This is their Expansion Plan outlay from Q1FY24 presentation:

Whioe this is their Expansion Plan outlay from Q2FY24 presentation:

How come this big difference in projections just one quarter apart?

This is their Expansion Plan outlay from Q1FY24 presentation:

Whioe this is their Expansion Plan outlay from Q2FY24 presentation:

How come this big difference in projections just one quarter apart?

Finally release of share pledges happened.

I was reading about M/s Pakka Ltd., wherein I came across an instance of a merger of a company owned by the promoters into M/s Pakka Ltd. As per my analysis, the valuation given to the merged company was very generous. I request your valuable inputs.

As per AR 2022-23, the company informed that it has absorbed by merger another company, called Yash Compostables Limited (YCL). The Scheme had been approved by the Hon’ble National Company Law Tribunal, Allahabad Bench vide order dated April 18, 2022. As such, 28,38,500 Equity Shares of Face Value of Rs. 10/- each of Pakka Limited were allotted on 13.05.2022 to the Shareholders of YCL.

AR 2022-23, Page 119,

In this way, around 7.45% of the company went to YCL shareholders.

From the Merger related documents available on website of Pakka Ltd., at least 99% of the shareholders of YCL were promoters of Pakka Limited.

So, it is clear that ~7.45% of the equity holding in Pakka ltd after the merger went to the existing promoters of Pakka Ltd only.

Now, the NCLT scheme annexure gives the basis of valuation of YCL as follows: –

Pdf named ‘YPL NCLT Convened Meeting- Notice to equity shareholders, pages 123-142.

As such, the methods used to value YCL and ‘Pakka Ltd’ were ‘DCF method’ and “Market Price method”, respectively, as Pakka Ltd was already listed on exchanges.

As the DCF takes into account the future projections, following were the projections used: –

So, the revenue was projected to grow at a CAGR of `~46% from FY 2020 to FY 2023.

Similarly, PAT was projected to grow from loss of -1.3 cr to profit of 16.2 cr.

Further, the valuer says that the management of YCL has forecasted company’s earnings.

The valuer did not feel any need to question such high projections.

As a result, the Equity value of YCL was calculated as ~118 crores as on 01.06.2020, whereas it was still making loss of 1.3 crores as of 31.3.2020.

AR 2022-23, Page 249 of Pakka Ltd shows that YCL has negative Net assets as on 01.04.2020.

Now, if we compare the projected revenues of YCL with actual figures from Pakka Ltd. ARs, we see projections were indeed too high. (Although not directly comparable, but since YCL was mostly making tableware products, I am using ‘Moulded products’ revenue from Segmental reporting in Pakka Ltd.

(in cr) FY 2020-21 FY 2021-22 FY 2022-23

Projected Revenue 344 516 670

Actual Revenue 23 32 53

Total Revenue of Pakka, after merger 184 291 408

Even the total revenue of Pakka Ltd. is way less than the projected revenue of YCL alone.

Also, the Moulded products division was not able to report profits even in FY2022-23, whereas it was projected that YCL would have ~16 crores of PAT in that FY.

Based on the information discussed above, it seems to me that promoters were able to get a bigger pie of Pakka ltd by valuing the YCL at exorbitantly high valuations.

Thanks a lot brother, even though the promoters were coming out in open and declaring that we have nothing to hide and are in talks with nestle and shareholders can visit the plant and blah blah blah. I really felt something was off so avoided giving 20 p/e, although stock has done well but still i don’t think it deserves anything above 10 p/e. I myself did a little bit of scuttlebutt and found that whatever the management might claim but wholesalers are avoiding this because of inconsistent product quality. I don’t know how it might pan out but all i know is i am not giving this company anything above 10 p/e. As far as QSRs are concerned consistency is important, so that whole dream of selling to anyone and everyone falls apart, and further about flexible packaging, i think huhtamaki is doing fantastic job, cracking nestle code won’t be easy. Other than that you can expand capacities as much as you want, no one is stopping you.

I second this thought, good management first delivers quality products, here in the case of chuk they are yet to be profitable, all of their growth is delivered from their commodity paper from which the market is ready to 3-4x multiple.

If the paper cycle turns, I mean when there will be degrowth.

As per building capacity, chuk products is yet to be successful and they are already building massive capacities for idk what. If you read satia calls you will know the demand is low, pricing is also half decent, and they are running on half capacities for their molded products

PAKKA LTD RESEARCH REPORT, DOWNLOAD FROM THIS LINK.

https://drive.google.com/file/d/1D5M6mCqkNJWzRmHcoX3AGe8OLr9DhTzX/view?usp=drivesdk…

TWITTER - https://x.com/SouravKhara4/status/1759607867076690183?s=20

THIS IS JUST FOR EDUCATIONAL PURPOSE. DISCLAIMER: I AM NOT SEBI REGISTERED RESEARCH ANALYST/ ADVISOR.

Can’t seem to open this can you please post it again

PAKKA LTD PERFORMANCE NOTE FOR Q4 FY24 DOWNLOAD FROM THIS LINK.

DISCLAIMER: I AM NOT A SEBI REGISTERED RESEARCH ANALYST/ ADVISORY.

THIS REPORT IS JUST FOR EDUCATIONAL PURPOSE.

In Q4, Mr. Ved announced that they have switched their investment banker from a Latin American company to Nomura. Nomura indicated that there is no project similar to the one conceptualized by the Pakka team. Furthermore, Mr. Ved mentioned their plan to raise ₹175 crore through a Qualified Institutional Placement (QIP). However, investors wanted the pricing to be ₹250 per share, which was not feasible as the share prices had risen above ₹350. According to SEBI guidelines, the average price of the last six months must be considered. Fortunately, the share price has since decreased, and investors for the ₹175 crore QIP are ready. Once they can proceed with the placement at ₹250 per share in compliance with SEBI rules, it will happen immediately. If this does not occur, they have also filed for a rights issue at ₹250 per share as an alternative option.

The total capital expenditure for India is ₹675 crore, with an additional ₹75 crore required for equity infusion in the Gautmala project, bringing the total to ₹750 crore. The funding plan includes raising ₹675 crore through QIP, covering 20% through internal accruals, and financing the remaining amount with debt.

Raising ₹175cr at ₹250/share means issuing 70 lakh shares. With company at present having ~392 lakh shares, the dilution will be ~18%, which is too high. The promoter holding will go down from ~47% to ~40%.

Another issue is that the company having ~400 cr of sales and ~50cr yearly PAT will be taking 375cr of debt on its books. That is very risky scenario.

Yes but looking at the future prospects , sustainability is the way of life , the company will do well and the equity dilution is temporary. But when the factory in Guatemala comes in stream in mid 2025 we can see a remarkable improvement in performance. Till then the business offers a chance to buy imho.

Any comments from experts are welcome

Dicl: Invested and slowly accumulating

During the Q4 conference call, Ved clarified that there would be a moratorium period for the loan, meaning that principal repayments will begin only after the commencement of commercial production for the Jagruti project. Additionally, the interest on the debt incurred until commercial production starts is included in the project cost.

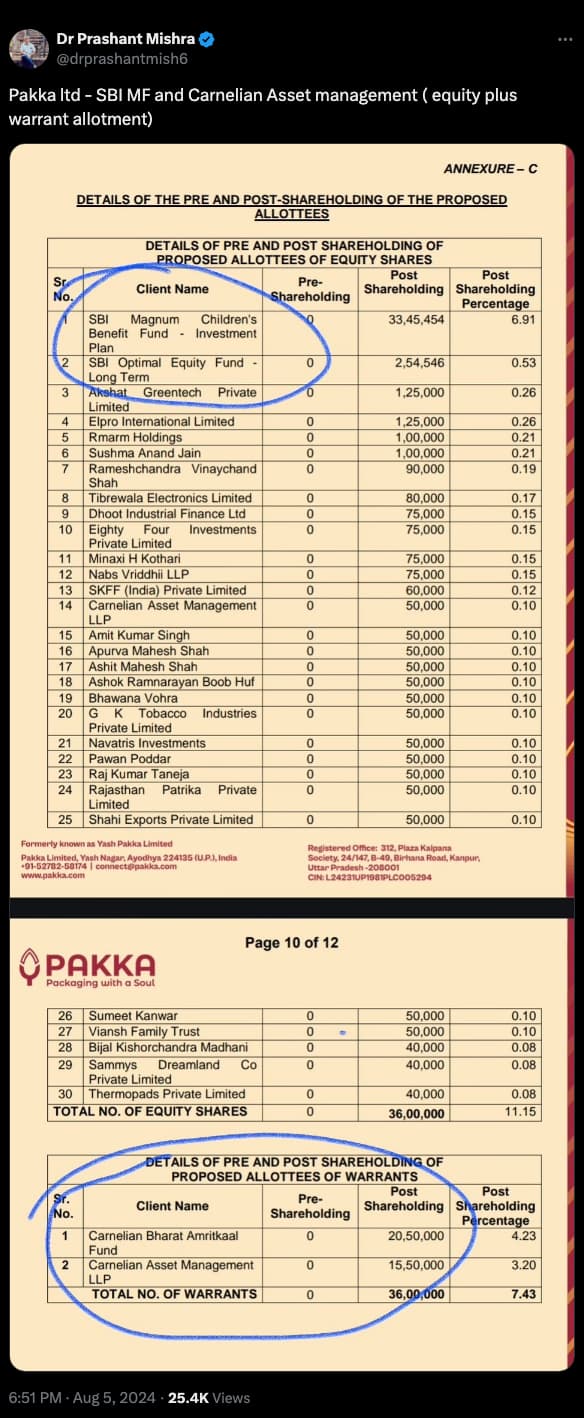

I’m just sharing this update from Twitter.

https://x.com/drprashantmish6/status/1820450083235606877

I hope this helps.

Not Invested.

dr.vikas

Full Document as shared to the exchange.

Equity + Warrant dilution of around 20% .

They have received the firepower for their expansion but equity is heavily diluted.

Another issue is the investment in their gautemala company , which is a nil revenue compnay.

Need to watch to see now if the plans materialize or not.

Disc : Invested

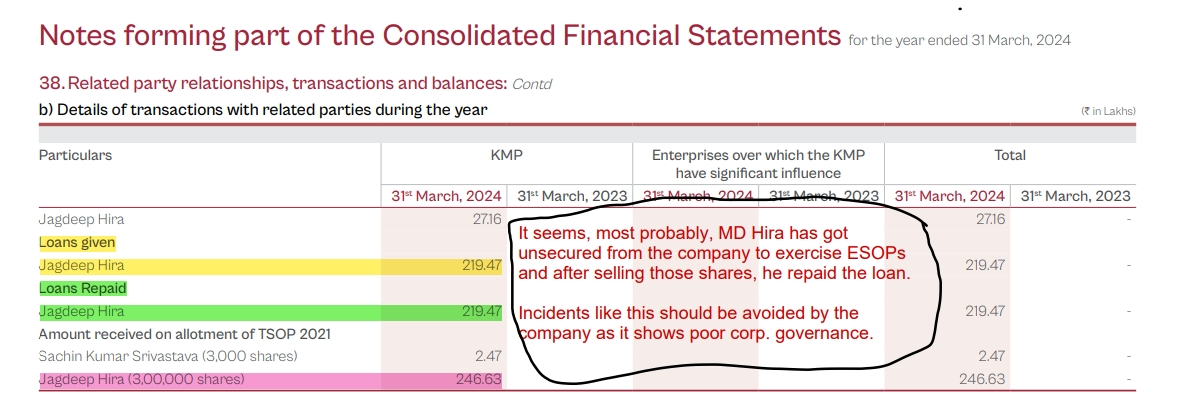

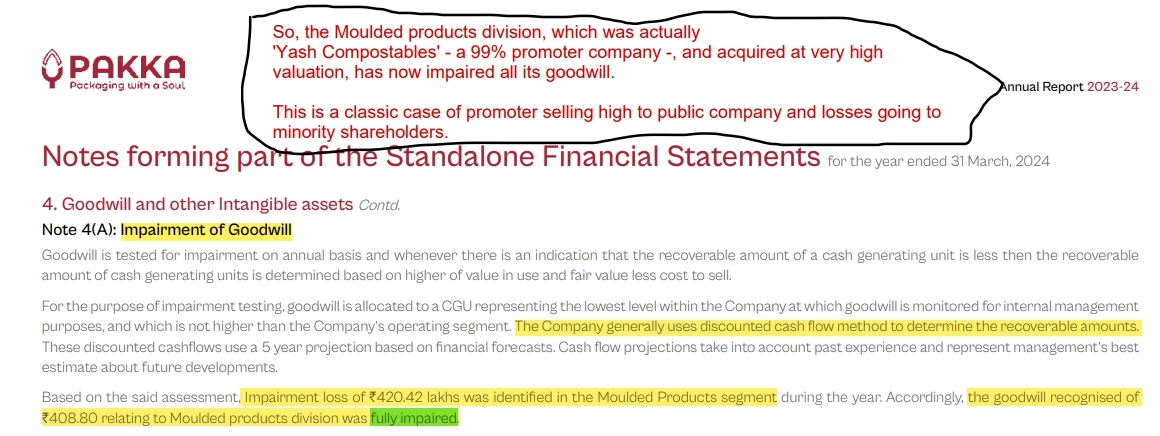

After reading the AR 2023-24, i found some aspects worth discussing, which i will be sharing in subsequent posts.