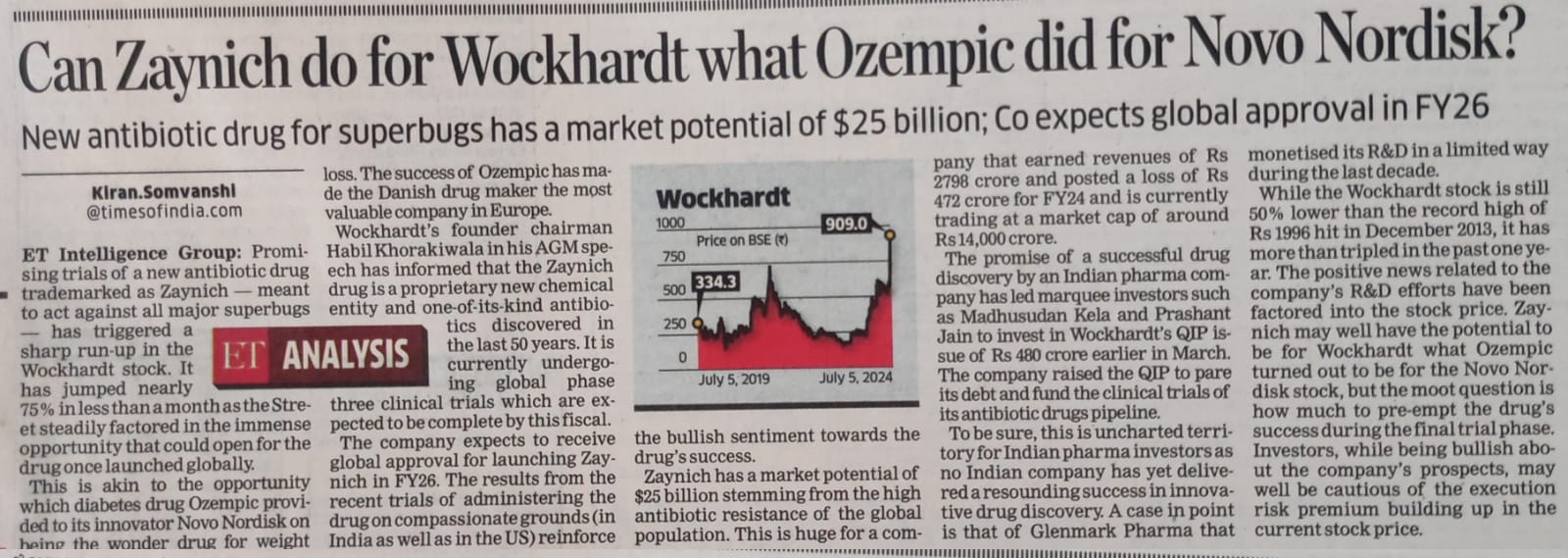

Globally renowned US body Clinical and Laboratory Standards Institute (CLSI) awards high susceptibility breakpoints to Zaynich (Zidebactam/Cefepime- WCK 5222). This is 1st time ever that an antibiotic has been granted a susceptible breakpoint of as high as 64 mg/L for all the three families of Gram negative pathogens; Enterobacterales, Pseudomonas and Acinetobacter.

3 Likes

I also loved this one.

WCK 5222 has been used successfully for a US patient!

Cleared out a nasty infection of metallo-β-lactamase-harbouring P aeruginosa in a young cancer patient, who was administered the drug on compassionate grounds, since there were no other treatment options left. 4 weeks, all clear, and well tolerated.

Feel proud that an Indian company has innovated like this.

Disclosure: Invested from lower levels, this is one of my investments “from the heart” (though I know one should never do this, what’s the fun if you don’t listen to your heart?)

13 Likes

Hi Shreya28, tell me one thing, if WCK5222 being NCE, if gets all clinical trials through, will it get PRODUCT PATENT and exclusivity of 15-20-25 years for global markets?

Short answer, the patent for WCK5222 expires in 2031-32.

Longer answer – the game of patents.

The patent system is very complex. In general companies file for multiple patents for any potential drug protecting different aspects of the chemical, e.g. its composition, X-ray diffraction, uses, delivery devices, process for manufacturing, etc. For example, the patent for composition, preparation and antimicrobial use of bicyclic-acyl hydrazides expires in 2032. One member of this family of hydrazides is zidebactam - the patent for zidebactam/cefepime expires in 2034. There are many other patents related to this family of chemicals, all of which are publicly available information.

However, the interesting game starts once a patented drug is approved by the FDA. Companies file hundreds of patents to keep their drugs out of the hands of generic competition and prolong their profits – this is called “evergreening” which is unethical but widely accepted tactics. Competitors sue the original drugmakers to get small tweaks and generics to the market. Moreover, if the drug is a blockbuster, then the game becomes more competitive: Multi-billion dollar companies will go through every line of their patent filings to find loopholes to get their hands on the drug, often using hostile takeovers or out-of-court settlements. The main question is not the actual expiry date of the patents, but whether the company can stand up to this “game”.

18 Likes

2 Likes

3 Likes

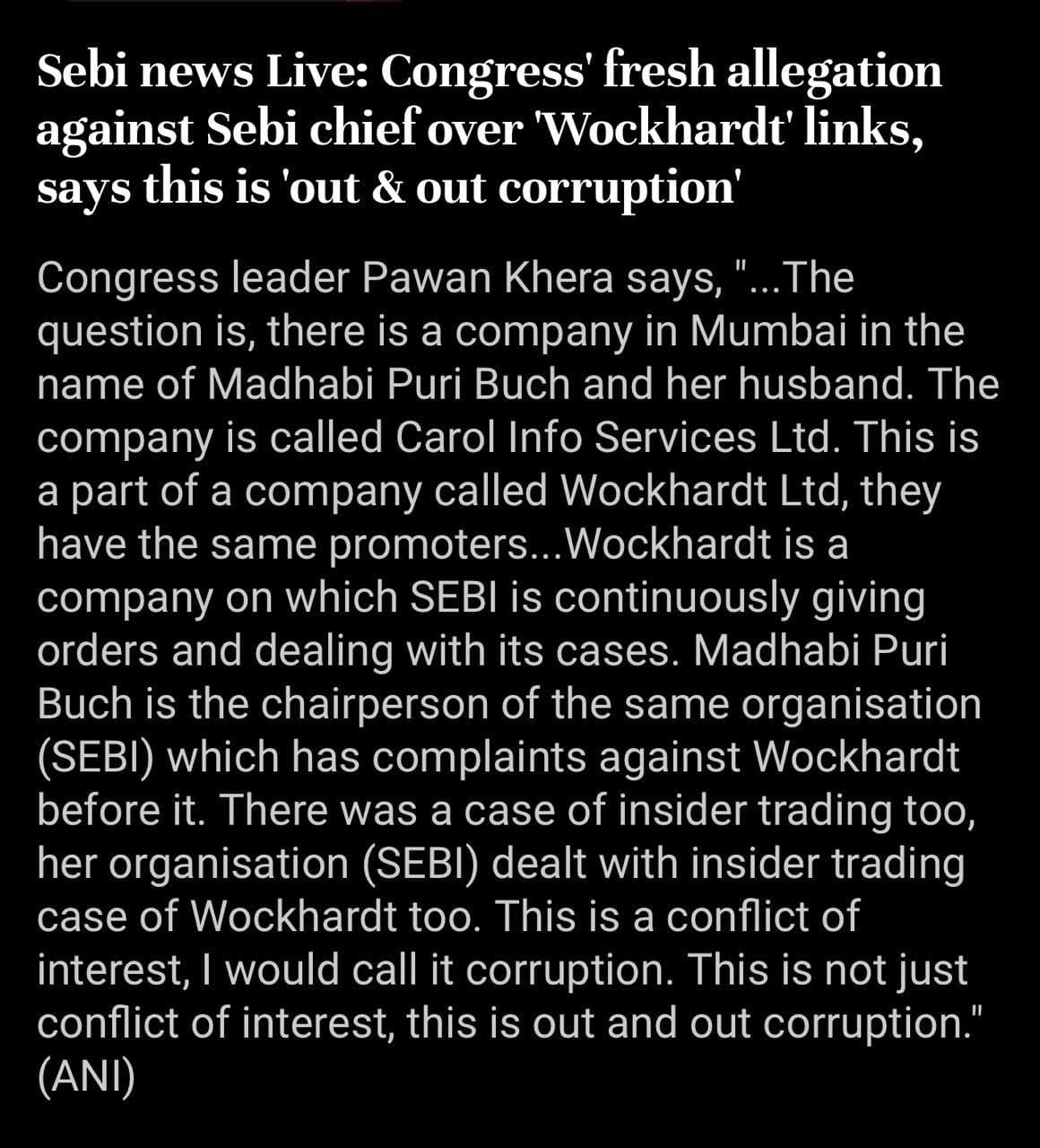

whats the implication of this approval…would appreciate some clarity on this

So the future sebi chief should have nothing to do with anybody who has less than 6 degrees of separation from any past , present and future listed company . Renting premises to a subsidiary of a listed company(probably not…only same owner) can not be legally or morally corrupt unless one can show that the rent is bribe . Very similar to the ICICI allegation, investors should ignore the noise unless they are invested in Madhabi Buch instead of the company being dragged into the political mudbath.

6 Likes

6 Likes

In the interview Mr. Khorakiwala gave an estimate of size of WCK-5222. According to him there are 700k patients in US along and current line of antibiotics cost around $8-10k/treatment.

8 Likes

4 Likes

New investor presentation released

4621e1ef-09ad-4f6c-aff3-b3eff866e4e1.pdf (3.9 MB)

1 Like

What has led to sudden increased investor interest? Have the phase 3 trials completed? Is there something the market knows.

There is a 99% chance of new drug approval now, launch in Feb 2025, as oer MD market is 80 B USD which is huge, lot of growth in intrinsic value going forward, WCK4777 is also fast tracked, Wockhardt has three more molecules in QIDP, this might become most valuable company of Pharma sector based on opportunity size. First indian company to launch a drug.

Disclaimer: holding from 600 levels in core portfolio for long long term.

7 Likes

It is really a huge figure.. Did he really quoted this figure?? Please submit the source if you are having..

1 Like

Was this mentioned in the last investor meet? There has been increased interest since last week.

Also, what are some of the risks currently? Their FDA trials (phase 3) have been successful so far, and 90% complete. Once the trials get completed, what would be the expected timeline for revenue to start hitting company books?

2 Likes

Yup, Khorakiwala mentioned in one of interview, look for it.

1 Like

USA has 700K patients with 10K USD treatment cost, across world 6 million patients annually for WCK5222. Patent for 20 years.

Out licensing, Royalty, direct sale for 20 years, heavy moat in place. One drug will be launched shortly in India replacing azithromycin in severe resistant cases.

WCK4777 fast tracked. How knows Wockhardt get CDMO shares as well.![]()

![]()

8 Likes