Wonderla ventures into food takeaway and delivery business in Kengeri, 16 km away from Wonderla Amusement Park. I guess this is more to have some sort of revenue over the next few months. Delivery is ensured through swiggy and zomato

3 Likes

I think they opened far from the park … not sure what they are expecting out of this

India’s leading amusement park and hospitality Brand, Wonderla Holidays Limited launched

their first-ever takeaway and home delivery venture with their first “Wonder Kitchen” outlet

at Kengeri, near to satellite town Bangalore, 16 km away from Wonderla Amusement Park.

Could be the use of ppl time on payroll, constructive effort though may not have any meaningful impact.

I felt this move is out of desperation to show some revenue …

I see additional costs for the move

- area which is rented out

- set up cost

- even if they are using ppl time on payroll–> what would happen once the op restarts

not sure if this would be good long term strategy

Disc :: i have invested in wonderla

3 Likes

I think the Idea behind Wonder Kitchen is broadly to keep people engaged with the Wonderla Brand and may be later on make customers visit the park by offering some kind of coupons. I see this as a marketing move rather than a new source of revenue.

5 Likes

I have done some digging up on wonderla concall scripts to figure out what is the worth of the land and found some pointers (could not get as much information as I expected and other members can correct/add if I have missed any information):

Break up of cost for building a park:

Building & civil work will be 30%,

the rides willaccount for another 30% and

we have got the land for 30%,

the balance 10% will be on plant and equipment.

Hyderabad Park details from RHP:

Original Land cost: 21.8 cr (including stamp duty, registration & other charges)

Land Developement: 20.3 cr

Civil construction: 100 cr

Land Rides: (imported + indigenious): 33 + 36 = 69

Water rides: 10 cr

Water + power related components: 25.7 cr

Others (computers, furniture etc): 10 cr

Consultancy: 2 cr

Mission Interstellar: 35 cr - 40 cr (launched in 2017 towards end)

Chennai Park details:

Land: 61.87 Acres X 1.07 = 66 (Aquisition cost) [seems now its price doubled at 2019 rates]

Investment in land is: 75cr + 10 cr(for leveling & filling & compound wall)

Total Investment Done so far: 100 cr+

2.75 acre water harvesting tank built already

Park will be planned & built for high water efficiency

Investment: 105 + 260 (planned)

Bangalore Park:

Land : 81.7 acres [the present cost could be 1 cr/acre from one of the concall details (probably

2019) where he mentioned in south land rate is 1cr/acre avg]

84 room resort (probably at 30-35 cr - Depreciation worth at present rates if the planned expenditure

for Hyd resort is considered]

6 restaurants

Kochi Park:

Land: 93.17

In house 264Kw Solar plant

400Kwp : 2 cr: 1600 Kwh per day [forgot what this note meant]

Bangalore park has a tie up with solar power supplying company which supplies at half the cost of BESCOM price [not sure how much % of requirement it caters to]

5 restaurants

Hyderabad Park:

Land : 49.5 [Acqusition cost: 21 cr; Now worth 3 times more as per 2019 concall]

4 restaurants

Advantages: Lot of tech companies around it. Closer to road. 15 mins from airport.

**On both Serious & lighter note, they should actually buy double the land requirement and sell off the extra land after park is built; This way they will earn more than what they earn by running the park

275 cr begining investment

Park launched in Apr 2016

30-32 cr Hyd resort (estimated cost to be incurred)

500Kw Solar plant (caters to 25% of daily requirement)

Odisha Park:

Planned Inv: 100-110cr

If things go well it can be launched 1yr after Chennai Park is started

This “slightly lighter” asset model is both a threat and advantage for Wonderla. If works out well, it reduces the capital intensity. Same advantage goes for competition, which is a threat.

Present Covid impact:

If I am right, 8 cr costs/month (?) will be cash loss with zero business.

Breakeven can be achieved with 2400 customers/park, if allowed to run.

Ad spend:

22cr advt for 2019

Yearly Park related capex:

10% revenue for new rides

Even though this is considered as maintainance capex as it is used to attract repeat customers,

it has an advantage of increasing the capacity which is being ignored by everybody. It helps if there is a growth in footfalls due to GDP growth.

Year 2000: Cochin Capex: 120-130 cr initial capex [19 yrs old park by 2019]

Year 2004/20045: Bangalore: 150-160cr [14-15yrs old park by 2019]

Hyd: 280-290 cr

Random note: 72-75 cr FCF: 2017-18 [Expected]

MarketCap:

750 cr (@130rs)

Take the following projections with loads of Salt [crude estimates; no solid logic behind estimations]

Cash: 125 cr; After Mar2021: 29 cr (if reopens in Jan: 53 cr): (Reopens in Sept: 77 cr)

Estimated capex: 260 cr + 110 cr = 370 cr

Cash flow: 50cr 80cr 40cr 50cr 80cr 110cr 130cr

Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Yr7

Chennai Orissa

Launch Launch

Capex: 100 160 110 100

Borrowing

needed: -27 +53 123 73 53 163 297

1200 (cash profit x 10) + 297 (cash) = 1497 [PE = 10]

Replacement value: 350x4 + 210 = 1610 cr

If things don’t go very bad, conservatively, it can double in 7-8 yrs fetching us FD & PF returns.

Discl: Bought @330 > 1 yr back & slightly averaged yesterday @133

10 Likes

It is not correct to take EBITDA for return ratios, in my opinion. First, accounting wise depreciation can be a non cash item, but for asset heavy or rather asset dependant business like wonderla, it’s a cost. Plus, this is a high maintenance cost business, and needs to be replaced after life span is over, hence maintenance capex like new rides also add to costs. And yes, as per text book formula also, roce is pbit/Capital employed.

If you see this business in this light, it would not be considered a great business, I would say.

3 Likes

I also wonder if the replacement cost (after lifespan is over) of the rides would be much higher than the first time around, because of general inflation. Hence, the depreciation cost might not be adequately reflect the real cost.

when there is some much investment going in company and economy is not normalized its diffcult to see roce . so he can break roce on project level basis if new is to done . for example Chennai would x roce in beginning and 2x after 5 years ( bcus of y reasons like gdp going up and j curves some sometime in these kind of buisness ) we can find its good business and rest we have to c , company has the right to win in that business… i think its a good business and right to win , but very long term stock where ppl are not afraid of spending 7000-8000 twice or thrice a year

2 Likes

And also remove the revaluation of land reserves in FY17. Thats one of the reasons for jump in net worth.

1 Like

I have just started to read this thread but without knowing something it is becoming very difficult for me to read further.

Could anyone please help me understand why company’s ROCE & ROE is so low and is continuously falling?

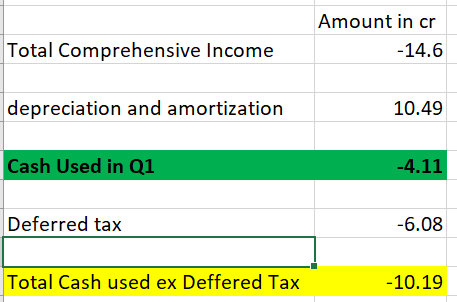

Just going through Q1 FY 21 …

I felt the management has done wonderfully in managing the expenses @10.19 cr … deferred tax of 6.08 has saved it and reduced the cash oh hands spend to 4.11

Cash on hands :: 110.11 cr i feel would be sufficient for the company to sustain for the financial year with out any debt

chennai Project :: 330.24 cost - spend 109.19 == 221.05 Funds required expected to start in oct 2020 till Apr 2022

Below would not have any importance , but just curious to understand what rate has management taken

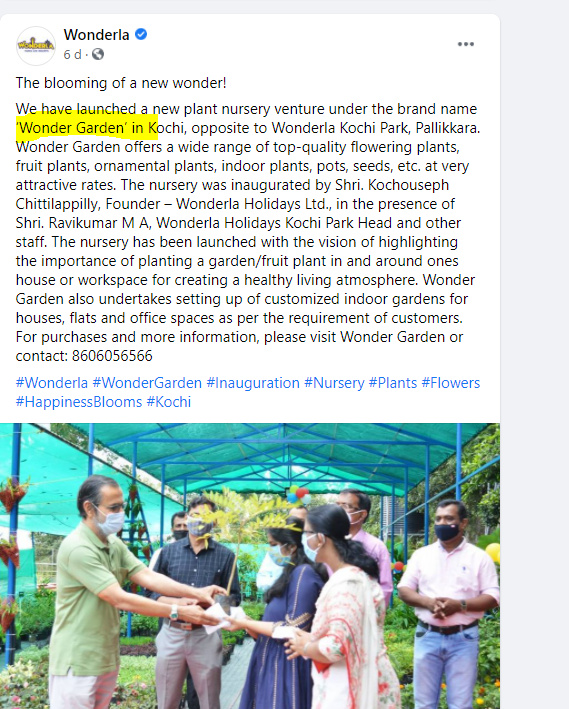

Update on Wonder Kitchen Initiative from the Conference Call.

The Management plans to open 3 more outlets. One each in Bangalore, Kochi and Hyderabad. The Capital outlay on the same is very minimum (limited to payment of deposit) as currently they are using the parks’ spare kitchen equipment.

They have decided to assess the success of these outlets for 6 months or so and then take a call on further expansion. They will like to have it as a permanent alternate source for revenue.

Operational Metrics :

Rent - Rs. 50,000 pm

Break-Even Level - Rs 13,000 per day (To date they have achieved sales worth Rs 5L)

Margins - 50-60%

3 Likes

Does anyone know what proportion of water they use in water parks is recycled/rain water and how much is derived from external sources?

Bangalore is suffering from a water crisis and is amongst BBC’s 11 cities most likely to run out of water (in the world), which definitely will be a bad thing for wonderla.

As per the latest annual report, they’ve recycled 370 million + litres of water but this number is quite useless since 1 litre recycled 1000 times = 1000 litres recycled. To make any sense of this number, we’d need the frequency of recycling and how much water does wonderla’s water park use.

If anyone can help in this regard, it would be really helpful!

4 Likes

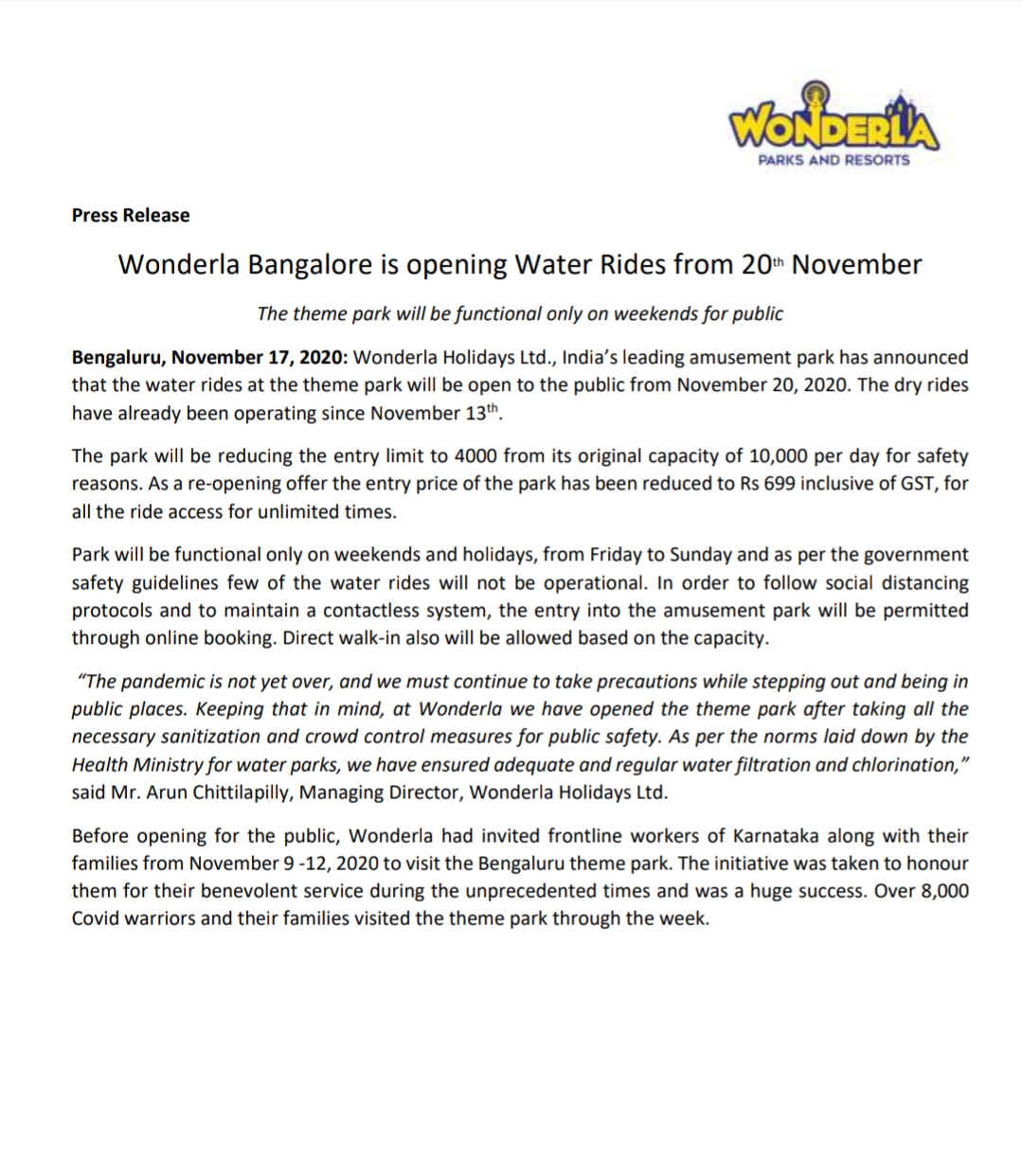

Bangalore park will reopen on November 9, 2020 post COVID (only on Fridays to Sundays at a price of 699+GST) with maximum capacity limited to 3000/day

5 Likes

Dont know if anyone observed…looks like Rakesh Jhunjhunwala firm(Rare enterprise) is invested or looking to invest in Wonderla as they were present in the concall.

6 Likes

Wanted to share some info:

I had contacted two of my friends who live in Bengaluru here is what they said:

One of them visited in 2008 and other in 2016.

- Both of them said that they did not like the experience because it gets very crowed, even if you take a VIP pass.

- One of them said that the rides were not great and just ordinary. Plus, people vomit during the ride so he did not enjoy the experience.

- Inside food was of poor quality. Even though there is Papa Jones inside.

- Their school (Sri Kumaran school) used to take them to Wonderla every year but now they have cancelled this tradition because children run away and misbehave, which is also difficult to track when you go for an outing in a big crowd.

- They both said that people are crazy about Wonderla in Bangalore but its over-hyped.

Hope this adds value to the thread.

3 Likes