It is expected that In forward 1.5 -2 years, revenue will get double as greenfield capacity units will get live.

PAT margin % will definitely improve as greenfield capacity includes production of capacitive core which is currently being imported in India. Capacitive core is a one of the parts of RIP bushing which is more than 80% product mix of Yash Highvoltage.

Present capacity of 9,000 to 10,000 bushing, we have been able to produce 7,000 plus bushing this year. After capex, our total capacity will be moving to close to 15,000 bushings. 65% we will be able to use in the year 2026-2027 (~9750 bushings, 40% growth)

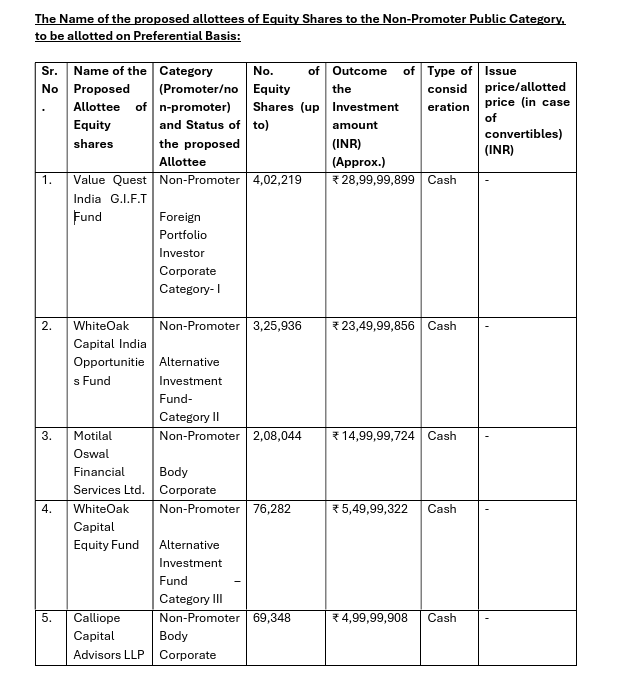

On 150 Cr fund raise, only availed the approval for now. Targeting 110 Cr for HV bushings and some working capital

Our target would be that eventually in next two to three years, we at least do 20% plus from exports.

So, Sukrut, we assume that in next four to five years, we should be able to cross at least INR150 to INR160 crores of revenue. And presently it is around INR25 crores, INR26 crores revenue financial year '26 (10% of Yash revenue)

Competition: There are three or four players in India who are putting up facility for localized RIP. Apart from us, CG Power, Hitachi India, and MIM, in Bhiwadi, Massa Izolyator Mehru, the Russian subsidiary in India. So, there are four people who are investing in the capacity for localized RIP bushings.

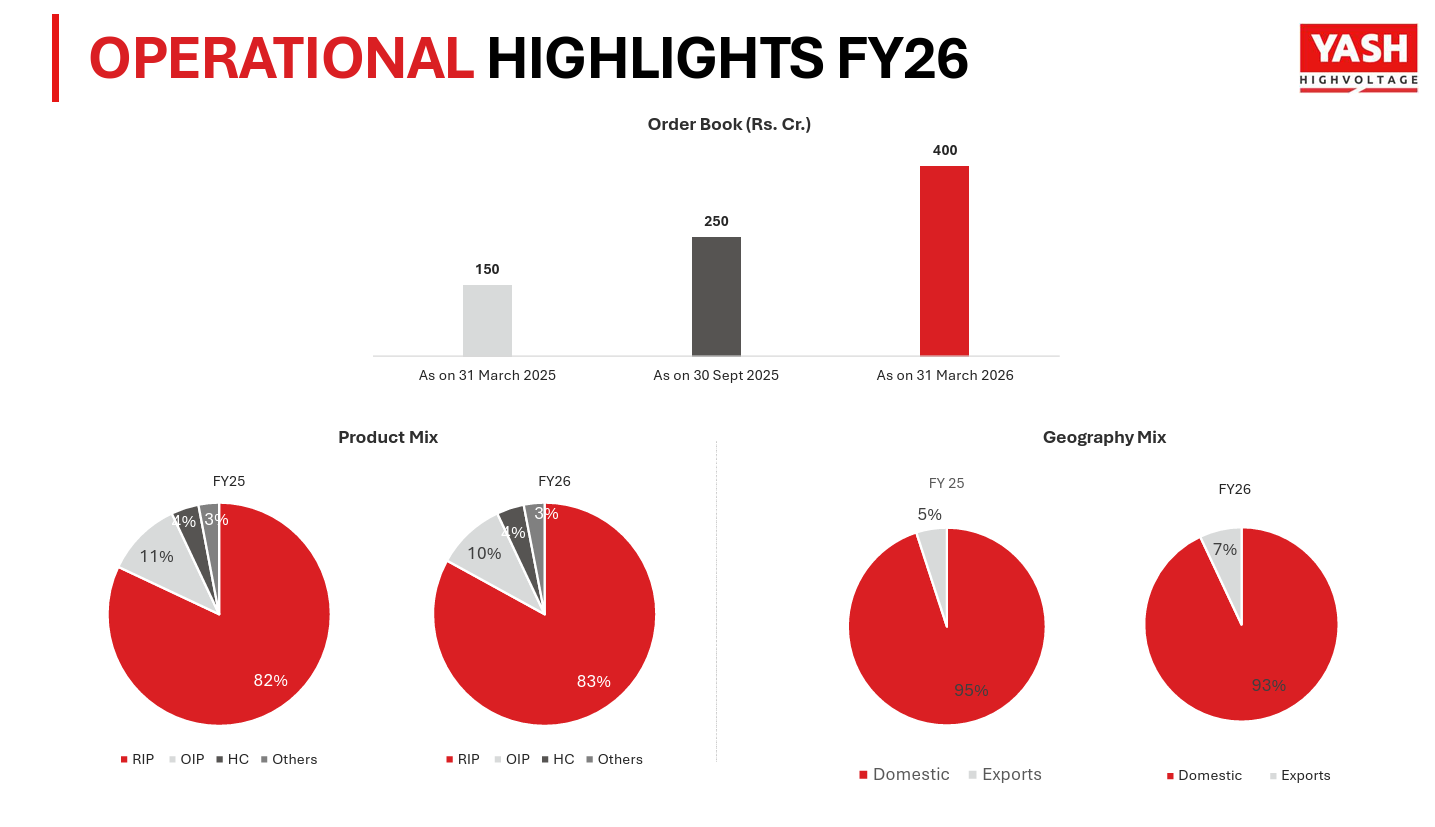

The order booking is of the almost same proportion as of what we have been invoicing. Okay. So, close to 15% to 18% is combination of OIP and high current and balance is of RIP.

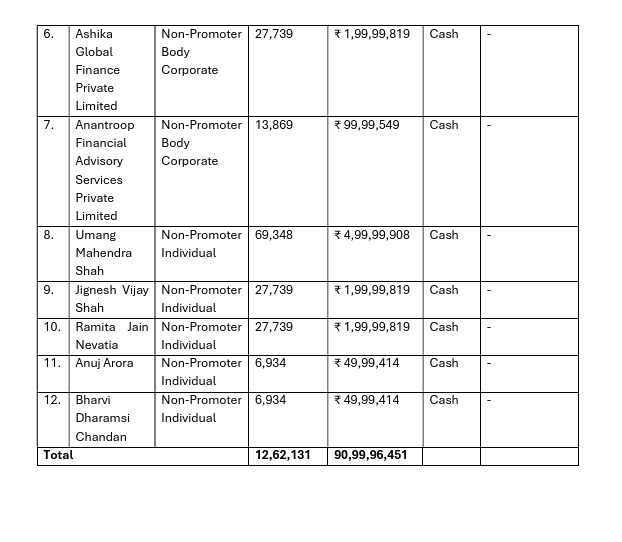

Management recently sold 1.81L shares in open market - did not see any block deals here which means shares got offloaded to retail including HNIs - but this happened just days after management giving super good guidance and con call etc

It doesn’t seems to be concerning looking at the percentage w.r.t the total shareholding. They still own large chunk. Promoters have a track record of buying their shares from open market. Promoters have personal financial lives too like taxes, diversification, real estate, whatever. None of that means they’ve turned bearish on their own business.

Although the demand for RIP bushings seems to be strong, other big players like Hitachi etc are also expanding capacity to meet the growing demand…Will it not be an issue for a small company like Yash?

If my understanding is correct, big players like Hitachi would be producing for self-consumption, not for selling to other companies. So, in my opinion, no. The broader question is would the backward integration into the in-house manufacture of bushings be carried out by more and more industry players, which may not be given that it is a small (in terms of overall % of value) component of transformers, yet very critical to their operation and needs specialised manufacturing. Check out the post of the master researcher Phreak.

Thanks for running such an active thread for this company. I recently started researching them, but I have a few questions.

According to the DRHP, the company planned to launch new indigenous dry RIP bushings up to 245kV, but now they are talking about achieving 550kV, and that too without a technical partner.

All along, I understood that this business is highly technical and acts as an entry barrier against competitors. However, with TRIL and CG Power expanding aggressively—and even Vilas Transcore Ltd. entering the space with Yash’s original co-founder.

I am left wondering: is technical complexity really the main issue here, or was it a lack of capital investment that held the company back until now? Furthermore, are they simply riding market demand, or can they truly build a first-mover advantage with scale?

Where do you get the point about not having technical collaboration. They are paying a consultant 10-12 cr and then tie up with mcg. Check Mr thakker (cfo) video commentary on ndtv.

AI generated but have validated by going through the video

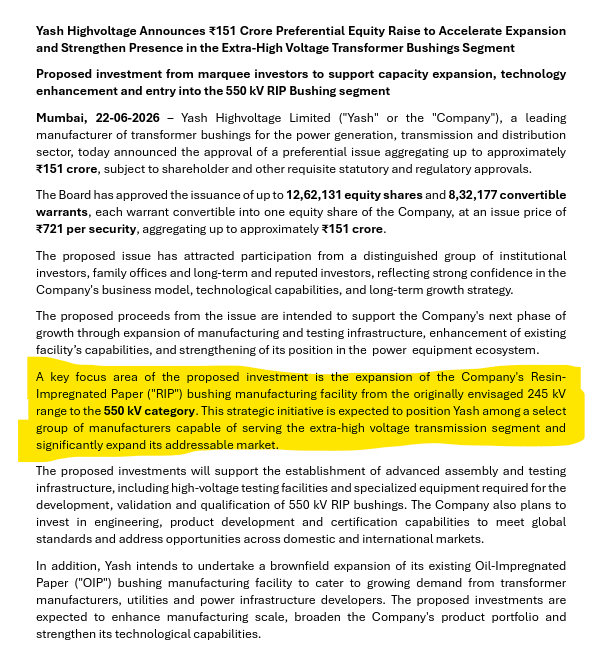

Fundraising Purpose (0:16-2:07): The company raised approximately ₹151 crore through a preferential issue. These funds are primarily earmarked for expansion into the 550 KV transformer bushing segment (a new technology area) and further development of their RIP (Resin Impregnated Paper) and OIP (Oil Impregnated Paper) product lines.

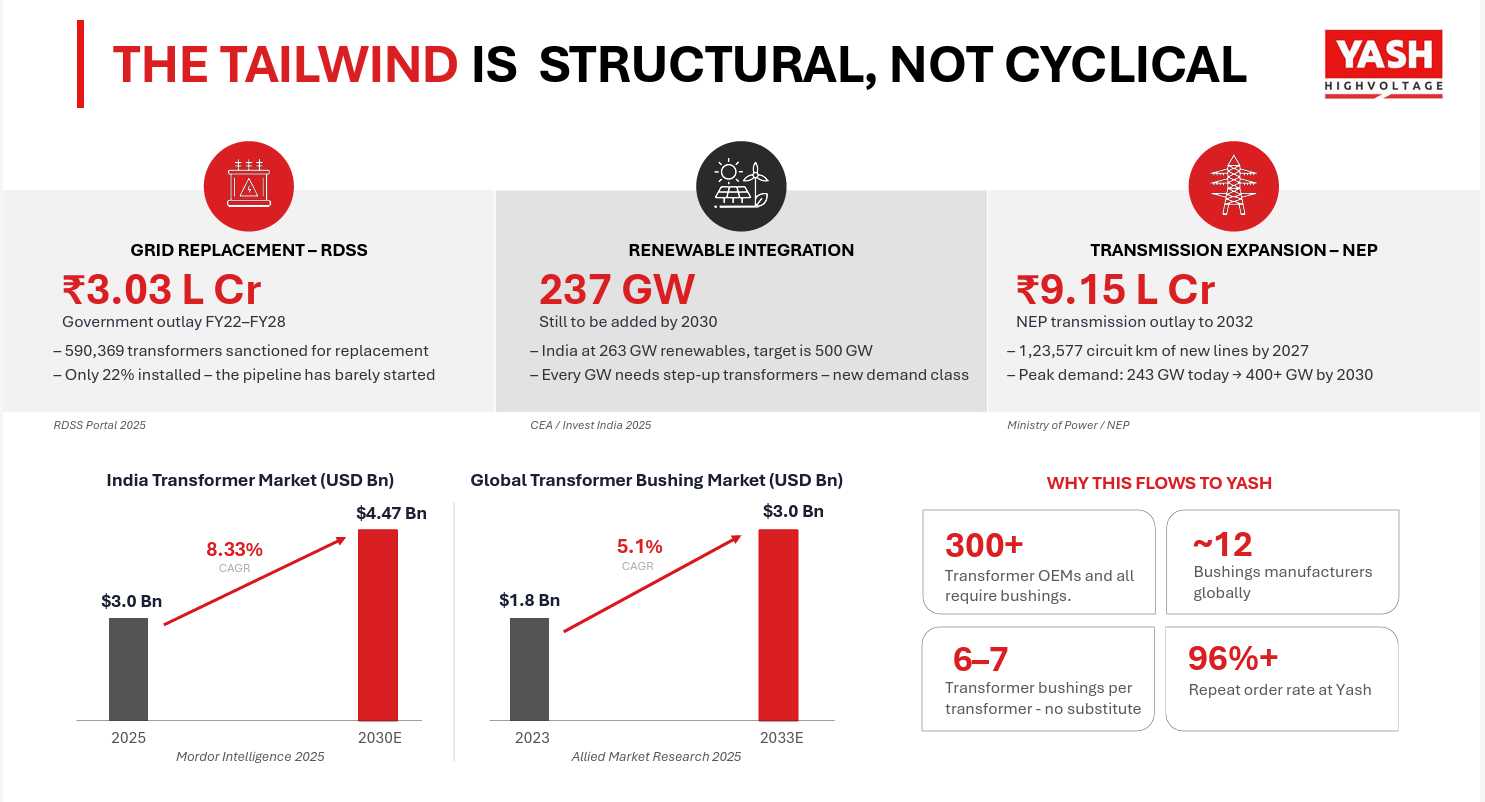

Industry Outlook (0:43-1:07): The company is capitalizing on massive tailwinds in India’s power sector, driven by unprecedented investments in transmission, renewable energy, EV infrastructure, and industrial expansion—estimated at ₹17 lakh crore over the next five to seven years.

Market Growth & Vision (4:33-5:17): Yash Highvoltage is targeting a global addressable market that is expected to grow to ₹28,000–30,000 crore over the next five years. The company aims to capture 5% market share, representing a 4x to 5x growth trajectory.

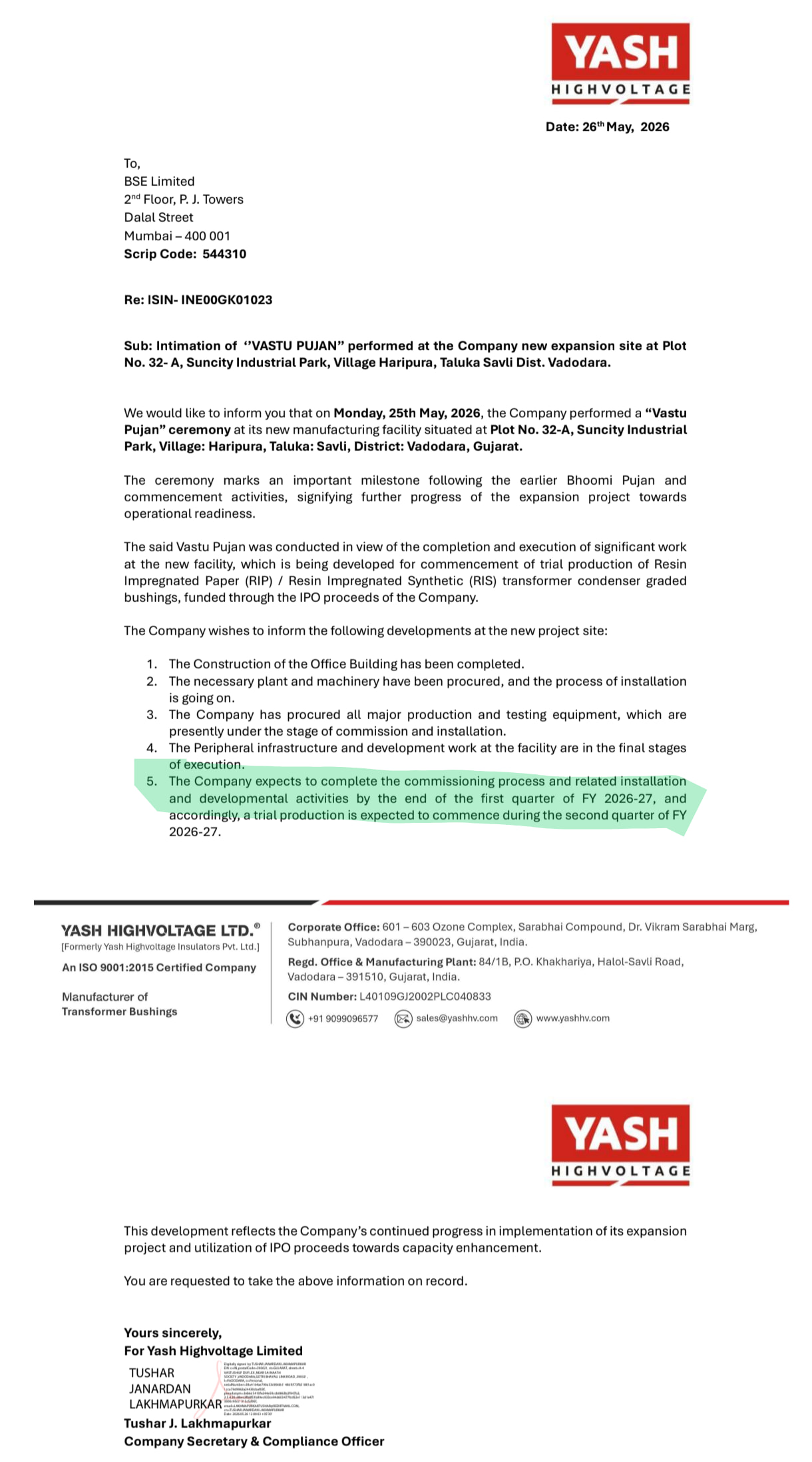

Operational Roadmap (3:46-4:10, 8:41-9:19): With the current capacity expansion and plant commissioning, the company anticipates entering commercial production for the 550 KV segment by the end of Q3. Post-expansion, they expect an installed capacity supporting a turnover of roughly ₹1,000 crore.

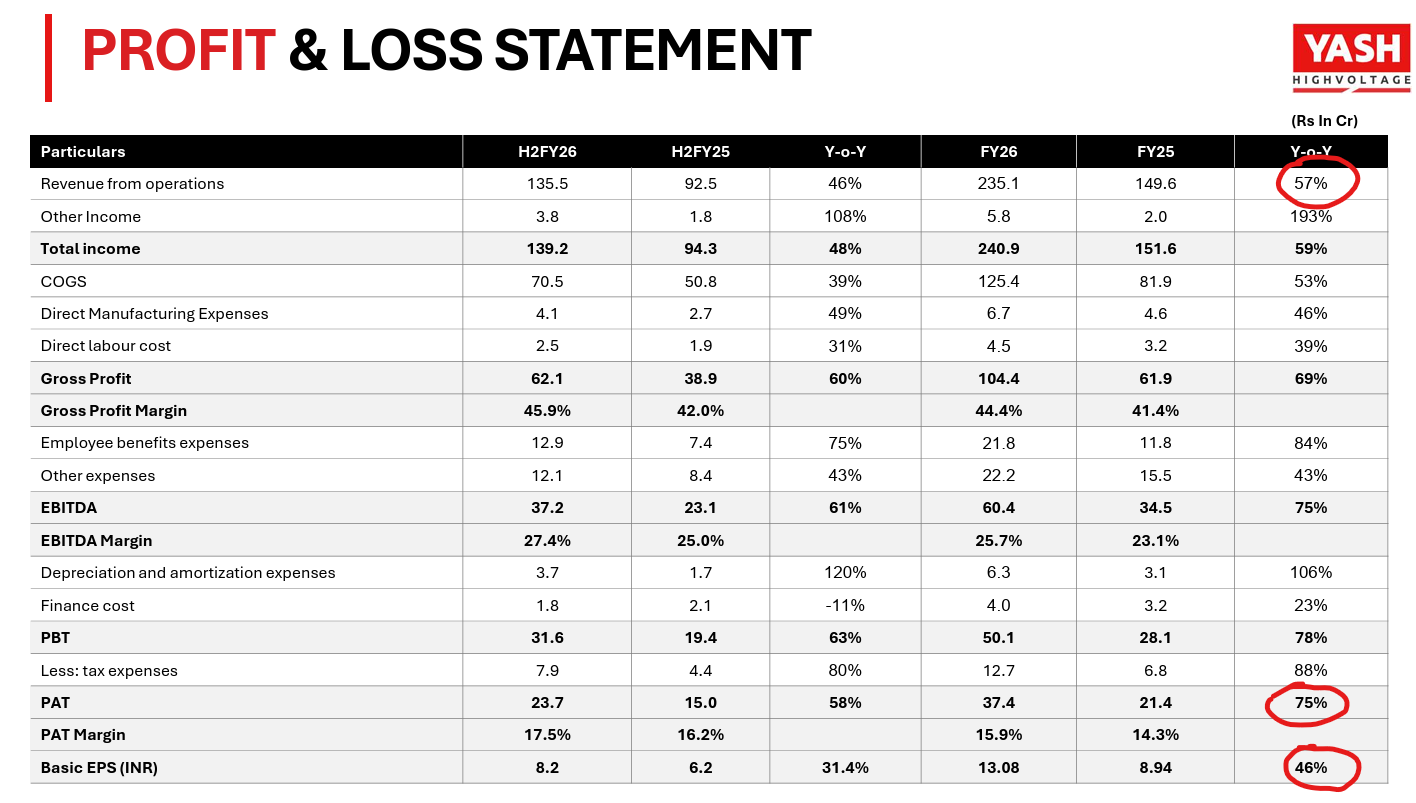

Financials & Margins (6:23-7:16, 11:02-11:22): While EBITDA margins are currently around 24%, the company expects a margin expansion of 4–5% in the next 18–24 months as they move toward indigenization of raw materials, reducing dependence on imports and lowering logistics costs.

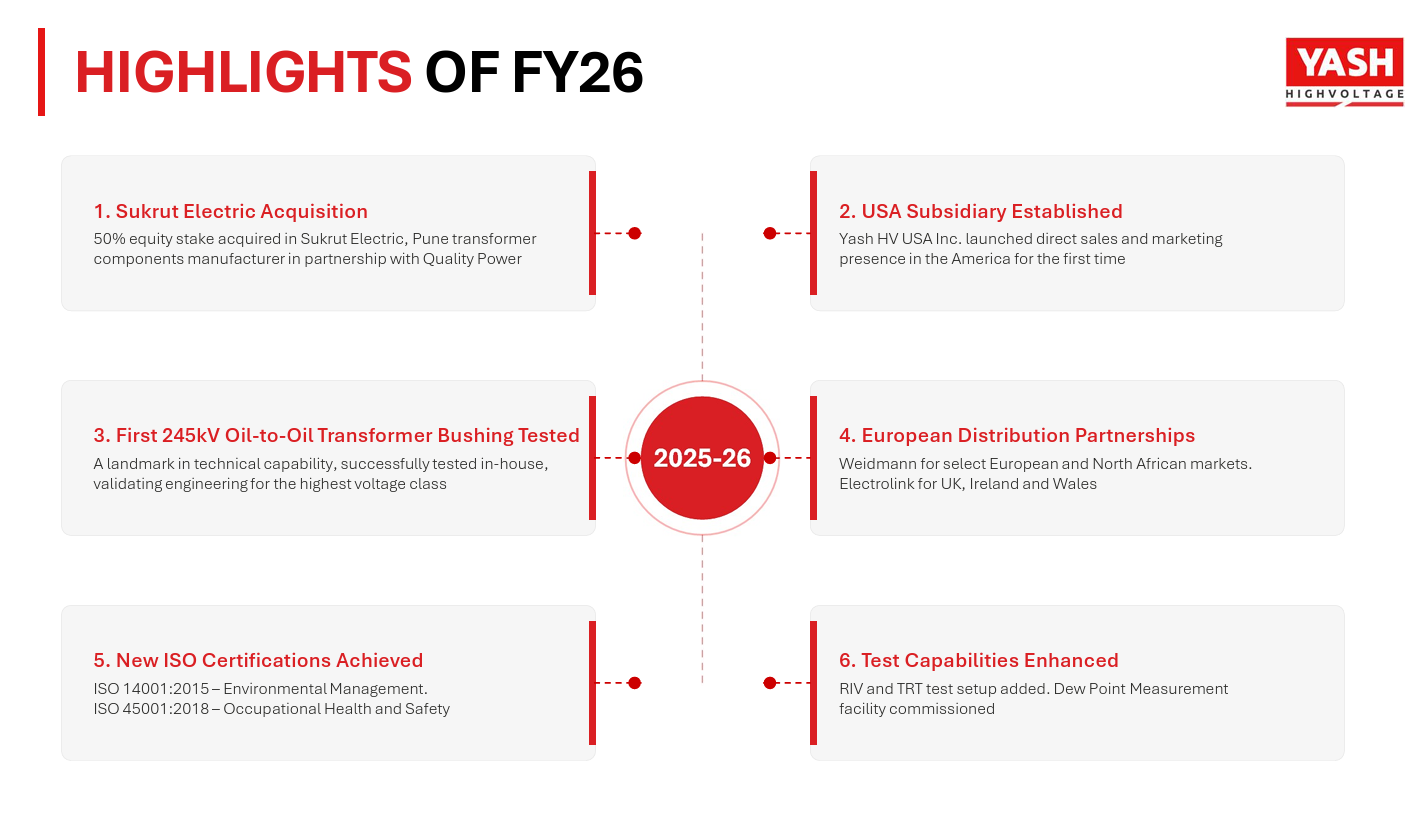

Technology Partner: To mitigate the execution risks associated with upgrading from 245 KV to the 550 KV segment, the company has officially onboarded a Swiss technology partner (7:50 - 8:02).

Some risk to be aware of:

Copper price increase might cause issue, although they pass on the increase to clients, but there’s a limit to that as well. They may also take some hit on the increase

Since moving to higher voltage is tech upgrade, they will be hiccups on the way.

Thank you for the detailed input; I appreciate it.

If I understand correctly, the key update is that the company hired a consultant. They shifted from a licensing arrangement with MGC—who previously managed the core—to developing their own core. With the consultant’s help, the company set up its own facility and acquired the necessary expertise to handle the core independently.

It seems I missed the discussion in FY25Q2, where it was noted that money was the only roadblock, which has now been resolved.

I understand that with this capital market funding, the company is now positioned to build the capability to expand its product range up to 550 kV.