Pledge release

2 Likes

Latest interview of Mr. Khoraiwala to NDTV.

-

Nothing much new, he could not quantify the market size of Nafithromycin. This drug will most likely be launched in FY25. WCK 5222 will mostly like be launched in FY26.

-

Wockhardt has two patents for Nafithromycin. One will expire in 2031 and second will expire in 2037.

-

Also for WCK 5222 they have two patents. India patent will expire in 2031/32 and I am assuming for other countries, it will expire in 2037.

Disclosure - Invested.

3 Likes

Approximate Market Size of Nafithromycin (WCK-4873)

Assuming Nafithromycin will target drug resistant community acquired bacterial pneumonia cases. (CABP)

According to the study - Incidence and risk factor prevalence of community-acquired pneumonia in adults in primary care in Spain.)

CABP rate in adults worldwide is 4.63 per 1000 persons/year.

According to this source global adult population greater than 20 years of age is approximately 7.76 billion.

Therefore, CABP cases worldwide are approximately 36 million/year.

Study - The antimicrobial resistance profile of Streptococcus Pnemoniae

suggest that global macrolid resistant rate in S.Pneumoniae, most common bacteria causing CABP ranges from (10-46%) and can taken at 28%.

therefore, it can be approximated that there are 28% of 36 million/year that is 10 million drug resistant pneumonia cases/year worldwide.

According to an approximation out of total cases 20-30% happen in developed countries (let’s say 25%) and rest that is 75% occur in developing countries.

therefore, approximately 2.5 million drug resistant cases of pneumonia occur in developed countries and 7.5 million happen in developing countries.

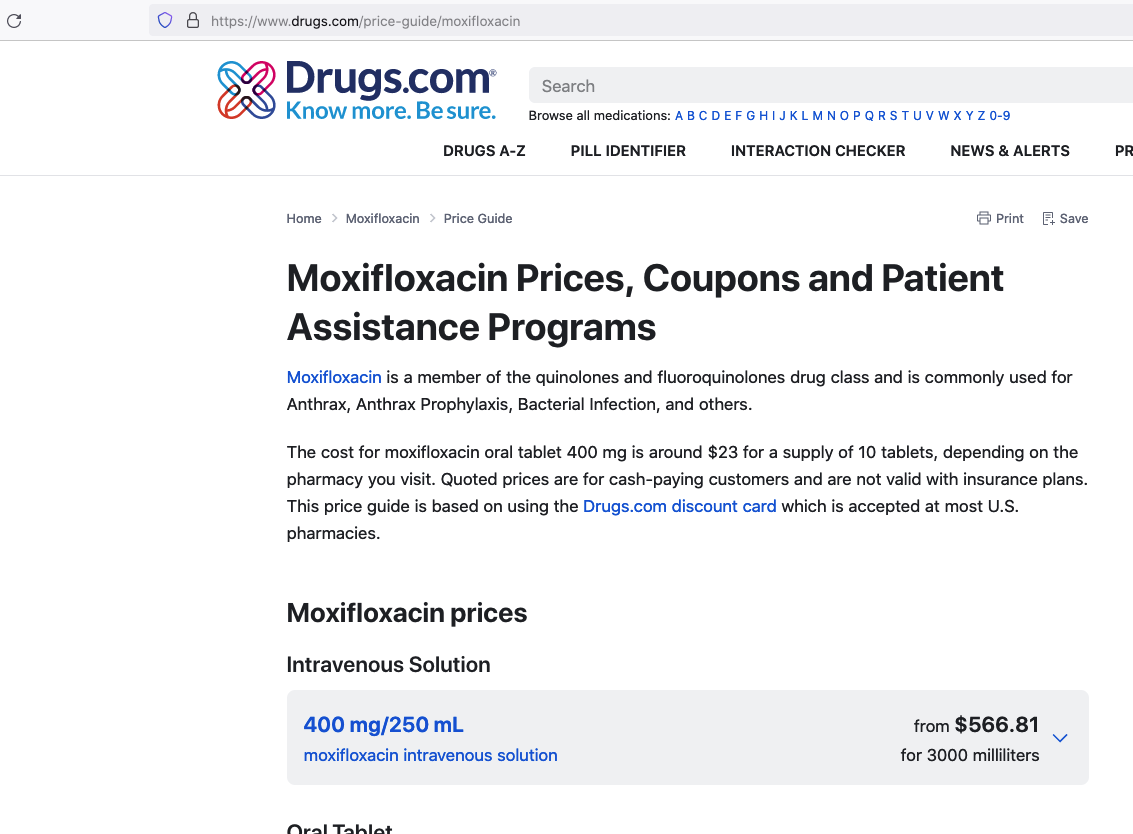

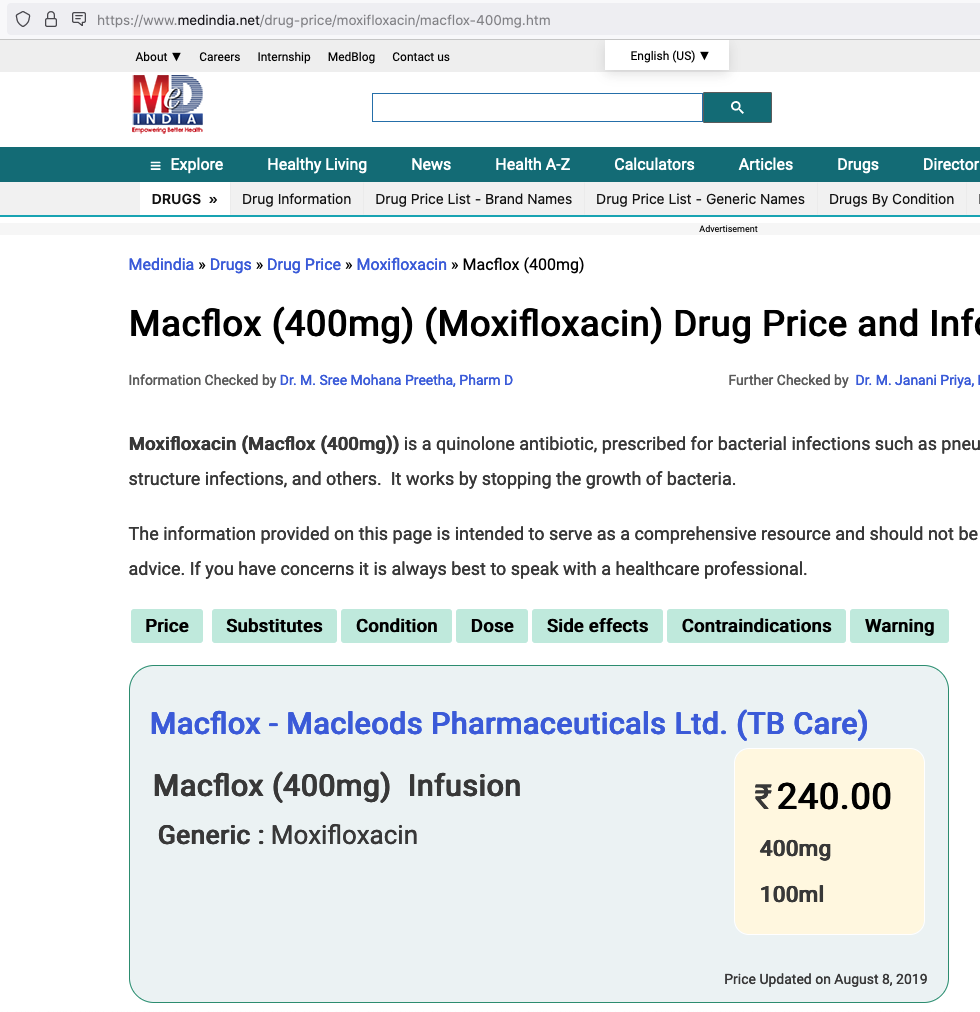

Now, we don’t know how drug will be priced but assuming it will be a substitute to Moxifloxacin intravenous and similarly priced.

Price of one regimen of Moxifloxacin in US is

and similarly for 12 doses of 400mg each price in India is

therefore, potential market size is

Developed countries = $1.5 billion/year &

developing countries = $263 million/year

Disclosure - I am invested and biased. The calculation uses various approximations to reach at conclusion and therefore should be considered an exercise for educational purposes only.

10 Likes

Approximately how many months/years does it take to generate revenue from a drug once phase 3 trial is successful.

Specifically when can we expect cash from nafithromycin to flow to the bottomline?

1 Like

After the phase 3 trial, the company seeks regulatory approval. They can start selling once the regulatory approval is granted.

In the USA, the FDA claims that it takes between 6 to 10 months to approve a New Drug Application (NDA) [1], but frequently it takes more than 12 months. It also takes a long time (anywhere from 2 to 12 months) for the company to prepare the NDA, which is a massive undertaking. So, in total the NDA + review process takes about 8-24 months. The timeline can vary in other countries.

Unlike other drugs, Nafithromycin has been approved as QIDP, so it will be processed under “Priority Review” [2] - we can be sure the review process will take less than 6 months [3]. The total time to market will depend on how fast the company can prepare the NDA. If they take 2 months, then the drug will come to the market within 8 months.

[1] Step 4: FDA Drug Review | FDA

[2] Priority Review | FDA

[3] 21 U.S. Code § 360n

8 Likes

Hi,

I had a few questions regarding the company,

- Will Wockhardt Ltd manufacture WCK 4873 for any market? What are the terms with Jemincare for manufacturing and which market will they cater to?

- When will the revenues from royalties for WCK 4873 start flowing in?

- What is the revenue from different segments; Contract manufacturing, Branded medicines,

Diabetics and Vaccines? - What are the margins from the these segments?

- What shall be the revenue model for WCK 5222, are there any partners sourced for manufacturing? What are the estimates for royalties that can be received by the company on that drug?

Would like to know your thoughts on the same.

Thanks

Wockhardt Bio AG, a subsidiary of Wockhardt Ltd will manufacture WCK 4873 for the Indian market. Jiangxi Jemincare Group Company Ltd, China will develop and commercialize the drug in China, Hong Kong, Macau and Taiwan. In the press release on Aug 26, 2021, the following terms were mentioned:

Jemincare will be responsible for exclusive development and commercialization of the Nafithromycin in the select markets. A joint steering committee is formed to oversee development and regulatory activities. Wockhardt will receive an upfront payment and will be eligible for regulatory-linked milestone payments. Further, Wockhardt would supply the product to Jemincare and will receive royalties on net sales. Wockhardt would transfer the manufacturing technology to Jemincare at mutually agreed time.

As of now, Wockhardt has entered royalty partnership with Jemincare. I will leave this question for others because I do not know the regulatory requirements of China.

Unrelated to your royalty question; but the revenue from sales in India will start after the DGIC approval – expected sometime in the middle of 2024. I also expect them to enter the US market, but I have not been able to find any information regarding NDA submission at the USFDA.

The company is restructuring its US business to shift from in-house manufacturing to contract manufacturing. However, this has not yet started. On the other hand, Wockhardt was itself a contract manufacturer for Covid-19 vaccines in the UK. I have not been able to find a breakdown of the other two segments: Branded Medicines and Diabetics. I will again leave that for other researchers.

Sales

| Segment | FY2023 | FY2022 | FY2021 | FY2020 |

|---|---|---|---|---|

| Non-vaccines | ₹2750 | ₹2727 | ₹2708 | ₹2844 |

| UK Vaccines | ₹23 | ₹523 | – | – |

EBITDA

| Segment | FY2023 | FY2022 | FY2021 | FY2020 |

|---|---|---|---|---|

| Non-vaccines | ₹208 | (₹39) | (₹47) | ₹245 |

| UK Vaccines | ₹15 | ₹357 | – | – |

Source: Annual Reports, 2021-22 & 2022-23

As far as I know, the company has not disclosed any revenue model for WCK 5222, neither has any partners been announced. Estimates of revenues / royalties vary widely: The floor is ₹0 if the drug is not approved and the ceiling is the total market size. Again, the total market size is debatable: In my opinion, it is around $4b. Moreover, past performance of the company has been erratic, so it is difficult to estimate an upper ceiling for the company.

Disclosure: Invested

12 Likes

https://www.ema.europa.eu/en/medicines/human/EPAR/exblifep

Orchid Pharma’s ‘Exblifep’ received positive recommendation from EMA.

The drug is cefepime+enmetazobactam, indicated for uses in

- Complicated urinary tract infections (cUTI), including pyelonephritis

- Hospital-acquired pneumonia (HAP), including ventilator associated pneumonia (VAP)

Can there be an impact on WCK 5222’s market size, given that one of the uses for this drug can be for Hospital acquired infections like VAP?

3 Likes

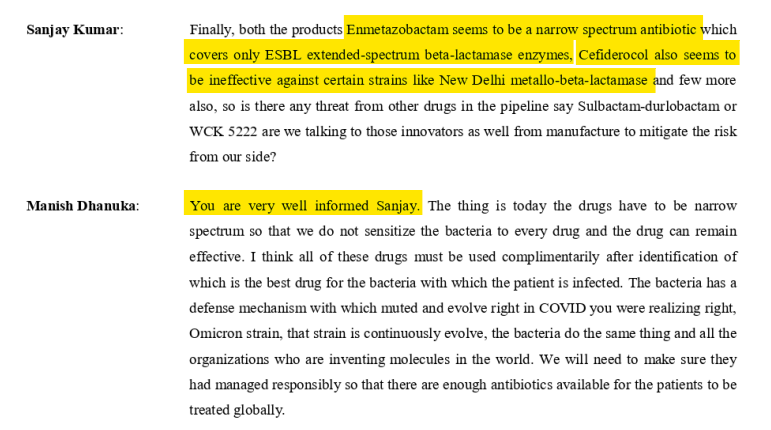

FEP-ENM or Cefepime/Enmetazobactam to be sold under brand name Exblifep has good efficacy in certain class-A beta-lactamases but overall its performance is comparable to Piperacillin/tazobactam (sold as Zosyn and gone off-patent in '23) which again is comparable to meropenems. These are not effective in MBL-producing strains is what the studies say.

WCK 5222 or FEP-ZID has efficacy against all classes of ESBL and carbapenamase producers (see FEP-ENM column and compare against FEP-ZID 1:1 column to get an idea). Bold text with or without greater-than signs mean those variants are resistant to the drug in that particular column.

Exblifep will be competing against a generic Zosyn and meropenem and odds of it being priced higher than these are slim since efficacy is equivalent. WCK 5222 is more comparable to CAZ/AVI (Avycaz) or ATM/AVI and is showing in studies that it is even better than those as its mode of operation is completely novel (BLE) compared to anything that currently exists.

If anything the royalty that Orchid can make can give us a good idea of what to expect with WCK 5222 (it has to be few times better than FEP-ENM)

22 Likes

Would request @phreakv6 and others to elaborate on this.

While it does look promising, are there any anticipated hiccups or slips between cup and lip.

5 Likes

Latest presentation shared today by company…

3413422b-6fcb-4520-88bf-8a86a7fc9de3.pdf (2.5 MB)

Discussed it here in brief.

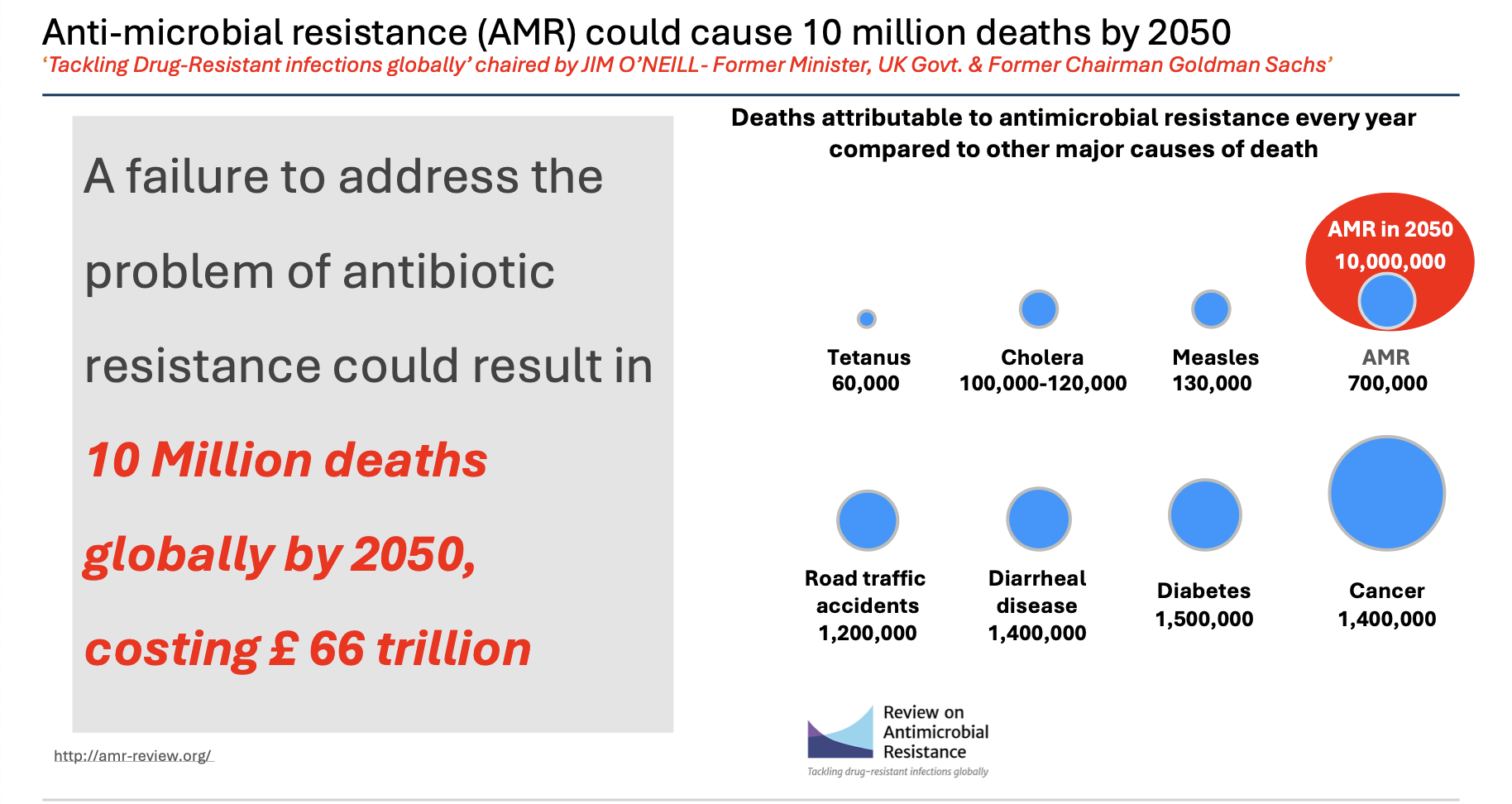

Today’s presentation has some very useful information

AMR deaths at 700k worldwide and could be 10 million by 2050.

I found the same information from multiple sources

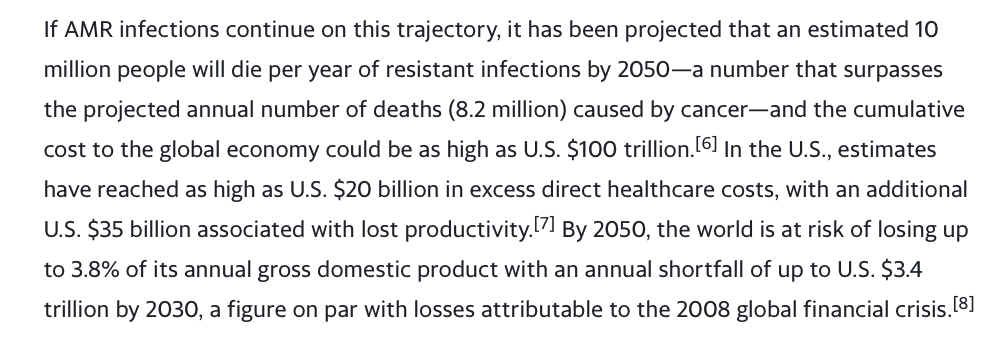

This bit is from Venatorx failing to get FEP-TAN approval this month (more on this later) which again speaks of a similar 10 million number by 2050.

Antibiotic pipeline is more or less dry so a company like Wockhardt which has kept its R&D going becomes all the more valuable, over and above the value of the 6 NCEs it has developed. (Consider gestation in decades and experienced talent with 315 scientists and 55 PhDs)

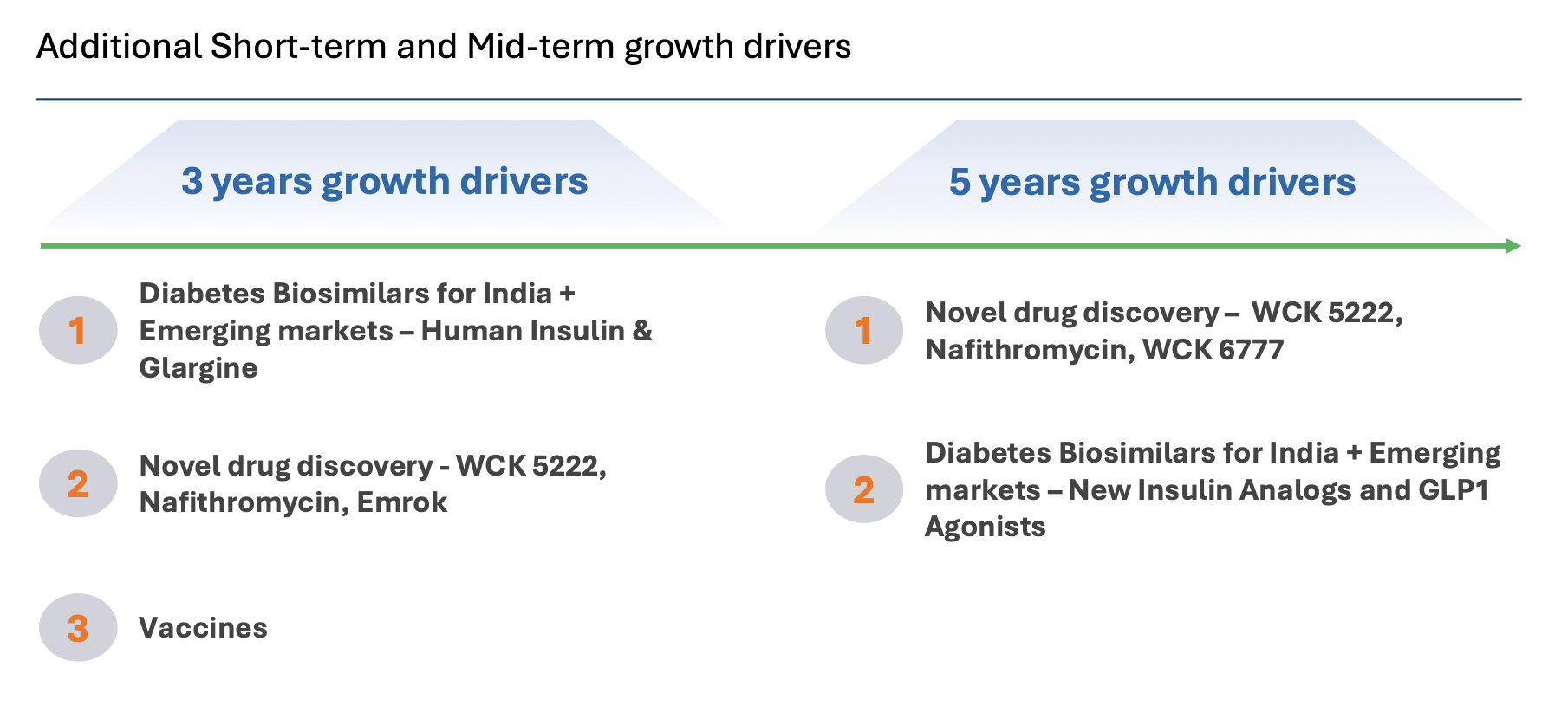

It looks like growth will come from insulin glargine launches in emerging markets and also from vaccines business (need more clarity here though on what these 150 million doses are for and what Wockhardt can expect to make from it - the longevity and profit-sharing is enticing but hard to figure out what it will generate) and from US business restructuring, alongside growth in Emrok/Emrok-O and Nafithromycin launches in India and other Emerging markets in the next 3 years - outside of WCK 5222.

Also good to see long-term vision in GLP-1 analogs - but this could be a rather crowded space by the time semaglutide goes off-patent.

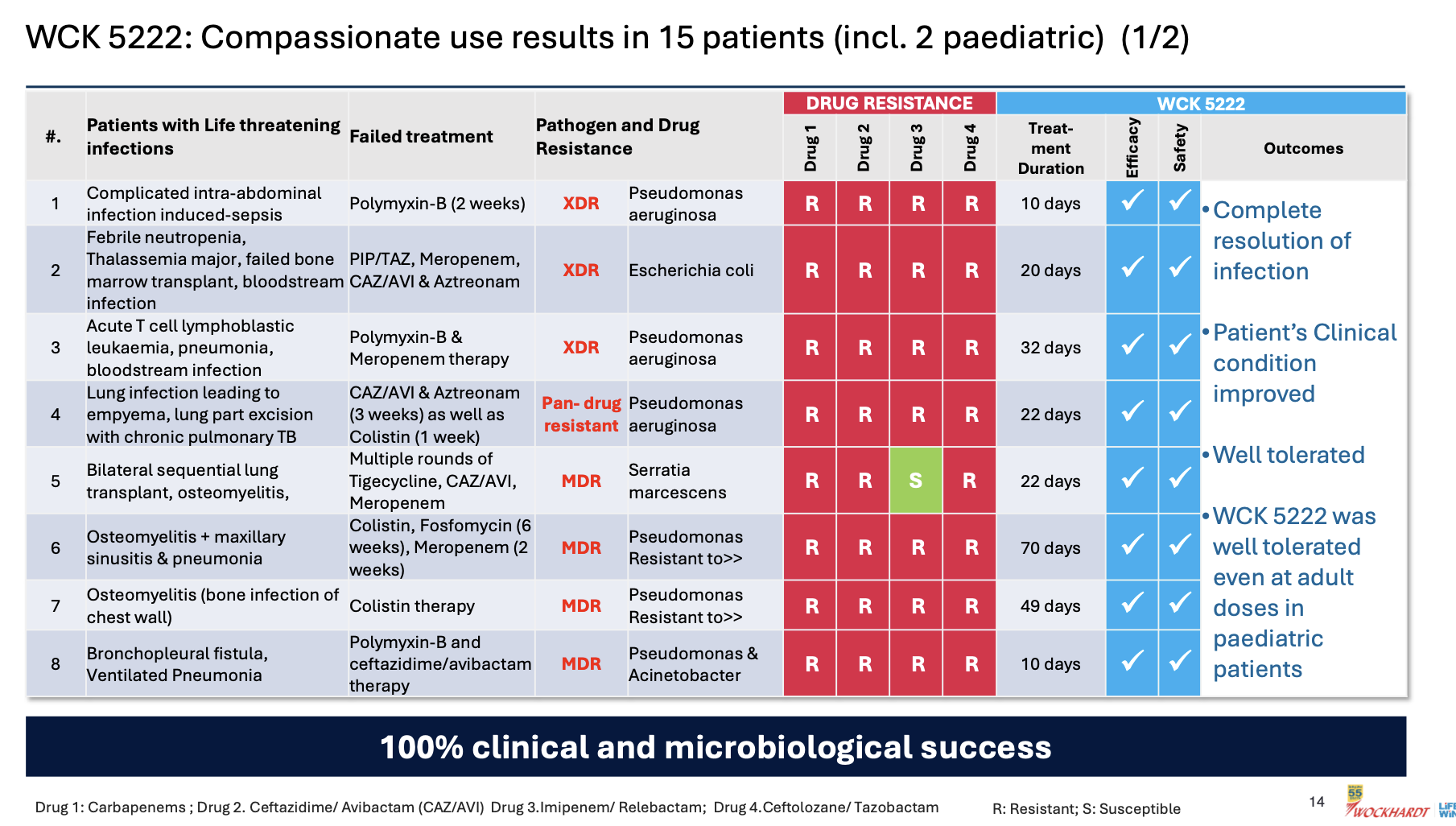

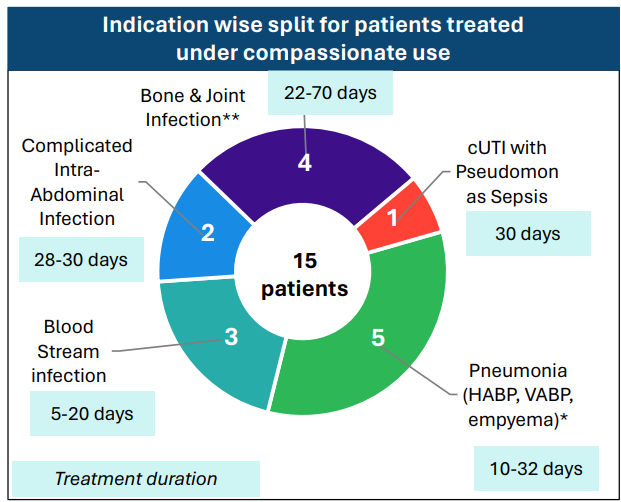

Coming back to WCK 5222, the company has disclosed the compassionate use results in great detail

Few things of note

- Pediatric use was well tolerated even at adult doses - so safety of the drug is becoming better established

- 100% clinical and microbiological success confirming efficacy

- CRPA is where WCK 5222 seems to shine (11/15 cases)

- Avg. use of drug could be around 4 weeks (though sample size is small, it appears varied so could be a general indicator)

- Colistin and Polymyxin are present in most ineffective treatment - wondering if these could be replaced with WCK 5222 right off the bat. While Meropenem is expected to fail in these, it is also good to see CAZ/AVI or CAZ/AVI + AZT resistant strains being susceptible to WCK 5222

(Please take above interpretations with pinch of salt - I am going by my half-baked knowledge)

This is the clincher for me

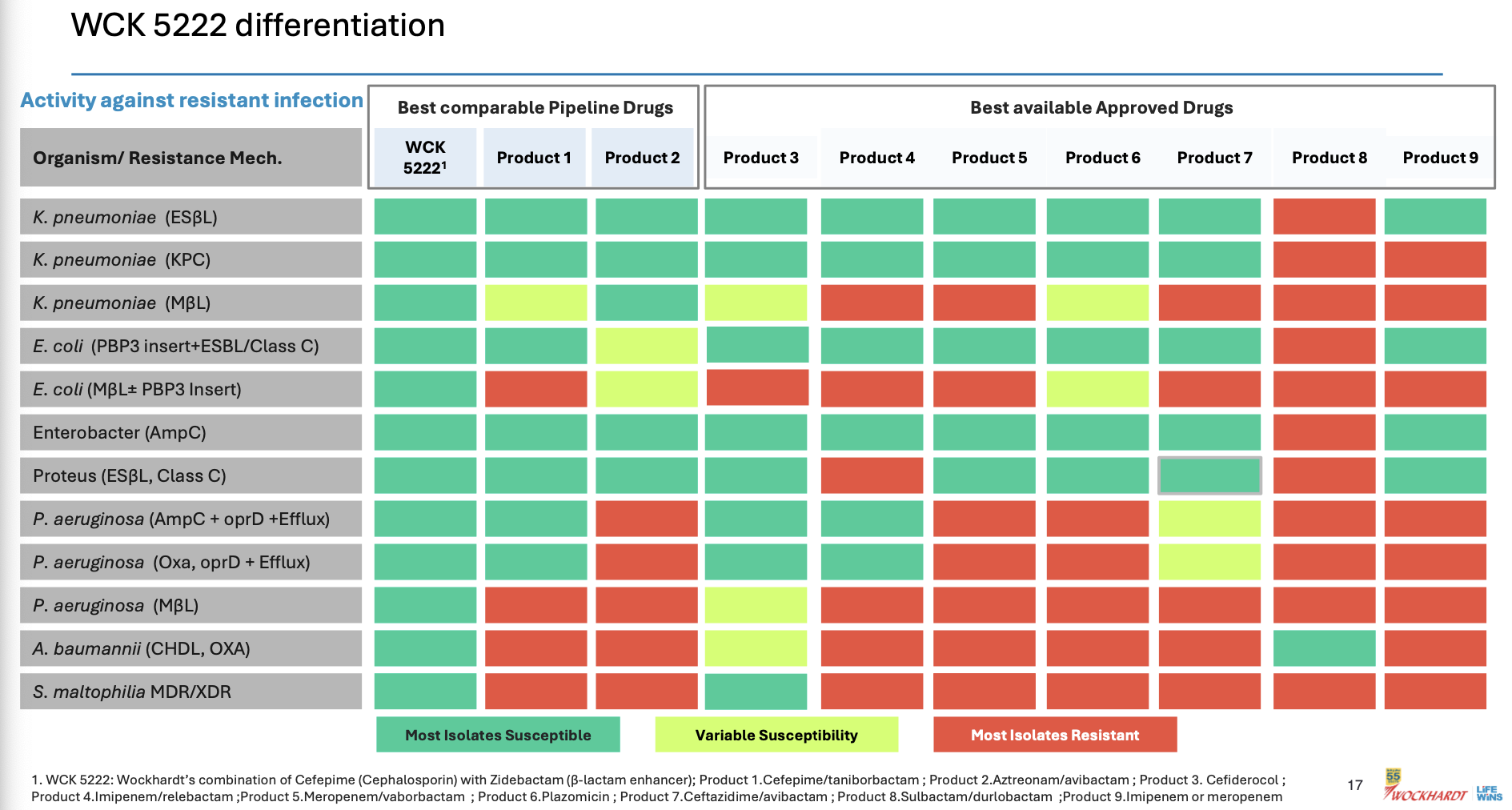

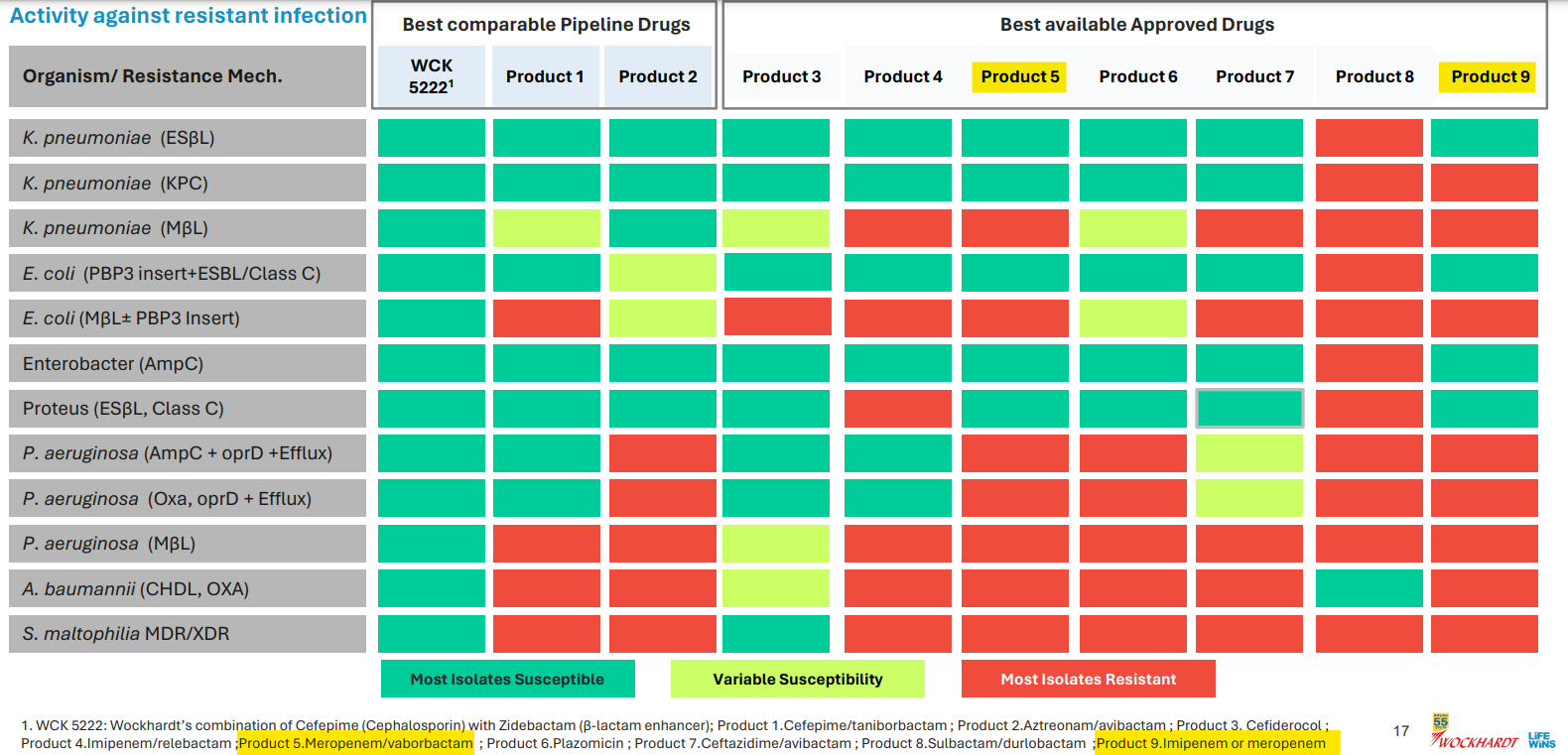

This was the point of our post based on our research from various papers. Here it is laid out clear for even a layman to understand.

The actual products are mentioned in fine-print at the bottom of the slide. I see WCK 5222 being better than CAZ-AVI, FEP-TAN, CFD, AZT+AVI which are the main comparable treatment against lot of the resistant strains - especially the MBL-producing PA and E. coli. With FEP-TAN too falling out (probably due to Treatment Emergent Adverse Effects being higher than Meropenem), value of WCK 5222 once approved should be substantial.

Before I close, the same yahoo finance piece mentioned MBL prevalence increasing the US

MBL-producing pseudomonas is where WCK 5222 has very good edge over the others. This increase in prevalence in the west again increase market value of WCK 5222 once approved

Overall things seem to be going in the right direction. Hope the company can raise the funds required to take the phase-3 to completion and not botch it up somewhere

Disc: Invested

33 Likes

Thanks for the deep explanation.

Any idea on what current dosage costs are for comparable drugs to WCK 5222 and WCK4873 are for the approximate period of recovery.

Below is the page for Global Phase 3 trial of WCK 5222. It was last updated on 14Dec23. It might be useful to track the page nonetheless -

https://clinicaltrials.gov/study/NCT04979806?term=wck%205222&aggFilters=phase:3&rank=1#locations

7 Likes

2 pharma experts talk about Wockhardt. Listen from 53.45:

https://x.com/unseenvalue/status/1769060267634180304?s=20

The point made by Mr. Aditya Khemka:

“Wockhardt announced that they have met some clinical endpoint. You study the trial design and compare it with other drugs. If I am a pharma company, I have the ability to design the trial in a manner that it is geared to show successful results. Are those results acceptable to the regulator? Probably not. If I am a disciplined pharma company, I will design the trial which is geared to fail and then if my drug succeeds, regulator will never say no to it because my design itself was very tough.”

I think he is wrong on many aspects. Trial design is developed in consultation with regulators. These designs have to follow international guidelines. And the trials do have discriminatory power to reveal under performing drug. The guidelines are such that a bad drug will show up irrespective of how you design it.

Many examples in the recent past - Tebipenem and Eravacycline failed, Cefiderocol failed in CREDIBLE CR!!! (Orchid has received sublicense to manufacture this drug for LMIC)

And Aditya sir makes it worse by not naming which drug he is talking about. WCK 4873 (Nafithromycin) has completed phase 3 and this was not a global trial. WCK 5222 is still in phase 3. We will look at the trial design of both.

WCK 5222:

THE TRIAL DESIGN WAS SUGGESTED BY US FDA!!!

Both India and US trials are public. Link to global Phase 3 trial of WCK 5222:

https://clinicaltrials.gov/study/NCT04979806?a=7

“A Phase 3, Randomized, Double-blind, Multicenter, Comparative Study to Determine the Efficacy and Safety of Cefepime-zidebactam vs. Meropenem in the Treatment of Complicated Urinary Tract Infection or Acute Pyelonephritis in Adults”

Why Meropenem is the comparator drug?

As per regulators, a new drug has to be compared with standard of care. Meropenem is the SOC for cUTI.

A slide from Wockhardt’s presentation lists the peers of WCK 5222 and Meropenem in isolation (Product 9) or in combination with Vaborbactam (Product 5) is a standard of care for some 4-5 high priority pathogens identified by WHO:

Orchid’s Enmetazobactam was tested against PipTaz but I feel both these drugs are inferior to WCK 5222 as they are narrow spectrum and will be used only in certain indications like ESBL:

Forget WCK 5222, I think Enmetazobactam and PipTaz are inferior to even Meropenem. Don’t know why Allecra made the strategic error in comparator selection. May be they only had preclinical data for Enmetazobactam in comparison to PipTaz which was presented to FDA. Ideally they should have used Meropenem as the comparator. Why do I say this? For carbapenem resistance pathogens, the line of action is:

1st line - PipTaz

2nd line - Meropenem

Last resort - Colistin

Colistin is toxic. So much that researchers are asked not to report Colistin as effective. So any new drug should compare itself with the 2nd line Meropenem. Otherwise, they can’t position as a drug comparable to any carbapenem. So it will have impact on uptake or peak revenues.

Why cUTI?

Any drug has to undergo 2 trials usually for the same indication. But US FDA was convinced of the safety of cefepime and zidebactam and allowed a single trial for phase 3 with half the number of patients (500 odd). US FDA wanted to expedite the process as the drug is for unmet need. One of the discussion points from the meeting with US FDA was that to expedite the availability of WCK 5222, initially, asked Wockhardt to take approval in cUTI. The main advantage of cUTI which no other indication offers is one can readily asses the microbiological cure of an antibiotic in a large number of patients which is not possible with pneumonia or blood stream. Any drug it is important to show that there is microbiological cure and clinical cure. Clinical cure can be assessed in all kinds of indication because the parameters are well understood by doctors. But clinical cure also can be subjective. To bring objectivity, US FDA wanted the trials in an indication where you can get strong data on microbiological cure. Microbiological cure is measured by pathogen isolation rate and it should be high in any indication. In blood stream, only 20% isolation is possible. In pneumonia, it is 30-40%. In UTI, the isolation rate is highest at nearly 80%. So it is easy to isolate the pathogen from urine sample than a blood sample.

Not just WCK 5222, many drugs in the last few years have been tested in cUTI.

Orchid’s Enmetazobactam was also tested in cUTI indication:

Ceftazidime Avibactam (which Gufic sells and Orchid makes) was approved in 2014 or 2015 for cUTI but is being used in the US for blood stream infections and pneumonia even though there was no clinical data available.

Even WCK 5222, in the 15 compassionate uses so far, was used for cUTI, Blood Stream, Intra-Abdominal, Pneumonia and the difficult to treat bone & joint infections:

So a drug will be used based on the spectrum and resistance coverage and WCK 5222 seems to have the widest spectrum of all drugs both available and in pipeline.

Wockhardt will anyway have another trial in pneumonia too for WCK 5222 which will happen post the fund raise maybe.

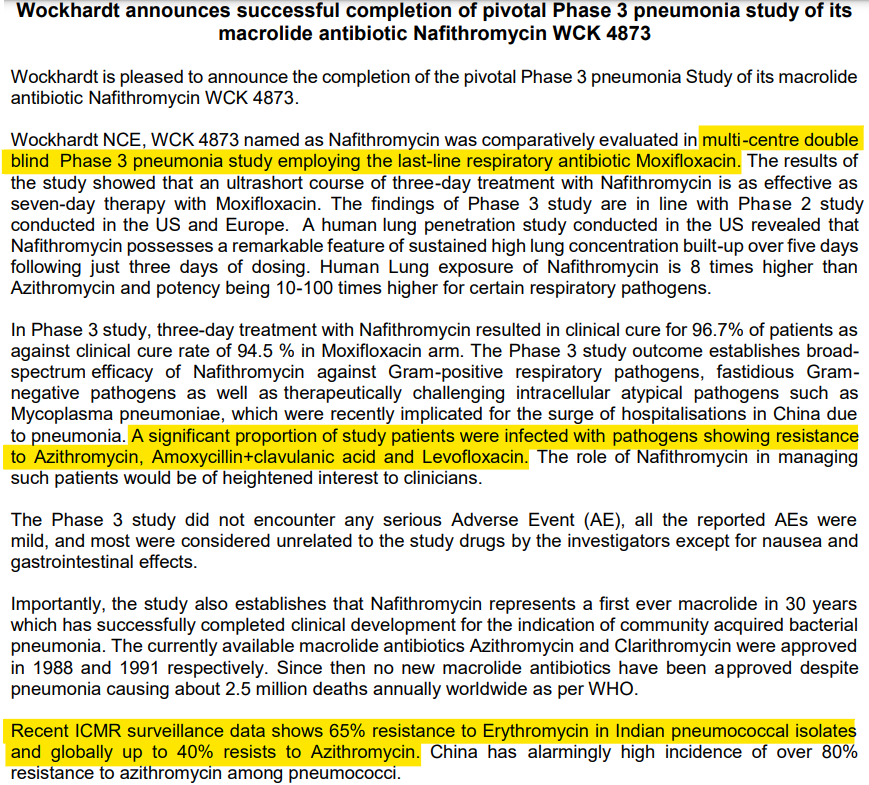

WCK 4873:

Why Moxifloxacin?

For Community Acquired Pneumonia indications, the line of action is:

Oral Cephalosporins are 1st line

Combination with Azithromycin or Erythromycin - 2nd line

Moxifloxacin or Levofloxacin - last line

According to the press release from Wockhardt, pathogens were already showing resistance to Azithromycin, Amoxycillin+clavulanic acid and Levofloxacin.

Efficacy wise Moxifloxacin is the standard of care. It’s the go-to last resort drug, when nothing works. So using Azithromycin or Erythromycin as comparator would have been unethical.

Anyway, this phase 3 was not a global trial. Wockhardt did this so they could launch in ROW. For regulated markets, Wockhardt will do a global phase 3 trial for Nafithromycin.

Wockhardt did the best stress test of WCK 5222 and WCK 4873 by testing against the best options currently available - Meropenem and Moxifloxacin respectively. I dont understand why Mr. Aditya felt otherwise. Would love to get an explanation from him as to how the trial design should have been.

Sajal sir spoke about the past of Wockhardt which is available in public domain. Mr. Habil Khorakiwala talks about all these issues in his book -

https://amzn.eu/d/9EroHh9

Dr. Habil is no saint. I don’t agree with many things he says in the book. He has made mistakes but has been blessed with a bloody good R&D team. Lucky!

In another video, Sajal sir talks about - “Return on capital must be calculated, adjusting for the time-adjusted cost of capital (opportunity cost)”

https://x.com/unseenvalue/status/1767911729965486425?s=20

There are 2 levels of IRR:

- IRR of Wockhardt’s R&D investment - this will be in deep negative currently and should improve depending on how successful WCK 5222 and other NCEs are in future.

- IRR of Wockhardt’s investor - depends on when you bought the stock.

I have already explained in this post as to why the past doesn’t matter for an investor who has bought recently. If you bought in 2004, it matters. But we are in 2024. Market had written off all the R&D investments and was not assigning any value to the NCEs in pipeline when I bought.

I don’t understand why these experts dont go through the research papers or talk to doctors to understand the magic of WCK 5222 and Wockhardt’s R&D potential. Sajal sir does mention about Orchid and Wockhardt’s R&D team having the same origin. But I believe Wockhardt’s R&D team is superior because what Orchid developed - Enmetazobactam - is in a way a cousin of an older drug Tazobactam and hence a BLI Inhibitor in terms of action. What Wockhardt has developed - WCK 5222 - is a NOVEL drug as it exhibits unique BLE enhancer action. Novel ![]()

50 Likes

Formulation or API research != NCE research

You need different expertise and different lens

2 Likes

And the capital raising is activated. QIP issue launch authorized.

1 Like

15f30474-d756-4eb2-b7ea-1c913dc3013c.pdf (bseindia.com)

480 Crores QIP done. Institutional investors including ICICI MF, TATA and Mirae,and MK among others.

4 Likes

Wockhardt planning new funding round - The company had completed a QIP of Rs 480 crore in March 2024.

2 Likes

Drug Discovery Update:

WCK 5222 (ZAYNICH): We continue to recruit more patients for our global clinical trial and

have recruited 392 patients. Recruitment of more than 100 patients has been done during the

current quarter. Clinical Trial study progressing in 9 countries. We have completed 30 patients

for compassionate use after approval of usage by DCGI. The product resulted in 100% cure

and was found to be safe even when administered upto 60 days.

Meropenem Resistance Clinical Trial: DCGI has advised to do a Clinical Trial of 60 patients

study. Patient recruitment process has been initiated. This Clinical Trial would be completed

within the next 8 to 9 months post which WCK 5222 (ZAYNICH) can be launched in India by

early 2025.

WCK 4873 (MIQNAF): The Company is pleased to announce the completion of the pivotal

Phase 3 pneumonia study of its antibiotic Nafithromycin WCK 4873 (MIQNAF). The product

has been filed for DCGI approval which is expected in the Q3FY25. Commercial launch

expected in Q4FY25.

After 30 years, a new oral antibiotic MIQNAF (WCK 4873) will be shortly introduced in India

and it is for Community Acquired Pneumonia with a success rate of over 97%. This will meet

a major antibiotic community need as existing drugs like Azithromycin has high resistance of

60%. It is only a three-day treatment and it has eight times higher lung concentration than

Azithromycin

https://www.bseindia.com/xml-data/corpfiling/AttachLive/f975f9fc-b6fd-4fd7-972e-c8a1ca66ad3e.pdf

9 Likes