hi @chikspat - thanks for the detailed analysis - have gone through your posts on Yatharth - quite detailed, do you consider it attractive at given valuations - isnt 3x growth guidance in 3 years quite aggressive too?

1 Like

Hello Deep_Mehta1,

Management guided for 30% CAGR for revenue. Which we shall monitor.

For operating leverage, there are room of improvement due to complex procedures, radiation therapy, CGHS rate revision, Noida airport opening, which may bring more international patience.

Valuation still compared to peers are reasonable. Once company get scale, higher valuation, brand building can help to have higher valuation.

Disclosure: Invested.

2 Likes

Yes on the operating leverage clearly there is room for improvement of ARPB which should improve with the facilities you mentioned, so this combined with top line execution should be something to clearly look out for. Got it.

On the valuation front also - checked peers like global health and they trade at 38x EV/EBITDA and Yatharth at 28x.

Thanks once again for taking out the time to respond with a detailed outlook@chikspat Dharmesh bhai.

1 Like

CRISIL has upgraded company’s rating from from A- stable to A stable which is 2nd upgrade in last 2 years, overall sentimentally positive..

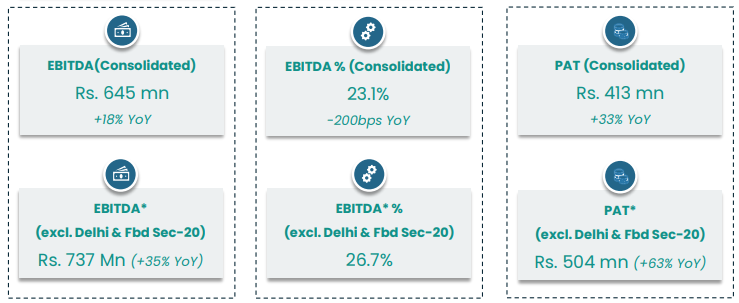

Good results by Yatharth, for this quarter I focus more on EBITDA excl. delhi & faridabad hospital as they are recently started.

Other highlights for the quarter are as follows:

To add to it, The Company received a favorable order on the pending Income Tax matter, releasing the provisional attachment of all its properties and Fixed Deposits, marking a significant step toward the long-standing Income Tax issue

1 Like

Yatharth Hospitals -

Q2 FY 26 results and concall highlights -

Revenues - 279 vs 217 cr, up 28 pc

EBITDA - 64 vs 54 cr, up 18 pc ( margins @ 23 vs 25 pc )

PAT - 41 vs 31 cr, up 33 pc ( due higher other income )

Cash on books @ 370 cr

Corporate level occupancy @ 66 vs 60 pc YoY

ARPOB @ Rs 32k vs Rs 30.6k

ALOS @ 4 vs 4.3 days

IPD revenues @ 249 vs 190 cr

OPD revenues @ 30 vs 27 cr

New hospitals led the revenue growth with a YoY jump of 110 pc. Mature hospitals witnessed a revenue growth of 19 pc

Hospital wise revenue percentage split for Q2 FY 26 vs Q2 FY 25 -

Noida extension - 33 vs 37 pc

Greater Noida - 29 vs 31 pc

Noida - 19 vs 21 pc

Jhansi - 8 vs 7 pc

Greater Faridabad - 10 vs 4 pc

New Delhi - 1 vs NIL

Split of company’s total bed capacity -

Mature hospitals -

Noida - 250 beds, Occupancy @ 89 pc

Noida extension - 450 beds, Occupancy @ 64 pc

Greater Noida - 400 beds, Occupancy @ 69 pc

Jhansi - 305 beds, Occupancy @ 71 pc

New Hospitals -

Greater Faridabad - 200 beds

New Delhi ( new opening ) - 300 beds

Faridabad ( new opening ) - 400 beds

Agra ( new acquisition ) - 250 beds

Comments from previous concalls -

Greater Faridabad hospital turned net profit positive within 1 yr of its opening ( its ARPOB was Rs 31 k )

Company estimates that both Delhi and Faribabad hospitals ( 2 new openings in Q2 ) should turn PAT positive in 15 months time

Greater Noida + Noida extension - brownfield expansion should now begin ( post opening of 2 new hospitals in Delhi ). Aim to add aprox 250 beds here ( combined ) by FY 28. Greater Noida + Noida extension brownfield should cost them aprox 175 cr. This brownfield expansion should go live in H2 FY 28

Notes from Q2 concall -

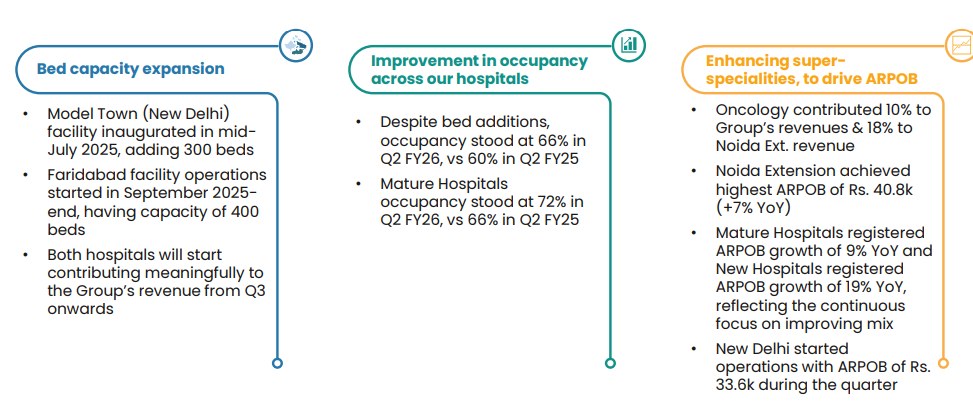

New Delhi’s hôpital went live in Jul. Faridabad hospital also went live towards the end of Q2. Both these r seeing increasing footfalls

Acquired a 250 bed Hospital ( Shantived Hospital ) in Agra for 260 cr ( all cash deal ) in Sep 25

CGHS rates have been revised wef Mid Oct - a big relief for the Industry

5 of company’s hospitals are located near Jewar International airport - should help them with medical tourism

In Q2, mature and new hospital clusters witnessed an ARPOB growth of 9 pc and 19 pc respectively

Model Town ( New Delhi ) facility started operations with ARPOB of Rs 33k - very encouraging sign. Occupancy here is already clocking 15 pc or so

Typically, occupancy required for a new hospital to break even is 30-35 pc

Agra Hospital’s financials will be consolidated with Yatharth wef 01 Jan 26

Payor mix - Govt Business @ 37 pc. Rest is equally divided between self pay and Insurance

Doctor’s salaries + Incentives as a percentage of revenues stand @ 21 pc

Jhansi Hospital is now clocking a very healthy occupancy of 71 pc

Capex spending outlay for next 5 yrs should be around 1500 cr. This includes the latest Agra acquisition, brownfield expansions at Noida and a new Greenfield facility or another acquisition that the company may go in for

Company has started opening International catchment centers - to tap international patients ( will be opening in Central Asian and African mkts ). Have already opened at 2 locations. Noida + Faridabad’s proximity to Jhewar airport should help them tap into international patients. ARPOBs in case of international patients are generally 30-40 pc higher vs domestic patients

Agra’s hospital is expected to clock ARPOB of Rs 30k + ( to begin with )

Agra’s hospital will be EBITDA positive from Day 1. H2 EBITDA margins should be close to H1 margins. Still maintaining their 30 pc + revenue growth guidance for full FY 26

The revision in CGHS rates should incline company’s revenues by about 2.5 pc and EBITDA margins by 1 pc in next FY

For next 2-3 yrs, avg corporate ARPOB growth should be in the range of 6-8 pc / yr, with an upward bias

The brownfield expansion @ greater Noida and Noida extension should go live in 18 months time from now

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation, posted only for educational purposes

3 Likes

Sub: Disclosure under Regulation 29 (2) of SEBI (Substantial Acquisition of Shares &

Takeover) Regulations, 2011

In terms of disclosure under Regulation 29 (2) SEBI (Substantial Acquisition of Share and

Takeover) Regulations, 2011, l, Neena Tyagi, R/o Sports Villa — 17, Director Lane, Jaypee

Greens, Greater Noida-201310, hereby submitting the Disclosure under Regulation 29 (2) of

SEBI (Substantial Acquisition of Shares & Takeover) Regulations, 2011 with regards to the

disposal of 5633800 Equity shares of Yatharth Hospital & Trauma Care Services Limited on

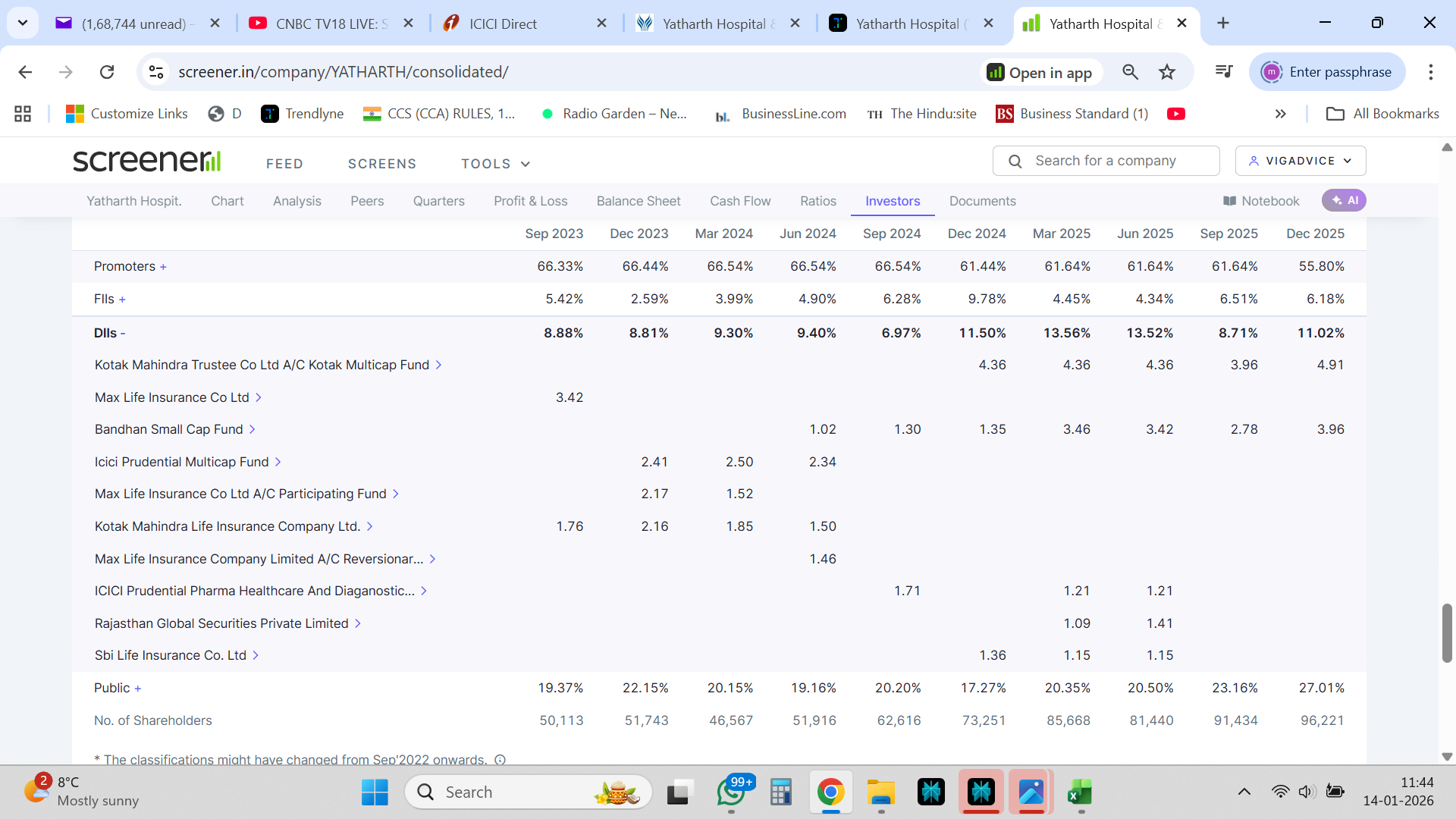

28th November, 2025 through Market Mode.. This is 5.85% of the total shareholding, what happened why Neena Tyagi from promoter groud has to sell 5% plus quantity in open market in single day due to this stock went down by 10%, any internal dispute within promoter famility?

1 Like

Think it is just offloading off some stake. Neena Tyagi (seller) is the spouse of Ajay Tyagi (Chairman) and son of Yatharth Tyagi.

Promoter sold 56.3lakhs shares

![]()

Kotak & Carnelian buying could absorb only 13.5lakhs share; rest offloaded in market?

![]()

![]()

1 Like

Why Suddenly promoter has to sell in open market at 10% lower than CMP, they could have done proper structure deal with some MFs..Immature Promoters..

how do we know who were the buyers? Definitely has to be institutions. Kotak and Carnelian Asset Management(Vikash khemani), only these 2 trades we can see on screener. But they just bought around 23% of the block. There must be some other big buyers.

2 Likes

These were the 5 buyers in bulk deal on 28 Nov. That took the price down and now it is struggling below 700 levels.

2 Likes

Nuvama starts coverage with ‘Buy’ on Yatharth Hospitals amid strong growth outlook

2 Likes

Nuvama has initiated coverage on Yatharth Hospitals with a Buy’ rating and a target price of ₹920, citing a strong growth outlook driven by aggressive bed capacity expansion and high revenue/EBITDA growth projections.

Key Highlights of the Nuvama Report

Rating and Target Price: Nuvama has initiated a ‘Buy’ rating for Yatharth Hospitals with a target price of ₹920 per share, which suggests a significant potential upside from its current market price.

Growth Projections: The report projects a robust 30% revenue and 31% EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) Compound Annual Growth Rate (CAGR) for the hospital chain over the financial years 2025–2028E.

Expansion Plans: The primary driver for this growth is the company’s aggressive bed capacity expansion strategy. Yatharth plans to nearly double its bed capacity from approximately 2,500 in FY26E to around 5,000 by FY30E through strategic acquisitions across Delhi, Faridabad, and Agra.

Operational Strategy: The company is focusing on high-end specialties like oncology and organ transplants to improve its payor mix and attract international patients, which is expected to drive a 7% growth in Average Revenue Per Occupied Bed (ARPOB).

Financial Health: Yatharth has a strong balance sheet. A robust balance sheet, with net cash of ₹370 crore and annual operating cash flow of ₹200 crore places the company in a strong position to fund its planned capex of ₹1,500 crore over the next four years.

Valuation: At the current market price, the stock is trading at around 17x FY27E EV/EBITDA, and Nuvama values it at around 20x H1FY28E EV/EBITDA, indicating an attractive valuation for investors.

Risks: Key risks mentioned in the report include the potential impact of a high government payor mix on working capital, any adverse ruling in pending tax disputes, and potential competition or slower-than-expected ramp-up of new facilities.

6 Likes

Mutual fund continues to lap up Yatharth

How do we get this data for other stocks?

Use this: Stocks held by Mutual Funds | RupeeVest

Data is available on the Screener. I think it is there on trendlyne too.

Also in Trendlyne.

Mutual Fund Dec 2025 share holdings and fund action in Yatharth Hospital.xlsx (26.0 KB)

1 Like

I’ve a slight critical view on it. Doing 1500 cr. of capex over 4 years on 200 cr. of cashflow seems a tall ask, I’d expect either dilution or debt. Did management indicate any plans?

From its last Feb’s low PE expanded 2x while EPS improved slightly; the p/e is now on contraction journey. Promoter sold signficant chunk, if they can’t hold for next 3-4 years despite visibility of the 2x capacity increase, then why expect investors to be ‘patient’?

Given the above, I’d not pay much heed to the MF and the analyst reports. On the other hand, a bargain valuation will help wether time correction and navigate possible promoter selling.

Discl. : Not invested, personal opinion, DYOR please.

9 Likes

Bumper Q3 results.

Net profit rose 49% year-on-year to ₹45.3 crore, while revenue climbed 46.3% to ₹320.4 crore. EBITDA increased 35.6% to ₹74.3 crore, though margins moderated to 23.1% from 25% a year earlier.

2 Likes