Some forward looking statement talks about backlog of weddings which can be seen as somewhat unavoidable for consumers. However, we need to bear in mind that all hotels and hospitality players will already be ahead in this game.

One overhang was one the leadership succession, but with Arun C coming back this can be considered a non issue. The question now is how is the business model getting impacted because of this and how the management is preparing for this?

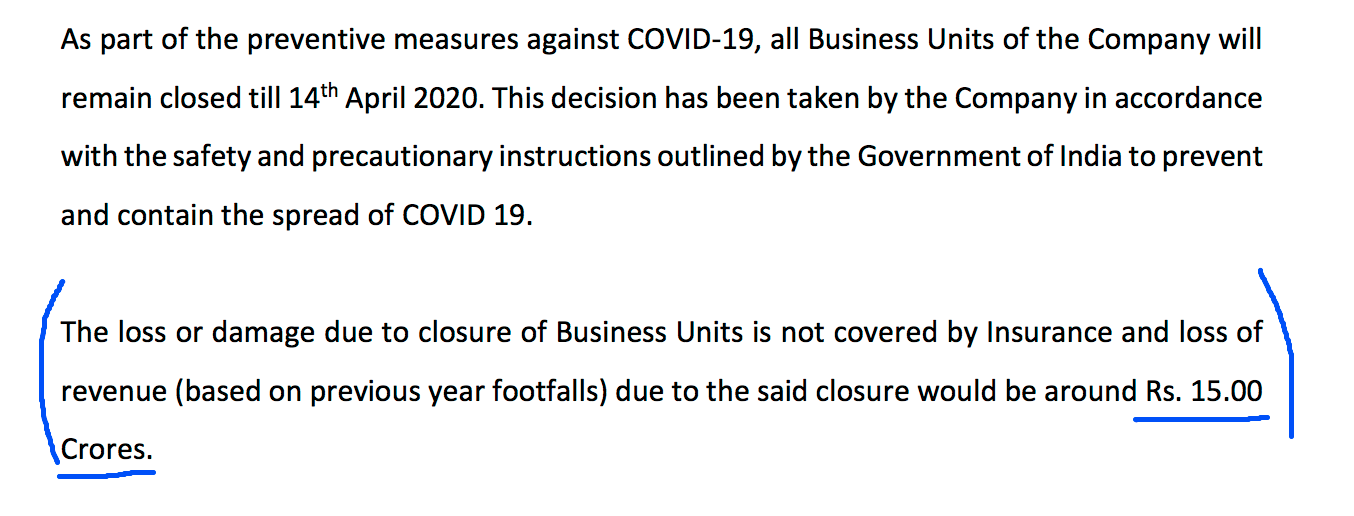

–no visitors, no income for time till vaccine or no new cases - min 2 Qtrs.

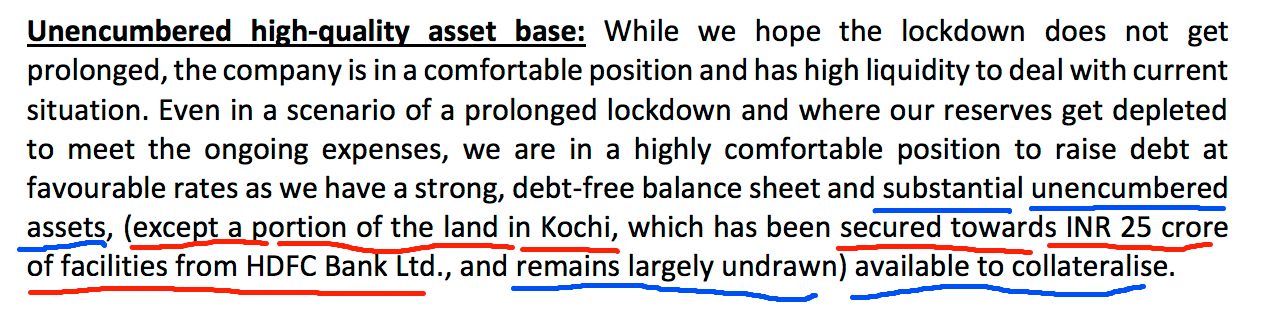

– company cash is enough to support necessary exp for close to a year at current burn rate, can last longer if situations persist by cutting down gradually

– all capex goes on hold, opex optimization measures to be taken.

– Company Value = Liability - Assets. We are getting it lesser than book value. Land will not get wiped off.

– Prmoters buying indicates something. Promoter integrity and quality is reassuring

This too shall pass

– Vaccine is found, virus is in control at some point

– Mkt will reward most beaten but strong balance sheets most handsomely- add Moat

– Competetion is likely to suffer worse who has higher debts

– Safety, security, distancing can be better managed in open amusement parks than closed spaces IMHO ( offices, malls, multiplexes, restaurants etc).

Imagine no footfalls to growing scenario

If business it shutting down for an year - can I still hang in? being a natural optimist I am - trouble times + moat biz+ promoter quality + strong balance sheet+ belief in biz model.

This is one of satellite portfolio bet - less allocation for now but may add on dips - though long shot.

Moat of Wonerla , has been discussed many times, but the fact is the business wont grow until and unless footfall increases dramatically, everytime for the last 2-3 years something or the other has shown the vulnerability of the business model, whenever they become stable another event happens which is totally out of control of the management and the business gets hit. So basically only when the footfall increases and keep on increasing Q on Q then only the business is going to get valued in terms of stock price.

Impacts that has happened in the last few years is , Nippah Virus in Kerala, Ride accident in Bangalore(social media made a small incident viral), Floods in Kerala, 2times, and now Covid19, in all these cases Management was just helpless to do anything. So investing in this and expecting to get good returns is going to take very long time.

Invested at higher levels! Not yet averaged as it can further go down once promoter buying gets reduced.

Sir,

Pardon for the amateur question.

Regarding the 300+ crore increase in equity due to revaluation of land, how can we trust the number? is there any way to verify it?

I remember seeing a valuation report on its website if you can locate it… Land is usually 30-50% of the prevailing residential rates in that region so that can be used as a ballpark

Buffett teaches that the best business is one which can generate high economic returns on large amounts of incremental capital over long periods of time.

In this context, I studied the business of Wonderla. I feel that the business doesn’t have the capability to generate good economic returns on the incremental capital.

Let’s take the upcoming Chennai park. The projected capex is 365 crs. Assuming that the park starts getting 10 lakh visitors in the first year (highly improbable but still taking the best case scenario), average revenue of Rs 1000 per visitor. The revenue would be 100 crs per year. EBITDA margin of 45% leaves EBITDA of 45 crs. Maintenance capex of 8-10 crs leaves pre-tax owner earnings of 37 crs. On an investment of 365 crs, that is just 10% ROCE. And this is assuming the best case scenario and this is pre-tax.

Let’s take the Odisha park which is to be built on an asset light model.The projected capex is 110 crs (without land) . Assuming that the park starts getting 6 lakh visitors in the first year (highly improbable but still taking the best case scenario), average revenue of Rs 600 per visitor. The revenue would be 36 crs per year. EBITDA margin of 45% leaves EBITDA of 16 crs. Maintenance capex of 5-7 crs leaves pre-tax owner earnings of 11 crs. On an investment of 110 crs, that is just 10% ROCE. And this is assuming the best case scenario and this is pre-tax.

The economics of the business doesn’t look attractive to me. Am I missing something ? Please share your views.

The amusement parks business is not an asset light model but is still economically feasible. When a new park is operational, it takes a few years to reach an optimum utilization level. The Hyderabad park did revenues of 57, 64, 76 cr. in the first 3 years of operations. It takes somewhere close to 5 years to reach revenues of 100 cr. And then incremental revenues are mostly driven by ticket price increase as footfalls reach a steady state. This is clearly seen in footfall numbers of Kochi (8-10 lakhs/year) and Bangalore (10 lakhs/years) parks. On the other hand, once the park is constructed, there is very little incremental capex (maintenance capex < 10 cr./park) to create additional revenue. That’s why these kind of businesses globally are valued relative to their book value.

I think this would be an unfair way of analyzing Wonderla. The beauty of building a park is that once you put up the upfront capex of building the park, there is very little incremental capex that is required to attract additional customers to the park. Maybe you have to introduce the odd new ride every other year to keep things fresh, but nothing majorly substantial.

The thing missing in your analysis is what the ROCE looks like 10 years after building the park. The gross capital employed would still be roughly the same (maybe 400 cr instead of 35), but hopefully, the park would have attracted many more visitors, increased ticket prices, increased F&B spend. So maybe after 10 years the revenue would be 300 cr and the EBITDA would be 135 cr. Maintenance capex would be a little higher so pre-tax earnings of around 120-125 cr giving a ROCE of 34-35% on the initial investment. Now think of what would happen if another player wanted to build a park opposite Wonderla’s because he is attracted to this high ROCE. By now land prices may have gone up substantially, there is 10 years inflation, so the same park that Wonderla built in 350 cr, might cost a new player 1000 cr to build after 10 years; and even then his best case scenario would be that maybe half the guests who went to Wonderla would maybe come to his park. The economics would look really bad compared to Wonderla, this is a big deterrent for any competition to arise in the same location that Wonderla already has a park. Wonderla would have a natural monopoly wherever he builds his park.

The initial investment cannot be taken as 365 Cr for the calculation after 10 yrs but considering a cost of capital of at least 7%, the capital after 10 yrs is 730 Cr. Hence RoCE is 16%.

I am simply stating that the quality of business looks mediocre given that the incremental capital would be invested at average rates of return. If the business looks mediocre, I would simply give it a pass without making an attempt to value it.

In my analysis, I took 10 lakh visitors for the Chennai park in the first year itself. Bangalore park was set up in 2005 and after 15 years, it is attracting 10 lakh visitors per year and the growth in footfalls has plateaued now. Kochi was set up in 2005. After 15 years, the footfalls are ~ 8 lakhs per year. Hyderabad was set up in 2016. After 5 years, the footfalls are ~7 lakhs per year.

Does it look feasible that Chennai will have 10 lakhs visitors in the first year and then footfalls will keep on increasing at a good rate for for the next 10 years? To my mind, the answer is a clear no.

We should not get excited by optically high ROCEs on assets valued at their historical costs.

It could be initial years it took for the Park to get to limelight. But 14 years and 25% is significant time. (Though there could be sharp U shape recovery ones the senario eases after lockdown is lifted.)

Having read the thread and analyzing annual reports, my conclusion is that the stock doesn’t seem to be a buy (even at the current prices) because I don’t see where growth will come from so fast as to generate meaningful returns for investors due to following reasons: (please correct me if I’m missing anything)

The revenues have stagnated in the past 2 years (I believe that sharp price hikes are not sustainable and it seems to have reached a breaking point)

Footfalls are almost the same or have declined as they were 4-5 years ago in B’lore and Kochi parks (although revenue has increased, the pace is still not that impressive)

Lot of uncertainty regarding footfalls every year due to some reason or the other (Excess heat/excess rain/high price hike/domestic issues etc.)

Earnings have only grown around 10% YoY for the past 5 years

Management can’t get the pricing right

Management says they’ll add a new park every 3 years but land acquisition/regulatory hurdles are a problem (eg. Chennai) and the 3-year timeline of adding new parks doesn’t seem realistic

Can’t rely solely on the value of huge land parcels owned by the company as being equal to its current market cap (or even higher) due to reasons like land being far away from the city, finding buyers etc.

Disc: Still closely observing

Look at the capital invested from two perspectives -

Amusement park

Land appreciation

Your arrived ROCE figure of 10% has been calculated assuming that all of 365 crs were required to generate the 30 crs. If we look at their past doings, usually 1/3rd of the land is used rest is kept for future expansions.

By maintenance capex if you mean adding new rides and doing capex for the same, I doubt they do an 8-10 cr one for each park every year. But if you mean general repairs, the EBIDTA consideration includes the miscellaneous expenses as well.

Moreover, by investing 365 crs now, apart from getting a 30 cr cashflow annually which increases more than the inflation rate, you also have an appreciation of land (both used and unsued).

While the capital returns from land appreciation are not as feasible to calculate, they should have a significant position in our return calculation.

From whatever concalls i have read they have time and again stressed that they are not looking to monetize land. Rather, they want to have an option in the future if they decide to do expansions which would otherwise become an expensive affair.

Thanks. It just seems like a waste of resources if the land is just sitting there. Without being rented out, farmed upon, whatever.

I guess one can assume a 3% or so appreciation of the land held every year & adjust economic profits of the business accordingly.