Yatharth Hospital’s board meeting on Nov 7th will discuss the agenda also includes potential fund raising through equity shares, convertible debentures, or other securities via private placement or public issue, subject to shareholder approval.

1 Like

Walk on talk is great but sustainable growth is better than aggressive expansion. In situation where our operating cash flow was negative last year. Margins will get impacted (fixed cost will be high) was that 60% acquisition necessary? Capital allocation is the key. We could have gone for the brownfield for existing capacity.

you are right that margin will be impacted in a shot run, In last call management said that for break even a new hospital needs 15 months time period and 30-35 % capacity utilisation. If company generate 200 bps less margin for 15 months and focus on the increasing the topline it will not impact much. As well as management is investing 100 Cr on Oncology treatment (robotic opearation). IT will also help to generate higher ARPOB.

THE COMBINATION OF HIGHER ARPOB AND HIGHER NUMBER OF BEDS WILL BOST THE TOPLINE AS WELL AS BOTTOM LINE.

1 Like

I’m not particularly concerned about the margins, as the industry naturally requires a minimum three-year period of initial strain, where costs are front-loaded and profits tend to come later. The acquisition of 300 beds was a strong move; however, was it necessary to acquire 60% of a facility? Expanding our existing units might have been a more strategic approach. My main concern lies in the capital allocation decisions. There are factors beyond our perspective, so I’m awaiting management’s response.

1 Like

Good Quarterly Result -

Source - https://www.bseindia.com/xml-data/corpfiling/AttachLive/514ca299-f654-4c53-ad9c-8a39393e3a2a.pdf

It was a decent quarter as it was expected, good improvement in ARPOB, occupancy in jhansi is ramping up that’s a good sign. Also the unfreezing of nearly half of the amount by IT department also is a good news, also 244cr of cash though around 160cr would be released for Delhi accusation is still decent for the quarters to come, debtors days down to around 122days TTM. Let’s see how will be the Management’s commentary tomorrow but I still dont think we can get close to 1000cr this FY, 500-600cr in 2 quarters that too Q3 being a weak quarter doesn’t look achievable!!

I still don’t understand the fund raising though let’s hope to get a good explanation tomorrow.

2 Likes

If the revenue gets around 800 as stated by crisil the net profit should be around 140cr and at 40x around 5700Cr Mcap approximately 10% higher than LTP, I dont think it will be valued more than 40times for 25% growth as big giants are also giving guidance of around 23% but at the same time revenue can cross 800cr as we are already at 430Cr and if we get around 180Cr in Q3 we can easily cross 240cr in the last quarter and get to 850cr mark making a 33% growth YoY as we did in the last FY.

Disc:- Views are obviously biased as invested!!

2 Likes

Q2 FY 2025 CONCALL HIGHILGHTS

Yatharth attracting leading doctors across NCR.

Deloitte is appointed as internal auditor.

Rise in employee cost due to new therapeutic areas, new doctors joining. Margins will be sustainable (25 to 26% at group level) with two more additional new hospitals. Mature Hospital margins is 28 to 29%.

Dropping occupancy in Noida hospitals due to reduction on government business. It is reduced by 1 to 2%. IPD volume increase. Focus on increasing cash and insurance segment. It will have positive impact in coming quarters.

EBIDTA loss in Faridabad Hospital, started in Q2 FY2025 is 28% Negative and reducing.

Planned CAPEX is from Internal accruals, 60 to 70 L per bed for expansion of beds in existing hospitals.

Decline in Jhansi ARPOB due to reduction in cash payments. Government panel drags in margin. It will be 15000 to 20000.

Max Hospital opened near Yatharth Hospital will build ecosystem in Noida, should benefit every operator. Continuous improving standards.

No difference between Q1 and Q2 Revenues due to no breakout of flu in areas of operation for Yatharth. Government business is reduced as per strategy by company.

Government business is reduced by 4% Q to Q, 6% H1 to H1. Target is to reduced government business to 25% in 3 years.

To fill available capacity government business is taken.

Expect Q3 and Q4 will be higher. Expect near to 1000cr. Revenue.

New Hospital in Model Town:

160cr. Will be paid to Union Bank. 25% paid by company’s book.

Additional 60 to 70 cr. For improving infrastructure and medical equipment. With this It will be 300 beds.

ARPOB in this hospital will be more than Noida hospital, will be super specialty in day one. It can be close to 40000 ARPOB easily achievable.

Existing capacity is 150 to 170 beds.

Hospital currently non-operational. It was operated by family of doctors. Face financial issue and bank take over. It was acquired by online auction.

Land, structure belong to Yatharth. No Rent.

Pay back period will be 3 to 3.5 years.

New Hospital in Faridabad:

Keep on investing on 60/40 % basis.

Minority shareholder is family from MGA. They do not operate any other hospital. One of the son is cardiologist.

Additional 90 cr will be spend to complete structure and medical equipment including Radiology.

Land, structure belong to Yatharth. No Rent.

Reason of adding one more hospital in Faridabad as they will be 15 to 20 km distance. Model of big player in city, which gives benefit of brand position, star doctors can be shared between two hospitals. Doctors wants to join as head of department as capacity will be 600 beds. Near to Airports and have great drainage of population and have massive expansion.

Expected ARPOB in this hospital can be 38000 Rs. Can be with start of and can go beyond.

Conclusion:

Revenue can continue grow with sustainable margin of 25 to 26%.

Have more debt, dilution in equity as company continue to acquire more hospitals.

Valuation is attractive compared to peers.

Room for improvement in ARPOB compared to peers.

Disclosure: Invested, may exit anytime. Reviewing.

3 Likes

Commentary from Q2 earnings call was good. From the developments in last 6 months, it it might look like the management is aggressive and trying over the limit of group’s ability. I think in the past they have executed well and maintained operation smoothly. Now the challenge is to harmonise/ synchronization of new additional capacity and getting to efficiency. We will know these metrics in next1-2 years. In 4-5 years they can get to 3000 bed capacity with ARPOB of Rs50000 at group level , with ebidta of 25%, and 85% occupancy, they can achieve an operating profit of over Rs 1000 Cr. There is optimism built in these assumptions.

However, the trajectory looks generally ok, with health care getting more and more organized, and the company’s effort to bring in high quality doctors , improvement in brand recognition. There is decent runway here for bit of expansion in valuation and reasonable growth.

Caveat is “the management will continue the good execution”.

2 Likes

Yatharth Hospitals -

Q2 FY 25 results and concall highlights -

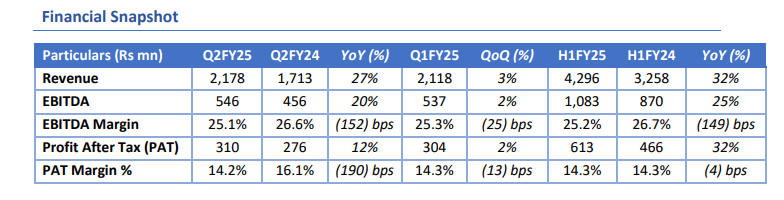

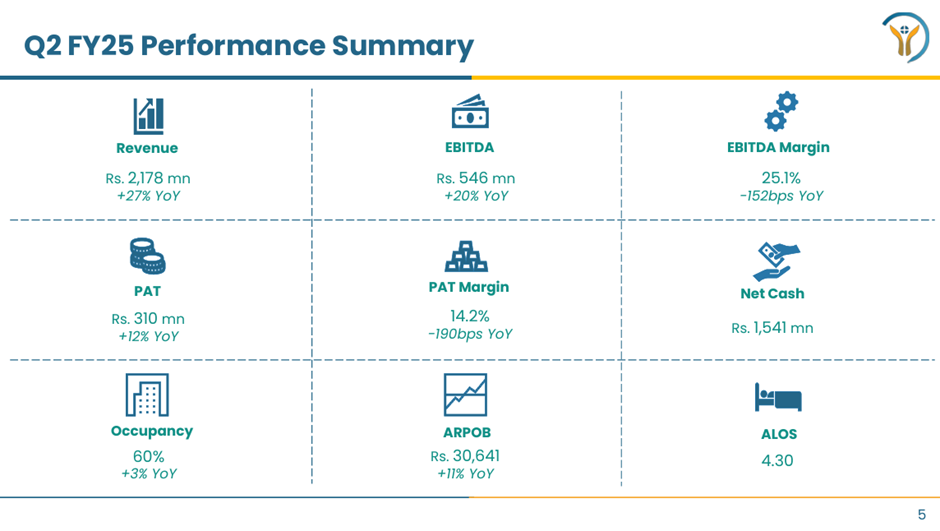

Revenues - 218 vs 171 cr, up 27 pc

EBITDA - 55 vs 46 cr, up 21 pc ( margins @ 25.1 vs 26.6 pc YoY )

PAT - 31 vs 27.5 cr, up 12 pc ( due accelerated depreciation and amortisation @ 16 vs 5 cr YoY )

Occupancy @ 60 pc, up 3 pc YoY

ARPOB @ 30.6k, up 11 pc YoY

Hospital Wise revenue contribution -

Noida Extension - 37 vs 31 pc

Greater Noida - 31 vs 36 pc

Noida - 21 vs 28 pc

Jhansi - 7 vs 5 pc

Faridabad - 4 pc vs NIL ( this hospital was acquired in Feb 24 )

In Oct 24, company has acquired 2 more hospitals - @ Model Town New Delhi ( for 160 cr, 300 beds ) and a second hospital in Faridabad ( bought 60 pc stake for 91 cr, bed capacity can go upto 400 + beds ). Both these hospitals are expected to go live in Q1 FY 26

Company’s existing bed capacity, Q2 ARPOB, Q2 Occupancy -

Greater Noida - 400 beds, 33k, 65 pc

Noida - 250 beds, 29k, 79 pc

Noida Extension - 450 beds, 38k, 59 pc

Jhansi - 300 beds, 14k, 48 pc

Faridabad - 200 beds, 28k, 38 pc

Company’s hospitals are at close distances from both Jewar and IGI International airports. This gives them ample opportunity to tap into Medical Tourism mkt

Company’s current bed capacity stands @ 1600. should go upto 2300 beds by Q1 FY 26 !!! ( because of recent acquisitions )

Cash on Books as on 31 Sep @ 244 cr - will be used for Faridabad, Model Town acquisitions

Company intends to infuse another 100 cr into the newly acquired hospital at Faridabad into upgrading its infra, medical equipment and setting up a new Onco unit. For the Model Town hospital, this figure should be around 60-70 cr

Onco now contributes to 12 pc of group revenues

Have appointed Delloite as their new Auditor

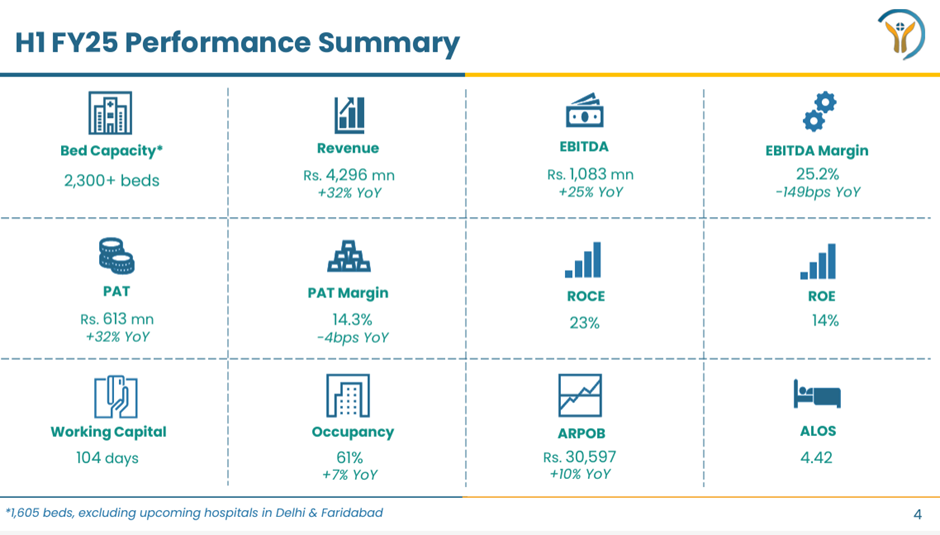

Working capital days have reduced from 112 days in Q4 FY 24 to 104 days in Q2 FY 25 ( despite sharp growth in H1 )

Model Town is a high per capita income area in North Delhi. Company expects this hospital to clock best ARPOB ( 40k or thereabouts to start with ) among their portfolio of hospitals

Model Town hospital was set up in 2019 but was non-operational for last 18 odd months as the previous promoters were facing financial difficulties and elected to halt operations

For both these new acquisitions, all the land, buildings shall come on the books of Yatharth Hospitals - basically they won’t have to pay rentals here

In Q2, there has been a slight drop in the occupancy levels @ Noida, Noida extension hospitals. The same has happened because of the company rationalising the Govt business. They are trying to improve the payor mix towards Insurance + Cash patients

Company intends to keep pursuing this inorganic acquisition strategy to expand their footprint for next 2-3 yrs as well. Plus they will be doing brownfield expansion at Noida extension and greater Noida hospitals - adding around 200 beds each over next 2-3 yrs

Aim to keep sustaining the 25 pc EBITDA margin trajectory for foreseeable future

**Company has reduced its share of Govt business ( which is lower margin ) by 6 percentage points H1 vs H1 LY. They aim to bring it down to 25 pc of their revenues inside next 3 yrs **

Expect to continue to see industry leading topline growth for FY 25-27 with EBITDA margins around 25 pc ( IMHO - this would be a huge positive if the company is able to pull this off )

Company is confident of sustaining 25 pc EBITDA margins in FY 26 despite operationalising 2 new hospitals wef Q1 FY 26 as they believe that the initial drag of two new hospitals will be compensated by increased occupancies and better ARPOBs at Greater Noida and Noida extension hospitals

Expect better results from the company in Q3, Q4 because of continued ramp up in the Faridabad, Jhansi, Noida Extension and greater Noida hospitals. Company should close FY 25 close to 1000 cr topline mark

Disc: holding, added recently, not SEBI registered, biased, not a buy/sell recommendation

6 Likes

Some thoughts: Blended: 1HFY25:30% IPD volume growth and 25% OPD growth (major lifting done in Q2). IPD revenue, up 33% while OPD revenue up 24%. ARPOB blended 10% y/y growth. IPD realization q/q has gone down aggressively. Blended occupancy up to 60% for the whole system. Greater Noida, saw occupancy dip from 73% to 65% but revenue is up 10%, so telling me that customers have paid more or/and got more complex treatment. Noida hospital has seen occupancy dip from 96% to 79% on account of higher beds (probably) but also lower revenue (only 6% decline) so again more private/cash and complex patient resulting in ARPOB jumping both at Noida as well as Greater Noida extension. Also, IPD volume is up 30% 1H and realisations have not dropped which again means that the additional private patient has not been dilutive to pricing. This implies that mix is changing with government reducing and private going up which is also suggestive of higher brand acceptance. Employee cost will need to be monitored. Finally, Faridabad ARPOB in line with Noida so not a bad area to expand.

4 Likes

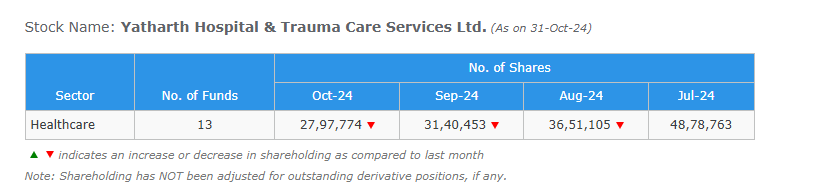

Seems there are lots of positive news and many growth driver for next couple of years, but there seems to be more selling pressure from mutual fund houses. I am wondering if most are concerned related EBITA De-growth from the more bed capacity which are going to be added in future. Its good keep track of all the metrics which can go wrong during the growth phase.

Disclosure: I don’t have any exposure to this counter. Studying this counter to improve overall Healthcare domain expertise.

Happy Investing,

Karthik

Its about a 2.25% decrease , but around 1.5% is compensated by increase in stake by FIIs.

Especially Marval, I was pleased to see them take a position, however small it is.

But yes, wonder why would some funds exit while company is doing generally good.

2 Likes

The valuations are coming near the industry valuations. My main motive for being interested in the company was the lower valuations compared the peers. Now I am seeing every other finfluencer covering the company on YouTube and linkedin posts for how it is the highest growing hospital. But since EV/EBITDA and PE is coming near the industry valuations, I doubt whether it makes sense to invest at these levels or not. The reason for worry is because of the “Issuer not cooperating” Rating by CRISIL, struggling free cashflows, and some issues going on within the management(as mentioned by someone above in the thread). Would like the views of others on these issues.

Disc. Holding a tracking position. No reco to buy/sell

1 Like

I see the PE ratio for TTM in screnner is b/w 39-40 compared to industry median of ~57(as per screener) and similar in case of EV/EBITDA .And considering the sector it is in ,compared to peers and its Mcap ,guidance the management is giving the valuations still seems to be attractive.

FY 25 - guidance 1000cr . considering similar net profit margins that were in fy24,Its profits are ~180cr.

PE ratio - cmap/net profit - 5202/180 - ~29

Disc: Invested tracking amount. Looking to enter when possible.

These are my views. Feel free to correct me

1 Like

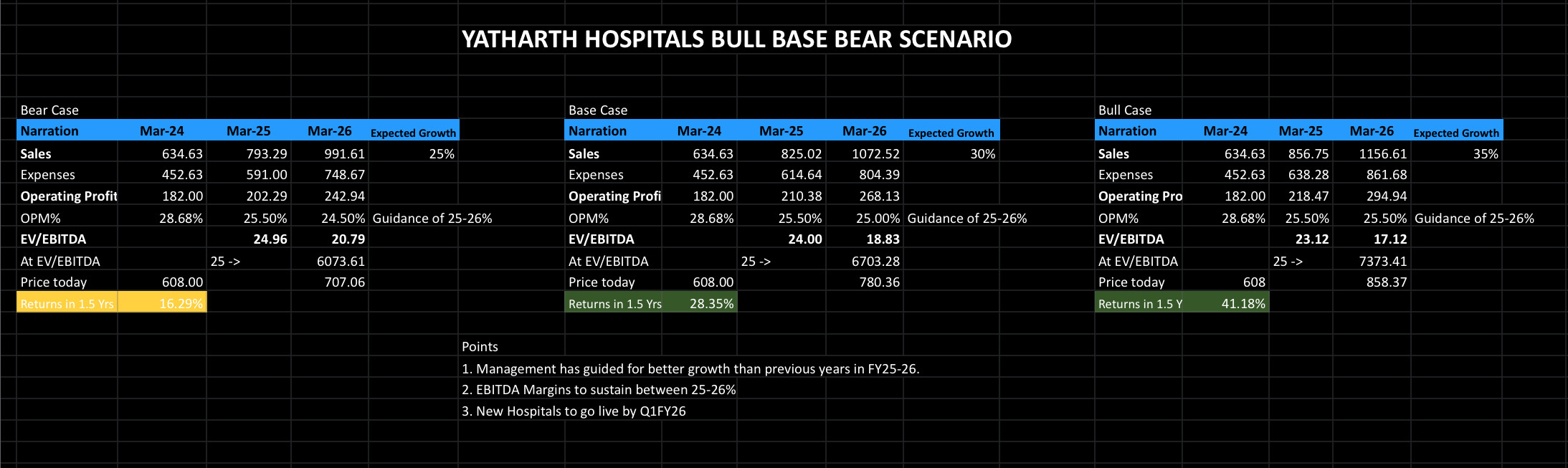

Created Bull base bear scenario for Yatharth hospitals for FY26.

In my view 8-10% fall from here will make it very interesting.

Disc: no reco.

4 Likes

Corporate Presentation November : https://www.bseindia.com/xml-data/corpfiling/AttachLive/f5661bfc-e4ee-496f-8f70-4a6cd87c4fdc.pdf

Didnt they mention most of the money is returned by the income tax department only around 30-31cr is still freezed? Is the income tax notice which company filed yesterday related to that or is it related to the land issue in jhansi case? BTW Floor price for QIP is set 626.18rs with 5% discount.

1 Like

Hello everyone,

I have just started looking at this company and the one thing that strikes out the most is the higher receivable days and cash conversion cycle.

Almost all the good players in the industry have a negative cash conversion cycle.

Can anyone help me understand, why is this not the case with Yatharth?

As per my understanding, this maybe due to higher ratio of Government Yojana patients. Do we have an idea of the ratio for this and are there any plans to reduce this and how?

1 Like

yes this is the reason as you mentioned in concoll they said they will reduce it gradually…when normal footfall comes to some point