As of today, I have added 1% position in INOX Leisure which brings the cash back to zero.

Rationale:

My long term growth projections for INOX is about 15-18% over the next 5 to 7 years based on data below:

- Plan to add 830 screens to the current screen count of 574 in next 5-7 years (increase in screens: 13.6%)

- Long term ticket price increase: 4%

- Premiumization: 1-2% (based on increased contribution of F&B sales and advertising revenue)

The normalized OPM are ~14% which gives me an fair enterprise value of ~2.2 times based sales. Lets do some crystal gazing!

FY19 revenues were 1664 cr, FY20 revenues will be close to 1600 cr. (taking COVID into account), FY25 revenues at 15% CAGR ~ 3200 cr., Enterprise value ~ 7040 cr. (P/sales: 2.2, share price: 685). The current share price of 190 gives an attractive risk reward. As company is unleveraged, there is a low likelihood of bankruptcy.

Key risks:

- Rapid expansion will lead to repeated equity dilution (in my estimate the SSG ~ 12-15%, anything more than that requires dilution).

- A shift to OTT

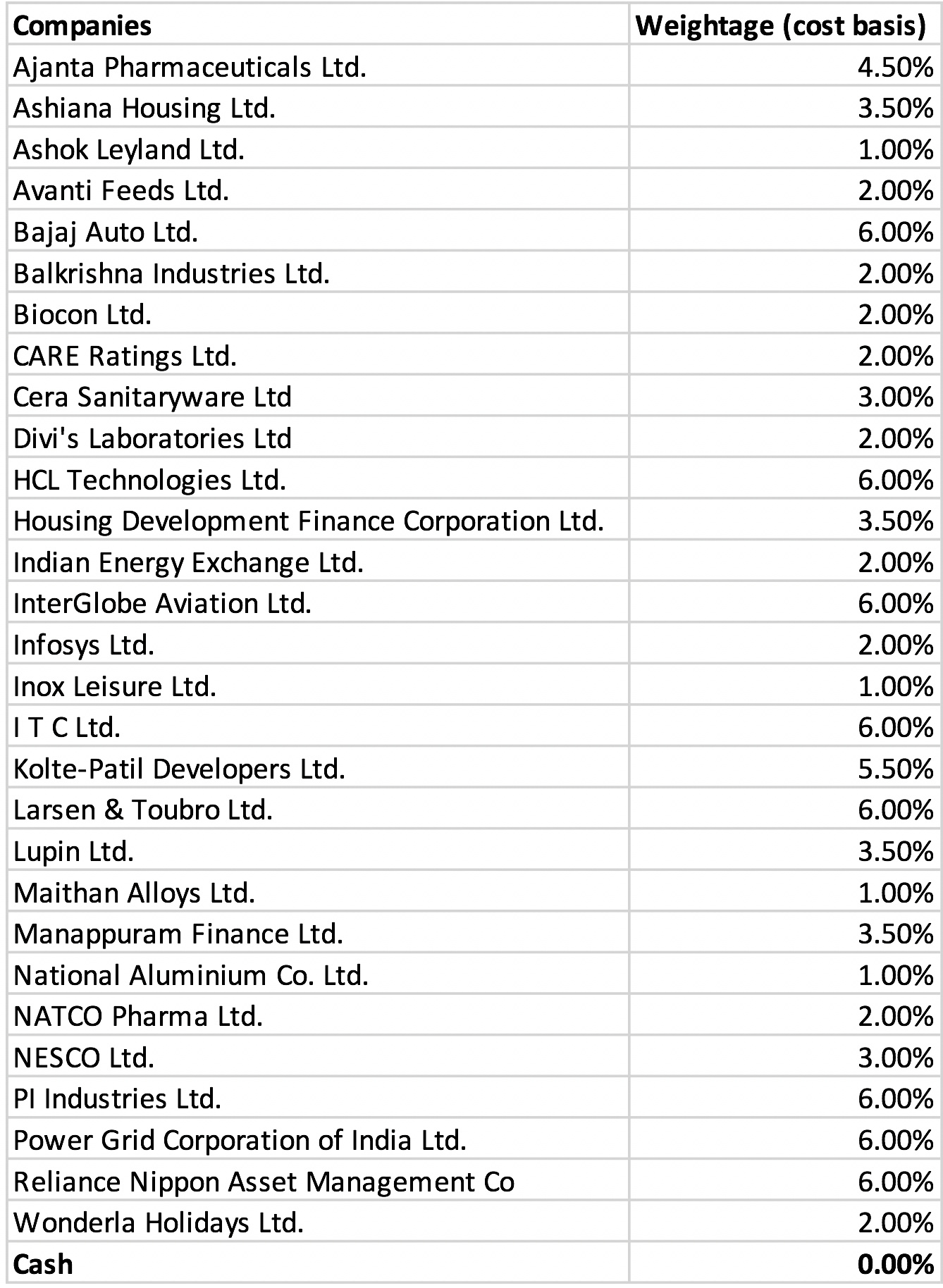

The updated portfolio is below: