debtors days is high bcoz 40% of the revenue use to come from the government schmes and there’s always a delay in the payment of govt but now they have reduced this to around 33% and the management has mentioned this in almost every concall they are expecting debtor days to be 100 by the end of FY25 and they want the govt revenue to take down to 20-25% in the couple of years that will help the debtor days come down further more!! Also the newly acquired hospitals which will be operational on the first day of FY26 they would have only 20-25% of the business from the govt from the day 1 itself! As they are also now bringing known doctors on board that will further help!!

Hope that answers!!

Disc:- Invested

2 Likes

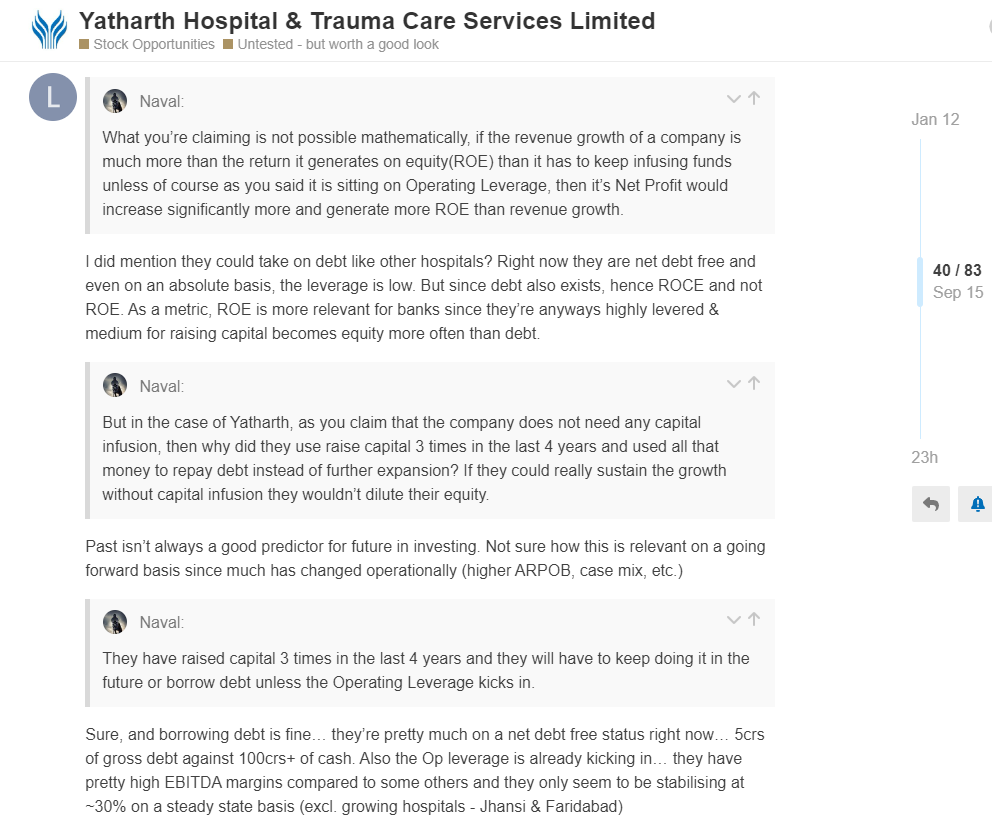

Did not expect a large fund raise like this considering the IPO was only 1 year back, and have cash on books, also they are generating cash flow and are improving. the scale of fund raise is almost 10-13% dilution. I know company is expanding quick, but dilution of this size is not so pleasant.

2 Likes

May be they want to strenghen their trade receivables part

Can you please explain why they are raising such a huge fund of ₹700 cr.? It is almost equal to the entire Shareholder’s fund atm. Still not a concern ig, because obviously they need funds to acquire more hospitals and grow rapidly?

3 Likes

They want to grow and grow quick obviously… they could grow organically and without less dilution too but that does come slowly… the way I see it - existing hospitals would continue to churn cash (around 200 Cr every year)… this plus this extra capital will be used to ramp up commissioning of existing M&A and for future M&A.

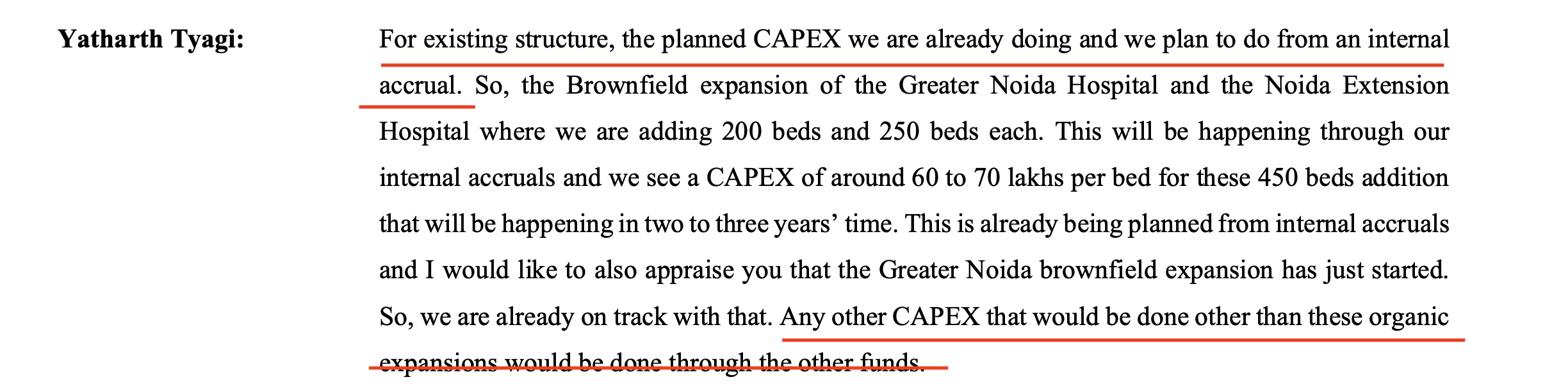

They need around 350cr for both of the newly acquired hospital to get operational on the first day of next FY and then again they will be acquiring another hospital next FY accusation cost should be approximately around 200-250cr that makes around 600cr and the expansion for the noida hospital will be from the internal accruals so the target for 3000 bed for FY27-28 should be achievable through this QIP they had an option for debt as well but the interest cost could’ve added extra burden given the piled up receivables and not to forget a single hospital has a maintenance capex of 15cr every year.

1 Like

Hi all…Have been on a recent visit to this hospital. I would like to tell you all about it, hoping it helps you all make an informed decision.

I live in New Delhi, am a doctor myself. Have been to various corporate hospitals such as Fortis,Max,Medanta,Rainbow, etc.

Disclaimer:

Visit was on a Sunday. So very less crowd. Hence, can’t comment on OPD numbers.

My relative was admitted as an emergency on Saturday night.

- Emergency care was adequate. The staff was kind ( we are dealing with an old couple). That’s where the good stops.

- The visit was to the Greater Noida Hospital, which is supposed to be their biggest. As compared to their Noida extension centre.

- Infrastructure less than adequate. 15 floors. Only 1, slow lift was working. Another one stopped working and a patient had gotten stuck.

- Unnecessary testing ordered, advised for admission for atleast 5 days for a condition that really does not require it… probably because they had insurance. Sure, it helps revenue, but destroys trust.

Believe me, I’m all for doctors earning… But, doing it in such a way, is sure to be detrimental in the long term. - The qualifications of doctors there is a little questionable. Quite a few which I saw online are qualified in their speciality from private, paid universities. I’m not saying that they may not be good, but personally, I would be hesitant in keeping a known to, in their care.

Overall, it left a bad taste in the mouth. I would not like to visit again.

Good hospitals require atleast competent staff and doctors, a flair for patient care and reliable infrastructure… And even then struggle for profitability. Take away most of these, and I struggle to understand how they can generate revenue and profitability for their shareholders.

Views entirely personal.

26 Likes

Thank you for sharing your experience Doc!! Appreciate that!!

1 Like

Yatharth’s rapid expansion was already a significant concern for me. Now, knowing that this growth comes at the cost of quality is a major drawback. I am stopping my SIP for now until there is an improvement in quality. If the quality remains the same, I may even consider selling my existing shares.

just a feedback by random person and stopping SIP is a big decision. i am not questioning authenticity of this person but still you should collect more data to check the real fact.

2 Likes

@Rushil_Kumar , this is very helpful and your feedback is much appreciated. These are good metrics. For something like healthcare, mistrust on doctors quality and qualification if very fundamental, whatever economical the cost is on a comparative basis.

2 Likes

I have just stopped SIP not sold off the stock. Anyhow its not just about the authenticity from one person. I already had my doubts with

- Very fast expansion, (I would prefer management to focus on quality of existing hospital rather than blind purchase spree).

- Raising funds when they can easily use cash.

3 Likes

Hey, if you look at how the mgmt have handled the business you would see a similar pattern. Before they IPO’d in Aug’23 they had almost 270cr worth of debt on the books most of which was utilised in capacity expansion either in the form of land or buying out other smaller hospitals.

Post IPO it was a good move to reduce debt using IPO money due to the fact that hospital business inherently a slow ROC generating industry which requires huge capex before the next set of growth can come in. But at the same time it’s a stable ROE generating business meaning once the required capex in terms of setting up the hospital (equipments, infra, staff) is done the hospital will keep generating ebit.

With that in mind we can conclude that hospitals have phases - three mainly -

- Capex Phase - Where the mgmt through debt, IPO, equity financing raises money for next capex cycle.

- EBITDA Breakeven - It’s worth mentioning here that the industry ebitda breakeven for hospitals is somewehere close to 12-16 months and if they take up govt business the time reduces to 13-15 months. (Yatharth’s Jhansi Hospital is somewhere in this phase)

- EBIT Accretion - Slowly and gradually the hospital starts to catch up in terms of traction and starts contributing to the overall EBITDA.

For eg - another good hospital company in its capex phase is Narayana Hrudayala (you can study the balance sheet to understand why I’m saying this)

Coming to your question of why such a huge fund raise of 700cr my guess is because of two main reasons -

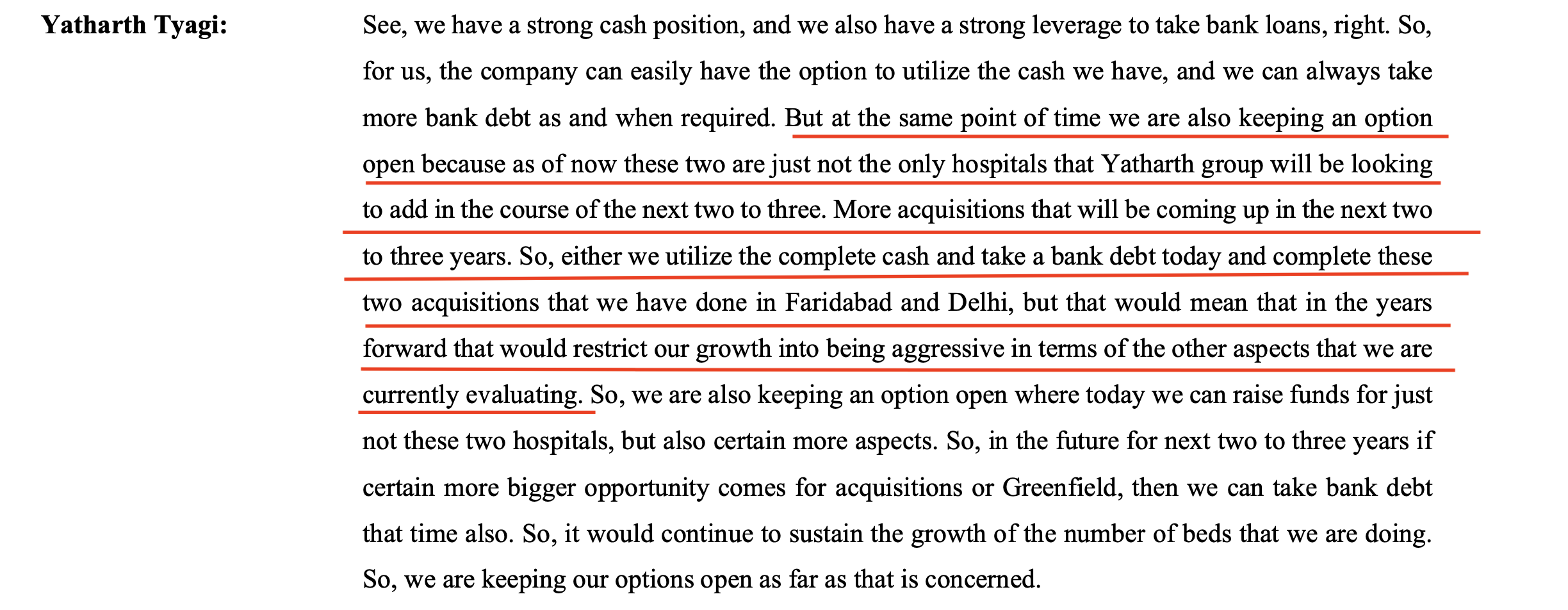

- They have just acquired two new hospitals in Delhi NCR and given the 3000+ bed guidance they might have to acquire more.

- The cash flows shows negative working capital changes probably due to the high share of govt business they have been doing in the past so it could be that mgmt was feeling some cash crunch (ofc QIP capital won’t be used for day to day operations)

Although we are very close to the next Q earnings call here’s what mgmt guided on the last set of similar questions -

To sum it up “Bhau Bhagwan Che” even after the overhang of S.281B notice of attachment and a bumper QIP signalling equity dilution the share price didn’t show weakness in the counter.

I hope this answers your query.

Disc: Invested, views are personal.

3 Likes

Hello Doc! Thanks for sharing your valuable feedback with the investor community, most of the hospitals in Delhi NCR have OPDs closed on sunday which explains the low footfall. I once visited Fortis, Gurgaon on a Sunday and saw a similar situation there.

Poor infra is a major issue, if one goes on google reviews the complaints about staff and infra are the most noticeable. As far as the number of tests ordered are concerned I think it’s an industry standard practice where if the patient has a health insurance the hospital tends to delay discharge/order more tests than required.

As far as the qualification of doctors are concerned I don’t think it would be appropriate to question their credibility unless they caused physical/mental harm owing to some medical negligence. In all these years I have personally visited most of the big hospitals in and around Delhi NCR and have on many instances encountered sub par medical advice.

Disc: Invested. Views are personal.

7 Likes

1 Like

QIP closed raised 625cr at 595rs

One more acquisition of super specialty hospital in New Delhi. Not much information provided regarding this acquisition.

Same hospital which early acquired in the month of October 2024 but the payment made today. No nee acquisition.

5 Likes

4 Likes