Now we have got a 13 year big multi year breakout above 177 and now we are well and truly on the way to ATH of 423 if the following things happen over next 6 months

Machine arrival

Order notification

Commercial production commencement

Clarity and Funding for atleast next 600 mw

if these things happen we are in for a minimum 2-3x in next 6 months

this is why. When a company starts doing an ATH production, usually ATH price gets achieved and hence that gut feeling of 6 months

Thank you, Apoorv, for the wonderful analysis so far. For the topline of 700-800 Cr, even if one gives a P/S of 2, this looks lucrative. Do you have any EBITDA benchmarks? Historical operating margins don’t give any reasonable range for any back-of-the-envelope calculations.

Anyone noticed the updated products portfolio in websol’s website?. I noticed Mono PERC M10 & M12 cells and modules just two days back and surprisingly enquiry tab was there.

Now it is showing like “website under construction”. Have they started production?

Of course, negative Q2 results expected but will they announce any big bang developments along with Q2 numbers?

Yes. The history was not good so as the whole Solar industry in India. A small company like Websol arrived to market with just 1 MW capacity way ahead of its time (Globalization year 1990) and suffered due to unfavorable policies. The traction in this sector was visible late 2010 only. So, there is nothing wrong in calling a spade a spade. Much respect to Vijay malik Sir.

However, the market is always a forward looking one. So, the shareholders must be interested in the future of the business and its potential to create a meaningful value. let’s hope the management walks the talk. It’s just my opinion. Hope the below image summarize this discussion.

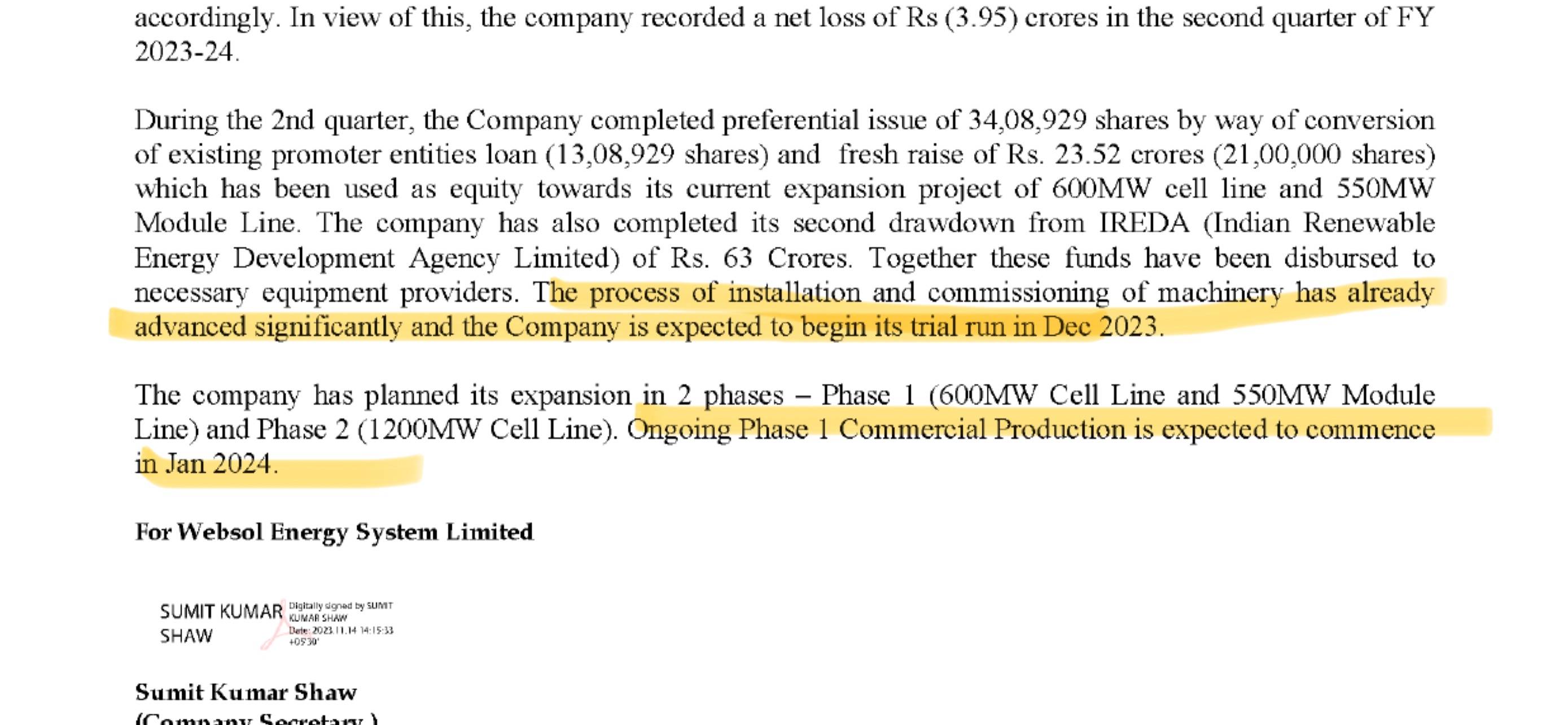

Result is on expected line with a surprise announcement.

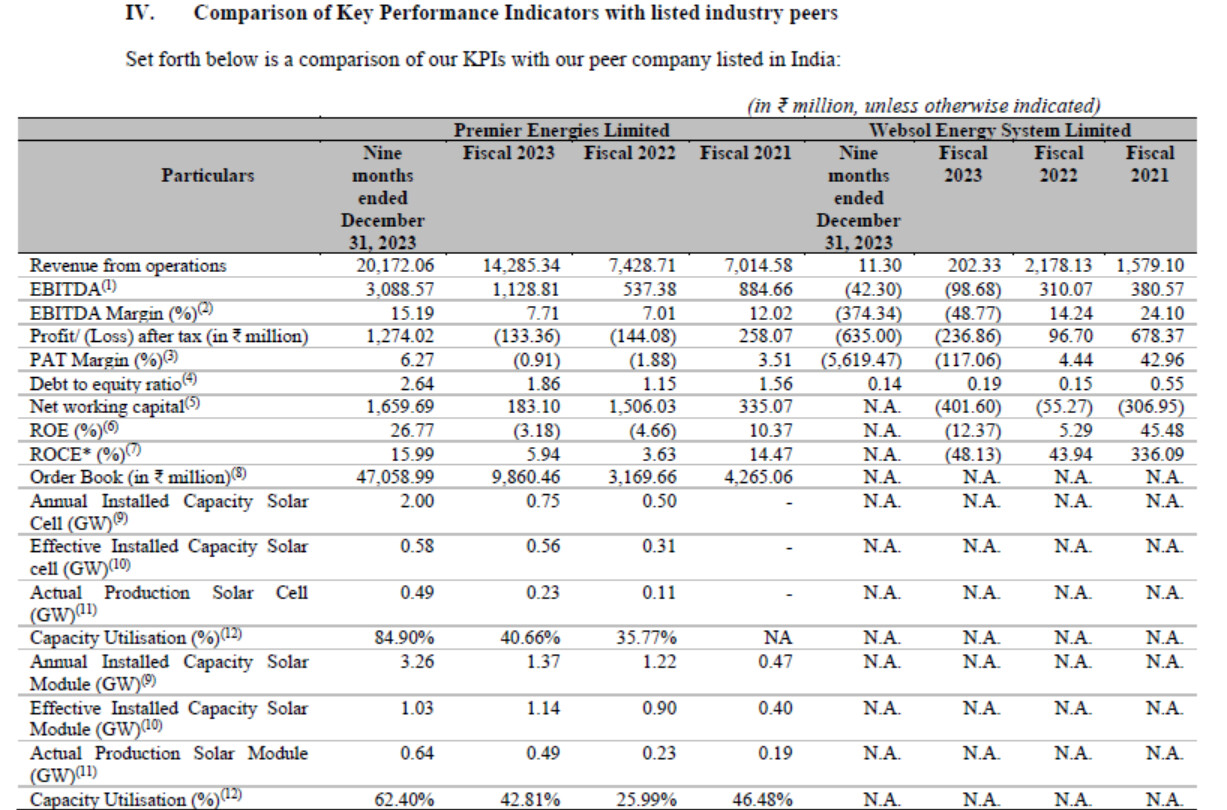

Please find below an excerpt from Waaree Energies Ltd DRHP. They recognised Websol as the only listed peer to them as on december 2023. However, it looks like they picked websol to project good numbers to the investors as websol figures are dented due to ongoing capex and old line impairment loss.

So, listing of Waaree should rerate Websol as Websol’s goal post has changed from Cell- Module line to integrated line starting from Ingots -wafer-Cell-Module (Polysilicon would be procured from China or local manufacturers). if this happens, Both waaree and Websol would share the same business segments and both will procure polysilicon outside. of course, there will be a huge difference in final module capacities.

Let us hope Websol starts producing numbers at the time of listing of Waaree energies Ltd.

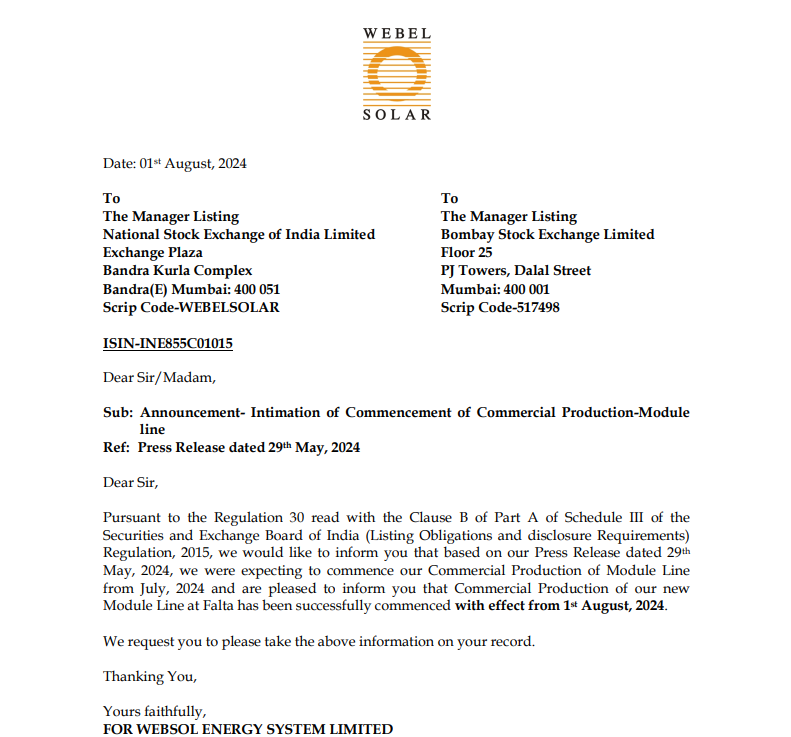

Company announced the Commencement of Commercial production of new Mono PERC Cell line of 600 MW capacity from today. They have already found buyers for the entire production of next 45 days in this FY. (Approx. 80MW). Let’s wait and watch the further developments.

A long long way from that update of mine. Now the next leg of growth should kick in next 2-3 years

I see rhis as Potentially 5000cr topline revenue generating company. 5-6 Gw capacity in next 3-4:years.

Should always be in growth mode and the valuation is free for you to give. At 5 mcap to sales. We are looking at a 10 bagger from here.

The board has approved the issue of 12,10,000 convertible warrants on preferential basis to Promoter Group at Rs.530/Share. So, infusion of Rs. 64.13 Crs for Approx. 2.8% of total shares. Interesting.

One more DRHP from another company which has presence in Cell + Module manufacturing compares KPI’s with Websol Energy. India made Solar Cell is the hottest commodity in the world now.

As we are aware that Websol is at an inflection point, a huge uptick of 11X in share price shows the same. Management successfully executed the Cell line which is believed to be the most complex process.

I believe the execution of Module line is a cakewalk for the management. Hope the production announcement comes soon.

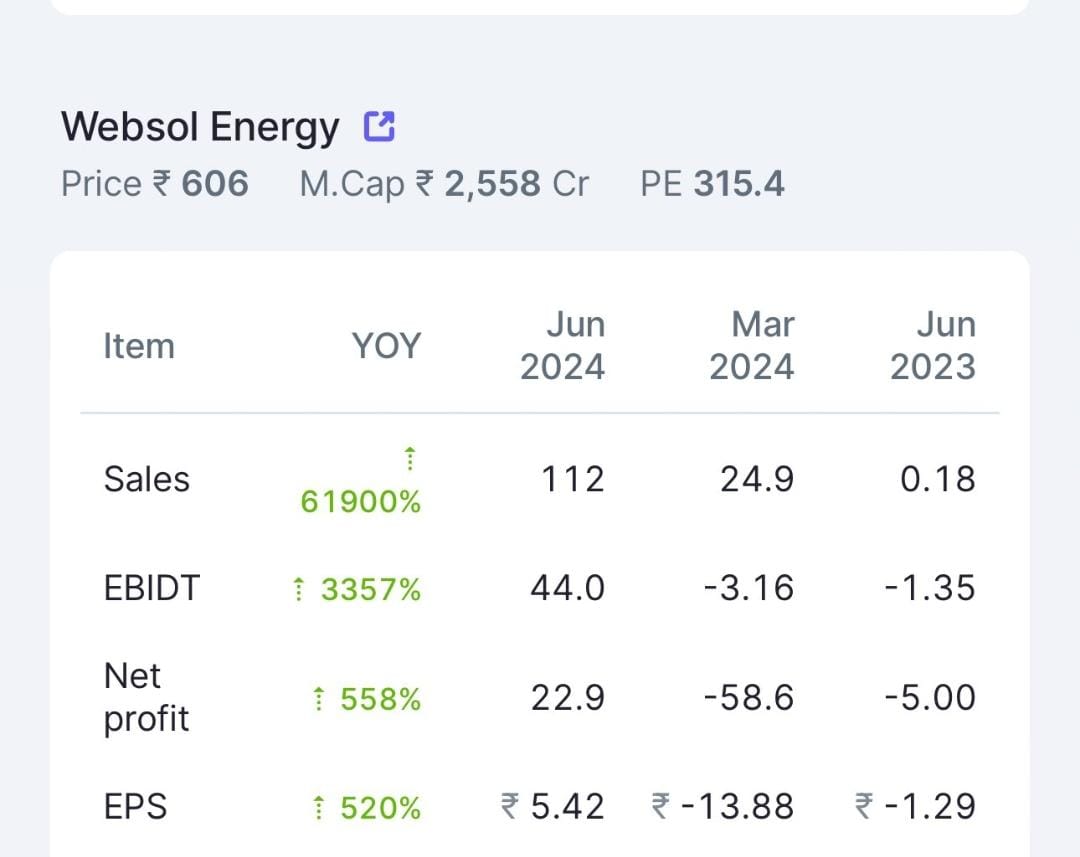

Websol energy systems posted its results for Q4 FY 2024

Revenue reported at 25 cr roughly for 1.5 operational months, this translates to roughly 325-350 cr. for FY2025 from one plant. The other plant should be operational by July. Their Operating profit is a mess, but ongoing CapEx will further help drive sales growth. Debt has also increased but the main point of worry remains operating profit. If we exclude depreciation entirely even then there is operating loss.

Impairment of assets also led to a decline net profit for the year.

Q1 and Q2 will give us a better picture of where the company is headed.

Hoping to learn more from everyone else’s views

Irrespective of short term price action. It’s clear that we should be sitting at 100cr annual PAT with the current capacity only. Get your valuations hat on. It’s a 10,000 cr mcap company 18 months down the line. Atleast.

4x from here.

Assuming the capex will rampup to 2.4gw by next CY 2025 December. And the company will further have aspirations to double the capacity.