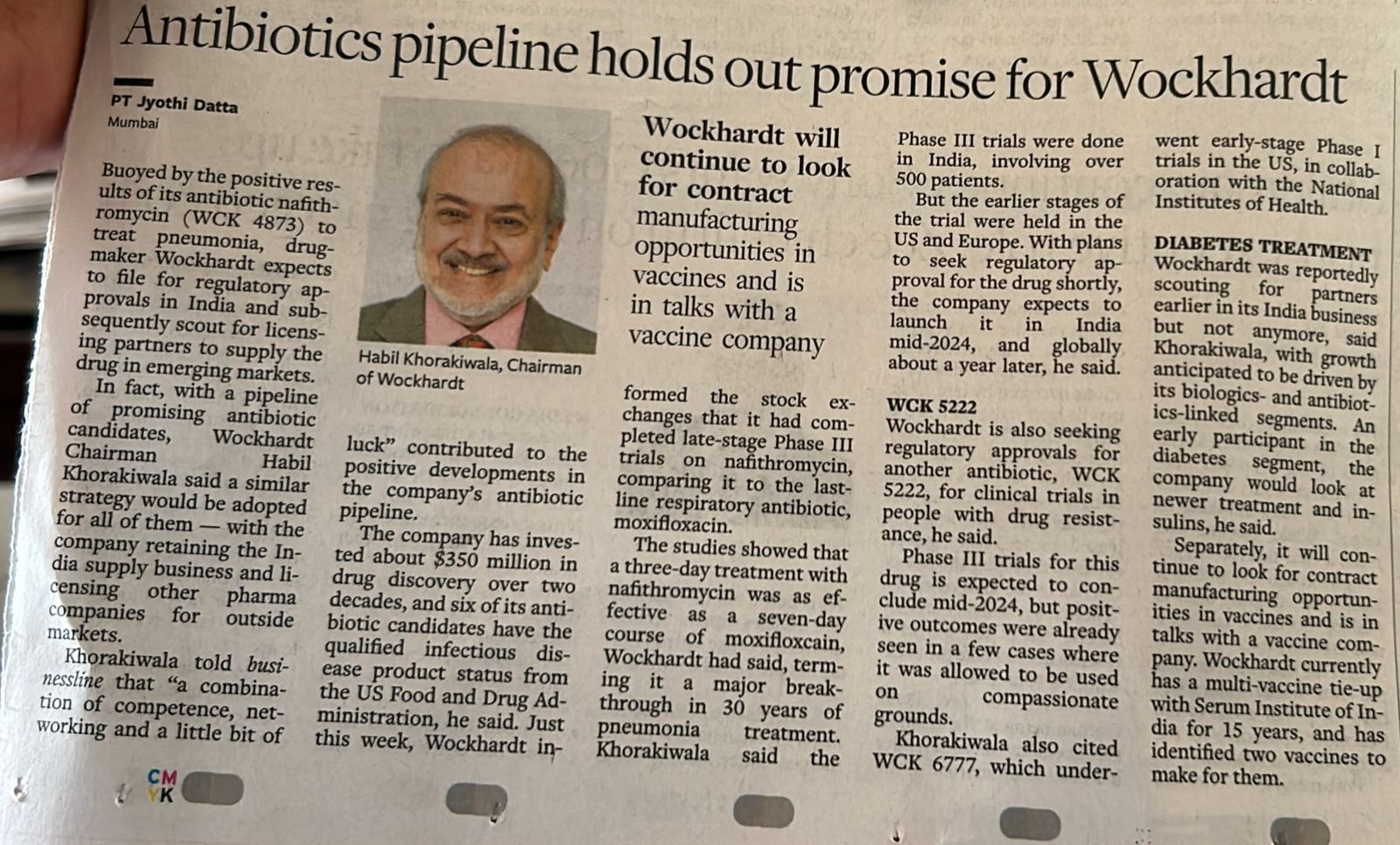

With all due respect to him, here is my take:

Wockhardt has spent ~3900 Crs between 2004 - 2023. (Source: Ace Equity)

| Wockhardt R&D (Rs. Crs) | Dec-04 | Dec-05 | Dec-06 | Dec-07 | Dec-08 | Mar-10 | Mar-11 | Mar-12 | Mar-13 | Mar-14 | Mar-15 | Mar-16 | Mar-17 | Mar-18 | Mar-19 | Mar-20 | Mar-21 | Mar-22 | Mar-23 | Total |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Capital Expenditures | 19 | 21 | 77 | 91 | 78 | 80 | 77 | 129 | 19 | 43 | 21 | 51 | 21 | 1 | 3 | 1 | 508 | 361 | 11 | 1613 |

| Recurring Expenditures | 53 | 60 | 51 | 35 | 30 | 40 | 33 | 45 | 201 | 198 | 241 | 250 | 238 | 189 | 169 | 137 | 114 | 95 | 86 | 2265 |

| Total R&D | 71 | 81 | 128 | 127 | 108 | 120 | 110 | 174 | 219 | 242 | 263 | 301 | 259 | 190 | 172 | 138 | 622 | 456 | 97 | 3878 |

| R&D as a % of Sales | 5.7% | 5.7% | 7.4% | 4.8% | 3.0% | 2.7% | 2.9% | 4.0% | 3.9% | 5.0% | 5.9% | 6.8% | 6.4% | 4.8% | 4.8% | 4.8% | 23.0% | 14.1% | 3.7% |

Even in a recent interview, Mr. Khorakiwala had said they have spent $350 Mn in 2 decades:

And if you have read his book, he states that the R&D was spent on 3 things - 1/3rd on Antibiotics, 1/3rd on Biologics and 1/3rd on rest. Something like that. I dont remember. It would be great if someone who has read the book provides the exact statement.

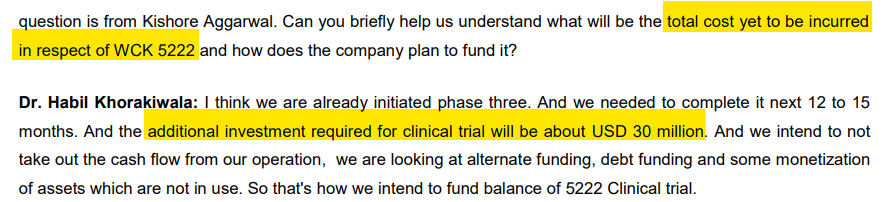

Conservatively, let us assume 50% of all the R&D was on Antibiotics. The R&D required to finish Phase 3 trials for WCK 5222 is around $30 Mn as stated in the Q3 FY23 concall by mgmt.

Calculating the IRR for this investment using only one NCE’s - WCK 5222 - cash flows assuming peak global sales of $1 Bn and 20% royalty for Wockhardt. Just their flagship NCE is enough to give them a 10% IRR. Throw in 4 more, IRR could be a decent 15% for someone who invested in 2004.

| Rs. Crs | Cash Flows | Sales of WCK 5222 |

|---|---|---|

| Dec-04 | -36 | |

| Dec-05 | -41 | |

| Dec-06 | -64 | |

| Dec-07 | -63 | |

| Dec-08 | -54 | |

| Mar-10 | -60 | |

| Mar-11 | -55 | |

| Mar-12 | -87 | |

| Mar-13 | -110 | |

| Mar-14 | -121 | |

| Mar-15 | -131 | |

| Mar-16 | -151 | |

| Mar-17 | -129 | |

| Mar-18 | -95 | |

| Mar-19 | -86 | |

| Mar-20 | -69 | |

| Mar-21 | -311 | |

| Mar-22 | -228 | |

| Mar-23 | -49 | |

| Mar-24 | -250 | |

| Mar-25 | 0 | 0 |

| Mar-26 | 0 | 0 |

| Mar-27 | 200 | 1000 |

| Mar-28 | 400 | 2000 |

| Mar-29 | 600 | 3000 |

| Mar-30 | 800 | 4000 |

| Mar-31 | 1000 | 5000 |

| Mar-32 | 1200 | 6000 |

| Mar-33 | 1400 | 7000 |

| Mar-34 | 1600 | 8000 |

| Mar-35 | 1600 | 8000 |

| Mar-36 | 1600 | 8000 |

| Mar-37 | 1600 | 8000 |

| **IRR | 10.2%** |

Very rough estimates. WCK 5222 peak sales could only be $500 Mn and not $1 Bn.

The main point though is, this IRR should matter for an investor who bought Wockhardt anytime between 2004 to 2023. Market has almost written off all the investments.

Anyone who bought recently will enjoy the benefits of all these investments of 2 decades.

While Sajal sir is right in saying that there is low probability of US FDA approvals in NCEs (apparently only 17% of Phase 3 drugs get final approval), Wockhardt either through luck or through capital (human and financial) or a bit of both, they have developed 5 NCEs and all of them have QIDP status which means US FDA knows their importance. Even better, the Phase 1 trial of WCK 6777 was funded by NIH. On WCK 5222, I am very confident that it will be approved by FDA and so are the doctors in India I have spoken to. WCK 5222 should be successful and the cash flows will take care of global trials for all other NCEs.

Also, the position size can take care of the risks.