- Pakka Limited")

Who are their competitors in India and globally…

what are its competitive and Technology /R&D advantage with the Company…

Are global players not working on compostible packaging

Disclosure : Invested for last 2 years and 2% of my portfolio.

Who are their competitors in India and globally…

what are its competitive and Technology /R&D advantage with the Company…

Are global players not working on compostible packaging

Disclosure : Invested for last 2 years and 2% of my portfolio.

Found CHUK in a popular resort in Hyderabad 2 days back.

85% of the shares of promoters are pledged. This is a worrying sign. Any views from experts here who are tracking this company?

Surely this is a risky sign but think about the other side of it- a promoter pledged all of his own wealth for the business expansion. It shows the determination and confidence in his vision.

Promoter pledge can be a very good sign of a growth story as well.

Pledge is not an issue at all…and at any point of time you may get the disclosure that pledge has been released… may be even during this month also…

Product idea is amazing and I wish it is successful for the sake of the environment. But when someone talks about such a big expansion in an unknown country which is many times the size of their Indian business - it sounds very very fishy.

Disc: Exited

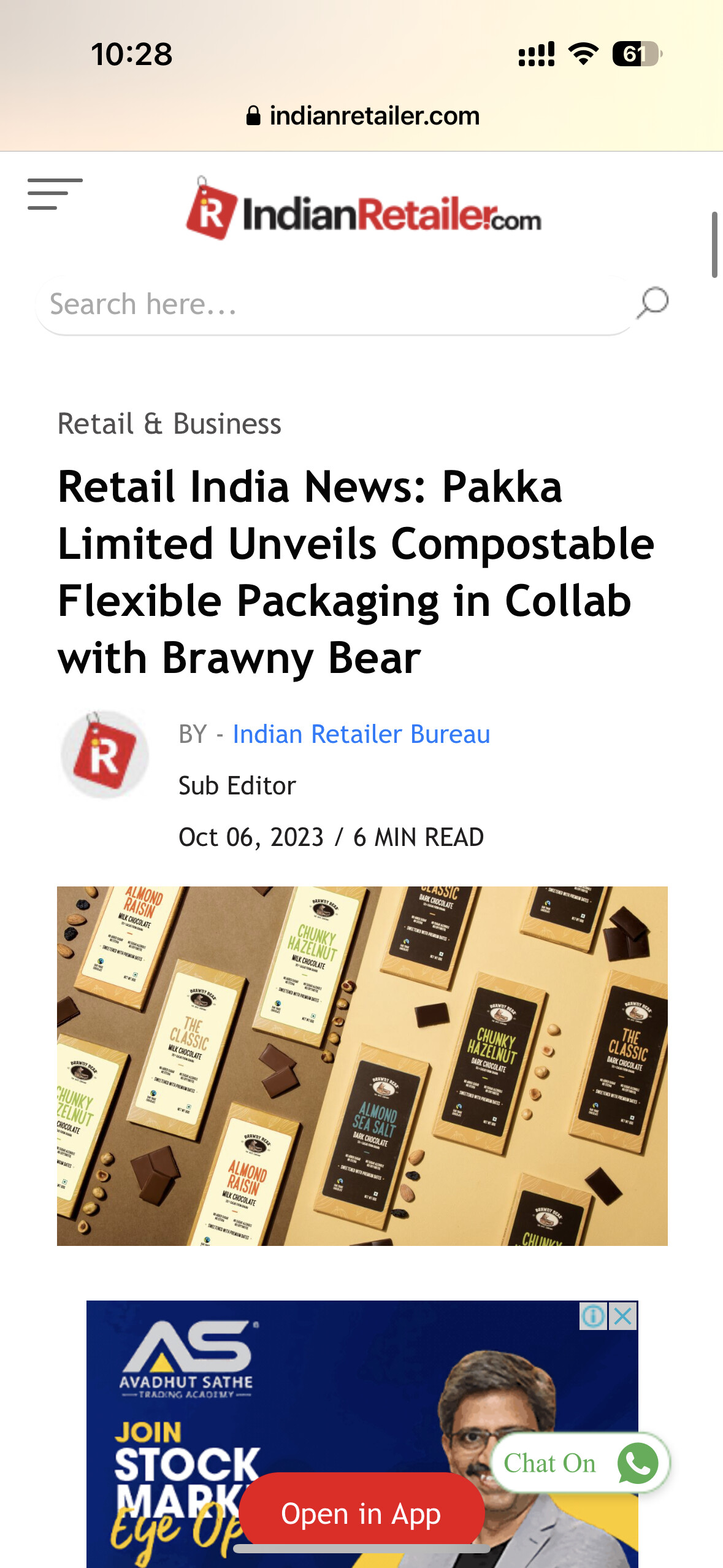

Pakka has successfully developed compostable flexible packaging for chocolates of Brawny Bear

How to drive the landed cost of Pulp and Pulp Paper ?

Any idea on deal size??

Been following it for long…story sounds good.

Execution is what I look for ![]()

Disc: Exited, might re-enter later.

85% of the revenues comes from Paper Segment and barely 15% comes from the Chuk and other products.

If we do a Sum of the parts, and assign Paper Cos valuation to Paper Biz and FMCG Revenues (I dont want to but still), then the equation works out to following.

Paper

Is operating At Peak margins — > We can assign 4-5 times EV-EBITDA to this stream , because thats what West Coast, JK Paper etc are getting.

So the 80 Crore of PBT in FY 23 translates to approx 90 Crore EBITDA.

Thus getting a valuation of 350-400 Crore of EV EBITDA. Lets assign the Debt to Paper Biz, so we are left with Market Cap of 250-300 Crore to Paper Biz

Chuk and Other Stuff

The market is then assigning 800 Crore Approx to Chuk biz for a sales of ~60 Crore in FY23 and loss making proposition

Yes it is a unique product but at what valuations ?

Yes, I sold my position today for the same reason. On the other hand, the argument on the opposite side is that the paper business maintains a relatively stable operating margin due to long-term contracts with their clients and their niche product offerings. If they carry out the 500 crore capital expenditure it is expected to result in substantial earnings growth in FY26."

Just curious why paper gets that level of multiples. Is there cyclicality in paper business, fragmented market due to unorganised players with no value differential?

When is the concall??

Not updated as of now…

Pakka Q2 concall -

Eduardo Estrada joins Pakka USA as CEO

Did anyone visited their factory on Investors Day (18th December)?

Looking forward for visit notes.

What is the status of pledged shares?