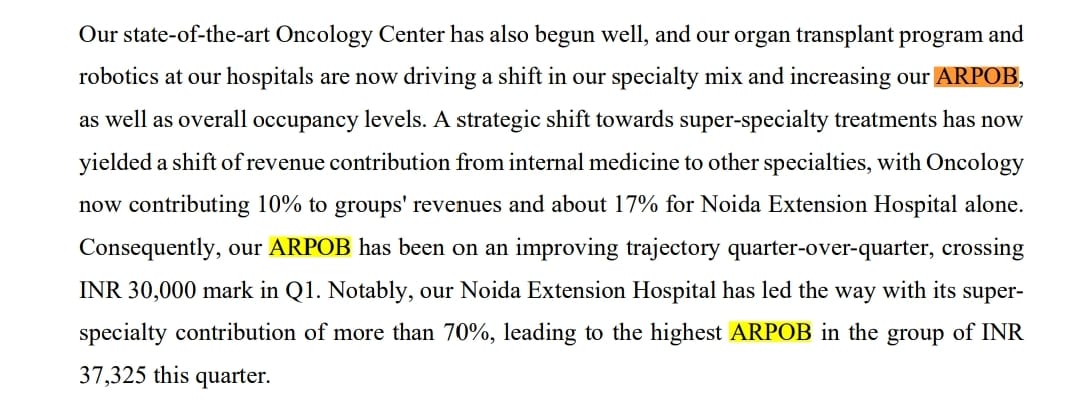

2. Avg. revenue per operational bed - ARPOB is among the lowest in the industry.

- ARPOB for Yatharth at group level is at ₹30,000 close to Narayana, KIMS and Shalby but Capex per bed is the highest among all (except Shalby).

Mind you this is FY2023 data, so consider that current ARPOB of these hospitals has risen by 6-8% CAGR in the last 2 years. But the ARPOB of Yatharth is of FY2024, putting that in calculation Yatharth has the lowest ARPOB in the industry.

- These are the current approx. ARPOBs across the industry.

- Occupancy rates - On the lower end.

Combining all the three factors, Yatharth should be generating ROCE lower than industry average. As per FY2022 ICRA report… Max hospitals has highest gross block per bed but also generates highest EBITDA per bed, having ROCE of 29%. Compared to this industry average ROCE is around 21%. But somehow Yatharth is generating ROCE of 30+% as per their AR.

Disc. - Not holding any positions.

13 Likes

Citigroup Global Markets Mauritius Private Limited sold around 40% today despite participating in the QIP a month ago at around 595. They must have sold at a loss (avg price 458). Something doesn’t seem right. Why would they sell so soon.

1 Like

There is the clarification from the company!!

1 Like

i have 1 question about yatharth’s management are they trusted

1 Like

No one here knows them personally I think and being listed just a year ago we dont even have a big history but that’s a risk in any investment you make (especially in a small or midcap) but by far the management have walked the talk but we dont know about the future so thats upto the individual but as far as this IT raid is concerned I dont think it should be an issue every 2nd growing company goes through this that’s how the system works here!!

3 Likes

No one really knows that to be certain, the stock volume today speaks for itself must have been a big whale exiting their positions on screen, which is a huge negative. As for me I was holding since lower levels and have completely exited my position.

Disc - No Holding.

3 Likes

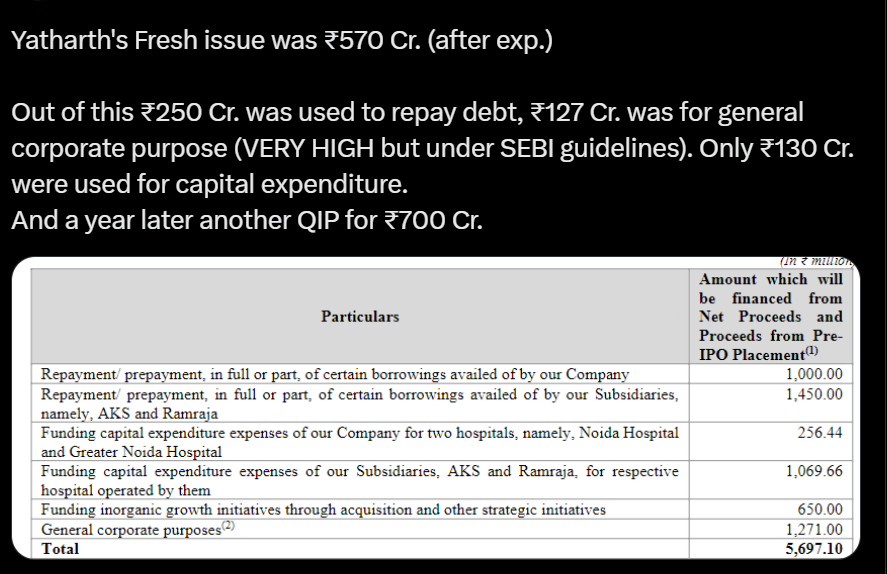

For this, would like to highlight two things…

1. A very high amount of proceedings from the Fresh issue was set aside for general corporate purpose

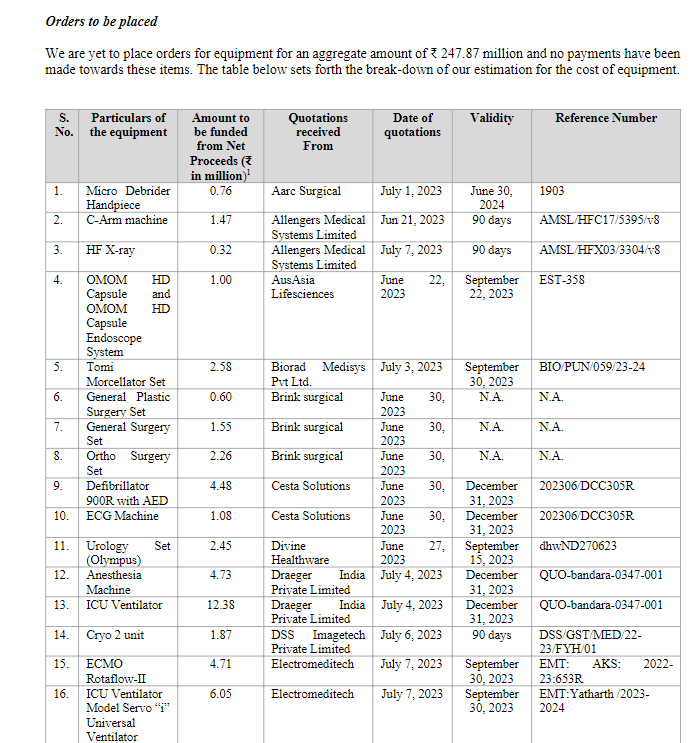

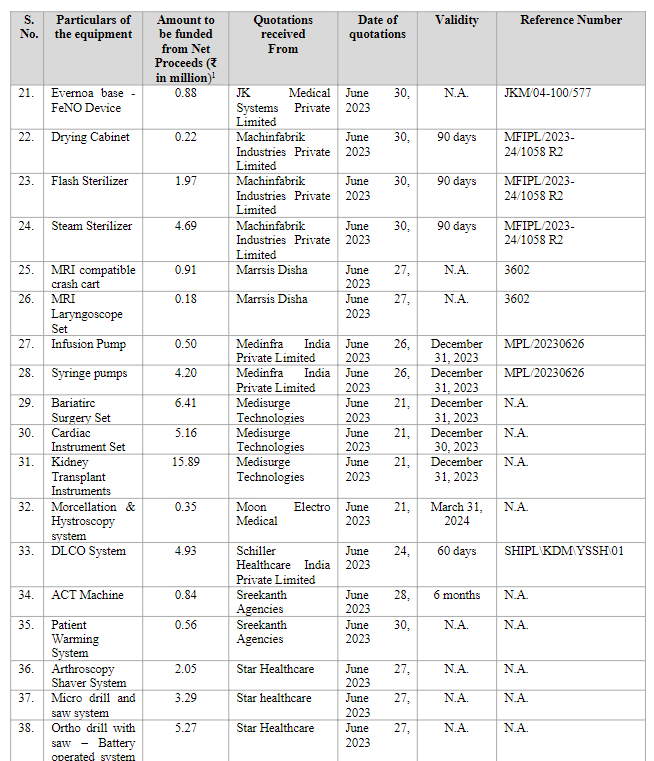

2. Take a look at the capital expenditure from their DRHP

This is the list of Capital expenditure for their Noida and Greater Noida Hospital, both of which are very mature and have been operating profitably for years.

Apparently they can’t even finance machinery worth a few lakhs without capital infusion? It looks as if they made the list of Capital expenditure just for the name sake.

5 Likes

Yatharth reported its financial results for Q3 FY2024-25, showing marginal growth in both standalone and consolidated operations. On a standalone basis, the company recorded revenue from operations of ₹1,104.11 million, marking an 8.5% increase from ₹1,017.31 million in the same quarter last year. The standalone net profit grew by 5.4% year-over-year to ₹222.53 million, with an earnings per share of ₹2.60. The consolidated performance was better, with revenue from operations reaching ₹2,191.55 million, a 31.4% increase from ₹1,667.93 million in Q3 FY2023-24. Consolidated net profit rose by 3.4% to ₹304.91 million, resulting in an earnings per share of ₹3.57.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/dd00a396-6511-4ae6-828d-b5fe1d6f9603.pdf

1 Like

That is pretty good numbers!! Now 1000cr this FY doesn’t look unachievable ! Let’s see what management has to say tomorrow!!

1 Like

If someone can attend the earnings call today, can you try to get some some color on…

for the two new hospitals (model town Delhi, Greater Faridabad) , how much more capital infusion is needed from Yatharth side to start operations, will it be phased manner or entire hospital capacity will be brought up onle at once?

when will they be fully operational, how long will it take to reach 70% occupancy

whats the expected ROCE?

why Faridabad hospital isn’t scaling up wrt to occupancy, its occupancy lower than last quarter, what the time line to get 60-70% occupancy for entire 200 beds?

3 Likes