That is bad to know. Small and midcap pharma companies are doing better job than Wockhardt. One thing which I found strange is that all the news for Wockhardt is only being quoted by CNBC and no other sources have any other information about it. How come this is possible?

It seems CNBC news was right about Morton Grove.

Please see attached link giving complete synopsis of Wockhardt issues with timeline.

It seems market has now baked in all the bad news related to US FDA and Wockhardt so even if the stock went down by 5% during the day, it is still up as compared to last week !

Disc - Painfully invested and sitting of huge losses! lessons learnt

1 Like

Negative news continues but stock price continues to remain unaffected. Does this mean market knows more than what is in the news or all negative news is already baked in… I expected stock price to fall big time but that did not happen at all

Also the European regulators (Ireland, Germany, UK) dont seem to find issues with Wockhardt’s Plants. Its only the US FDA.

The commentary from management is also elusive on US FDA issues.

Disc. Invested.

Can’t understand the lows in the stock. US business seems to have stagnated and even growing QoQ. Granted that there is a EBITDA loss, but that is more due to high R&D than low profitability. Also, the company has invited USFDA to come and audit the plants.

I was investor in this company for more than 4 years and had this stock as my largest holding at one point in time. After attending AGMs and following up the company’s progress, I gave up on this company in late 2017, which seems like a great decision now  . Earlier this year, I read autobiography of Mr. Khorakiwala (Odyssey of Courage). After reading, it became very clear that promoter is more interested in scoring brownie points by being innovator, filing more patents, receiving more accolades from scientific/pharma community rather than focusing on stakeholder returns

. Earlier this year, I read autobiography of Mr. Khorakiwala (Odyssey of Courage). After reading, it became very clear that promoter is more interested in scoring brownie points by being innovator, filing more patents, receiving more accolades from scientific/pharma community rather than focusing on stakeholder returns  . I wish I was aware of this earlier.

. I wish I was aware of this earlier.

I would request all Wockhardt investors to read this book. Will help you understand the promoters interest and focus

7 Likes

2 Likes

The Print earlier this week said that Modi in a meeting on 2 January warned top pharmaceutical companies like Zydus Cadila, Torrent Pharmaceuticals and Wockhardt to adhere to marketing ethics, and not bribe doctors with foreign trips, gadgets and women.

1 Like

latest press release :-

COVID-19 vaccine partnership with UK Government

Wockhardt, on Aug 3rd, 2020 entered into an agreement with the UK Government to fill finish COVID-19 vaccinesfor which manufacturing will be undertaken at CP Pharmaceuticals, a subsidiary of Wockhardt based in Wrexham, North Wales. As per the terms of the agreement the company has reserved manufacturing capacity to allow for the supply of multiple vaccines to the UK Government in its fight against COVID-19, including AZD1222, the vaccine co-invented by the University of Oxford and its spin-out company, Vaccitech, and licensed by AstraZeneca.

If anyone has viewed results in detail

I want to know shareholder/trackers view here…

Can someone clarify on below point 7. Which subsidiary has made this profit…I can’t see it in consolidated numbers

We did not review the interim financial information of four subsidiaries included in the

Statement, whose interim financial information reflect total revenues of Rs 693.63 crores

(before consolidation adjustments), total net profit after tax of Rs 166.53 crores

(before consolidation adjustments) and total comprehensive income of Rs 165.59 crores

(before consolidation adjustments), for the quarter ended 30 June 2020, as considered in the

unaudited consolidated financial results.

Russia’s sovereign wealth fund, the Russian Direct Investment Fund (RDIF) has reached out to three companies in India — Zydus Cadilla, Wockhardt and Reliance Lifesciences — for manufacturing and trials of Sputnik V, the first registered Covid vaccine in the world.

Disclosure: Invested

1 Like

Anyone still tracking this one?

WCK 5222 is a combination of Zidebactam and Cefepime. This superdrug introduces an entire new class of antibiotic treatment. Earlier US FDA has granted a breakthrough fast track clinical trial and approval process (QIDP status) for this superdrug. This drug meets the urgent threat of Carbopenem-resistant Enterobacteriaceae and serious threats like Multidrug-resistant Acinetobacter, Extended spectrum β-lactamase producing Enterobacteriaceae (ESBLs), Drug-resistant Salmonella typhi and Multidrug-resistant Pseudomonas aeruginosa. This is the categorisation based on which US FDA has given this special QIDP status. Wockhardt has taken this antibiotic for a worldwide clinical development. This drug in scientific community is well documented by a large number of oral and scientific poster presentation at ASM Microbe at Boston and ECCMID at Amsterdam and ID week at New Orleans.

2 Likes

“Shareholders, however, approved a proposal to raise up to Rs 1,600 crore through a qualified institutions placement (QIP) to eligible investors through an issuance of shares or other eligible securities.”

Read more at:

1 Like

Before I proceed, credit where its due - This idea originated with @Anant whose inputs prodded me to look deeper into this story and @Sanjay_Kumar_E who is the nuts and bolts man whose ability to wade in deeper than the rest regardless of industry is simply unparalleled. I am simply piecing together everything in a way I can explain to my 10 year old son.

Understanding Antibiotics

I usually avoid stocks with large pledging (I assume fraud), stay away from businesses that are complex to understand (complexity needn’t be in comprehension of the business but the dynamism of its moving parts as well) and ignore turnarounds. This one has got all these in troves so should be a strong avoid, yet here I am, ready to make a fool of myself.

The following is my understanding of things - it is aimed at people like me with no prior medical background and is written in layman language to develop an intuition as to how things work.

To understand WCK 5222, it is important to have a lot of pre-requisites. It is probably these pre-requisites that are keeping people out.

Antibiotics are class of compounds that are used to treat bacterial infections. All of us have had one at some point of time. Azithromycin is probably the most common we would have been prescribed at some point. Most of us have heard of Penicillin which is the first antibiotic discovered by Fleming in 1928, by accident and developed into practical antibiotic much later in 1940s. Since then it has revolutionised medicine right from its use in WW-II.

Antibiotics typically work by killing (bactericidal) or impeding growth (bacteriostatic). They do this by compromising integrity of cell wall or messing with the processes within the cell.

Since penicillin, we have discovered several classes and numerous antibiotics that work against various types of bacteria. Important thing to understand is that, as our antibiotics are evolving, so are the bacteria themselves as drug resistant varieties proliferate, needing newer antibiotics

A lot of names get thrown around and its easy to get lost in names of antibiotics. It is always easier for our brains to view things in categories based on some attributes.

| Class | Examples | How they work? |

|---|---|---|

| Penicillins | Penicillin, Amocixillin, Ampicillin | Interferes with cell wall synthesis |

| Cephalosporins | Cephalexin, Ceftriaxone | Disrupts cell wall formation |

| Macrolides | Erythromycin, Clarithromycin, Azithromycin | Inhibits protein synthesis |

| Fluoroquinolones | Ciprofloxacin, Levofloxacin, Moxifloxacin | Inhibits DNA replication |

| Tetracyclines | Tetracycline, Doxycycline | Interferes with protein synthesis |

| Carbapenems | Imipenem, Meropenem | Inhibits cellwall synthesis in MDR (multi-drug resistant) bacteria. Most potent class |

There are others like Sulfonamides, Aminoglycosides, Glycopeptides, so this is not an exhaustive list.

Few things to understand before we proceed further

In Vitro vs In Vivo

In vitro experiments are conducted outside a living organism, typically in a lab, with lab equipment (petri dishes and test tubes) while In vivo are studies conducted with living organisms (rats, mice). Important thing to understand is that even if an experiment is successful In Vitro, it could fail In Vivo, for various reasons.

MIC

MIC stands for ‘Minimum Inhibitory Concentration’. It is the lowest concentration of the drug that inhibits growth of a given strain of bacteria, typically expressed in micrograms/milliliter (μg/mL). Needless to say, this varies a lot between drugs and strains of bacteria and there are standard ways of representation of a AST (Antibiotic susceptibility testing).

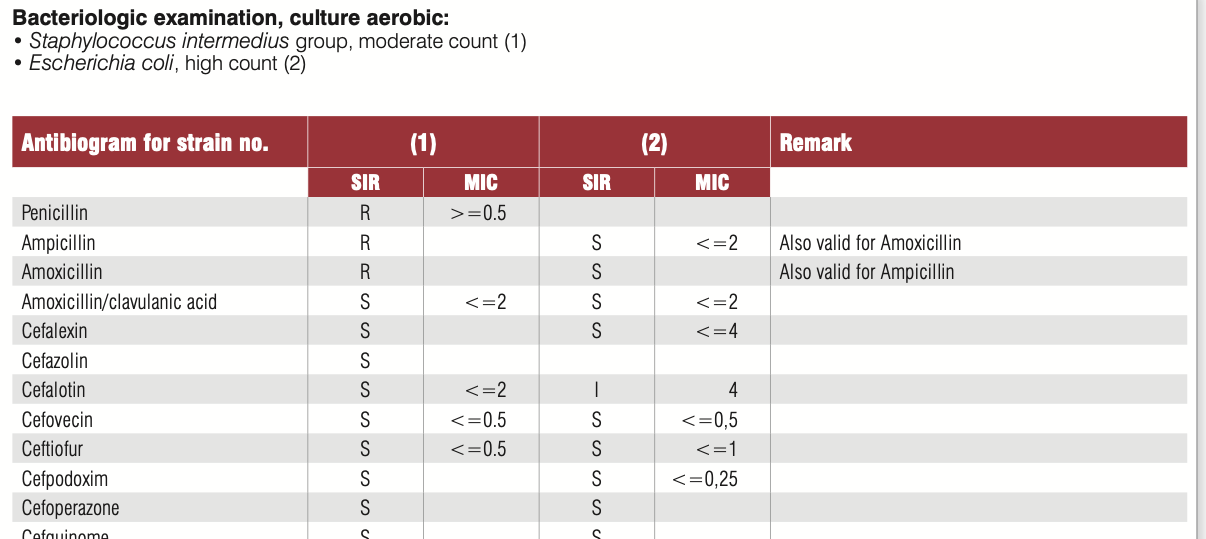

A typical AST result looks like this.

In this, the SIR column is one of S/I/R which is Susceptible (Bacteria is susceptible to the dosage), Intermediate (May be effective at higher dosage) and Resistant (Drug not effective). MIC values usually have a ≤ sign when organism is susceptible. The above tables has two specimens (1) and (2) and have. SIR and MIC for the these two specimens against various antibiotics. Penicillin is not effective against (1) while Cefalotin is effective at a MIC of 2 μg/mL.

You will also notice that several different antibiotics can be effective against a microorganism. How does one choose which one to use? is the next natural question that arises

PK/PD

Just because a drug is effective In-vitro doesn’t mean it will be In-vivo. The reasons can be many but fall into these two categories Phamacokinetics (PK) and Pharmacodynamics (PD). In layman language - PK is what the body does to the drug and PD is what the drug does to the organism.

So Pharmacokinetics (PK) is the kinetics of drug absorption, distribution from where its administered, Metabolism within the body (how its used up) and Excretion (How its removed). As you can see, all these will in turn affect how much of the drug is available in the tissue or plasma to come close to the In vitro experiment if it was in fact successful

Pharmacodynamics (PD) deals with antimicrobial activity that is desirable (inhibition or killing) and undesirable (adverse effects to the host). We cannot keep increasing the concentrations of the drug if it is adverse to the host or worse, it helps to develop resistance in the microorganism thereby making it useless.

Breakpoints

This segues us nicely into the concept of “Breakpoints”

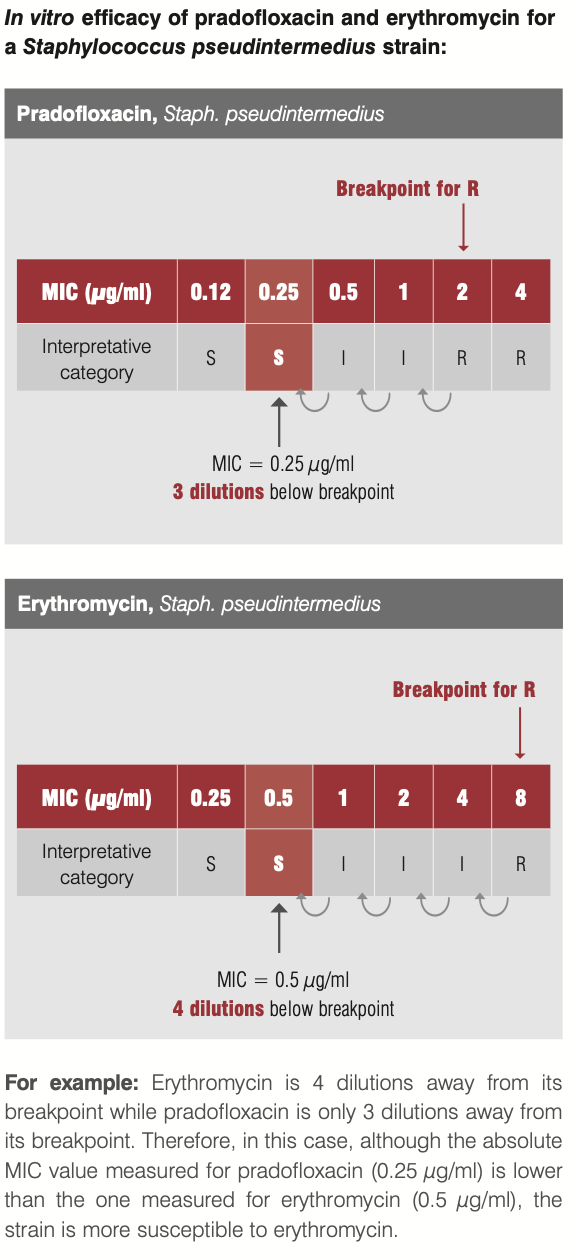

To get back to the question of which antibiotic to use when bacteria is showing sensitivity to multiple antibiotics, our intuition should tell us that lower the MIC, the better it might be. Our intuition couldn’t be more wrong.

Take this eg. of efficacy of pradofoxacin and erythromycin against staph infection. Though our intuition may tell us Pradofloxacin at MIC of 0.25 should be better than Erythromycin at 0.5, it is the latter that is a better drug since its 4 dilutions away from the breakpoint where the organism starts developing resistance to the drug.

But who sets these breakpoints? These are internationally governed by bodies like CLSI (Clinical and Lab Standards Institute), EUCAST, FDA. These get reviewed periodically based on scientifically available evidence.

If a drug can work at much lower dilutions away from breakpoint, it might be preferred - all else remaining equal

So hopefully that helps to develop the intuition between In Vitro and In Vivo

MDR/XDR

MDR and XDR stand for Multi-drug resistant and Extremely drug-resistant. You would have noticed in the Antibiotics table that Carbapenems are used in XDR cases where all else fails

Pharmacodynamics

Re-visiting this again separately, since this is important to understand further. So we know that drug is effective at MIC and above but below breakpoint. But it doesn’t tell us for how long and how much higher it needs to stay to be effective.

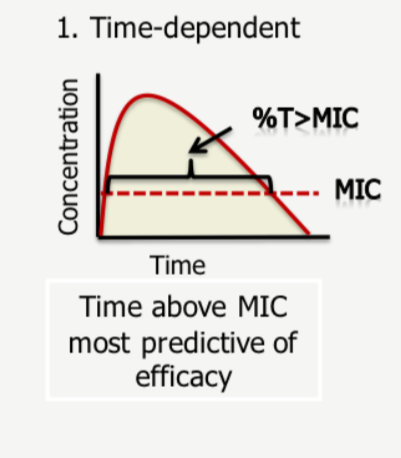

Based on In Vitro experiments, the effect of the drug on the microorganisms are classified as time-dependent or concentration-dependent or AUC dependent.

Time-dependent bactericidal effect

The drug needs to stay above MIC for a certain amount for time (dosing interval) for it to be effective. Typically drugs that interfere with cell-wall of the bacteria (penicillins, carbapenems) need to stay above MIC for a period of time.

So the percentage of time the drug spends above the MIC value is crucial here.

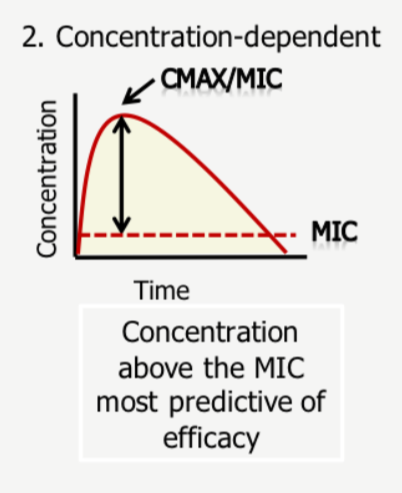

Concentration-dependent bactericidal effect

Max MIC or CMAX is the most-important predictor of success here. So achieving max safe concentrations at the site of infection is crucial

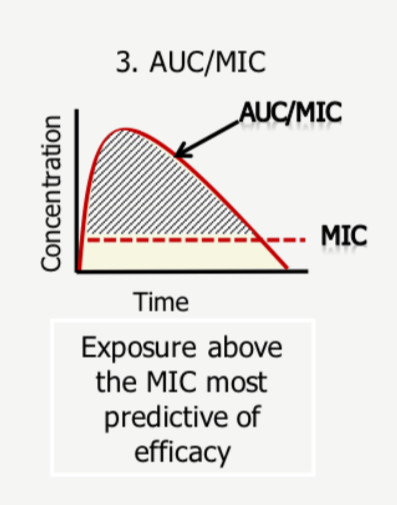

AUC/MIC

This is a combination of time-dependent and concentration-dependent as it requires a cumulative exposure of certain concentration over a period of time

AUC simply stands for Area under curve - so efficacy depends on maximising this area - its intuitive to understand here that if CMAX or T% is low, this treatment becomes ineffective - so both needs to be maximised to maximise the area under curve.

When CLSI sets breakpoints, it goes by this information from the reports - what it specifically looks for to set a susceptible breakpoint is a the highest MIC achieved for efficacy in 90% of patient population

There are more nuances here in terms of MIC and %T which we can get into at a later point but for now this should suffice.

The effectiveness of the drug on the bacteria is measured through base-10 log notations. So 1 log would be a 10^1 reduction and 2-log would be 10^2 reduction and so on in orders of magnitude. So in a colony of 1 million microbes, 1-log would achieve a 90% kill, 2-log a 99% kill and 5-log a 99.999% kill and so on. FDA is happy with a 1-log kill (90% reduction) to approve a drug.

This much is of course is table-stakes to understand papers on WCK-5222 - in terms of chances of approval, in terms of market size and so on (if it can replace existing drugs, market size will be bigger). I will try to summarise the rest in another post or two next week, if time and interest permits.

References:

microbiology-guide-interpreting-mic.pdf (235.1 KB)

Understanding Pharmacokinetics (PK) and Pharmacodynamics (PD).pdf (437.6 KB)

Disc: Invested (This is just an academic exercise at understanding antibiotics and then on to WCK 5222 and hopefully inspire others to pursue this. This could be a very high-risk bet, so please don’t go by fancy jargon in this post to plonk your money. Effort required to understand doesn’t translate to returns, and in fact could be inversely correlated)

UPDATE: Part 2 is here

79 Likes

4 Likes

Hello Everyone,

First of all, kudos on such great research on this topic. It is definitely quite insightful!

I had some questions regarding this sector. Coming from a non-science background, they might be a little basic but would really be helpful for me to delve deeper into this topic.

- What is the next stage after the Clinical trials are done? And what might be the success rate of a drug clearing Phase III of these trials?

- After the drug has received FDA approval, what shall be next step? Will the innovator company manufacture this drug on its own, or outsource/license other companies? How much % of revenue oppurtunity could Wockhardt have from the total market of this drug?

- What could be the timeline for this drug (WCK 5222) to be in the market, my assumption is atleast 2 years. But since it is being used on humanitarian grounds already, can we expect the authorities to expedite the approval process?

Thankyou so much!

Interesting take from Sajal on WCK 5222 on twitter

1 Like

With all due respect to him, here is my take:

Wockhardt has spent ~3900 Crs between 2004 - 2023. (Source: Ace Equity)

| Wockhardt R&D (Rs. Crs) | Dec-04 | Dec-05 | Dec-06 | Dec-07 | Dec-08 | Mar-10 | Mar-11 | Mar-12 | Mar-13 | Mar-14 | Mar-15 | Mar-16 | Mar-17 | Mar-18 | Mar-19 | Mar-20 | Mar-21 | Mar-22 | Mar-23 | Total |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Capital Expenditures | 19 | 21 | 77 | 91 | 78 | 80 | 77 | 129 | 19 | 43 | 21 | 51 | 21 | 1 | 3 | 1 | 508 | 361 | 11 | 1613 |

| Recurring Expenditures | 53 | 60 | 51 | 35 | 30 | 40 | 33 | 45 | 201 | 198 | 241 | 250 | 238 | 189 | 169 | 137 | 114 | 95 | 86 | 2265 |

| Total R&D | 71 | 81 | 128 | 127 | 108 | 120 | 110 | 174 | 219 | 242 | 263 | 301 | 259 | 190 | 172 | 138 | 622 | 456 | 97 | 3878 |

| R&D as a % of Sales | 5.7% | 5.7% | 7.4% | 4.8% | 3.0% | 2.7% | 2.9% | 4.0% | 3.9% | 5.0% | 5.9% | 6.8% | 6.4% | 4.8% | 4.8% | 4.8% | 23.0% | 14.1% | 3.7% |

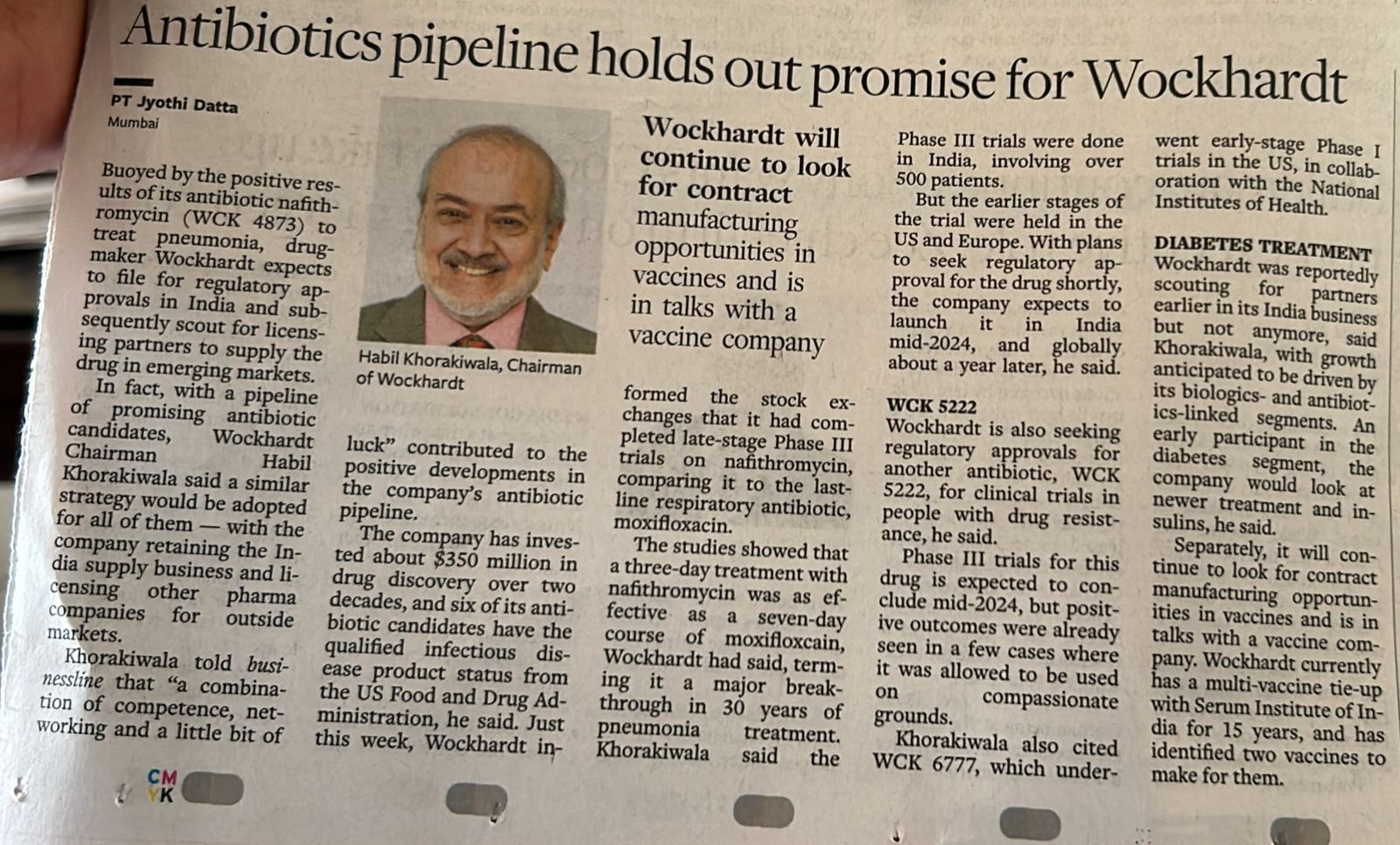

Even in a recent interview, Mr. Khorakiwala had said they have spent $350 Mn in 2 decades:

And if you have read his book, he states that the R&D was spent on 3 things - 1/3rd on Antibiotics, 1/3rd on Biologics and 1/3rd on rest. Something like that. I dont remember. It would be great if someone who has read the book provides the exact statement.

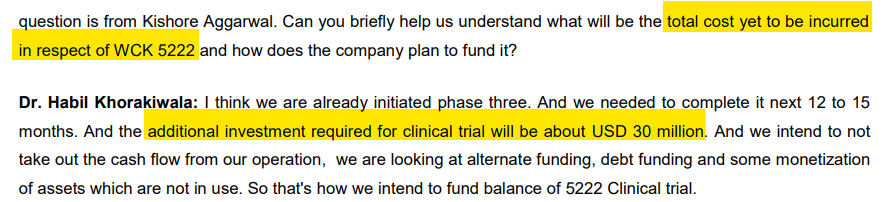

Conservatively, let us assume 50% of all the R&D was on Antibiotics. The R&D required to finish Phase 3 trials for WCK 5222 is around $30 Mn as stated in the Q3 FY23 concall by mgmt.

Calculating the IRR for this investment using only one NCE’s - WCK 5222 - cash flows assuming peak global sales of $1 Bn and 20% royalty for Wockhardt. Just their flagship NCE is enough to give them a 10% IRR. Throw in 4 more, IRR could be a decent 15% for someone who invested in 2004.

| Rs. Crs | Cash Flows | Sales of WCK 5222 |

|---|---|---|

| Dec-04 | -36 | |

| Dec-05 | -41 | |

| Dec-06 | -64 | |

| Dec-07 | -63 | |

| Dec-08 | -54 | |

| Mar-10 | -60 | |

| Mar-11 | -55 | |

| Mar-12 | -87 | |

| Mar-13 | -110 | |

| Mar-14 | -121 | |

| Mar-15 | -131 | |

| Mar-16 | -151 | |

| Mar-17 | -129 | |

| Mar-18 | -95 | |

| Mar-19 | -86 | |

| Mar-20 | -69 | |

| Mar-21 | -311 | |

| Mar-22 | -228 | |

| Mar-23 | -49 | |

| Mar-24 | -250 | |

| Mar-25 | 0 | 0 |

| Mar-26 | 0 | 0 |

| Mar-27 | 200 | 1000 |

| Mar-28 | 400 | 2000 |

| Mar-29 | 600 | 3000 |

| Mar-30 | 800 | 4000 |

| Mar-31 | 1000 | 5000 |

| Mar-32 | 1200 | 6000 |

| Mar-33 | 1400 | 7000 |

| Mar-34 | 1600 | 8000 |

| Mar-35 | 1600 | 8000 |

| Mar-36 | 1600 | 8000 |

| Mar-37 | 1600 | 8000 |

| **IRR | 10.2%** |

Very rough estimates. WCK 5222 peak sales could only be $500 Mn and not $1 Bn.

The main point though is, this IRR should matter for an investor who bought Wockhardt anytime between 2004 to 2023. Market has almost written off all the investments.

Anyone who bought recently will enjoy the benefits of all these investments of 2 decades.

While Sajal sir is right in saying that there is low probability of US FDA approvals in NCEs (apparently only 17% of Phase 3 drugs get final approval), Wockhardt either through luck or through capital (human and financial) or a bit of both, they have developed 5 NCEs and all of them have QIDP status which means US FDA knows their importance. Even better, the Phase 1 trial of WCK 6777 was funded by NIH. On WCK 5222, I am very confident that it will be approved by FDA and so are the doctors in India I have spoken to. WCK 5222 should be successful and the cash flows will take care of global trials for all other NCEs.

Also, the position size can take care of the risks.

48 Likes

wow, .thank you so much sir for your kind efforts to demonstrated complex topic so easy to understand to all . being a biologist i cannot summarize in this in lay man language way. simply superb ![]()

![]()

3 Likes

Tweet says time value of 10000crs , not absolute value of 10000crs, I guess Sajal calculted it as opptutunity cost of 3900crs thats invested over time