Q4 2024 Yatharth Hospital conference call

Robotic surgery are integrated seamlessly.

One of big 6 audit firm will be appointed as auditors.

Case mix shift to specialty treatment will lead to ARPOB growth.

Upcoming Jewar Airport in Noida ( planned to be largest in Asia) will help to draw international patients. Set up dedicated marketing professional to attract international patience. Dedicated floor and lounge under renovation. 150 kidney transfer in 1.5 years, 90% are international. They will contribute to double digit in overall revenue.

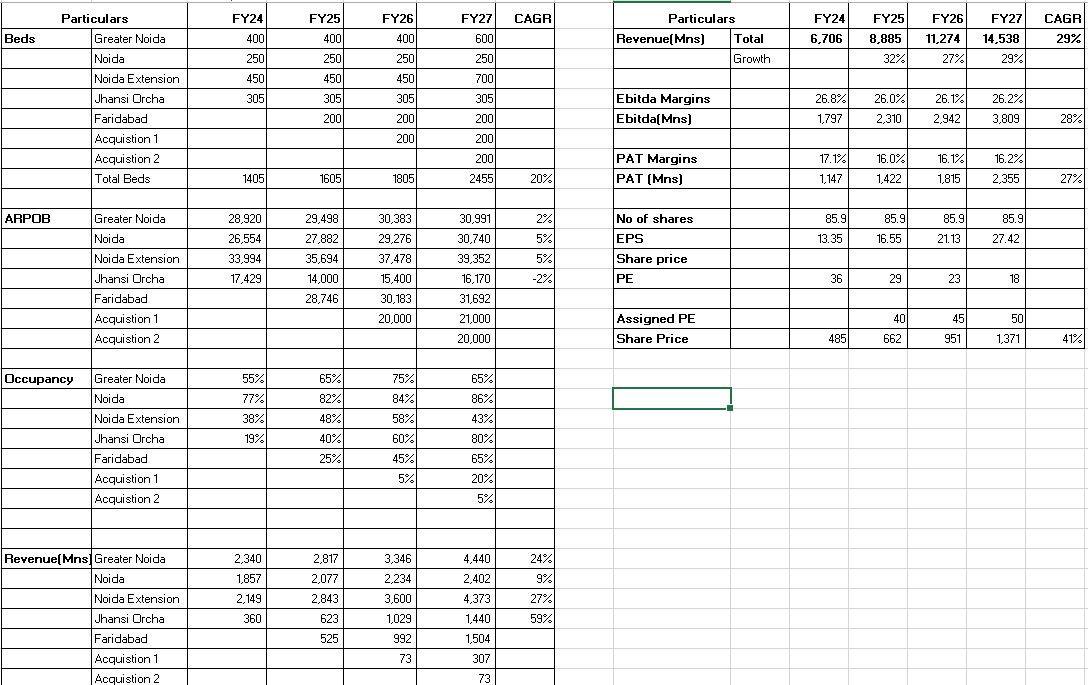

Industry leading growth in profitability and revenue.

Confident of maintain revenue and EBIDTA growth 29% and 35% in upcoming years.

Payer mix not in focus. Focus on increasing ARPOB.

Govt rates are 20 to 25% rates are lesser then govt. business. For oncology govt rates are not such big, it is less.

Govt business will come down due to international patience ramp up.

Annual rate hike is 6 to 8% rate hike for cash. For insurance it is one to one negotiation with insurance companies and it is for 2 years for govt insurance, for private depends on 1 to 2 years.

International Patients:

Upcoming Jewar Airport in Noida ( planned to be largest in Asia) will help to draw international patients. Set up dedicated marketing professional to attract international patience. Dedicated floor and lounge under renovation. 150 kidney transfer in 1.5 years, 90% are international. They will contribute to double digit in overall revenue.

Jhansi Hospital:

Jhansi Hospital at 34% Occupancy in Q42024.

ARPOB decreased due to government business. It will be in increasing trend in upcoming years.

Faridabad Hospital:

Waiting for two machines then cardiac department will be running.

Occupancy can be much earlier then Jhansi in terms of occupancy.

Expansion Strategy:

Organic and in organic.

Asian Fidelis Hospital renamed as Yatharth Hospital and start commercial operation from 12 May 2024. 116cr to buy and 34 cr for machinery. Little capex is pending, should be ramp up very well. Faridabad is huge potential.

One hospital to acquire each year from FY24 to FY26. It will be mix of internal accruals and debt. Company will be still net debt free.

It will be primarily in North India. CAPEX of 60 to 70 lacs per bed similar to Asian Fidelis hospital.

Receivables:

Increase in Govt. Business. Now it is 40%. May be due to election or Q4, will be normalized soon. Q1 will have significant reduction in debtors.

Coming two quarters will see drop in receivables.

Income tax:

Oct 2023 as filed, money is still with company for 76 cr. Expect in this FY money will be back to company. It do not affect working capital. Investigation do not found suspicious, it is frozen as per procedure.

Concall Transcript:

In nutshell, If company demonstrate revenue growth with considerable improvement in receivable will be positive.

D: Invested