Company: Yash High Voltage Ltd : Transformer Guardians

Sector: [Electric Equipment/Capital Goods]

Exchange: [BSE SME ]

Basic Details

• Market Cap: ₹1289 crores

• Issue Price: ₹146

• Current Price: ₹451 (as of 13 Dec 2025)

• Listing Date: Dec 19, 2024

Financial Highlights

• Revenue (2025): ₹150 crores

• Net Profit: ₹21 crores

• ROE: 22.6%

• Debt-to-Equity: 0.17

• Revenue Growth (3-year CAGR): 32%

Business Overview

• What they do:

Leading Indian manufacturer of critical high-voltage and high-current transformer bushings and provides retrofit services.

• Key Products/Services:

Yash specializes in two primary types of bushing technology: the traditional Oil Impregnated Paper (OIP) and the modern Resin Impregnated Paper/Synthetic (RIP/RIS). The company’s strategic pivot to the more advanced RIP/RIS technology was driven by a clear market shift, as major Indian power utilities like POWERGRID and NTPC mandated the use of modern, dry-type bushings, making the transition essential for growth.

YashHV also offers specialized retrofit solutions (OIP-to-OIP, OIP-to-RIP, etc.) for aging transformer fleets of any global make up to 245 kV and 25,000 A, providing a niche edge in the market

• Market Position:

- Overall Market Share: Currently holds an estimated market share of over 30% in India’s high-voltage bushing segment (up to 245 kV) of the Indian high voltage bushing market, which is valued around Rs 1,500 crores and is expected to grow at a CAGR of ∼6% during 2024 to 2034

- RIP Bushings: The company holds an estimated 70% market share in RIP bushings (up to the 245 kV class). Yash pioneered the localization of RIP bushing technology in India , capitalizing on the trend where premier central utilities like POWERGRID and NTPC mandated the use of RIP transformers.

- At present, company holds around 1% of the global addressable market, underscoring the immense scope for ahead growth.

- Vision for Global Leadership: The company’s vision is explicitly stated as "to be recognised among the top 5 transformer bushing manufacturers in the world

(… detail info in thesis segment)

• Key Customers:

Excerpt from concall

-

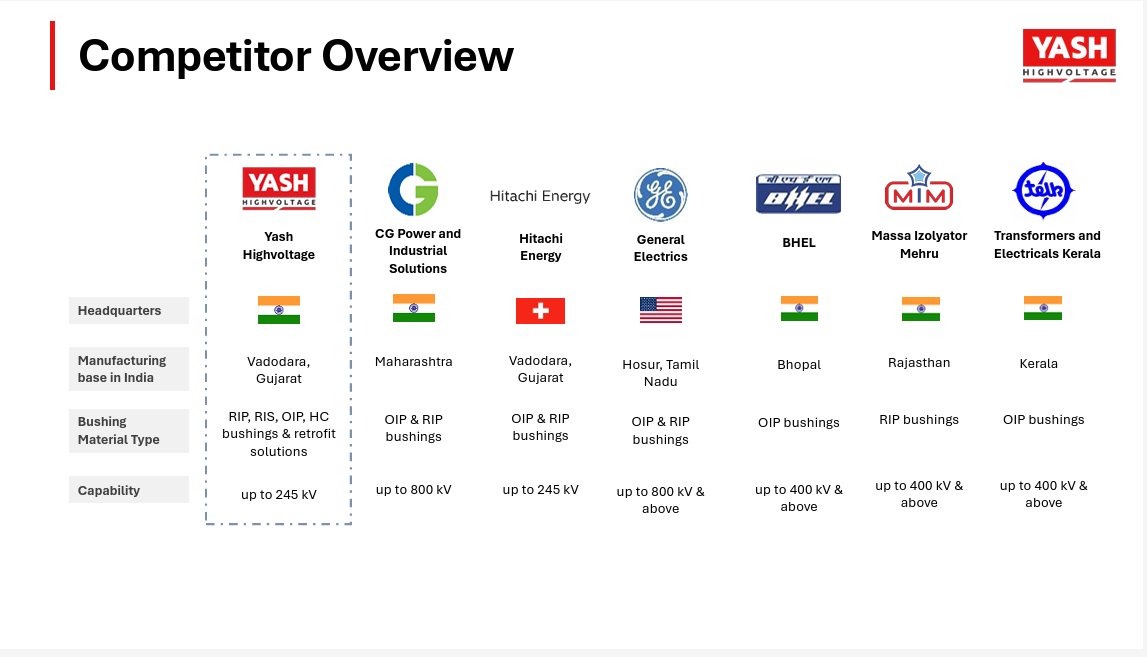

Key Competitors

-

Domestic Competitors: Crompton Greaves, Massa Izolyator Mehru , Hitachi in India

-

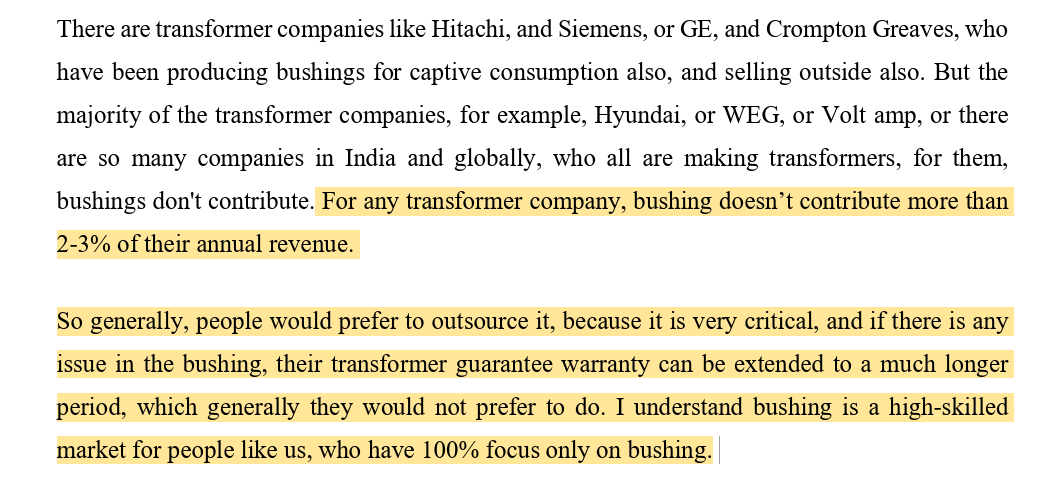

The company’s relationship with global giants like Hitachi and General Electric is nuanced. While these firms are significant market players, they primarily manufacture bushings for their in-house transformer production. Due to their own capacity constraints, they frequently purchase bushings from Yash, positioning them as both competitors and customers. This dynamic underscores Yash’s competitive cost structure and validated technical capabilities. As an Indian manufacturer, Yash enjoys a competitive pricing advantage over these global players, allowing it to capture market share while still generating strong margins.

Management Quality

• Promoter Background:

• Promoter Holding: 57.94%

• Key Management: Mr. Keyul Shah (man behind the show), a first-generation entrepreneur. Brings in the necessary high-level expertise, rather than relying solely on internal development. He engineered a significant transformation by bringing in critical technology that the company “could not have developed themselves”. He initially collaborated with the Swiss major MGC Moser Glaser to introduce and localize RIP bushing technology in India . This move was strategically timed to capitalize on market shifts away from older technology.

Investment Thesis

This is just to capture your attention. Details will follow later

Let’s get into the how of it

- Based on FY 25, export : domestic revenue split is 5:95

- RIP/RIS Conventional Bushings: 82% of revenues

- OIP Bushings:13.08% of revenues

- Exports already accounted for 40% of the company’s total sales in OIP.

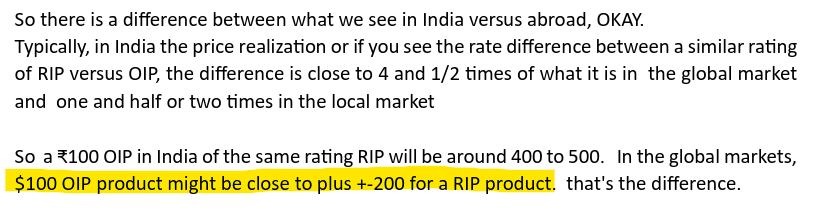

Price Comparison of RIP vs OIP bushings

Domestic: RIP is 4x that of OIP

Export: RIP is 2x or 3x that of OIP

To sum up the above points, currently company is only exporting OIP bushings which represents only 5% overall. Majority sales come from RIP (higher premium than OIP) which is only sold domestically at present. They can’t export RIP because of license restrictions.

Phase 1 (Current): Yash is currently exporting its OIP products to over 60 countries. This strategy serves to establish the Yash brand, build sales channels, and cultivate customer relationships in key international markets.

Phase 2 (Post-2026): Capex will go live by 2nd half of FY 26-27 where company will produce the RIP core domestically which is currently being imported (part of license). The company will have the right to export its high-margin RIP bushings. This will allow Yash to leverage the channels built in Phase 1 to introduce its premier products into lucrative developed markets.

To support this global push, Yash has already made key strategic moves, including the establishment of Yash HV USA Inc. to serve the Americas, and signing agency agreements with Weidmann to cover major European and North African markets, and Electrolink for the United Kingdom.

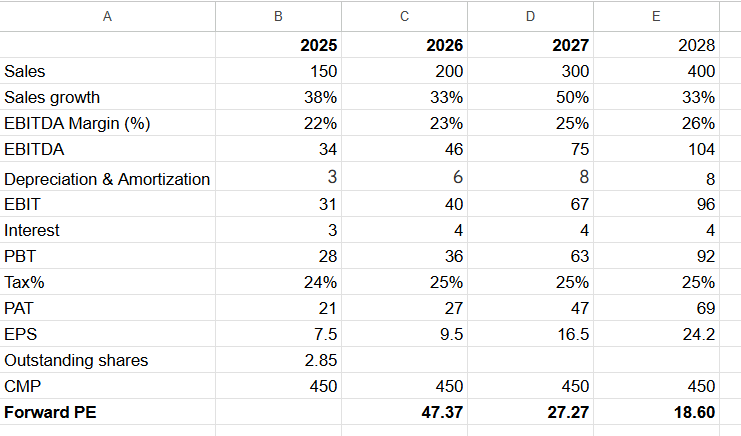

Rough Base Case Valuation

Concerns & Risks:

- Reliance on External Technology for Core Product (RIP): Till capex goes live, company still currently relies on importing RIP/RIS cores from overseas manufacturers.

- Capex delay

- Forex: The company has a significant reliance on imports for RM

- Market Competition: Its in highly competitive market.

- Transformer sector dependency: Any change in transformer sector will impact drastically.

- SME risk

Disclosures:

Invested. No transaction in past 6 months

Disclaimer

SME stocks carry higher risks due to their smaller size, limited operating history, and relaxed regulatory requirements. This analysis is for educational purposes only and should not be considered as investment advice. Always conduct your own research or consult with sebi registered financial advisors before making investment decisions.