yes that is the reason why the market is giving them low valuation .Let see hopefully things will change from here onwards

1 Like

Who is doing the contract manufacturing for Chuck near Bangalore which they had announced last year? They have actually not tied up with ANYONE as yet. Scuttlebutt reveals trials after trials at different facilities around the country for contract work but nothing seems to work. Company has lied about the tie up for contract manufacturing near Bangalore.

1 Like

In the concall …they mentioned that they tried the vendor in Bangalore but eventually it dint work out so they stopped exploring further.

I agree lots of trials…but then I don’t expect too much from a company of that scale.

Their resources , their might is limited …they are expanding their horizons. They are taking that leap of faith to expand more than 100% of their current capacity.

To me it would be more prudent to watch out that in which direction they are moving. Certainly they are venturing into something new and lots of trails and rework is expected. Very difficult to get it right in first few shots…

They are learning and evolving…But imagine down the line what scope that learning offers…the end result a product in market…revolutionary…and it has huge demand.

ESG theme…every company wants to do something environment friendly…They can impact/change the packaging story big time.

3 Likes

They had come out with such packaging paper in 2019. Please refer to my post earlier in this thread. Link attached for easy reference.

At that time also, it was told that they are targetting to use for packaging etc and had sent to Biggies like Nestle and HUL for testing which might take 6-12 months. But nothing happened in last 3-4 years, obviously covid was there. But still took a real long time.

4 Likes

Which big chain uses their products at a large scale?

I order atleast 8-10 meals from Zomato every week, from various restaurants. I’ve never seen anything being delivered in a Chuk plate, EVER!

The photo I posted is from a small eatery near my home in Bangalore.

Despite all the noise for last 5-6 yrs, they have not managed to get even hlaf decent volumes on molded products, forget about their target numbers.

Bottomline is, product is not good enough and won’t get traction till they come up with one

2 Likes

I live in Gurgaon.

Experienced their products in Chai Point and Haldirams , both outlets in Worldmark Sector 65 Gurgaon.

Dont forget their background…they have evolved from near a bankruptcy…to testing most innovative packaging material(shampoo /chocolate sachets) .

Image Copied from Twitter

4 Likes

How did you find the quality of their product… Why they are not able to scale up Capacity utilisation for CHUK when demand is there…

Why all the paper stock give 52 week high break out including seshasayee , west coast , Andhra paper , what is the main reason or its just a bull market run up

Overall the global pulp cycle which was expected to have bottomed out and now reversed that is one major reason why stocks have started moving up. So say 470-500$ /tonne of global pulp has now moved to 550$. All paper mills have started revising the prices upwards. Also, they were very cheaply valued. Obviously bull market is also a reason.

1 Like

I find the product to be okay.

It needs to be noted that there are many similar type of products available in the market.

Not only they are under utilised but they are also expanding capacity with the third party vendors.

Like I can recall from conversation…there are some clients who ask the first question…

Can you service this huge demand?

So from that perspective…they are making themselves ready to take it to large scale that even the huge orders can be serviced.

They mentioned they are supplying cutlery in Mata Vaishno Devi shrine board and are in talks with ISKON as well.

Though they may even earn less from these but imagine brand building that happens in such cases.

Now that they are confident on the Product output after lots of work-reqork-improvement cycle…I am hoping in next quarter they will pick up volumes as well.

In this quarter Chuk should turn profitable.

More than Chuk, their revolutionary products on packaging will drive margins and volumes higher

2 Likes

Pakka ltd Annual report Highlights

408Cr revenue in FY23,94Cr EBITDA and 51Cr PAT.

76% of the revenue from domestic and rest export.

74% of revenue from paper,13% from pulp and 13% from compostable.

For people who are new to the company, in next 4-5 years Pakka ltd is taking on a huge capacity expansion in Ayodhya and Guatemala location. Turnover potential from Ayodhya after expansion will be 200 USD Million (2026-27) and from Guatemala (2027-28) will be 400 USD million. For a company with annual revenue of 500 USD Million (2022-23), this is quite ambitious ![]() .

.

Company will spend 575cr in Capex at Ayodhya site. Pakka ltd has incoporated a subsidary in USA Pakka inc, this company will raise funding for Guatemala project through equity and Debt. Parent company Equity won’t be diluted for Guatemala capacity. Main purpose of this expansion is to enter flexible packaging solutions (Wrappers/tubes used for FMCG products like chocolate and shampoo). Company will also expand existing business in paper/pulp/compostable.

Given the scale of capital expenditure company plans to spend there is substantial risk involved here. If this capex went wrong, it will strain the company balance sheet for a very long time. Company management has spend a lot of pages in this year annual report explaining the rationale/confidence in this project.

I will summarise the main talking points from board/management in next post.

3 Likes

Coversation with “PAKKA” leaders

summary of the main talking points from board/management.

Ved Krishna, Non exdcutive vice chairman:

Focus is to achieve global scale with bagasse (sugarcane residue) and create three solutions.

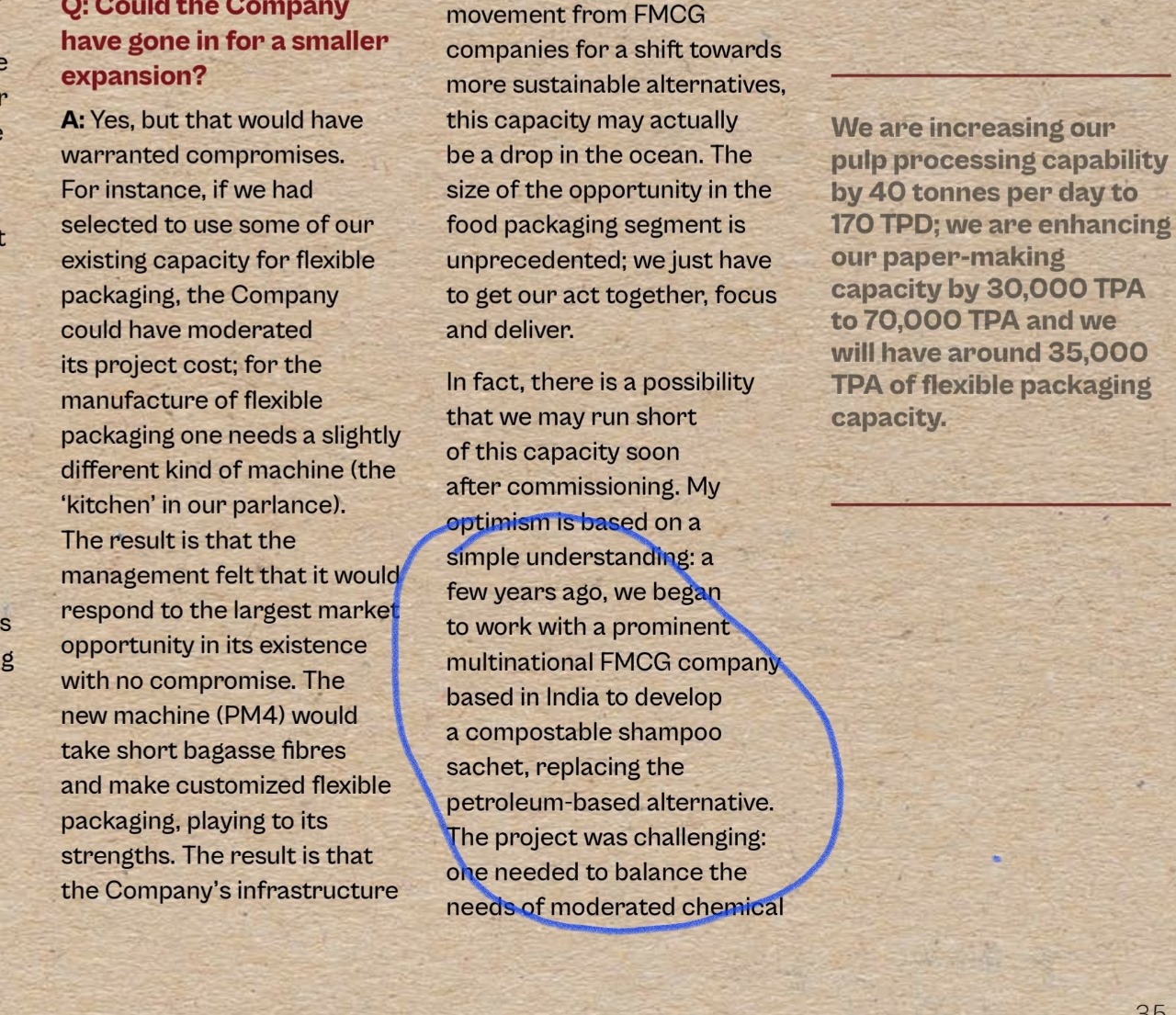

We created breakthroughs in compostable, flexible packaging substrates and it is time to take the leap of faith to commercialize our offerings. The expansion was necessary given the fact that the Company had already reached around 94 percent capacity utilization during the year.

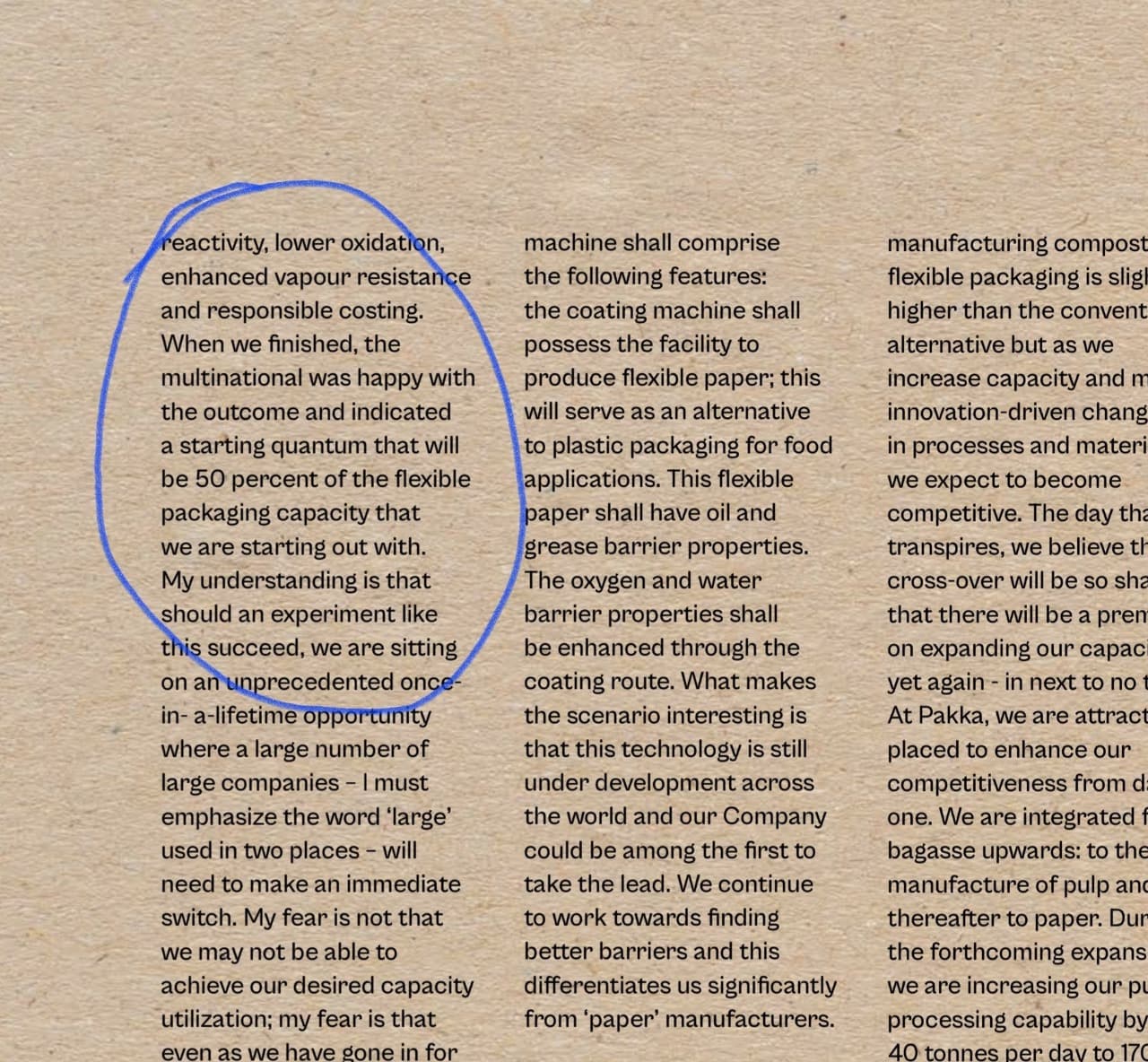

I must communicate that the cost of manufacturing compostable flexible packaging is slightly higher than the conventional alternative but as we increase capacity and make innovation-driven changes in processes and materials, we expect to become competitive. Besides, if we sell bagasse-based paper today we address realizations of around USD 1000 a tonne but if we manufacture bagasse based flexible packaging, the starting realization pay would be around USD 3000 a tonne. The delta available to us, combined with our installed capacity, should translate into an adequate re-investable surplus that kickstarts growth that is profitable and sustainable.

Jagdeep Hira, Buiseness head paper & pulp:

last year Following increased instrumentation investment, the quality of bagasse pulp improved and is widely recognized as the best in India. In the manufacture of paper, grammage and moisture variations across different batches of the same product declined nearly 80 percent; the result is that there was a sharp reduction in quality issues at the customer’s end from the second half of the last year. For compostable, capacity utilization improved to 52 percent in FY 2022-23 and is expected to improve to more than 65 percent in the current financial year. This business was under preforming last few years, expected to improve in future,

Satish Chamy Velumani, Head of compostable division:

Challenge is the cost of petrochemical based packaging enjoys large economies of scale and will always be cheaper – by a third as a quick estimate - than agro-based packaging. But the overall cost of the compostable packaging, despite being relatively expensive, would still account for a nominal share of the overall meal being ordered.

There are some other positive attributes that we have built: our brand (CHUCK) is national; the brown colour of our cutlery sends out a message of naturalness; the shape of our compostable tableware is proving to be a differentiator in a me-too marketplace.

During the current year, we expect to double revenues once again (a trend we expect to sustain for the next few years, making ours the fastest-growing business within the Company). This growth will be sustained through arrangements with more moulded fibre product converters, an asset-light way of growing our business. We also intend to commission two greenfield plants to service a total addressable Indian market of 2000 tonnes per day.

Neetika Suryawanshi, CFO:

The Company is attractively placed to build around a robust Balance Sheet. At the close of the year under review, the quantum of long-term debt on the Company’s books was negligible, indicating that it was virtually debt-free. The Company’s interest cover was strong, indicating an extensive comfort in meeting lender obligations. On the other hand, we possessed INR 213.48 crores in net worth as on 31st March,2023. We believe that these fundamentals will empower us to borrow affordably and adequately for our capital expansion without stretching the Balance Sheet and without compromising the prospective earnings capacity of the Company.

Disclaimer: Invested and biased

3 Likes

Agree with you, on the top of this:

- Company’s model can be replicated, weak moat.

- Did scuttlebutt, no evidence of chocolate wrapper being negotiated with any of food MNCs

Disc.: Invested from lower levels, planning to trim position.

4 Likes

Why has the global pulp cycle reversed? And how long do you think it will keep rising?

Hey - how did you arrange for their plant visit ? Did you directly contact the management ?

Hello,

I personally met them in their Mumbai meet by reaching out to Company Secretary.

I m sure they would be welcoming to someone wanted to visit their Ayodhya plant .

Try reaching out to CS

Thanks

1 Like

In janmashtami visited ISKON temple (mumbai) found CHUK there while “prasad” distribution.

3 Likes

Based on what I hear from the various management, this current pulp price should stabilize. The earlier prices were very low and unsustainable.

Dear Fellow Investors in Pakka,

Have a query, what would be right valuation criteria for this stock in current context?

Since traditional indicators P/E & EV/EBITDA might be misleading considering expansion plans in progress.