Nuvama come up with research report.

Going Forward:

Capacity expansion by adding beds, occupancy increase on Jhansi and Faridabad hospital which are currently at approx. 25% AND 15%.

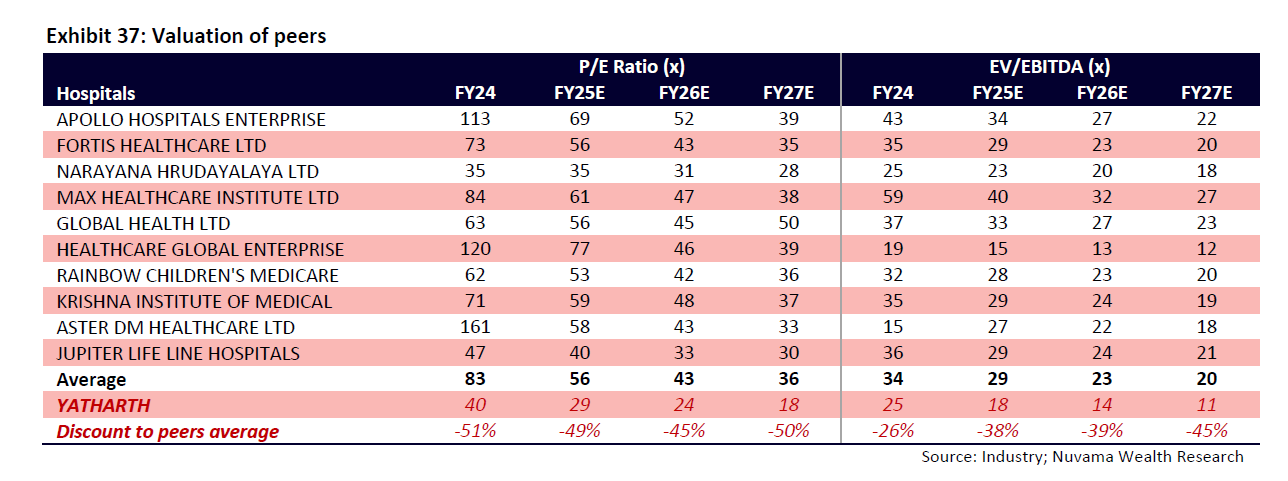

Margin expansion due to increase in ARPOB, Which is at 59% discount to peers in Delhi-NCR region, it will be supported by specialty clinics and treatment.

Narrowing down of valuation gap compared to peers.

Thanks for sharing this! I appreciate your effort.

I have a quick question - why do people post Excel links instead of direct Google Sheet links? With a Google Sheet, we could bookmark it and easily go back. For Excel files, we have to download them each time. Just curious about the reasoning behind this choice.

Company may decide to change the rating agency. In this case existing agency will mention in their report that the issuer company is not co-operating. Over the period of time another agency might come up with new ratings. This is normal and should not be taken seriously.

Optimistic and Confident: The promoters, led by Mr. Yatharth Tyagi (Whole-Time Director), consistently express confidence in the hospital’s performance, focusing on growth through both organic and inorganic means. They are proud of their achievements, such as introducing advanced robotic surgeries and expanding into new specialties like oncology and organ transplants.

Growth-Oriented: The tone in each call emphasizes aggressive growth strategies, particularly in expanding bed capacity and enhancing hospital services with advanced medical technologies. The leadership is forward-looking, aiming to double the bed capacity by 2028.

Commitment to Expansion: The promoters consistently highlight strategic acquisitions, including the purchase of hospitals like Asian Fidelis (Faridabad) and their continued efforts to grow in North India. This indicates their commitment to scaling the business rapidly through both greenfield and brownfield projects.

Growth Guidance:

Revenue and Bed Capacity Growth: Yatharth Hospitals has shown consistent double-digit revenue growth across all quarters. For instance, in Q4 FY24, revenue grew by 29%, and the company’s profit after tax surged by 74%. The promoters have set aggressive targets, aiming to increase bed capacity to 3,000 by FY28 through acquisitions and organic expansions .

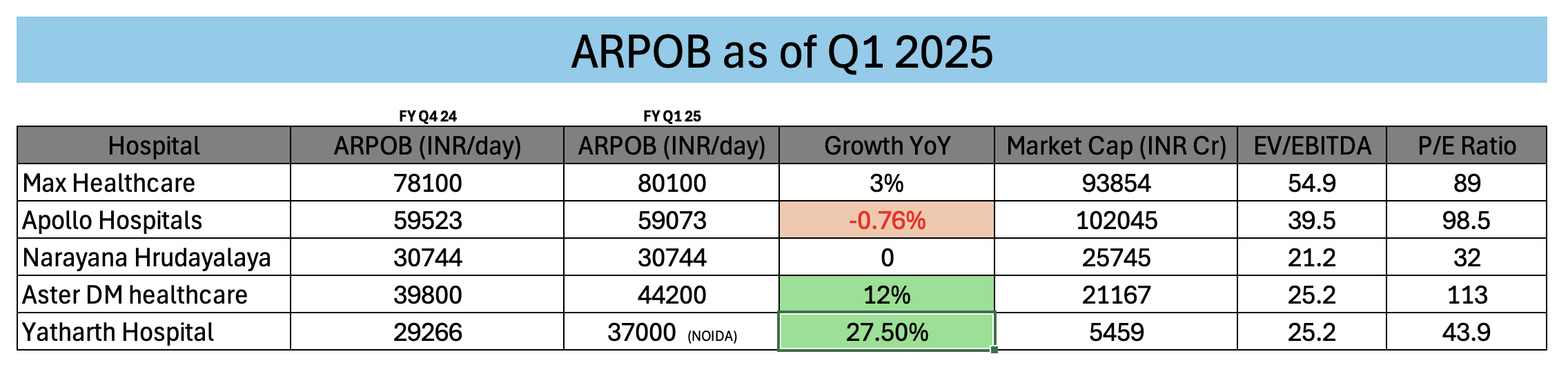

Focus on High-End Procedures: The hospital has successfully integrated robotic surgeries into their service offerings and expanded super-specialty treatments. These high-margin services are expected to drive higher ARPOB (Average Revenue Per Occupied Bed). Hospitals like Noida Extension are already achieving ARPOB as high as INR 37,000, significantly improving revenue per patient.

Strategic Acquisitions: The acquisition of hospitals, such as Asian Fidelis in Faridabad, and plans to acquire one hospital each year until FY26, reflect their ambition to grow rapidly. The company is also exploring partnerships in other healthcare segments, such as medical tourism.

Market Positioning and Expansions: The promoters aim to increase their footprint in regions like Delhi NCR, Uttar Pradesh, and potentially in Bihar and Madhya Pradesh. They are confident in capturing larger market shares in these regions.

Risks:

Inorganic Growth Risks: While acquisitions are an important part of the growth strategy, these carry risks related to integration challenges, financial outlay, and operational disruptions. The Faridabad acquisition is an example, where initial operational losses were incurred, and there is uncertainty regarding how quickly new acquisitions will break even.

High Dependence on Government Receivables: Around 35-40% of revenue comes from government schemes, but this also leads to delayed payments. As of March 2024, 75% of the receivables were from government entities, which can increase cash flow risks.

Debt and Financial Management: The company has reduced its finance costs substantially post-IPO but continues to take on debt for expansions. The strategic use of debt needs to be carefully managed to avoid over-leveraging, especially with upcoming acquisitions.

Operational Risks in New Markets: Expansions into new geographies, such as Bihar or Madhya Pradesh, come with market-specific risks, including competition from established players and regulatory hurdles.

The key monitorable for me here is Payer Mix improvement. A large chunk of revenue comes from Government healthcare schemes like CGHS, ECHS, ESI. Due to which there is payment delays and lower ARPOB.

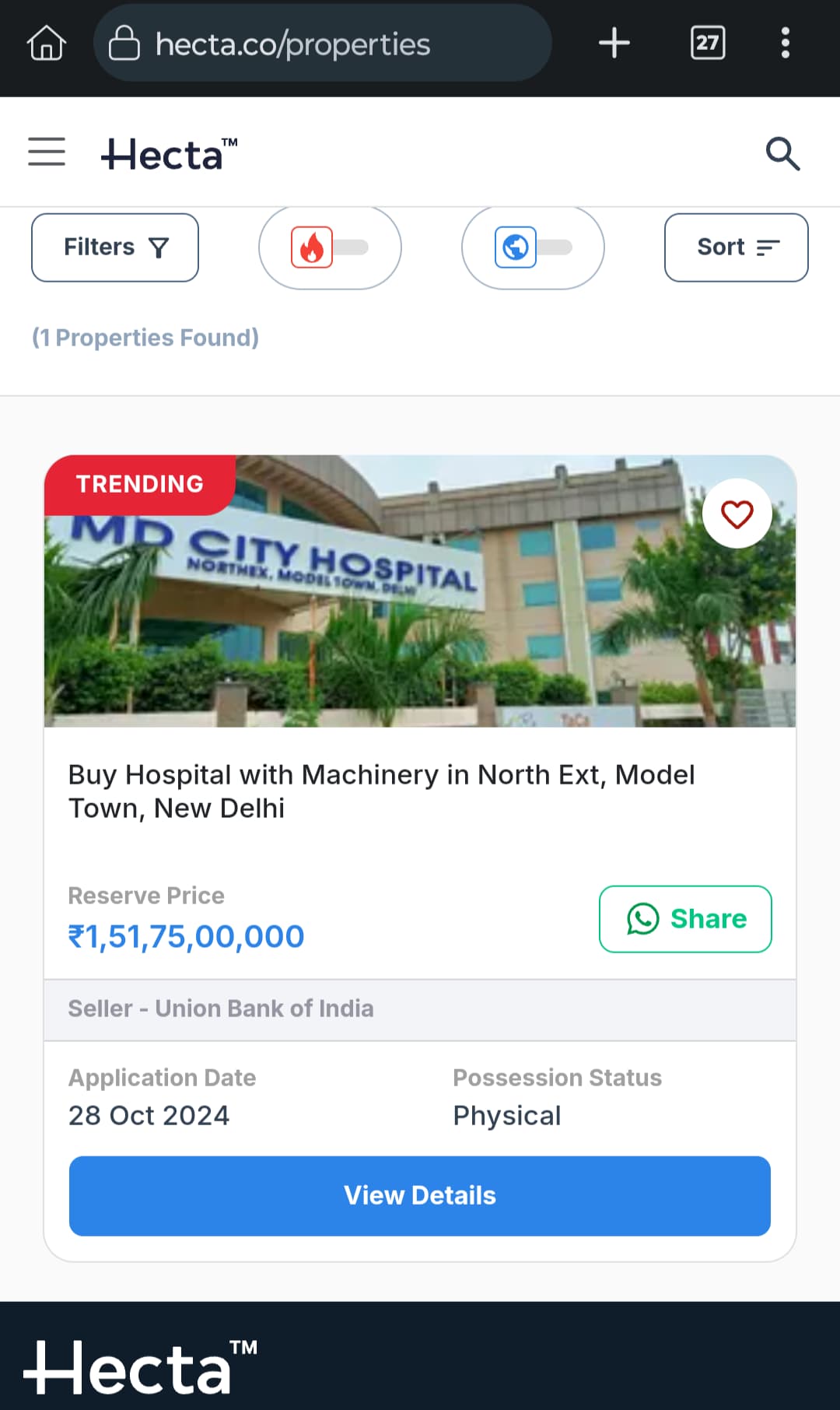

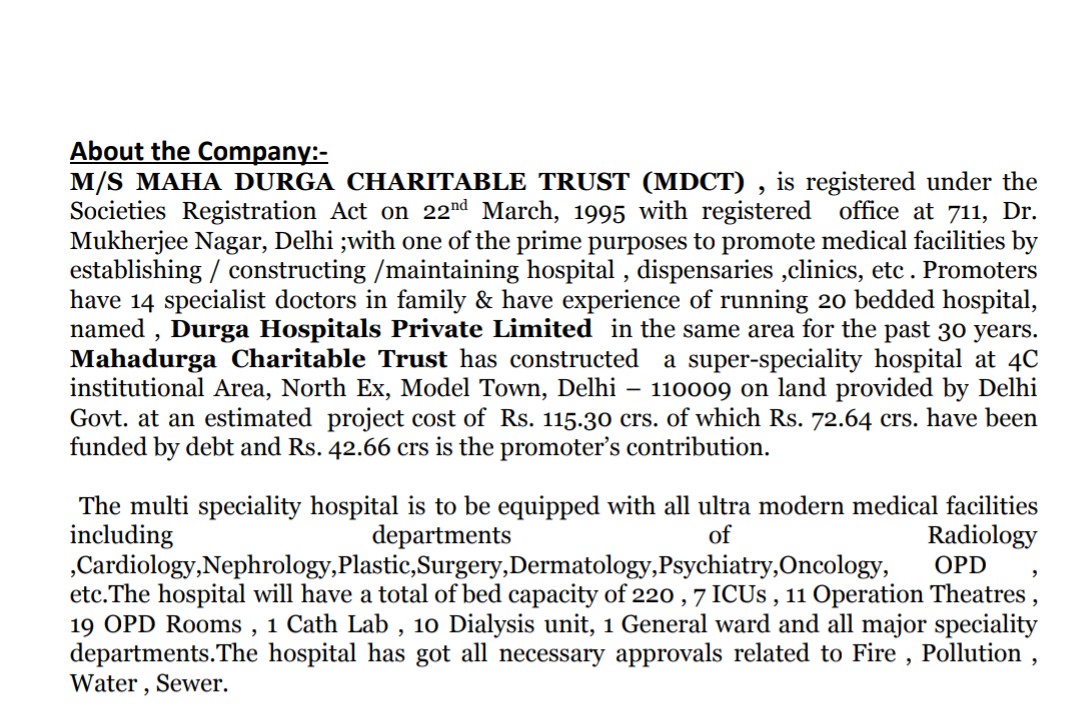

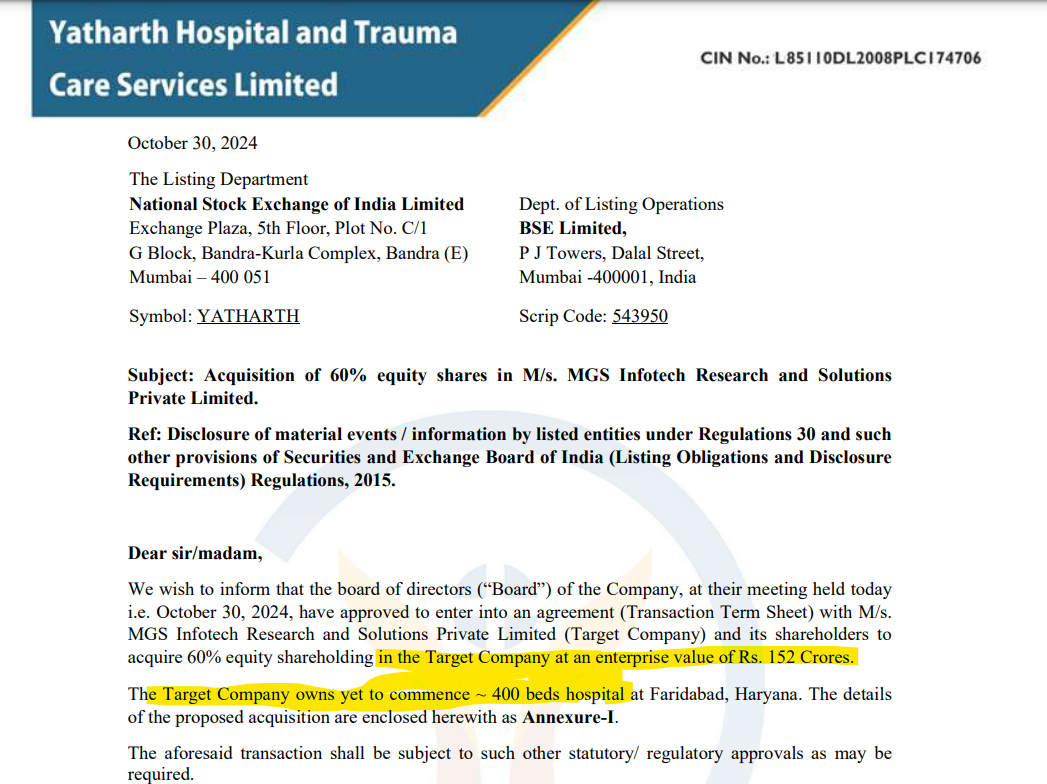

Yatharth Hospital acquires super specialty hospital based out of Model Town, New Delhi. The hospital has an expandable capacity of 300 plus beds and caters

to a large catchment of residential and institutional client base

was this a good time to increase fixed cost by acquiring two hospitals? I mean when you already have two recently acquired hospitals (jhansi & faridabad) shouldn’t they focus on the occupancy of these two first and maybe also improve ARPOB especially in jhansi,they should have taken some time and let these two operate with good occupancy and then looked for new accusation especially when you have majority of revenue coming from Govt schemes and you already have CFO negative for the last year. Because the target of 2800beds is for FY28 and also 450beds can be extended in noida itself they had time to take things slowly and improve the operating cash flows and bring debtors day further down. Disc:- Invested

That is fair criticism, however, there is enough cash on the balance sheet for them to actually acquire. One may argue that these might have been good deals and they did not want to miss them. Also if you compare Yatharth expansion plans to others, one thing in their favour is that these are brownfield for the Noida hospitals so that also reduces execution risk. In addition, NCR is one of the most deprived areas in terms of hospitals so it is seeing interest from a lot of players. I think Yatharth wants to have dominance in the region before others jump in as this will allow them to establish the brand name and patient loyalty. If they do anything more than this I would share your concern.

That is still yet to happen of 450 beds 200 & 250.

Apart from that yeah they had cash and one acquisition was already expected but another one was kinda surprise that too with additional 100cr to be spent more for the facilities and all

Its fine… their annual EBITDA is going to be roughly 230crs for FY25. Assuming a 60% cash conversion, that comes out to be ~140crs. On top of it they have around 80-100crs on balance sheet? They can go aggressive while continuing to grow the existing hospitals which don’t need a lot of capital investments.