I was following the company for some time and took a tracking position very recently. The things that I like about the company are

- Promoter integrity

The promoters have around 69.52 % stake. The company is owned by v guard group family . They are not known for any corp governance issues so far. So not expecting any nasty suprises there other than MD being away for some time as pointed out in the forum already. It seems like he is already back in the business. The company is already established a brandname and has a goodwill. Promoter holding is at 69.58 % with some recent insider buying. FIIs hold around 15.39 % stake in the company.

2)Zero debt

Even when the business is considered as asset heavy, the company has managed to payoff debt prudently and is now a debt free company. However they plan to raise some fresh debt for the proposed Chennai park. The company has been very careful while raising debt.

4)The rides in the park are known to be best in safety. An incident in any other park can also be a negative for the company in the short term. Talked to a project manager at Dubai Parks and resorts some time back and had mentioned that Wonderla may probably be the only park in India where he would be ready to get on the rides. Having said that any accident can be a severe deterrent.

5)Management’s expansion strategy

The management has a good vision on growing business and expansion. To open a new park every 3 year. But due to the land acquisition and other regulatory guidelines, this may not be possible everytime. The Chennai park has lagged a lot. Now that the construction has started, management expects the park to be completed in 18 months. And company is exempted from levy of entertainment tax for a period of 5 years from the commencement of commercial operations or from 30 th September 2021. Company is also evaluating the possibility of opening an asset light model at Orissa by raising some debt and through internal accruals. I like the idea of company going forward to open up smaller parks in Tier 2 or 3 cities. Ticket prices will be lesser than what it is now which will improve affordability.

6)Large Landbank

Company is having a very large unused landbank at all it’s parks. As per last revaluation the value of land assets is higher than the market cap.

Unused land at it various parks

Bengaluru: 42.5 acres

Kochi :64.4 acres

Hyderabad :22.5 acres

Chennai: 64 acres

The land kept idle doesnot add any additional value as many in the forum has already highlighted. The current business model they have adopted requires a lot of land. These parks needs new rides to be installed every few years to improve the visibilty. To purchase new land around developed parks once the park is operational is not going to be economically vaiable. So they have to buy a land parcel in the begining itself. Whole land cant be developed together as it will entail a lot of investment which will mean higher debt and longer period to break even. So I like the way they open the park and then develop the park slowly based on requirement and using internal accruals. I think availablity of unused land is very much essential for them to take the parks to the next level. Once there is enough footfalls company may develop the land and rent out some of the properties which will be a very source of revenue. I have seen this at Dubai Parks and resorts where they have developed the land inside the park and has rented out the same to numerous hotels and restaurants. They have already opened resorts at Bengaluru and Hyderabad.

Considering the very large population we have I believe there is very good scope for the business going forward. Company is also trying to increase sales through various promotional offers like discount to groups, students etc. Iam quite positive on the Chennai park, but the commencement may get further delayed due to the lockdown

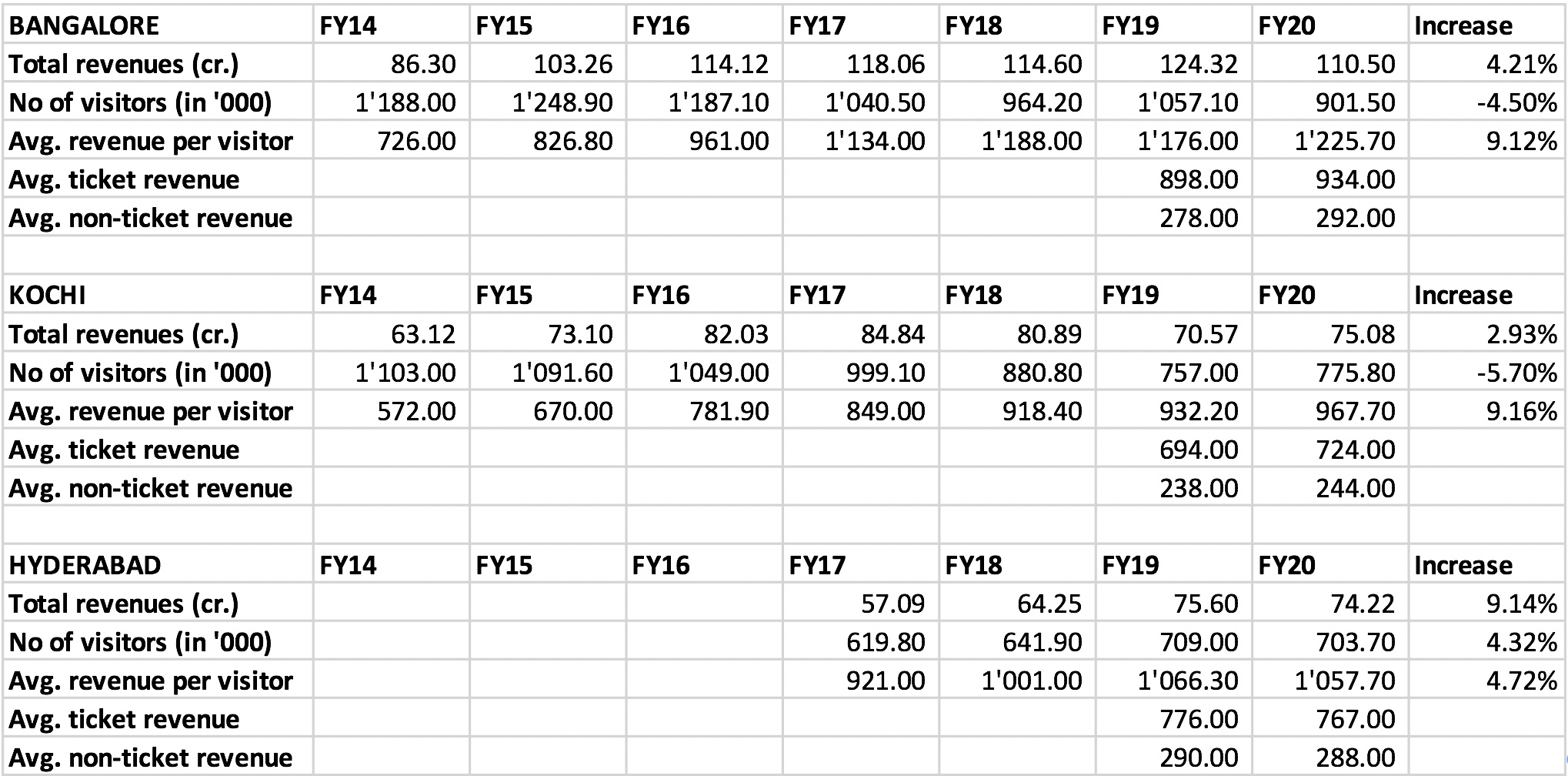

OPM is above 40 %. There is considerable increase in non ticketing revenue. One major risk cited by many is the entry of some biggy like Disney. But I believe it may take many years for Disney for land acquistion and be operational due to the many regulatory bottlenecks which is evident from the Chennai Park. Similarly Wonderla can also consider tie ups with Marvel or Lionsgate for themed rides as well as for hosting their characters. But for any large tie ups like this , I think they will need more parks and more footfalls.

ROCE goes down whenever company starts land acquisition for a new park due to large gestation period and large upfront investment required on land and machinery. Once the park starts maturing , ROCE goes on increasing due to relatively low additional capital required. I believe ROCE will start improving once Chennai Park becomes operational.

They are considering an asset light park in Orissa for the first time, so if thats successful, company may build more asset light parks from hereon. The company can hive off unused land available at the existing parks and sell them anytime they want if they dont feel that the land can’t be made to any better use at the park( company has repeatedly reiterated that they have no such intentions). With no reliable, successful business models for an amusement park to follow so far in our country , they are in the process of developing one based on models in many other countries and the business is only moving from an embryonic to growth phase.

Now with market cap at a discount to gross block the company surely looks attractive. Price is at a discount of 20% to book value and available at IPO prices.

Key risks

The current covid19 crisis will be a testing time for the company. Children being the ones mostly attracted to the parks , the company’s revenue will be considerably hit until covid 19 is totally sorted out as social distancing will not make any sense at an amusement park. We may see very muted or NIL revenue for a couple of quarters to the least.

Affordability

The ticket rates at Bengaluru park is already around 1300/*. The company may find it tough to increase the rates going forward.

Disc: invested. Around 2% of my portfolio.Views may be biased. Not a recommendation to buy or sell the company discussed